Introduction

Before an NRI can invest a single rupee in Indian mutual funds, one process must be completed first: KYC. It is the mandatory identity and address verification process that Non-Resident Indians and OCIs must complete before any mutual fund transaction can be initiated or processed.

This is not optional paperwork. SEBI mandates KYC for all securities market participants under its Master Circular on KYC norms (SEBI/HO/MIRSD/SECFATF/P/CIR/2023/169), while RBI's Master Direction on KYC extends the requirement across all financial institutions. For NRIs specifically, FEMA adds another layer — governing how money moves and is invested across borders.

That regulatory density is exactly why many NRIs delay their investment journey — the KYC process feels opaque before you've been through it once.

This guide covers what you actually need to know:

- Exact document requirements for NRIs and OCIs

- How attestation works when you're outside India

- What FATCA declarations require and why

- Common mistakes that cause applications to stall

Key Takeaways

- NRI KYC is a one-time mandatory process required by SEBI and RBI before investing in any Indian mutual fund

- Self-attest and submit your passport, PAN card, overseas address proof, NRI status proof, and a recent photograph

- KYC completed through any SEBI-registered KRA is valid across all AMCs — no repetition required per fund house

- Switching residency status (resident to NRI or vice versa) requires an explicit KYC update — your existing resident KYC will not carry over

- US and Canada-based NRIs must submit a FATCA declaration and can only invest through AMCs that are explicitly FATCA-compliant

What Is the NRI KYC Process?

KYC — Know Your Customer — is the regulatory verification process through which financial institutions confirm an investor's identity, residential address, and residency status before allowing them to invest.

For NRIs, the scope goes further. KYC also verifies cross-border compliance under FEMA, since NRI investments in Indian mutual funds are governed by Schedule 5 of the Foreign Exchange Management (Non-debt Instruments) Rules, 2019.

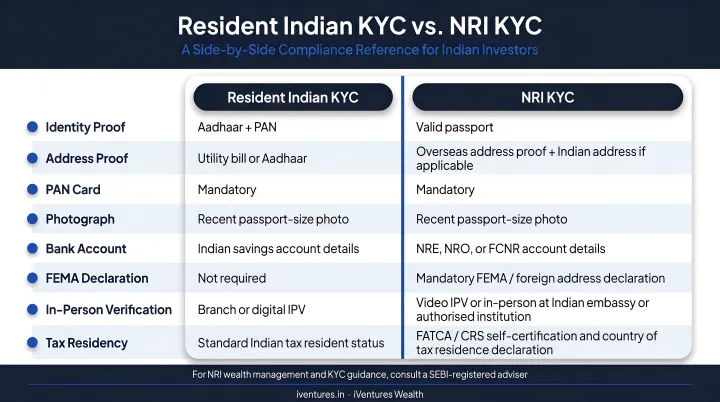

How NRI KYC Differs from Resident KYC

This distinction matters practically: mismatched documentation is one of the most common reasons NRI applications are rejected or delayed at the KYC registration agency level.

| Requirement | Resident Indian KYC | NRI KYC |

|---|---|---|

| Identity proof | Aadhaar, PAN, or other OVD | Valid Indian passport (primary) |

| Address proof | Indian address | Overseas address proof required |

| NRI status proof | Not required | Mandatory (visa, OCI card, work permit) |

| Third-party attestation | Not typically required | Required for offline physical submissions |

| FATCA declaration | Not applicable | Required for US/Canada tax residents |

According to AMFI's individual KYC application form, non-residents and foreign nationals must submit passport/PIO/OCI documentation and overseas address proof, subject to RBI and FEMA guidelines. A resident KYC record does not automatically satisfy these requirements. NRIs who relocate abroad without updating their KYC status often find existing folios frozen or new applications rejected until the correct documentation is submitted.

Documents Required for NRI KYC

Documents fall into four categories: identity proof, NRI status proof, address proof, and photograph. All copies must be self-attested before submission. Offline physical submissions require additional third-party attestation (covered below).

Identity Proof

A valid Indian passport (front and back pages) is the primary and most widely accepted identity document. Persons of Indian Origin may also use a foreign passport combined with an OCI card, though acceptance varies by AMC.

NRI Status Proof

This is the most commonly missed document. A passport alone does not prove NRI status. You must separately provide one of the following:

- Valid visa or work permit for the country of residence

- Residence permit issued by the foreign government

- OCI card (for Persons of Indian Origin)

- Mariner's declaration or certified CDC copy (for Merchant Navy NRIs)

Address Proof

Two types may be needed:

Overseas address proof (mandatory):

- Recent utility bill — per AMFI's KYC form, utility bills used as deemed proof of address must not be more than 2 months old

- International bank statement or passbook — CVL KRA specifies this should not be more than 3 months old

- Foreign government-issued residence permit

Indian address proof (optional but helpful):

- Aadhaar card, utility bill, or rental agreement — not mandatory but facilitates smoother processing with some AMCs

Note: Document recency requirements are document-type and KRA-specific, not a universal SEBI rule. Check with your KRA or AMC for their specific requirements.

PAN Card and Photograph

PAN is mandatory for all mutual fund investments for tax compliance purposes. Under Income Tax Rule 114B, transactions above ₹50,000 require PAN; in its absence, Form 60 must be submitted.

A recent passport-sized colour photograph must also accompany your KYC form — keep 2–3 copies ready, as different AMCs may ask for them separately.

Attestation Requirements

For offline/postal submissions, self-attestation alone is not sufficient unless you present original documents in person. Per AMFI's official KYC form, authorised attestors include:

- Indian Embassy or Consulate General in the country of residence

- Notary Public

- Court Magistrate or Judge

- Overseas branches of Indian Scheduled Commercial Banks registered in India

These authorised parties can also conduct In-Person Verification (IPV) and record it directly on the KYC form, combining both steps in a single visit.

How the NRI KYC Process Works: Step-by-Step

The end-to-end flow: check existing status → gather documents → choose your submission channel → complete FATCA if applicable → await confirmation.

Step 1: Check Your Existing KYC Status

Before starting, check whether you already have a KYC record. Enter your PAN on the portal of any SEBI-registered KRA:

Your status will show as KYC Validated, KYC Registered, KYC On-Hold, or Rejected — along with whether you're marked as "Resident" or "NRI." If you're marked as Resident but now live abroad, proceed to Step 2 before attempting any investment.

Step 2: Gather and Prepare Your Documents

Collect all documents across the four categories above. Before submitting:

- Sign and date every copy (self-attestation)

- Arrange third-party attestation if submitting offline without original verification

- Ensure scanned copies are legible and in accepted file formats if submitting digitally

- Verify document recency — expired or outdated proofs are among the most common rejection reasons

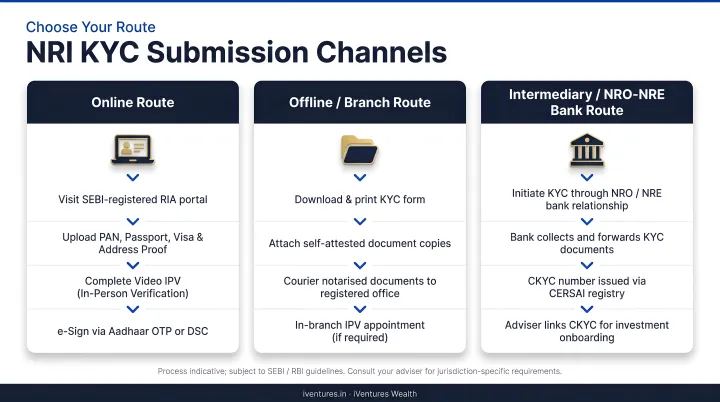

Step 3: Choose Your Submission Channel

Three routes are available:

Online/Video KYC — the preferred route for NRIs abroad. Documents are uploaded digitally and identity is verified via a live video call with the intermediary's representative. SEBI circular SEBI/HO/MIRSD/DOP/CIR/P/2020/73 (April 24, 2020) formally permits this technology-enabled KYC route. Note that it does not eliminate document requirements — it replaces in-person verification only.

Through a mutual fund intermediary — an AMC, SEBI-registered distributor, or SEBI-registered investment adviser can facilitate document verification. For NRIs working with a SEBI-registered adviser like iVentures Wealth (SEBI RIA No. INA000019026), the process is handled end-to-end, which is especially practical for US/Canada-based NRIs navigating FATCA requirements alongside standard KYC. Documentation support is included, and onboarding typically completes within 7–10 business days of submission.

Offline/postal submission — KYC form plus properly attested documents mailed to the AMC or KRA's India office. Used when online options are unavailable, but typically the slowest route.

Step 4: Submit Your FATCA/CRS Declaration (If Applicable)

This is a separate step from KYC. Skipping it will block investment even after KYC is approved.

NRIs who are tax residents of the US must submit a FATCA declaration. Per SEBI circular SEBI/HO/MIRSD/SECFATF/P/CIR/2024/12 dated February 20, 2024, FATCA/CRS certifications are now centralised at KRAs.

Required declaration fields include:

- Country of tax residence

- Tax Identification Number (TIN) or functional equivalent

- Country and city of birth

- Citizenship/nationality

NRIs from other CRS-covered countries face the same requirement. India's income tax rules 114F, 114G, and 114H govern due diligence and reporting obligations for financial institutions, with AMFI Best Practice Circular 63 (September 16, 2015) providing implementation guidance.

Step 5: Await Verification and Confirmation

Once submitted, the KRA processes and validates your documents. If everything is in order, KYC is registered and confirmation is sent. If discrepancies exist — expired documents, missing attestation, illegible scans — you'll be notified by email to resubmit.

Once confirmed, your KYC is valid across all AMCs — you do not repeat the process for each new fund house. That said, you must update your KRA record whenever your address, residency status, or other KYC details change.

One important restriction: per SEBI's KYC FAQ, clients with KYC On-Hold or Rejected status cannot transact in the securities market until deficiencies are resolved.

Common Mistakes and Misconceptions About NRI KYC

Resident KYC Does Not Cover NRI Status

A common but costly assumption: that existing resident Indian KYC continues to work after you become an NRI. It does not. Once your residency changes, your KYC record must be explicitly updated to reflect NRI status using the AMFI KYC change form. Failing to do this means your mutual fund transactions may be flagged or rejected outright.

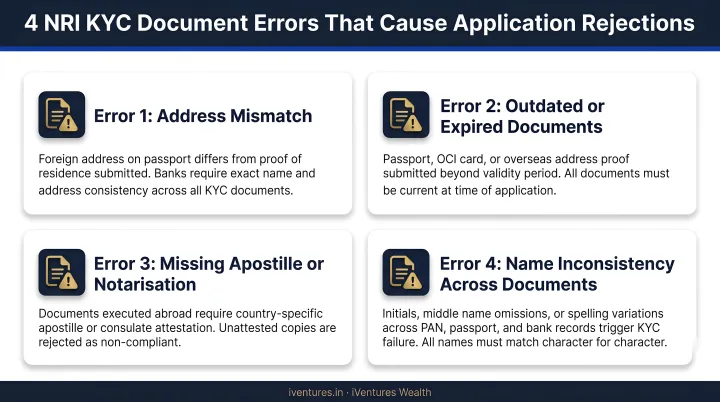

Document Errors That Cause Rejections

Several document errors consistently lead to KYC rejections:

- Submitting overseas address proof that exceeds the recency limit (utility bills older than 2 months, bank statements older than the KRA's specified period)

- Not including NRI status proof separately from the passport — they are distinct requirements

- Assuming self-attestation is sufficient for physical offline submissions where third-party attestation is actually required

- Submitting illegible or low-resolution scanned copies when using digital channels

The US/Canada Misconception

Many NRIs from these countries believe they cannot invest in Indian mutual funds at all. They can — but only through AMCs that are FATCA and CRS compliant. Not every fund house accepts subscriptions from US or Canada-based NRIs.

Officially confirmed examples of AMCs that accept US/Canada-based NRI subscriptions include:

- SBI Mutual Fund: US/Canada investors can purchase units offline

- PPFAS Mutual Fund: accepts subscriptions when the investor is physically present in India at the time of transaction

- NJ Mutual Fund: SAI confirms US and Canada-based NRI/PIO subscriptions are accepted, subject to stated conditions

AMC policies on this change without notice. Verify current acceptance directly with the fund house or a SEBI-registered adviser before proceeding.

Conclusion

NRI KYC is a one-time process. Once completed through any SEBI-registered KRA, it unlocks investing across all AMCs in India — no repetition required per fund house. The barriers that slow most NRIs down are document preparation (particularly attestation when abroad) and not understanding that resident KYC and NRI KYC serve different regulatory purposes.

Staying compliant beyond initial registration means updating your KYC if your residency or address changes, and ensuring your FATCA declaration remains current. An outdated or mismatched KYC record can freeze investments already made — not just block new ones.

For NRIs managing US or Canada tax obligations, multi-country residency, or ₹5 Crore or more in investable assets, KYC is the starting point — not the full picture. Compliance, fund selection, DTAA structuring, and currency management each interact with the others, and handling them in isolation tends to create gaps.

iVentures Wealth (SEBI RIA No. INA000019026) works with NRIs on this as a single coordinated mandate — so KYC, cross-border tax planning, and portfolio decisions are sequenced and aligned from the outset rather than treated as separate tasks.

Frequently Asked Questions

How do I complete NRI KYC for mutual funds?

Submit your passport, PAN card, overseas address proof, NRI status proof, and photograph through video KYC, a registered AMC/distributor, or by posting attested documents to a KRA's India office. Once registered with any SEBI-registered KRA, your KYC is valid across all mutual fund investments — no need to repeat it per fund house.

What are the KYC documents required for NRI?

The core documents required are:

- Valid Indian passport and PAN card

- NRI status proof (visa, OCI card, or work permit)

- Overseas address proof (utility bill within 2 months, or bank statement per KRA guidelines)

- Recent passport-sized colour photograph (self-attested)

Indian address proof is optional but can be helpful. All copies must be self-attested.

What is the SEBI circular governing NRI KYC?

The primary governing document is SEBI's Master Circular SEBI/HO/MIRSD/SECFATF/P/CIR/2023/169 (October 12, 2023), which consolidates KYC norms for all securities market participants. Supplementary circulars cover KRA risk management (August 2023) and FATCA/CRS centralisation at KRAs (February 2024).

Who can certify KYC documents for NRI?

Per AMFI's official KYC form, NRI documents can be attested by: the Indian Embassy or Consulate General in your country of residence, a Notary Public, a Court Magistrate or Judge, or overseas branches of Indian Scheduled Commercial Banks registered in India. These same parties may also conduct In-Person Verification.

Can NRIs from the US or Canada invest in Indian mutual funds?

Yes, but only with FATCA and CRS compliant AMCs — not all fund houses accept US or Canada residents. A FATCA declaration disclosing your country of tax residence, TIN, and citizenship details is required in addition to standard KYC. Verify AMC acceptance before applying, as some digital platforms may not support registration for these residents.

Is NRI KYC a one-time process?

Yes. KYC is completed once and maintained centrally by SEBI-registered KRAs, making it valid across all AMCs and mutual fund schemes. However, you must update your KYC record whenever key information changes — including your address, residency status, or contact details. An unresolved On-Hold or Rejected status will block transactions until the deficiency is corrected.