Introduction

Concentrating wealth within a single geography is a structural risk — not a conservative choice. For UHNIs, family offices, founders, and NRIs, global markets offer access to asset classes, sectors, and currencies that simply don't exist domestically at comparable scale.

Yet two problems persist. Many HNI investors under-allocate internationally because the frameworks feel unfamiliar. Others enter global markets without a structured strategy, leaving themselves exposed to currency volatility, regulatory complexity, and concentration risk.

This guide covers the main global investment strategies, why they matter for Indian wealth builders, and how to access them within the regulatory framework.

Key Takeaways

- Global strategies involve allocating capital across international markets, asset classes, and currencies for diversification and long-term growth

- Main approaches span passive (index funds, ETFs), active (mutual funds, hedge funds), and alternative strategies (REITs, private equity, commodities)

- Currency, geopolitical, and regulatory risks are manageable through diversification, hedging, and expert advisory

- Indian residents access global markets via RBI's LRS (up to USD 250,000/year), international mutual funds, and global brokerage platforms

- Global portfolios demand continuous monitoring and rebalancing, not a one-time setup

What Are Global Investment Strategies?

Global investment strategies involve the systematic allocation of capital across international markets — equities, bonds, real estate, commodities, and alternatives in various countries and regions — with the objective of diversification, risk management, and long-term capital growth.

Three terms worth distinguishing:

| Term | Meaning |

|---|---|

| Global investing | A worldwide mandate that may include the investor's home market |

| International investing | Allocating to markets outside the home country |

| Offshore investing | A domicile or account-structure question; for Indian residents, must be tested against FEMA, LRS, and reporting rules |

The Spectrum of Approaches

Strategies range from fully passive (tracking a global index) to actively managed (selecting securities to outperform benchmarks). Target markets span:

- Developed markets — US, Europe, Japan — for stability and blue-chip exposure

- Emerging markets — select Asian and Latin American economies — for higher growth at higher risk

- Frontier markets — high-risk, high-reward opportunities for a small satellite allocation

Institutional investors — pension funds, sovereign wealth funds — have used these strategies for decades. Norway's Government Pension Fund Global (NOK 21,478 billion in assets) is a useful reference point: a rules-based pool spanning equities, fixed income, real estate, and infrastructure, built to perform across market cycles.

Indian HNIs and family offices can apply the same allocation logic at their own scale, structuring portfolios that span asset classes and geographies rather than concentrating in a single market.

Why Global Investing Is Now Accessible

Digital brokerage platforms, cross-listed ETFs, and India's Liberalised Remittance Scheme have opened international markets to individual investors. For Indian HNIs and NRIs, this means global diversification — once the domain of institutional desks — is now a practical portfolio tool, not an aspirational one.

Key Types of Global Investment Approaches

Passive Global Strategies

Global index funds and ETFs track international benchmarks — the MSCI World Index (1,308 constituents across 23 developed markets), the MSCI Emerging Markets Index, or the S&P 500 — providing broad, low-cost exposure to hundreds of companies across geographies and sectors.

The cost advantage is significant. Vanguard's S&P 500 ETF (VOO) carries a 0.03% expense ratio on USD 1.6 trillion in net assets. Morningstar data shows traditional index funds average 0.09% in fees versus 0.57% for active funds — a gap that compounds materially over time.

One important caveat: the MSCI World Index is 72.45% US-weighted with 30.66% in information technology as of May 2026. A single developed-market ETF is not geographic diversification — it is primarily US tech exposure.

Systematic investing (rupee- or dollar-cost averaging) into global ETFs builds international exposure gradually without trying to time volatile foreign markets. This approach suits founders, CXOs, and salaried professionals deploying regular surplus capital.

Active Global Strategies

Global mutual funds and separately managed accounts (SMAs) employ professional portfolio managers to select stocks worldwide with the goal of outperforming benchmarks. SMAs allow customisation based on the investor's specific risk profile and exclusion preferences — useful for UHNIs with concentrated positions or ESG requirements.

The cost is higher management fees in exchange for the potential of alpha — a trade-off the data scrutinizes closely:

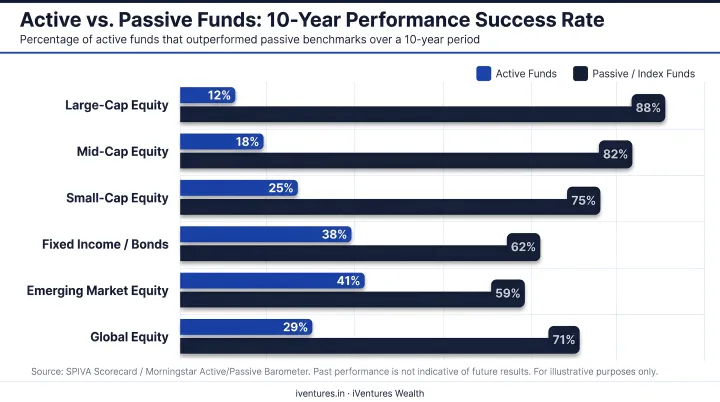

- Only 21% of active strategies survived and outperformed passive peers over 10 years through 2025, per Morningstar's Active/Passive Barometer

- Foreign-stock active funds fared slightly better at a 24% success rate

- Active mandates need a measurable, documented edge — not just brand reputation or AUM size

Global macro hedge funds and long/short equity strategies employ leverage, derivatives, currency positions, and cross-asset arbitrage. These target high absolute returns and are typically accessible only to UHNIs and institutional investors due to high minimums and regulatory complexity.

For UHNIs seeking exposure to this space, iVentures Wealth structures access to global hedge funds spanning long-short equity, macro, event-driven, and multi-strategy mandates — positioned as low-correlation complements within a broader portfolio, not standalone bets.

Alternative Global Strategies

Alternatives serve distinct portfolio roles beyond equities:

- Global REITs — The FTSE EPRA Nareit Global REITs Index covers 325 constituents with USD 1.77 trillion in net market cap and a 4.03% dividend yield. Nareit reports over 1,000 listed REITs globally. Liquid, income-generating real estate exposure without direct property underwriting

- Commodities — Gold, oil, and agricultural products as inflation hedges; the World Gold Council notes gold is a long-term inflation hedge though less reliable over short horizons

- Private equity and venture capital — High-growth exposure to disruptive global businesses; suitable as a satellite allocation for UHNIs with long time horizons and locked liquidity tolerance

Why HNIs and UHNIs Should Think Globally

Portfolio Diversification

Markets across geographies are not perfectly correlated. When Indian equity markets face headwinds, US or European markets may be performing differently — and vice versa. A genuinely diversified global allocation smooths portfolio volatility over a full market cycle.

Access to Sectors Unavailable Domestically

MSCI World allocates over 30% to information technology, with NVIDIA and Apple together exceeding 10% of the index. The S&P 500 provides deep exposure to sectors with no one-for-one domestic equivalent at comparable scale:

- Semiconductors — foundational to AI, defence, and automotive transformation

- Cloud platforms — hyperscalers driving enterprise infrastructure globally

- Global pharmaceuticals — innovation pipelines in oncology, genomics, and rare disease

- E-mobility — supply chains and battery technology reshaping transport

iVentures Wealth's CFA-led research team has specifically curated globally disruptive companies through low-cost international ETFs across these categories — sectors they categorise as "Dominators, Disruptors & Enablers."

Currency Diversification as a Structural Hedge

World Bank data shows the INR moved from approximately ₹61.03 per USD in 2014 to ₹83.67 per USD in 2024 — roughly 3.2% annualised depreciation. For a family with future USD expenses — offshore education, global philanthropy, or non-India succession assets — unhedged USD exposure is a liability-matching tool, not just a return bet.

That 3.2% annual erosion compounds meaningfully over a decade — making multi-generational wealth structuring in stable foreign jurisdictions not optional, but necessary.

Multi-Generational Wealth Creation

Global assets — real estate, offshore trusts, and equity holdings in stable jurisdictions — can be structured to transfer wealth across generations in a tax-efficient manner. For family offices and UHNIs, this structuring discipline matters more than near-term returns.

iVentures Wealth has structured cross-border arrangements for families with assets across India, the US, and the UK — creating unified, compliant frameworks for inheritance and succession that hold across jurisdictions.

Risks in Global Investing and How to Manage Them

Currency and Market Risk

Currency risk works simply: when an Indian investor holds a US stock and the dollar weakens against the rupee, returns shrink even if the stock price holds. The reverse also applies — INR depreciation amplifies USD-denominated returns.

Mitigation approaches:

- Currency-hedged funds — remove exchange rate volatility from overseas equity exposure

- Forex forward contracts — lock in exchange rates for specific transactions

- Natural hedges — for NRIs with foreign-currency liabilities, unhedged USD assets can match exposure

iVentures structures portfolios across all three approaches — fully unhedged, partially hedged, or fully hedged — based on portfolio size and currency outlook.

Currency risk is only part of the equation. Market volatility in emerging and frontier markets can be sharp and rapid — driven by capital flight, commodity shocks, or local political events. A barbell approach works well here: pair higher-volatility emerging market allocations with the relative stability of developed market equities and investment-grade bonds.

Geopolitical and Regulatory Risk

Geopolitical risk is not theoretical. On 28 February 2022, the Bank of Russia halted trading on MOEX equity and derivatives markets. MSCI subsequently reclassified Russia from Emerging Markets to Standalone status at an effectively zero price.

Investors in Russia-heavy EM funds lost that allocation entirely — not to volatility, but to market access disappearing overnight.

The lesson: cap single-country exposure, use diversified EM funds rather than country-concentrated positions, and understand custodial arrangements.

Regulatory and tax complexity adds another layer. Each jurisdiction carries different:

- Foreign investment restrictions

- Capital gains tax treatment

- Withholding tax rates on dividends

- Reporting obligations

For Indian investors specifically, this means FEMA compliance, DTAA benefit claims, TCS implications under LRS, and Schedule FA disclosures in annual tax returns. Navigating this landscape requires advisors who understand both Indian regulations and international frameworks — not just domestic wealth managers who treat global investing as an add-on.

The Indian Investor's Angle on Global Markets

The LRS Gateway

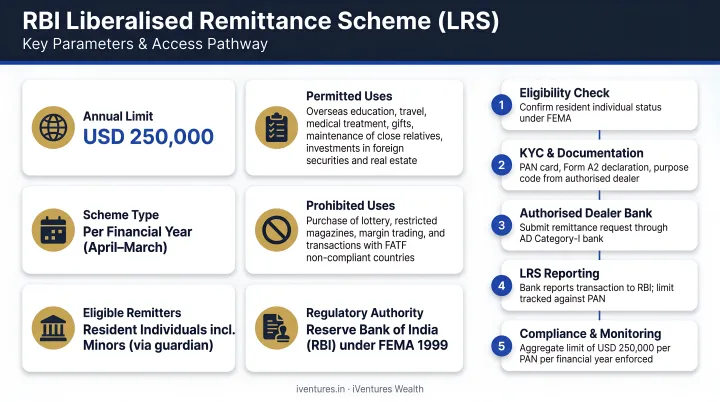

The RBI Liberalised Remittance Scheme (LRS) is the primary regulatory pathway for resident Indians. Key parameters:

- Limit: USD 250,000 per resident individual per financial year

- Permitted uses: Foreign equities, ETFs, bonds, bank deposits, and real estate

- TCS: Raised from 5% to 20% for non-exempt LRS remittances above ₹10 lakh (effective October 1, 2023). TCS is recoverable against tax liability but creates cash-flow friction — model this before remitting

For NRIs and OCIs, different rules apply. They are not subject to LRS limits and can invest through NRE/NRO accounts or overseas brokerage accounts in compliance with FEMA regulations.

Domestic Vehicles Providing Global Exposure

Investors who prefer not to remit under LRS can access international markets through domestic wrappers:

- International mutual funds and feeder funds registered with SEBI (examples include Mirae Asset NYSE FANG+ ETF FoF and Franklin U.S. Opportunities Equity Active FoF)

- Domestic ETFs tracking global indices such as the Nasdaq 100 or S&P 500

- Fund of Funds structures providing diversified global exposure in a single domestic product

One important constraint: SEBI's 2021 circular capped the overseas mutual fund industry at USD 7 billion for overseas securities and USD 1 billion for overseas ETFs. AMFI subsequently froze each AMC at its February 1, 2022 exposure level. Several schemes remain closed to fresh subscriptions — always verify current status before relying on a domestic international fund.

Where iVentures Fits

FEMA compliance, DTAA optimisation, TCS planning, and portfolio construction across geographies are not tasks most investors should tackle independently. Each layer adds regulatory complexity — and a misstep in any one of them can cost more than the diversification benefit itself.

iVentures Wealth (SEBI-registered RIA since 2010) manages the full process for UHNIs, family offices, NRIs, and OCIs: account setup with SEC and FCA-regulated international custodians, LRS declarations, TCS compliance, fund transfers, and consolidated portfolio reporting in both USD and INR. From initial engagement to first investment typically takes 7–10 business days.

Frequently Asked Questions

What are the five investment strategies?

The five widely recognised strategies are: growth investing (targeting above-average earnings growth companies), value investing (buying undervalued assets), income investing (focusing on dividends and interest), index investing (passive benchmark tracking), and buy-and-hold (holding quality assets through market cycles). Most global portfolios combine elements from multiple strategies.

What is Warren Buffett's 70/30 rule?

Buffett's 2013 letter recommended 90% in a low-cost S&P 500 index fund and 10% in short-term government bonds; the "70/30" variation (70% equities, 30% bonds) is a popular adaptation. His core message emphasises low-cost, long-term, passive investing — not a universal prescription for Indian UHNIs with cross-border tax and estate considerations.

What is the difference between active and passive global investment strategies?

Passive strategies (global index funds, ETFs) replicate a market benchmark at low cost with minimal management intervention. Active strategies involve portfolio managers making deliberate security selection and timing decisions to outperform the benchmark — typically at higher fees. Research consistently shows most active managers fail to beat passive peers net of fees over 10-year periods.

How can Indian investors access global markets?

Three main routes are available:

- RBI LRS — up to USD 250,000/year for direct investment in foreign equities and assets

- SEBI-registered international mutual funds, feeder funds, and domestic ETFs tracking global indices (subject to SEBI/AMFI subscription limits)

- NRIs and OCIs — direct investment via international brokerage accounts linked to NRE/NRO accounts, without LRS caps

What are the main risks of investing in global markets?

Four primary risks to account for:

- Currency fluctuation — exchange rate movements affecting INR returns

- Geopolitical and regulatory risk — policy reversals, sanctions, or market closures (as seen with Russia in 2022)

- Market volatility — particularly pronounced in emerging markets

- Tax and compliance complexity — navigating rules across multiple jurisdictions

All are manageable through diversification, selective hedging, and advisors experienced in cross-border investment frameworks.