Key Takeaways

- Women face a triple gap—longer lifespan, lower earnings, and career interruptions—making early, structured investing essential to long-term financial security.

- India offers women-focused instruments across risk profiles: SIPs, PPF, ELSS, NPS, and Sovereign Gold Bonds each serving different goals across safety, tax efficiency, and growth.

- A life-stage approach beats a static strategy: your asset mix should evolve as your life circumstances change.

- A SEBI-registered, fiduciary adviser provides guidance aligned to your goals—not to commission-driven product sales.

Why Women in India Need a Distinct Investment Approach

Most Indian women save diligently. Few invest strategically. That gap is expensive—and for women specifically, the cost compounds over decades in ways that rarely get discussed directly.

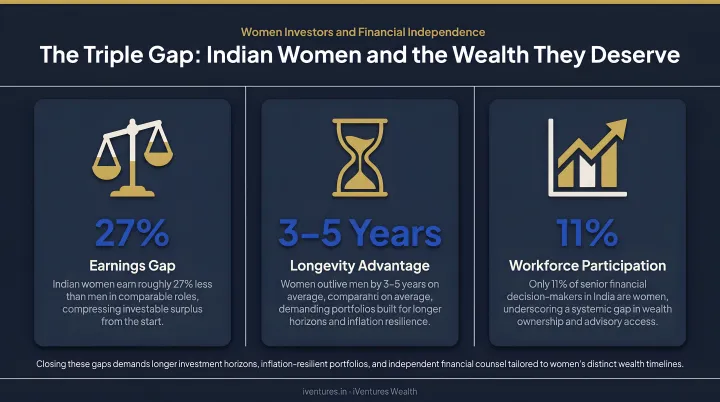

The Triple Gap

Three structural realities make investing more urgent for women than men:

- Earnings gap: PLFS 2023-24 data shows salaried women earn ₹17,034/month on average versus ₹22,375 for men. For the self-employed, this gap widens further—₹5,803 versus ₹16,723.

- Longevity gap: World Bank data shows Indian women live to 73.9 years on average, nearly three years longer than men. A longer life requires a proportionally larger retirement corpus—that difference needs to be planned for, not assumed away.

- Participation gap: Female labour force participation stands at just 32.4%, meaning more women face interrupted income timelines—through caregiving, relocation, or family responsibilities.

Each gap individually is manageable. Together, they create a compounding deficit that only strategic investing can close.

The Savings Trap

Keeping money in a savings account feels safe, but the numbers tell a different story. SBI's savings rate currently stands at 2.50% p.a., while India's CPI inflation ran at 3.93% provisional as of May 2026—meaning your savings account loses purchasing power every year it sits idle.

What this looks like in practice:

| Instrument | Approximate Return | Real Return (post-inflation) |

|---|---|---|

| Savings account | 2.50% p.a. | –1.43% p.a. |

| Fixed deposit (1-year) | ~6.5–7.0% p.a. | +2.57–3.07% p.a. |

| Equity mutual funds (long-term avg.) | ~11–13% p.a. | +7–9% p.a. |

Fixed deposits do better than savings, but not by enough. Over a 25-year retirement horizon, even a 1–2% annual shortfall against inflation steadily shrinks your real purchasing power.

Women Are Actually Better Investors—Once They Start

A 2018 Warwick Business School analysis of 2,800 investors found women outperformed men by 1.8% over time. Men were more likely to trade speculatively and react to short-term noise. Women's tendency toward patience and consistency is an investing advantage—it's the lack of a starting point, not capability, that holds most women back.

The Compounding Case for Starting Early

Consider this: investing ₹5,000/month starting at age 25, assuming 12% annualised returns, builds roughly ₹1.76 crore by age 60. Starting the same SIP at age 35 produces approximately ₹52 lakh—less than a third, for the same monthly commitment. Ten years of delay costs over ₹1.2 crore. That's the real price of waiting.

Best Investment Options for Women in India

There's no single "best" instrument—the right choice depends on your age, risk tolerance, tax situation, and goals. Here's how the main options compare:

Mutual Funds via SIP

SIPs (Systematic Investment Plans) are the most accessible entry point for most women. You can start with as little as ₹500/month, automate contributions, and access professionally managed, diversified portfolios.

- Equity mutual funds: Higher growth potential, suited for 5+ year horizons

- Debt mutual funds: More stable, appropriate for shorter timeframes or conservative risk profiles

- ELSS (Equity Linked Savings Scheme): Equity growth plus a Section 80C deduction of up to ₹1.5 lakh/year, with the shortest lock-in of any tax-saving instrument—just 3 years

As of March 2025, 1.38 crore women were mutual fund investors—just 25.91% of total unique investors, per AMFI's Annual Report FY2025. There's significant room for more women to participate.

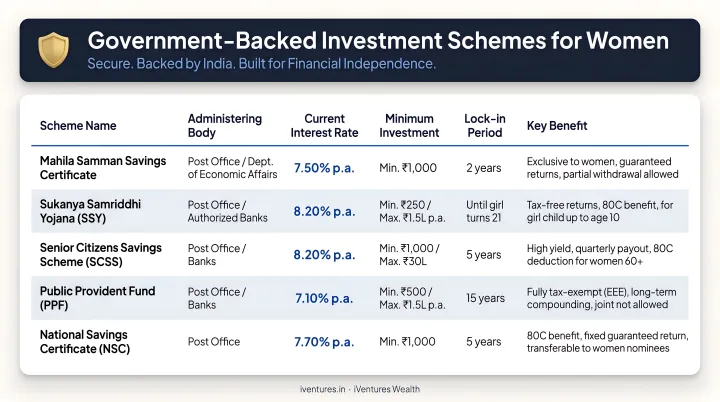

Government-Backed Schemes

These are the foundation layer—low risk, high trust, and government-guaranteed:

| Scheme | Interest Rate | Key Benefit |

|---|---|---|

| PPF | 7.1% p.a. | Tax-free returns, 80C deduction, 15-year lock-in |

| Sukanya Samriddhi Yojana | 8.2% p.a. | For girl children under 10, fully tax-exempt |

| NPS | Market-linked | 80CCD(1B) gives additional ₹50,000 deduction |

| SCSS | 8.2% p.a. | For 60+, quarterly interest payout |

Rates are reviewed quarterly—verify current rates before investing.

SSY deserves special mention: with 2.73 crore accounts opened and nearly ₹1.19 lakh crore in deposits as of 2021, it's proven and widely trusted. For any mother of a daughter below 10, this should be a priority.

Sovereign Gold Bonds

Gold is a meaningful part of many Indian portfolios, but physical gold carries real costs. Sovereign Gold Bonds (SGBs) give you full price exposure without the storage risk, making charges, or purity concerns of physical holdings.

SGBs offer 2.50% fixed annual interest in addition to gold price appreciation, and are backed by the Government of India. Gold ETFs offer a similar digital-gold exposure with greater liquidity if you prefer a fund structure.

Equities and Real Estate

For women building a mature, long-term portfolio:

- Direct equities (via DEMAT account) offer the highest growth potential but require risk tolerance and a 5+ year horizon

- Real estate provides tangible ownership and rental income, though it demands significant capital and is far less liquid than financial instruments

Both work best layered on top of a core portfolio of mutual funds and government schemes. Once that base is established, equities and real estate can meaningfully increase growth potential and income diversification.

A Life-Stage Investment Roadmap for Women

Each decade brings different financial priorities. This roadmap breaks down what to focus on — and what to protect — at every stage.

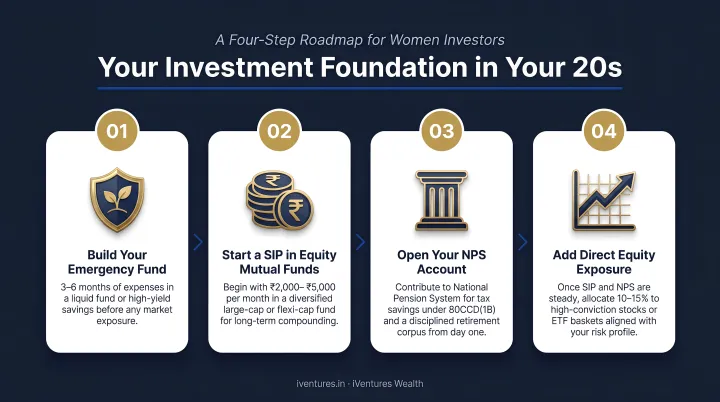

Your 20s: Build the Foundation

This decade carries the most powerful investing advantage available: time.

- Build a 3–6 month emergency fund first — before investing anything

- Start a SIP in an equity mutual fund or ELSS — even ₹1,000/month compounds significantly over 35 years

- Enrol in NPS from your first job — the earlier you start, the less painful it is later

- Prioritise growth: with 35+ years ahead, you can afford equity-heavy allocation

Starting a ₹5,000/month SIP at 25 versus 35 can mean a difference of over ₹1 crore at retirement. That gap is why this decade matters more than any other.

Your 30s: Balance Growth With Protection

This decade often involves marriage, children, career peaks, and competing financial demands simultaneously.

- Keep equity SIPs running—don't pause them for lifestyle inflation

- Add term life insurance (not investment-linked products)

- Open a PPF account for stable, tax-free compounding

- Start SSY if you have a daughter below 10

- Maintain financial independence within a joint household—investments in your own name matter

Your 40s: Rebalance Toward Stability

Retirement is no longer abstract. The 40s are when portfolio construction becomes more deliberate.

- Gradually shift allocation from equity-heavy toward a balanced equity-debt mix

- Introduce debt mutual funds or SCSS as stability anchors

- Review and update nominees across all instruments

- Get a proper will drafted—not a future task, a current priority

- Review health insurance coverage—this decade is often when gaps become expensive

Your 50s and Beyond: Plan the Drawdown

Accumulation gives way to distribution. The question shifts from "how do I grow this?" to "how do I make this last?"

- Systematic Withdrawal Plans (SWPs) from mutual funds provide regular income while keeping capital invested

- SCSS offers predictable quarterly payouts at 8.2% for senior citizens

- Annuities provide guaranteed lifetime income—useful for the portion of corpus requiring certainty

- Plan for 25–30 years of retirement, not 10–15—women's longevity data demands this

Practical Tips to Start Investing With Confidence

Start With One Goal, One Product

Decision paralysis is real. Don't wait until you understand everything before starting. Pick one goal — retirement, a passive income corpus, or a child's future — and begin building a portfolio anchored to that objective with guidance from a qualified adviser. Progress over perfection.

Systematize Your Investment Discipline

When investments move automatically — on a fixed date, to pre-agreed allocations — the decision is already made before you second-guess it. A structured investment plan tied to cash flow removes emotion from the equation. Consistency, more than any single market call, drives long-term results.

A few ways to build that discipline:

- Link investment triggers to income events (salary credit, business distributions, dividend receipts)

- Set asset-class targets upfront so rebalancing is rule-based, not reactive

- Work with your adviser to automate rebalancing when allocations drift beyond a set threshold

Review Annually, Not Daily

Checking your portfolio daily produces anxiety, not returns. An annual review with a financial adviser is enough to assess alignment with goals and rebalance if needed. Market noise is not information. Respond to changes in your life — income, goals, timeline — not to short-term market movement.

How to Choose the Right Investment Partner

What a SEBI-Registered Adviser Actually Means

Under SEBI's Investment Advisers Regulations, a registered investment adviser (RIA) is legally required to act in a fiduciary capacity—putting your interests first. They cannot accept commissions from product manufacturers, which structurally eliminates the incentive to mis-sell.

A commission-based distributor earns more when you buy certain products or switch funds. A fee-only RIA earns a transparent fee from you, and that's it. That distinction shapes every recommendation they make.

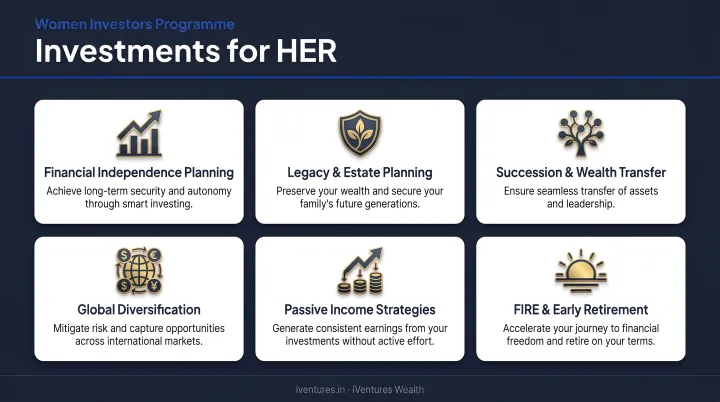

iVentures Wealth (SEBI Registration INA000019026) operates on exactly this model. Their dedicated "Investments for HER" programme specifically addresses the planning nuances women face—longer retirement horizons, career break structuring, emergency fund planning, and estate integration.

With 20+ years of experience, a CFA-led research team, and ₹1,146+ crore in assets under advice, the firm's fiduciary approach means every recommendation is built around your goals.

Questions to Ask Before Choosing an Adviser

Before signing on with any adviser, ask these directly:

- Are you SEBI-registered as an RIA? Ask for their registration number and verify it on the SEBI intermediary list.

- How are you compensated? Fee-only (charged to you) versus commission (paid by product manufacturers) is a fundamental difference.

- Can you share a sample financial plan for someone in my life stage? A competent adviser should be able to walk you through what a plan actually looks like—not just a pitch deck.

- How often will we review my portfolio, and what triggers an off-cycle review? You want regular scheduled reviews plus proactive contact when markets or your life circumstances shift materially.

Frequently Asked Questions

Which investment is best for women?

No single investment fits every situation — age, income, risk tolerance, and goals all shape the answer. For most Indian women, a combination of SIPs in equity mutual funds, PPF, ELSS, and Sovereign Gold Bonds covers growth, stability, tax efficiency, and inflation protection across different time horizons.

How do you double ₹10 lakhs in 5 years?

Using the Rule of 72, doubling in 5 years requires approximately 14.4% annualised returns. Equity mutual funds or a diversified equity portfolio can achieve this over time, but it comes with meaningful risk and is never guaranteed. Align this goal with a financial adviser before committing.

What is the 3-6-9 rule of money?

It's a personal finance framework: keep 3 months of expenses as a basic emergency fund, 6 months for a more comfortable buffer, and use the equivalent of the 9th month's amount to start investing. The logic is simple: build financial security before moving to aggressive wealth-building.

How much should a woman invest per month?

There's no fixed number. A common rule of thumb is at least 20% of monthly income, but the right amount depends on your expenses, debts, and goals. Starting with ₹500–₹1,000/month via SIP is far better than waiting for the "right" amount to materialise.

Is it safe for women to invest in mutual funds?

Mutual funds are regulated by SEBI, with daily NAV disclosures and monthly portfolio transparency. All investments carry some risk, but choosing reputable AMCs and matching fund type to your risk tolerance makes mutual funds a sound, accessible option for most investors.

Can a homemaker invest in India?

Yes. Homemakers can invest independently using a PAN card, a bank account, and completed KYC — which explicitly lists homemaker/housewife as a valid occupation. SIPs, PPF accounts, and DEMAT accounts can all be opened in a homemaker's name, building independent financial security.