Two things to establish immediately. First, India has no dedicated tax-free threshold exclusively for foreign income — it is taxed the same way as any domestic income. Second, your residential status under the Income Tax Act is the single most important factor determining how much foreign income you owe tax on.

Foreign income includes payments from foreign clients or employers, dividends from US stocks or foreign mutual funds, capital gains on foreign assets, rental income from overseas property, royalties, and interest from foreign deposits. If any of these apply to you, this guide covers what you need to know.

Key Takeaways

- There is no exclusive tax-free limit for foreign income — it is added to your total income and taxed at standard slab rates

- Your residential status (ROR, RNOR, or NRI) determines whether foreign income is taxable at all

- NRIs owe zero Indian tax on foreign income; RNORs get significant exemptions during their 2–3 year transition window

- Under the new tax regime (AY 2026-27), the Section 87A rebate makes total income up to ₹12 lakh effectively tax-free

- Filing Form 67 is mandatory to claim Foreign Tax Credit and avoid double taxation on foreign income

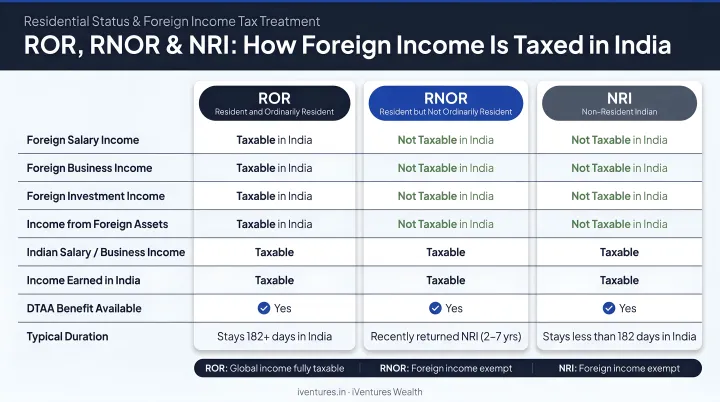

Residential Status and Its Impact on Foreign Income Taxability

India follows the residence rule of taxation: if you qualify as a tax resident, your global income is taxable here, regardless of where it was earned. The country where income originates taxes it under the source rule — India's claim comes on top of that, subject to treaty relief.

The Three Categories That Matter

The Income Tax Department's Non-Resident FAQ outlines the classification framework:

| Status | Who Qualifies | Foreign Income Tax Treatment |

|---|---|---|

| ROR (Resident and Ordinarily Resident) | Most individuals who have been living in India for several years | Worldwide income taxable — all foreign earnings included |

| RNOR (Resident but Not Ordinarily Resident) | Non-resident in 9 of the preceding 10 years, OR in India 729 days or fewer in the preceding 7 years | Foreign income exempt unless from a business controlled in India |

| NRI (Non-Resident Indian) | Does not satisfy Section 6 residency tests | Only India-source income taxable; foreign income fully exempt |

The Day-Count Tests

Residency is determined by physical presence:

- 182-day rule: Resident if present in India for 182 days or more in the relevant year

- 60+365 rule: Resident if present 60+ days in the current year AND 365+ days across the preceding 4 years

- 120-day rule: For Indian citizens or Persons of Indian Origin (PIOs) with Indian-source income exceeding ₹15 lakh, the 60-day condition shifts to 120 days

A special Deemed Resident provision under Section 6(1A) applies to Indian citizens with Indian-source income above ₹15 lakh who are not taxable in any other country — they are treated as residents but taxed like RNOR.

The RNOR Window: A Planning Opportunity Worth Timing Carefully

For returning NRIs, the RNOR classification typically applies for 2–3 years after resettling in India. During this period, foreign income that is neither received in India nor linked to an India-controlled business is generally exempt from Indian tax.

That window opens specific options worth acting on before ROR status takes effect:

- Realising foreign capital gains on overseas assets

- Liquidating foreign portfolios or unwinding offshore positions

- Timing the receipt of foreign income to fall within the exempt period

iVentures Wealth advises returning NRI clients on residential status analysis and coordinates this with broader portfolio restructuring decisions, helping them make the most of this limited window before worldwide taxation applies.

How Much Foreign Income Is Tax-Free in India?

The direct answer: there is no dedicated exemption threshold for foreign income alone.

Foreign income is added to your total income from all sources, and the combined figure is subject to standard exemption limits and slab rates. For AY 2026–27, those limits are:

- Old regime: Nil slab up to ₹2.5 lakh

- New regime: Nil slab up to ₹4 lakh

(Confirm these figures against the current Finance Act before filing.)

The Section 87A Rebate Effect

Under the new regime, resident individuals with total income up to ₹12 lakh pay zero net tax after the Section 87A rebate (up to ₹60,000). For salaried individuals, the ₹75,000 standard deduction extends this effective zero-tax threshold to ₹12.75 lakh. Both domestic and foreign income count toward this ₹12 lakh ceiling — so a returning NRI with mixed income sources needs to plan accordingly. Note that the rebate does not apply to special-rate income such as certain capital gains; confirm treatment with a tax advisor.

Two Genuinely Tax-Free Scenarios

Two residential status categories offer meaningful foreign income exemptions:

- RNOR (Resident but Not Ordinarily Resident): Foreign income not received in India and not from a business controlled in India is fully exempt — the most significant tax planning opportunity for returning NRIs.

- NRI (Non-Resident Indian): All foreign income is completely exempt. Only income earned, accrued, or deemed to accrue in India is taxable.

Foreign Gifts and Remittances

- Gifts from relatives abroad (as defined under Section 56(2)(x) — spouse, parents, siblings, lineal ascendants/descendants): fully exempt, no ceiling

- Gifts from non-relatives: tax-free only up to ₹50,000 per year combined; above this threshold, the entire amount becomes taxable as Income from Other Sources — not just the excess

- Inheritance under a will: fully exempt

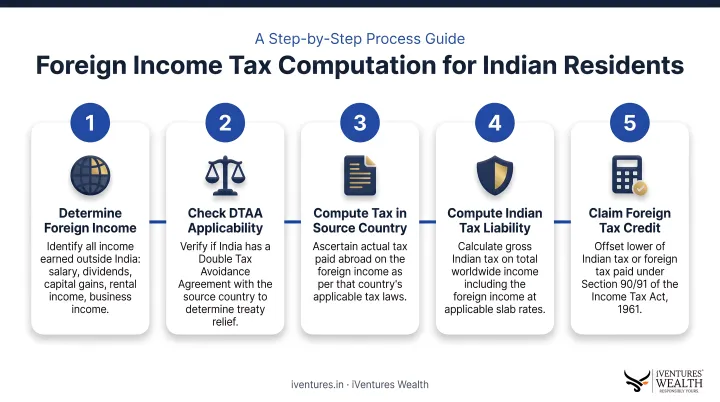

How Foreign Income Is Taxed: Slabs, Rates, and Calculation

Foreign income earned by a resident Indian is taxed as part of total global income — the process involves currency conversion, slab application, surcharge, and credit for taxes already paid abroad. Here's how it works in sequence.

Step-by-Step Tax Computation

- Convert foreign income to INR using the SBI telegraphic transfer buying rate on the applicable specified date under Rule 115 — the correct date varies by income category, so check Rule 115 carefully rather than defaulting to the date of receipt

- Add the INR equivalent to all other Indian income

- Apply slab rates under your chosen regime

- Add 4% Health and Education Cess on total tax plus surcharge

- Claim Foreign Tax Credit for any tax already paid abroad

Tax Slabs for FY 2025-26 / AY 2026-27

New Regime (default):

| Income Range | Rate |

|---|---|

| Up to ₹4 lakh | Nil |

| ₹4–8 lakh | 5% |

| ₹8–12 lakh | 10% |

| ₹12–16 lakh | 15% |

| ₹16–20 lakh | 20% |

| ₹20–24 lakh | 25% |

| Above ₹24 lakh | 30% |

Old Regime: Nil up to ₹2.5 lakh → 5% up to ₹5 lakh → 20% up to ₹10 lakh → 30% above ₹10 lakh.

(Always verify current slabs at incometaxindia.gov.in before filing.)

Surcharge for High-Income Earners

For UHNIs with large foreign portfolios, surcharge can materially increase the tax burden:

| Income Level | New Regime | Old Regime |

|---|---|---|

| ₹50L – ₹1 Cr | 10% | 10% |

| ₹1 Cr – ₹2 Cr | 15% | 15% |

| ₹2 Cr – ₹5 Cr | 25% | 25% |

| Above ₹5 Cr | 25% (capped) | 37% |

One important carve-out: the enhanced 25%/37% surcharge does not apply to income under Sections 111A, 112, and 112A, or to dividend income — surcharge on those categories is capped at 15%. On ₹5 Cr in foreign equity gains, for instance, the surcharge difference between 37% and 15% alone can amount to roughly ₹11 lakh in additional tax — making this a structuring consideration worth reviewing carefully.

Which ITR Form to File

- ITR-2: Individuals with foreign income, foreign assets, capital gains, or dividends but no business income

- ITR-3: Freelance or business/professional income from abroad

- ITR-4: Presumptive taxation under Section 44ADA (up to ₹50 lakh professional turnover) — but not available where foreign income or foreign assets need to be reported

- ITR-1: Generally not available to taxpayers with foreign income or foreign assets

Avoiding Double Taxation: DTAA and Foreign Tax Credit

How DTAA Works

India has signed Double Taxation Avoidance Agreements with a large number of countries. These agreements determine which country has primary taxing rights on specific income types and provide relief mechanisms to prevent the same income from being taxed twice. Claiming treaty benefits typically requires:

- A Tax Residency Certificate (TRC) from the foreign country

- Form 10F (or Form 41 under the Income Tax Act, 2025 materials) supplying prescribed particulars

Foreign Tax Credit Mechanism

The FTC allows you to offset Indian tax liability by the amount of tax already paid abroad on the same income. The credit is the lower of:

- Tax paid abroad (converted to INR), or

- Indian tax attributable to that foreign income

FTC is claimed by filing Form 67 under current rules, or Form 44 under the Income Tax Rules, 2026 (which specifies filing within 12 months from the end of the relevant tax year). Filing late can trigger denial or litigation. Courts including the Madras High Court have allowed FTC on delayed Form 67 filings in select cases, but relying on judicial relief is a risk not worth taking. File on time.

Managing FTC across multiple jurisdictions — US, UK, UAE, Singapore — requires tracking capital gains, dividend income, and foreign tax payments in parallel across tax years. For HNIs and NRIs with cross-border portfolios, iVentures Wealth helps structure investment holdings and coordinates with the client's chartered accountant to ensure FTC eligibility, Schedule FA disclosures, and documentation are addressed within the advisory framework well before ITR deadlines.

Key Compliance Requirements and Common Mistakes

Mandatory Disclosures for ROR Taxpayers

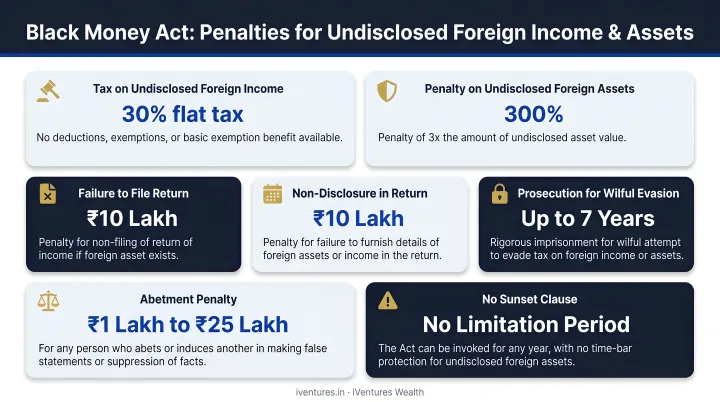

- Schedule FA (Foreign Assets): Requires disclosure of all foreign bank accounts, equity holdings, mutual funds, immovable property, and any account with signing authority. Non-disclosure carries a penalty of ₹10 lakh per year per undisclosed asset under the Black Money Act — this applies even if the asset generated no income in that year

- Schedule FSI (Foreign Source Income): Foreign income reported by country, type, and amount

- Schedule TR (Tax Relief): Summarises DTAA or unilateral relief claimed

The Black Money Act imposes tax at 30% on undisclosed foreign income, with a penalty equal to three times the tax — making the combined tax plus penalty burden 120% of the undisclosed income. Prosecution and reassessment powers add further risk.

Three Mistakes That Attract Notices

- Form 67 filed late — courts have not treated this as an automatic disallowance in every case, but delayed filing significantly increases the risk that your Foreign Tax Credit claim is rejected outright

- Wrong exchange rate used — Google rates and brokerage platform rates are not accepted. Use the SBI TT buying rate on the applicable date as specified under Rule 115

- Schedule FA omitted — non-disclosure of foreign assets is a standalone breach under the Black Money Act, even when those assets generated zero income that year

When to Seek Specialist Advice

Proactive planning around the RNOR window, regime selection, treaty positioning, and asset structuring can meaningfully reduce your foreign income tax exposure. Where the picture involves multiple income streams, assets spread across jurisdictions, and cross-border family finances, a SEBI-registered adviser with cross-border expertise — such as iVentures Wealth (INA000019026) — can handle the treaty structuring, compliance filings, and asset-level planning in an integrated way. The firm works with NRI and OCI clients who have ₹5 Cr or more in investible assets.

Frequently Asked Questions

How much foreign income is tax-free in India?

There is no separate tax-free limit for foreign income — it's combined with your total income and taxed under the standard slabs. Under the new regime for AY 2026-27, effective tax is nil up to ₹12 lakh after the Section 87A rebate. NRIs owe no Indian tax on foreign income; RNORs may also be exempt on qualifying foreign income not received in India.

How much tax will I pay on foreign income?

Foreign income is taxed at the same slab rates as domestic income — 0% to 30% depending on total income — plus a 4% cess and applicable surcharge for higher incomes. The actual amount depends on your total annual income, your chosen tax regime, and whether you can claim Foreign Tax Credit for taxes already paid abroad.

Is income from abroad taxable in India?

For Resident and Ordinarily Resident (ROR) individuals, yes — all global income is taxable in India. NRIs are taxed only on Indian-source income. RNORs are generally exempt on foreign income unless it is received in India or derived from a business controlled here.

Does DTAA help avoid double taxation on foreign income in India?

Yes. India's DTAAs with over 90 countries allow taxpayers to claim a Foreign Tax Credit for taxes already paid abroad on income also taxable in India. This credit is claimed via Form 67 (or Form 44 under the 2026 Rules) and is limited to the lower of the tax paid abroad or the Indian tax on that income.

What is the tax treatment for NRIs receiving foreign income?

NRIs are not taxable in India on foreign income. Only income earned, accrued, or deemed to accrue in India — such as Indian salary, rental income from Indian property, or capital gains from Indian assets — is taxable for NRIs.

What happens if I don't disclose foreign income or foreign assets?

Penalties under the Black Money Act are steep: ₹10 lakh per undisclosed foreign asset per year, plus 30% tax and a penalty equal to three times that tax — a combined burden of up to 120% of undisclosed income, with prosecution also possible. Always declare foreign assets in Schedule FA, even if they generated no income that year.

This article is for informational purposes only and does not constitute tax advice. Tax laws change frequently — always verify current figures with the official Income Tax Department portal (incometaxindia.gov.in) or consult a qualified tax professional before filing.