According to a 2026 Mint report, commissions still dominate India's wealth management landscape, with distributor income reaching up to 1% of AUM while pure advisory fees sit far lower. That gap tells the real story.

This article breaks down every pricing model, regulatory cap, embedded cost, and factor you need to evaluate before engaging a financial advisor in India.

Key Takeaways

- SEBI caps RIA fees at 2.5% of AUA per year (AUM mode) or ₹1,51,000 per year (fixed mode) per client family — these are legal ceilings, not typical market rates

- MFDs don't send you a bill, but regular mutual fund plans carry higher expense ratios — a gap that compounds into lakhs over a decade

- 18% GST applies to SEBI RIA advisory fees and must be factored into your total annual cost

- Fiduciary, fee-only advisors are structurally prohibited from earning product commissions — a critical distinction when evaluating objectivity

- Always verify SEBI registration before engaging any advisor at the SEBI Investment Adviser registry

How Much Do Financial Advisors Charge in India?

There is no single standard fee. Pricing depends on advisor type, regulatory structure, portfolio size, and scope of services. Getting this wrong has real costs: investors unknowingly pay embedded trail commissions, underestimate fee-only advice, or mistake a low apparent cost for better value.

The three main pricing models work quite differently — and which one applies to your situation changes what you actually pay.

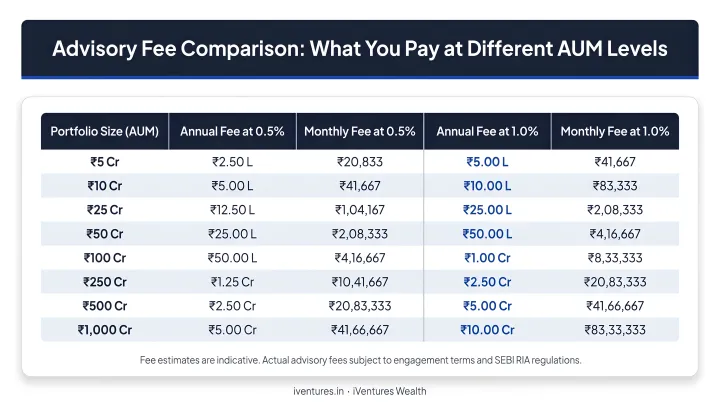

AUM-Based Fee (Percentage of Assets Managed)

The most common model for full-service wealth management. You pay a percentage of your assets under advice annually.

SEBI's regulatory cap for non-institutional clients: 2.5% of AUA per annum per client family. This is the legal maximum — not a benchmark for typical market fees.

In practice, pure advisory fees for HNI/UHNI clients tend to run lower. A practical example:

| Portfolio Size | Annual Fee at 1% | Annual Fee at 0.5% |

|---|---|---|

| ₹1 Cr | ₹1,00,000 | ₹50,000 |

| ₹5 Cr | ₹5,00,000 | ₹2,50,000 |

| ₹10 Cr | ₹10,00,000 | ₹5,00,000 |

Most full-service firms use tiered structures — the fee percentage decreases as AUM grows. In practical terms, a client crossing into a higher tier pays a lower rate on incremental assets — so the effective cost as a percentage falls as the portfolio grows. At iVentures Wealth, for example, the tiered schedule reduces basis points as client assets move from HNI (₹5–50 Cr) to UHNI (₹50 Cr+) to Family Office thresholds (₹100 Cr+).

Add 18% GST to every figure above — it applies to all SEBI RIA advisory fees.

Flat / Retainer Fee

A fixed annual amount covering a defined scope of services, regardless of portfolio performance. Best suited for clients who want predictable costs.

SEBI's current fixed-fee cap for non-institutional clients: ₹1,51,000 per annum per client family (excluding statutory taxes and charges), updated from the previous ₹1,25,000 cap under SEBI's January 2025 Investment Adviser Guidelines.

This model works well when:

- Portfolio size is modest relative to the breadth of services needed

- Clients want budget certainty across tax planning, estate coordination, and reporting

- The mandate involves financial planning more than active portfolio management

Commission-Based (Mutual Fund Distributors)

MFDs don't charge you directly. Instead, they earn trail commissions from AMCs — embedded in the Total Expense Ratio (TER) of regular mutual fund plans. Investors in regular plans pay more than those in direct plans without receiving a separate bill.

The cost difference is real. Take HDFC Flexi Cap Fund as a current example:

| Plan | TER (as of 12 June 2026) |

|---|---|

| Direct Plan | 0.78% |

| Regular Plan | 1.38% |

| Spread | 0.60 percentage points |

That 0.60% gap compounds annually. According to Financial Express, a 1% TER difference can reduce your final corpus by ₹10–15 lakh over 20 years.

HDFC Bank's commission disclosure shows equity fund trail ranges of 0.04%–1.30% and ELSS trail ranges of 0.21%–1.55% — so "0.5%–1%" is a useful illustration, not a fixed rate.

Key Factors That Affect Financial Advisor Fees in India

Pricing is determined by a mix of regulatory, operational, and client-specific factors. Understanding each helps you assess whether you're getting fair value.

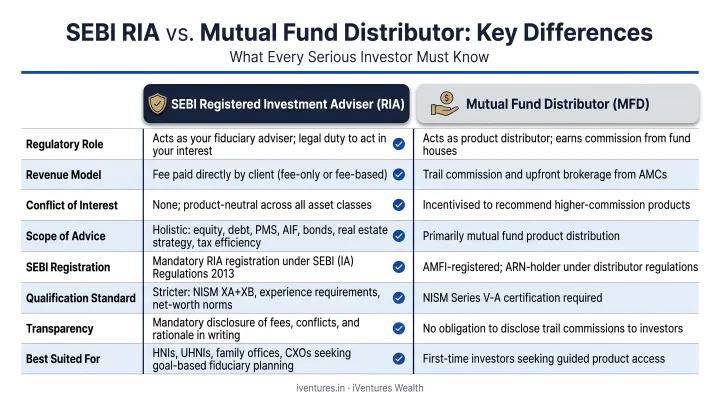

Advisor Type and Regulatory Model

The structural difference between advisor types has a direct impact on what you pay and whose interests are served.

| Attribute | SEBI RIA | Mutual Fund Distributor |

|---|---|---|

| Revenue source | Fee from client | Commission from AMC |

| Fiduciary obligation | Yes — must act in client's best interest | No fiduciary standard |

| Can recommend direct plans | Yes | No |

| Fee transparency | Explicit, invoiced, + GST | Embedded in fund TER |

As of June 2026, SEBI's registered Investment Adviser list shows only 1,039 registered RIAs across India — a small number relative to the broader MFD distribution ecosystem.

Portfolio Size and Complexity

Simple portfolios with a single mutual fund SIP require minimal advisor time. Complex situations cost more — and rightly so.

Complexity drivers include:

- Multiple legal entities (HUF, trusts, private limited companies, LLPs)

- Foreign assets, cross-border tax obligations, or NRI/OCI compliance requirements

- Business income, ESOPs, RSUs, or liquidity events

- Multiple custodians and asset classes requiring consolidated reporting

A family office managing ₹100 Cr+ across jurisdictions needs meaningfully more advisor bandwidth than a professional investor with a single portfolio.

Scope of Services

Advisory fees rise when the engagement extends beyond investments. A narrow investment-only mandate costs considerably less than a full-service wealth management relationship.

Comprehensive services that increase fee levels:

- Tax planning coordination and CA interface

- Estate planning, will drafting, private family trusts

- NRI/OCI compliance, DTAA structuring, FEMA routing

- Real estate advisory and rental yield strategies

- Succession and legacy planning

- Consolidated portfolio reporting across entities

For context on what this looks like in practice: iVentures Wealth structures its HNI and UHNI engagements to include all of the above within the advisory fee. Clients also receive access to the iVentures Wealth App for consolidated portfolio tracking, quarterly performance reviews, and tax summary reports — without separate billing for each.

Advisor Credentials and Firm Track Record

Credentials such as CFA and CFP, combined with experience managing high-value relationships, command premium fees. A CFA-led research team managing ₹50 Cr+ relationships over multiple market cycles offers a different proposition than a generic distributor with product access.

This is a legitimate cost driver. Research quality, portfolio construction discipline, and behavioural coaching through volatile markets have measurable value — which the next section addresses directly.

GST and Other Charges

18% GST applies to advisory fees charged by SEBI-registered RIAs — confirmed by CBIC sectoral FAQs covering investment and portfolio research/advice under taxable financial services.

A few things to keep straight:

- GST is charged on the advisory fee invoice, not embedded in mutual fund TERs

- Mutual fund TERs already include statutory levies (inclusive of GST on the AMC/distributor side)

- Always ask for the GST-inclusive total when comparing advisor costs — it can add 18% to the headline figure

What's Really Included in the Fee? A Full Cost Breakdown

The quoted advisory fee is rarely the total cost. Here are all the layers:

Advisory fee (recurring) The primary fee paid to the advisor — either AUM-based or a fixed retainer. One-time setup or financial plan creation fees may apply for onboarding, though some firms waive these for higher-AUM relationships.

GST on advisory fees (recurring) 18% added to every advisory invoice for SEBI RIA engagements. On a ₹3,00,000 annual fee, that's ₹54,000 in GST — an amount most investors miss when comparing advisor quotes side by side.

Fund-Level Costs: What's Hiding in the Product

Separate from the advisory fee and charged at the product level:

- Mutual fund expense ratios (TER) — lower for direct plans, higher for regular

- PMS management fees (typically 1%–2.5% annually)

- AIF fees (management fee plus performance fee structures)

- Brokerage on direct equity trades

In regular mutual fund plans, the fund embeds trail commissions directly in the TER — you pay them whether you realise it or not.

To put a number to it: a client with a ₹10 Cr portfolio paying a 0.75% RIA advisory fee owes ₹7,50,000 + ₹1,35,000 GST = ₹8,85,000 annually to the advisor alone. Fund-level costs come on top of that, depending on the product mix.

Low-Cost vs. High-Quality Advisory: What's the Difference?

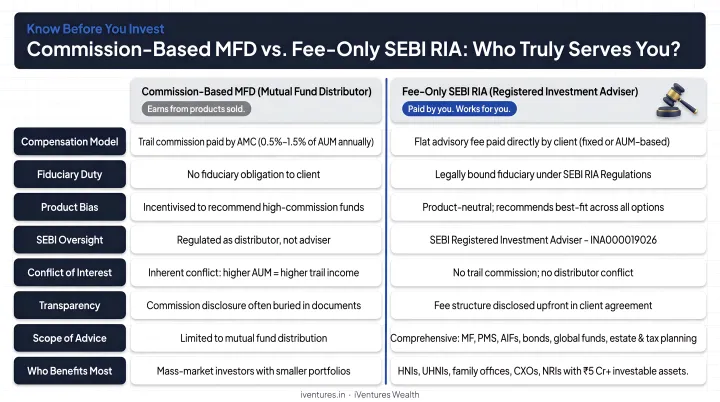

Objectivity and Conflict of Interest

A commission-based MFD earns more when you invest in products with higher trail commissions. That creates a structural incentive to recommend regular plans over direct, higher-commission funds over better-fit alternatives. The problem isn't intent — it's the structure itself.

A SEBI RIA is legally prohibited from earning product commissions. The fiduciary obligation runs to the client, not the AMC. This structural difference matters more than the percentage fee difference in many cases.

Scope and Depth

What you typically get at each model:

| Commission-based MFD | Fee-only SEBI RIA |

|---|---|

| Mutual fund distribution (regular plans) | Comprehensive financial planning |

| No tax planning | Tax-efficient portfolio structuring |

| No estate planning | Estate planning and succession advisory |

| No NRI compliance | DTAA structuring, FEMA compliance |

| Product-shelf restricted | Open-architecture, full product universe |

Long-Term Value

The scope difference above translates into measurable outcomes. Vanguard's Advisor's Alpha research estimates advisor value at approximately 3% net annually, with behavioural coaching alone worth 150 basis points. Morningstar's Gamma framework suggests sound planning decisions can generate 29% more retirement income on average. These are not guarantees — but they ground the conversation in evidence.

A 1% advisory fee is easier to justify when it covers:

- Preventing panic selling during a market correction (behavioural coaching)

- Structuring a DTAA-efficient NRI portfolio to reduce cross-border tax drag

- Catching a capital gains error worth ₹20 lakh before it becomes a liability

How to Budget for a Financial Advisor — and What Most Investors Get Wrong

Focusing on the Percentage, Not the Rupee Amount

A 1% fee on ₹5 Cr is ₹5 lakh per year. That's the number to evaluate — not whether 1% "seems" reasonable in the abstract. Ask what you receive for ₹5 lakh annually: investment management only, or a full mandate including tax coordination, estate planning, reporting, and proactive reviews?

Treating the MFD Model as "Free"

Many investors genuinely believe their distributor costs nothing. The bill just doesn't arrive in their inbox. But the regular plan TER is higher than the direct plan TER by 0.30%–0.70% or more, depending on the fund category. On a ₹1 Cr mutual fund portfolio, that's ₹3,000–₹7,000 per year in embedded cost that compounds over time — silently reducing your final corpus.

Not Verifying SEBI Registration

Working with an unregistered advisor provides no regulatory protection. SEBI has taken enforcement action against unregistered advisory operations — including a February 2024 order against M/s NIFM Equity and Commodity Research and a warning letter in April 2025 against an unregistered investment adviser. Verify any advisor's registration at the SEBI Investment Adviser registry before engaging.

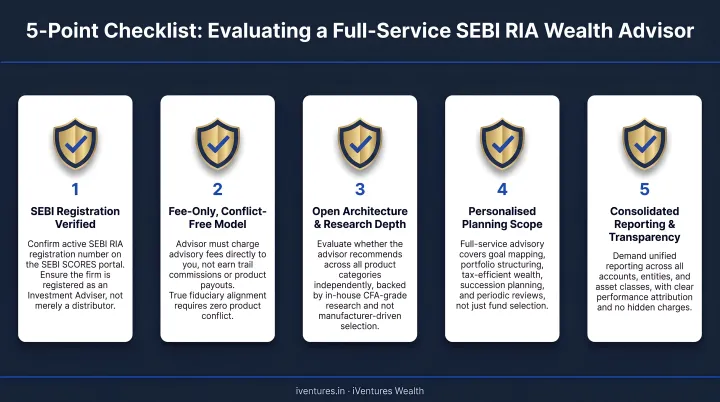

What to Look for in a Full-Service Relationship

For UHNIs, family offices, founders, and NRIs managing significant wealth, the right advisory relationship goes well beyond fund selection. Once you've identified what you're paying — and what you're not — evaluate any advisor against these criteria:

- SEBI RIA registration (verifiable on SEBI's public registry)

- Fee-only model with no trail commissions

- CFA-led or credentialled research capability

- Comprehensive service scope: tax, estate, reporting, NRI compliance

- Transparent fee agreement signed before investment

iVentures Wealth (SEBI RIA: INA000019026) is one example of this model in practice — fee-only since 2010, with a CFA-led research team and a service scope that spans investments, tax coordination, estate planning, NRI advisory, and consolidated reporting across 150+ client relationships. When a firm's fee agreement spells out that scope in writing before you invest, the higher cost becomes straightforward to justify.

Frequently Asked Questions

How much do financial advisors charge in India?

Fee-only SEBI RIAs charge either an AUM-based fee (capped at 2.5% of AUA per year by SEBI) or a fixed retainer (capped at ₹1,51,000 per year per client family). Commission-based MFDs earn trail income embedded in regular fund expense ratios. All SEBI RIA fees are subject to 18% GST on top of the quoted amount.

Are 1%–2% financial advisor fees reasonable in India?

It depends on what's included. A 1%–2% fee is reasonable when it covers comprehensive financial planning, tax coordination, estate planning, NRI compliance, and portfolio management. For investment-only mandates, the same fee may be hard to justify. Evaluate the rupee amount, the scope of services delivered, and the advisor's fiduciary status before deciding whether the fee is justified.

Can financial advisors advise on crypto in India?

SEBI-registered RIAs cannot officially recommend cryptocurrencies as regulated investment assets; no SEBI framework currently permits this. Under Indian tax law, gains from virtual digital assets are taxed at 30% under Section 115BBH, with 1% TDS under Section 194S. Confirm your advisor's regulatory scope and your own tax exposure before acting on any crypto guidance.

What is the difference between a SEBI RIA and a mutual fund distributor in India?

A SEBI RIA is a fee-only fiduciary advisor legally required to act in the client's best interest and prohibited from earning product commissions. An MFD earns trail commissions from AMCs for distributing mutual funds and operates under no fiduciary standard. In practice, this means an MFD's product recommendations may be shaped by commission structures rather than your financial goals.

Is GST charged on financial advisor fees in India?

Yes. CBIC classifies investment and portfolio advisory services as taxable financial services at 18% GST. This applies to fees invoiced by SEBI-registered RIAs and is charged in addition to the advisory fee. Mutual fund TERs handle GST differently — it's included in the TER rather than billed separately to investors.

Are financial advisor fees negotiable in India?

Within SEBI-prescribed caps, fee structures can often be negotiated — particularly for larger portfolios or complex multi-asset mandates. Ask for a full breakdown of what's included, whether a tiered structure applies as your assets grow, and whether onboarding fees apply or can be waived. Any agreed fees should be documented in a written advisory agreement before investment begins.