The problem isn't just noise. It's structural. Many of these advisors operate under no fiduciary obligation, earn commissions from product providers, and face zero regulatory consequences if their advice causes significant losses.

SEBI registration changes that equation entirely. It isn't an administrative badge — it's a regulated framework that mandates fiduciary conduct, mandatory qualifications, fee disclosures, periodic compliance audits, and formal investor recourse. For affluent investors and family offices managing serious wealth, that distinction is material.

This article breaks down exactly what SEBI registration means in practice, why it matters, and what you risk when you skip it.

Key Takeaways

- A SEBI-registered RIA is legally required to act in your best interest — not a product provider's

- SEBI registration requires ongoing qualifications, risk profiling, fee disclosures, and annual audits

- Commission-driven distributors and bank RMs carry no fiduciary obligation — a structural conflict of interest

- Fee transparency under SEBI rules eliminates hidden costs buried in expense ratios or premiums

- SEBI-RIA clients have formal complaint recourse through the SCORES portal — a protection unregistered advisors can't offer

What Is a SEBI-Registered Investment Advisor?

A SEBI-Registered Investment Adviser (RIA) is an individual or firm officially registered under the Securities and Exchange Board of India (Investment Advisers) Regulations, 2013, as amended, and authorised to provide personalised investment advice for a fee.

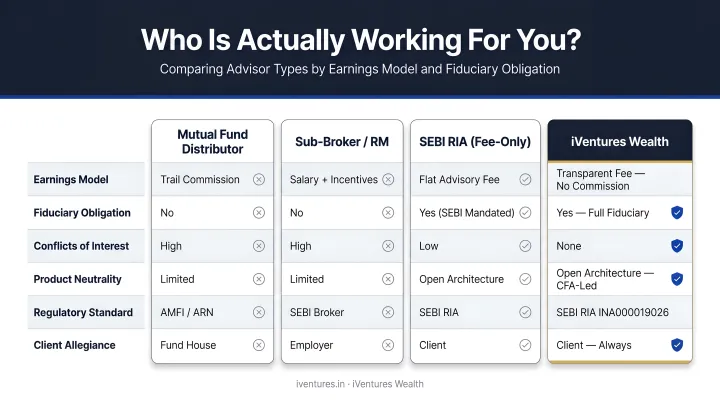

The key difference from other market participants comes down to who pays them — and who they're legally required to serve:

| Advisor Type | How They Earn | Fiduciary Obligation |

|---|---|---|

| SEBI-Registered RIA | Client fees only | Yes — legally mandated |

| Mutual Fund Distributor | Commissions from fund houses | No |

| Bank Relationship Manager | Salary + product-linked incentives | No |

| Insurance Agent | Product commissions | No |

What Registration Actually Requires

SEBI registration is not a formality. Registered advisors must meet ongoing requirements:

- Pass NISM-Series X-A and X-B Investment Adviser certification exams

- Meet qualification standards (postgraduate or professional qualifications, or CFA)

- Maintain minimum net worth or deposit requirements

- Conduct mandatory annual compliance audits by a third-party auditor

- Maintain client records for a minimum period

- Prohibit any receipt of commissions, trail income, or placement fees from product manufacturers

- Complete mandatory risk profiling before any advice is given

The commission prohibition is the most significant requirement. By prohibiting commission income entirely, SEBI regulations remove the primary incentive to recommend unsuitable products.

Key Advantages of Choosing a SEBI-Registered Investment Advisor

Advantage 1: Fiduciary Duty — Your Interests Come First

Fiduciary duty under SEBI regulations means the advisor is legally and ethically obligated to prioritise your best interest in every recommendation. Not their own revenue. Not a product company's commission targets.

In practice, a SEBI-RIA cannot recommend a product because it pays a higher trail commission. Every recommendation must be justified against your risk profile, investment goals, time horizon, and tax situation — and that justification must be documented in writing.

For HNI and UHNI investors managing portfolios across multiple asset classes, this structural protection matters in specific ways:

- Recommendations across equity, debt, alternatives, and real estate are made on merit — not distributor payout rankings

- Portfolio construction follows research and asset allocation logic, not product shelf incentives

- Advisors have no financial motive to churn your portfolio — a common source of hidden tax drag and transaction costs in commission-driven models

The cost of commission-driven advice is not theoretical. SEBI issued an Interim Order in the Baap of Chart unregistered advisory case in October 2023, and a subsequent enforcement order against M/s NIFM Equity and Commodity Research for unregistered investment advisory activities in February 2024 — both illustrating the active risks from unregulated advisory channels. These cases are particularly instructive for large-ticket investors, where the financial consequences of misaligned advice scale with portfolio size.

Advantage 2: Regulatory Oversight and Formal Accountability

SEBI-registered advisors operate under continuous regulatory oversight, with concrete accountability mechanisms that unregistered advisors simply cannot offer:

- Third-party auditors conduct annual compliance audits

- Client records must be maintained for SEBI-prescribed periods

- Advisors file periodic reports with SEBI and face registration cancellation for misconduct

According to SEBI's October 2024 board memorandum, there were just 927 registered investment advisers as of August 31, 2024, serving over 12 crore investors — a ratio SEBI itself described as "not commensurate with the size of the securities market." As of June 2026, that figure had grown to only 1,039 registered IAs. With roughly 11 crore unique NSE investors divided among 1,039 advisors, the arithmetic implies approximately one regulated advisor for every 100,000 investors. That scarcity makes credential verification — not assumption — the only sensible starting point.

What regulatory oversight delivers in practice:

- Clients can file formal complaints through SEBI's SCORES (SEBI Complaints Redress System) portal

- Registered entities must submit an Action Taken Report within 21 calendar days of a complaint

- Unresolved complaints can be escalated for further review within defined timelines

- SCORES explicitly excludes complaints against unregistered or unregulated activities — meaning unregistered advisors offer no equivalent recourse

This is particularly critical for NRIs, family offices, and corporates navigating complex multi-jurisdictional investments where formal grievance mechanisms are non-negotiable.

Advantage 3: Fee Transparency and Conflict-Free Portfolio Construction

Regulatory accountability and fee transparency are two sides of the same coin. SEBI prescribes explicit fee caps for registered investment advisers:

- AUA-based fee: Maximum 2.5% of Assets Under Advice per annum per family

- Fixed fee: Up to ₹1,51,000 per annum per family

Both must be disclosed upfront in a signed client agreement, with no hidden charges embedded in product costs. This transparency is the opposite of how commission-based advice typically works.

The Hidden Cost of "Free" Advice

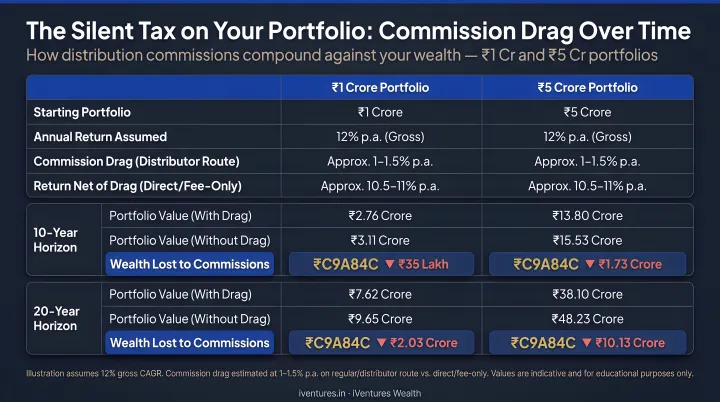

Commission-embedded advice from mutual fund distributors, bank RMs, and insurance agents appears free at delivery — but the cost is baked into the product's expense ratio or premium structure, rarely disclosed in proportion to what you're actually paying. According to Value Research, equity direct plans carry expense ratios 0.30% to 0.95% lower than regular plans, with the difference flowing directly to the distributor as commission.

That gap compounds significantly at scale:

| Portfolio Size | Horizon | Cost of 0.30% Drag | Cost of 0.95% Drag |

|---|---|---|---|

| ₹1 crore | 10 years | ~₹6.99 lakh | ~₹21.55 lakh |

| ₹1 crore | 20 years | ~₹35.76 lakh | ~₹1.07 crore |

| ₹5 crore | 10 years | ~₹34.94 lakh | ~₹1.08 crore |

| ₹5 crore | 20 years | ~₹1.79 crore | ~₹5.36 crore |

Illustrative calculations assuming 10% gross annual return. Assumes constant expense drag. Not a guaranteed saving.

For UHNIs with large portfolios, the fee paid to a SEBI-RIA is often materially smaller than the hidden cost drag embedded in regular plan products recommended by commission-based distributors.

What Happens When You Choose an Unregistered Advisor

Unregistered advisors operate outside SEBI's regulatory framework entirely. The risks are concrete:

- No fiduciary obligation — they are under no legal requirement to recommend what suits you

- No mandatory risk profiling — advice can be given without any assessment of your capacity for loss

- No annual compliance audits — no third-party checks on advice quality or conduct

- No formal complaint mechanism — SCORES explicitly excludes complaints against unregistered activities

Real-world consequences include portfolio churn to generate ongoing distributor trail commissions, accumulation of high-cost ULIPs or insurance-linked products presented as investment advice, and recommendations from affiliated companies rather than the best available options.

One client who came to iVentures Wealth held twelve mutual funds and ULIPs built up over several years — with total returns barely ahead of fixed deposits. After a full portfolio review and reconstruction into a focused, research-backed allocation, long-term return potential improved significantly.

Misalignment at high AUM levels creates tax inefficiencies, unnecessary concentration risk, and expensive restructuring — at precisely the point when that capital should be working hardest.

How to Get the Most Value from a SEBI-Registered Advisor

SEBI registration is the baseline, not the ceiling. To maximise the value of the relationship:

- Verify registration directly — search by name or registration number on SEBI's official Investment Adviser list. Confirm the registration number, contact details, and validity period match what the advisor has disclosed

- Review team qualifications — check whether the advisory team holds CFA, NISM certifications, or relevant postgraduate credentials beyond the minimum requirements

- Confirm risk profiling happens before any advice — a written risk profile and documented investment rationale should precede any recommendations

- Expect a written fee agreement — the fee structure, scope of advice, and complaint escalation process should all be in writing before you invest

- Treat it as a long-term partnership — the value of consistent, fiduciary-aligned advice compounds over time, particularly through market cycles when behavioral coaching and staying invested matter most

That last point has research behind it. Vanguard's Advisor's Alpha study estimates quality advisory adds approximately 3% in net returns annually, driven primarily by behavioral coaching — keeping clients aligned to their plans during volatile periods rather than reacting emotionally.

That figure is a global estimate, not India-specific. But the underlying dynamic holds: an advisor paid for your continued engagement, not for product sales, has a direct financial incentive to keep your decision-making steady when markets aren't.

If you are looking for a SEBI-registered firm that meets these criteria — fee-based, fiduciary, research-driven, and with a verifiable compliance record — iVentures Wealth (SEBI Registration No. INA000019026) is one example worth considering. Operating since 2010 as a registered investment advisor, the firm is led by a CFA-qualified research team, has ₹1,146+ crore in assets under advice, and has maintained zero investor complaints on SEBI's record since FY 2021-22, serving 150+ affluent families, UHNIs, and corporates across India.

Conclusion

In a market where product sellers routinely present themselves as advisors, SEBI registration is the clearest enforceable signal that an advisor is legally accountable to you — not to a fund house, insurance company, or bank.

That accountability compounds. Fiduciary duty, regulatory oversight, and fee transparency deliver better portfolio decisions, lower embedded costs, and an advisory relationship that holds through market cycles — not just once, but across decades of wealth-building.

Treating SEBI registration as the non-negotiable starting point of any advisor selection process is the most consequential filter an affluent investor can apply.

Frequently Asked Questions

How do I verify a SEBI-registered advisor?

Visit SEBI's official Investment Adviser list at sebi.gov.in and search by name or registration number. Confirm that the registration number, contact details, and validity period match exactly what the advisor has disclosed to you.

Who are SEBI's registered investment advisors?

SEBI-registered investment advisers are individuals or firms registered under the SEBI (Investment Advisers) Regulations, 2013 — including independent RIA firms, wealth management companies, and financial planners who have met SEBI's qualification, net worth, and compliance requirements and are authorised to provide personalised investment advice for a fee.

How many investment advisors are registered with SEBI?

As of June 2026, SEBI's official intermediaries list showed 1,039 registered investment advisers. SEBI's own 2024 board memorandum flagged that 927 advisers were serving over 12 crore investors — a ratio the regulator described as "not commensurate with the size of the securities market," signalling an intent to expand RIA access.

What is the difference between a SEBI RIA and a mutual fund distributor?

A SEBI RIA charges a transparent, pre-agreed fee and is legally bound to act in the client's best interest under fiduciary obligations. A mutual fund distributor earns commissions from fund houses for selling products and carries no fiduciary obligation toward the investor.

What is the fee structure for a SEBI-registered investment advisor?

SEBI caps RIA fees at either 2.5% of Assets Under Advice per annum per family, or a flat fee of up to ₹1,51,000 per annum per family. The applicable fee structure must be disclosed upfront in a signed written client agreement, with no hidden charges permitted.

Can I file a complaint against a SEBI-registered advisor?

Yes. Clients of SEBI-registered advisors can file formal complaints through SEBI's SCORES portal at scores.sebi.gov.in. Registered entities must submit an Action Taken Report within 21 calendar days. This formal recourse mechanism does not exist for unregistered advisors — SCORES explicitly excludes complaints about unregistered or unregulated activities.