Introduction

Decades building a business. One founder, one vision — and usually no written plan for what comes next. When the question of succession comes up, the silence is often uncomfortable.

This isn't unusual. According to PwC India's research, only 63% of Indian family businesses have formal governance structures including shareholder agreements, family constitutions, or wills. The remaining 37% are operating without a documented plan for one of the most consequential transitions a business will ever face.

The consequences show up in court filings, forced asset sales, and family rifts — not in boardrooms.

This article covers what founders and business families need to know heading into 2026:

- The legal and tax structures available under Indian law for business succession

- How to separate ownership from day-to-day management

- Common planning mistakes that trigger disputes and forced sales

- Concrete steps to protect both the business and generational wealth

Key Takeaways

- Estate planning for family businesses extends well beyond a Will — ownership transfer, tax structuring, governance design, and liquidity planning all require separate attention.

- In India, private trusts, family settlement agreements, HUF structures, and buy-sell agreements are the primary succession vehicles.

- The most critical challenge: separating ownership succession from management succession without triggering family conflict.

- Gradual transfer strategies require an early start; delayed or crisis-driven planning raises costs in tax, time, and family cohesion.

What Is Estate Planning for Family Business Succession — And Why It Can't Wait

Two Concepts, One Integrated Plan

Estate planning is the structured process of deciding how ownership, control, and economic value transfer to the next generation — covering legal documents, tax structures, and governance frameworks across both personal and business assets.

Succession planning is narrower: it governs who takes over operations, when, and under what terms. Neither works in isolation. A Will that distributes shares equally among three children means nothing without a shareholder agreement clarifying who controls the board, how decisions get made, or what happens when two siblings disagree on strategy. Indian family business founders need both — working together.

The Cost of Waiting

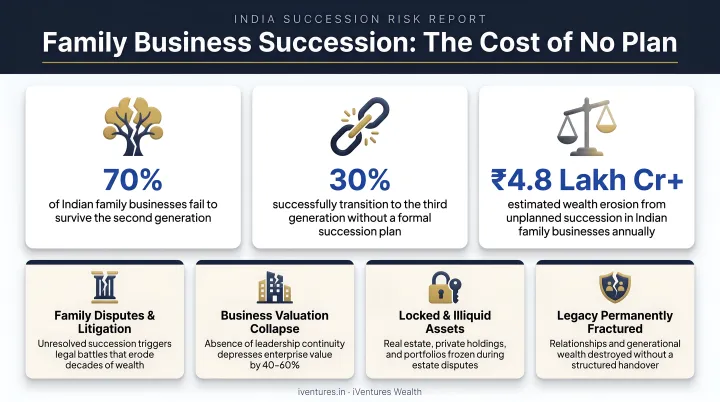

The numbers tell a clear story. According to the Confederation of Indian Industry, only 13% of Indian family businesses survive to the third generation and just 4% beyond that. Approximately 70% don't survive past the second generation.

The reasons are rarely external. They're structural — fragmented ownership, unclear governance, disputes among heirs who hold equal stakes but unequal operational involvement.

When a founder dies without a documented succession structure, the consequences are predictable:

- Operational paralysis — family members contest control before anyone runs the business

- Active vs. non-active heir conflicts over who manages the business versus who simply collects returns

- Forced asset sales at distressed valuations to fund buyouts or settle legal claims

The Ambani case remains the most instructive Indian example. Dhirubhai Ambani died in July 2002 without a Will. The family's 46.67% equity in Reliance Industries had no documented succession structure. A multi-year public dispute followed. It was resolved only by a mother-brokered family settlement in 2005 that split the empire — and the two resulting entities have taken dramatically different trajectories since.

The Ambani outcome wasn't inevitable. It was the result of a missing document — and that's precisely the kind of structural gap that a coordinated estate and succession plan is designed to close before a crisis forces the issue.

Key Legal Structures for Family Business Succession in India

India offers several well-established legal vehicles for family business succession. Most robust plans use a combination rather than a single instrument. India offers several well-established legal vehicles for family business succession. Most robust plans use a combination rather than a single instrument. Here's how each structure works — and when to use it.

Private Trust (Indian Trusts Act, 1882)

A private trust is one of the most effective succession vehicles available to Indian business owners. By placing business shares into a private discretionary or specific trust:

- Business assets bypass probate, enabling faster and more private transfer

- Management control can be consolidated within a trustee structure, preventing fragmentation

- Economic benefits flow to designated beneficiaries without those beneficiaries holding direct voting rights

- Under Section 47(iii) of the Income Tax Act, transfer of capital assets to an irrevocable trust is exempt from capital gains tax

The distinction between determinate trusts (beneficiaries' shares fixed, income taxed in their hands) and discretionary trusts (income taxed at the maximum marginal rate) has material tax implications and requires professional structuring.

Will (Indian Succession Act, 1925)

A Will is the foundational document, but a generic Will is insufficient for family business owners. It must specifically address business interests and align precisely with any shareholder agreements, partnership deeds, or trust structures already in place. A Will that contradicts a shareholder agreement creates litigation.

One recent change to note: the mandatory probate requirement under Section 213 of the Indian Succession Act was abolished by the Repealing and Amending Act, 2025 (Presidential assent December 20, 2025). Probate can still be obtained voluntarily for businesses in Mumbai, Kolkata, or Chennai.

Family Settlement Agreements (FSAs)

An FSA is a consensual arrangement among all family members governing the division of business interests, management roles, and asset allocation. The Supreme Court in Kale & Others v. Deputy Director of Consolidation (AIR 1976 SC 807) held that family settlements are "highly favoured by the law" because they promote domestic harmony and prevent prolonged litigation.

Key practical points:

- Oral FSAs are legally valid

- No capital gains tax typically applies when settlement is among close family members

- Where the settlement deed creates or extinguishes rights in immovable property, registration under the Registration Act, 1908 is mandatory

Buy-Sell Agreements

A buy-sell agreement specifies exactly what happens to a founder's stake upon death, incapacity, or retirement. Two elements are non-negotiable:

- A pre-agreed valuation methodology — prevents disputes about what the stake is worth at a critical moment

- A funding mechanism — typically a life insurance policy structured to provide liquidity without straining business cash flows

These agreements can include put/call options, buyback provisions, and tag-along rights that protect minority stakeholders — all governed under the Indian Contract Act, 1872 and Companies Act, 2013.

Hindu Undivided Family (HUF)

HUFs remain a useful wealth-holding structure, but carry specific complications in business succession. The Hindu Succession (Amendment) Act, 2005 granted daughters equal coparcenary rights by birth, confirmed retroactively by the Supreme Court's August 2020 ruling.

This significantly expands the number of claimants in HUF property, requiring careful Karta succession planning and active partition risk management.

Tax and Liquidity Planning: Protecting the Business from a Forced Sale

The Indian Tax Landscape for Succession

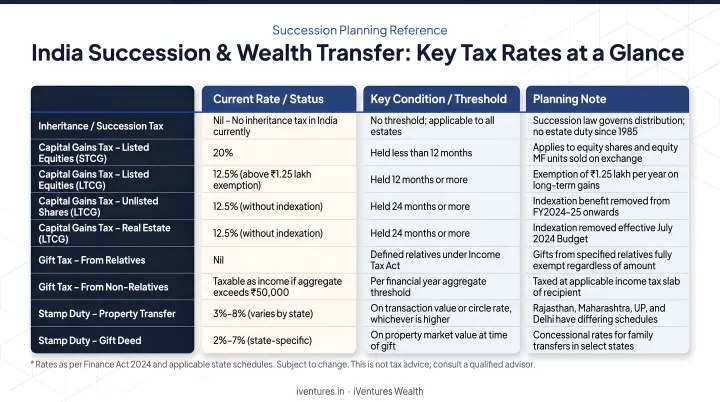

India abolished estate duty in 1985, so there is no inheritance tax to plan around. However, three tax considerations remain live:

| Tax | Trigger | Rate/Treatment |

|---|---|---|

| Capital Gains (LTCG) on unlisted shares | Transfer of shares held 24+ months | 12.5% flat (post-Budget 2024, indexation removed) |

| Gift tax — Section 56(2)(x) | Transfer to non-relatives exceeding ₹50,000 | Taxable as income from other sources |

| Stamp duty on share transfers | Transfer of shares | 0.015% (uniform post-2020 rules) |

Transfers among specified relatives (spouse, siblings, lineal ascendants and descendants) are fully exempt from gift tax under Section 56(2)(x), regardless of value. That exemption is what makes structured, multi-year gifting programmes viable for most family businesses.

Lifetime Gifting to Reduce Transfer Costs

Transferring business shares to the next generation gradually — over years rather than in a single event — can significantly reduce overall tax liability. Where minority interest discounts or lack-of-marketability discounts apply in professional valuations, the taxable value of transferred interests decreases further.

The critical constraint is lead time. A 10-year gifting programme allows discounts to compound across multiple transfers, spreads capital gains events, and keeps each individual transfer below thresholds that attract heightened scrutiny. A single crisis transfer achieves none of this.

Key factors that affect gifting strategy design:

- Valuation timing — transfers made when business value is lower reduce the taxable base

- Relationship eligibility — only specified relatives qualify for the Section 56(2)(x) exemption

- Discount applicability — minority interest or lack-of-marketability discounts require a documented professional valuation

- Holding period — shares must be held 24+ months to qualify for LTCG rates rather than short-term treatment

Solving the Liquidity Problem

Many family businesses are asset-rich and cash-poor. When the business is the primary asset, an estate may lack the liquidity to pay debts, fund buyouts, or cover transition costs — creating pressure toward a distressed sale.

The standard approach involves a life insurance policy held within a private trust, structured so that:

- Death benefits (tax-exempt under Section 10(10D)) are immediately available to the estate

- Proceeds sit outside the taxable estate

- The business does not need to be sold or leveraged to fund the transition

This structure is typically executed with specialist insurance and legal counsel. The wealth advisory function ensures this layer is coordinated with the broader succession and asset allocation plan.

iVentures Wealth's approach to this challenge involves structuring surplus business profits into a three-bucket framework (safety, stability, and growth) that builds personal financial independence outside the business. This ensures the senior generation's lifestyle is not dependent on business performance, and no forced sale is needed to fund their retirement.

Holding Structures and SPVs

Placing business interests into a holding company or SPV allows for:

- Cleaner transfer of economic interest to the next generation

- Retention of governance rights by the original promoter through differential voting rights (DVR) shares under Section 43(a)(ii) of the Companies Act, 2013

- Separation of operational and holding entities for tax and liability purposes

A documented professional business valuation is essential before executing any transfer strategy. Valuation directly affects gift tax computations, stamp duty, and capital gains exposure; undervaluation attracts tax authority scrutiny.

Separating Ownership from Management: The Critical Distinction Every Founder Must Make

The Core Problem

A founder may want to distribute wealth equally among three children — which is fair. But only one child is capable of, or interested in, running the business — which is reality. Conflating the two leads to governance paralysis and family conflict.

Equal ownership among unequal contributors is one of the most common causes of Indian family business breakdown.

The Structural Solution

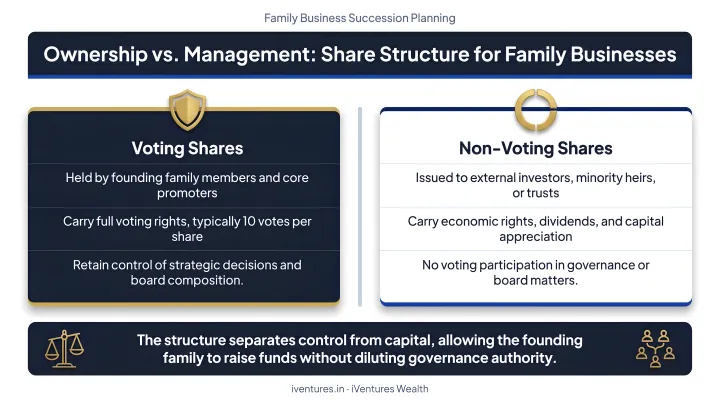

The mechanism for resolving this is a stock recapitalisation into voting and non-voting share classes:

- Non-active family members receive economic-only (non-voting) shares — they participate in dividends and wealth appreciation without influencing operational decisions

- The designated successor holds voting shares or management rights, with clear authority to run the business

This approach respects both fairness (everyone participates in wealth creation) and practicality (one person has clear authority to run the business).

Formalising the Governance Layer

Shareholder agreements and family constitutions do the work that goodwill cannot sustain across generations. These documents pre-specify:

- Who becomes Managing Director and under what conditions

- How board seats are allocated among family branches

- Which decisions require family council approval versus executive authority

- How disputes are resolved — whether through mediation, arbitration, or defined buyout mechanisms

The CII-FBN India Chapter recommends that family constitutions be drafted as inclusive, documented processes — not imposed top-down. Getting the governance layer right matters beyond paperwork: it determines whether the share structures, wealth transfer instruments, and family agreements reinforce each other or create contradictions when tested.

What Happens Without a Plan

The Murugappa Group case illustrates the practical cost of ambiguity. A dispute over board representation for the family branch of late M.V. Murugappan — including daughters seeking seats on Ambadi Investments (the holding company) — was complicated further when four group companies saw substantial share price increases, altering the relative valuations underlying any proposed division.

Without documented governance frameworks, even families with good intentions find themselves in protracted negotiations over shifting ground. The absence of a plan creates compounding risks:

- Business value erodes during the transition period, when competitors and stakeholders are watching

- Valuation disputes intensify if asset prices shift mid-negotiation

- Successor authority is challenged without a documented mandate

- Legal costs and delays accumulate, draining both capital and management focus

Building Your Succession-Aligned Estate Plan: A Practical Step-by-Step Approach

The Seven Core Steps

- Conduct a comprehensive asset audit: business interests, investments, real estate, liabilities, and overseas assets, consolidated into a single family balance sheet

- Define succession intent: who takes over management, and how ownership is distributed among all heirs

- Choose the right legal structure: trust, Will, FSA, buy-sell agreement, or a combination tailored to the family's complexity

- Align estate documents with business governance documents: shareholder agreements, board compositions, and Wills must be internally consistent

- Address liquidity needs through insurance: structure policies within a trust to fund buyouts and cover transition costs without a forced sale

- Formalise and communicate the plan: all key stakeholders, including active and non-active family members, should understand the structure

- Schedule regular reviews: the plan must evolve as the business, family, and tax environment change

The Professional Team Required

No single professional can address all dimensions of this work. A robust succession plan requires:

- A corporate lawyer to draft trust deeds, Wills, shareholder agreements, and FSAs

- A tax consultant or CA to address capital gains, gift tax, stamp duty, and income tax implications

- A family business governance expert to facilitate family council processes, draft constitutions, and manage stakeholder dynamics

- A SEBI-registered wealth advisor to coordinate the financial and investment architecture across all structures

The wealth advisor's role is distinct from the others. Lawyers document intent; CAs ensure tax compliance. The wealth advisor determines how assets should be allocated, invested, and structured to sustain the succession plan across generations — and keeps those decisions coherent as circumstances change.

iVentures Wealth serves as this coordinating partner for founding families and UHNIs across India. As a SEBI-registered fiduciary with 20+ years of experience, the firm consolidates all family assets into a unified view, structures tax-efficient transfers, and ensures the investment strategy for trust assets remains on track through and beyond the transition.

The Cost of Starting Late

Getting the professional team in place early matters because the most powerful transfer strategies — lifetime gifting, trust funding over multiple years, structured share recapitalisations — are only available when started well in advance. A plan built over ten years is not just more tax-efficient; it offers a longer gifting runway, more stakeholder alignment, and far less exposure to forced decisions under pressure.

The cost of not planning is borne by the family, the employees, and the business — not by any external party.

Frequently Asked Questions

What is estate planning in family business?

Estate planning in the family business context is the process of transferring business ownership, control, and value to heirs or successors in a structured way. It covers legal structures like trusts and Wills, tax optimisation strategies, governance frameworks, and liquidity planning — so the business survives the founder's exit intact.

Does estate planning cover succession?

Estate planning and succession planning are related but distinct. Estate planning is the broader umbrella covering all assets; succession planning specifically addresses who takes over operations. For family business owners, the two must be integrated — the succession plan should be embedded within and aligned to the overall estate plan.

How to plan for succession in a family business?

Start by identifying your successor — family member, key employee, or external buyer — and separating ownership decisions from day-to-day management. Formalise the plan in binding documents: shareholder agreements, buy-sell agreements, and trust deeds. Address tax and liquidity implications, then review periodically as family and business circumstances change.

What are the 7 steps in the estate planning process?

The seven steps are: (1) asset audit, (2) defining goals and succession intent, (3) choosing legal structures, (4) drafting key documents — Will, trust deed, buy-sell agreement, (5) liquidity and insurance planning, (6) communicating the plan to all stakeholders, and (7) periodic review as family and business conditions evolve.

What are the 5 D's of succession planning?

The 5 D's represent the trigger events that make succession planning urgent: Death, Disability, Divorce, Disagreement (among owners or family), and Distress (financial). Each of these events, without a plan in place, can force an unplanned and value-destructive business transition.

What are the 4 elements of an estate?

An estate consists of four elements: (1) real and personal property, (2) business interests and investments, (3) liabilities and debts, and (4) intangible assets such as intellectual property. For family business owners, the business interest is typically the largest and most complex element — requiring dedicated planning.