The good news: TCS is not a permanent cost. It is advance tax, and every rupee collected can be credited back against your income tax liability when you file your ITR. This guide breaks down exactly how TCS works, what rates apply from April 1, 2026, and how to recover what you've paid.

Key Takeaways

- TCS under LRS is advance tax — not a fee — and is fully recoverable when you file your ITR

- The TCS-free threshold is ₹10 lakh per financial year per PAN, aggregated across all banks and all remittance purposes

- TCS rates above ₹10 lakh: 0% for education loans, 2% for education/medical (self-funded), and 20% for all other purposes

- Overseas tour packages attract 2% TCS on the full amount with no ₹10 lakh exemption

- Form 27D (TCS certificate), Form 26AS, and your ITR are the three documents needed to claim TCS credit

What Is TCS Under LRS?

The Statutory Foundation

TCS on foreign remittances is governed by Section 206C(1G) of the Income Tax Act, 1961, inserted by the Finance Act 2020. It requires every authorised dealer (any bank or forex provider licensed by the RBI) to collect a percentage of each qualifying outward remittance on behalf of the Income Tax Department at the point of the transaction.

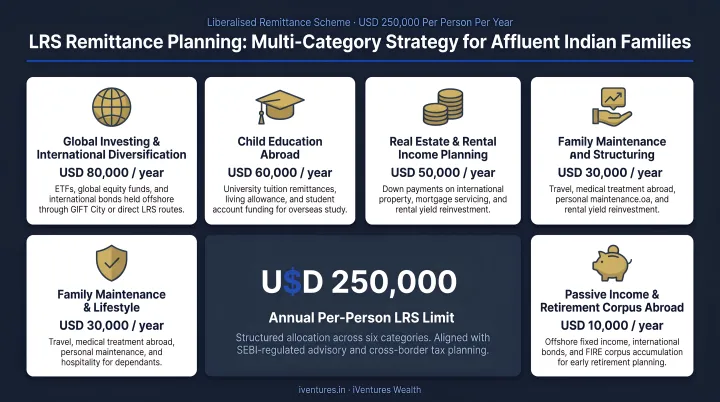

The remittance framework itself is the Liberalised Remittance Scheme (LRS), an RBI mechanism that allows all resident Indian individuals — including minors with guardian countersignature — to remit up to USD 250,000 per financial year. This limit covers both current and capital account transactions abroad. Full eligibility criteria and permitted uses are detailed in the RBI's LRS FAQ.

TCS vs. TDS: A Critical Distinction

Both are advance tax mechanisms, but they work differently:

| Feature | TCS | TDS |

|---|---|---|

| Who collects it | Your bank / authorised dealer | Your employer / payer |

| When collected | At the point of remittance | Before crediting income |

| Who bears it | The remitter (you) | The income earner |

| How to recover | Credit against ITR tax liability | Credit against ITR tax liability |

Both are refundable credits — not permanent costs — for any taxpayer who files returns.

TCS Rates on Foreign Remittances Under LRS: 2026 Update

The Union Budget 2025-26 raised the LRS TCS threshold from ₹7 lakh to ₹10 lakh, effective April 1, 2026. The full revised rate structure — confirmed in the Income-tax Act 2025 as amended by Finance Act 2026 — is set out in the two tables below, followed by key compliance rules every remitter should know.

Current Rate Table (Effective April 1, 2026)

| Purpose of Remittance | TCS Rate | Threshold |

|---|---|---|

| Education — loan from a specified financial institution | 0% | No collection |

| Education — self-funded | 2% | On amount exceeding ₹10 lakh |

| Medical treatment | 2% | On amount exceeding ₹10 lakh |

| All other purposes (investments, gifts, maintenance, travel) | 20% | On amount exceeding ₹10 lakh |

| Overseas tour programme packages | 2% | On the full amount (no threshold) |

Pre-2026 vs. Post-2026 Comparison

| Purpose | Pre-April 2026 Rate | Post-April 2026 Rate | Threshold Change |

|---|---|---|---|

| Education (loan-funded) | 0% | 0% | No change |

| Education (self-funded) / Medical | 5% above ₹7 lakh | 2% above ₹10 lakh | Threshold raised; rate reduced |

| Other LRS purposes | 20% above ₹7 lakh | 20% above ₹10 lakh | Threshold raised only |

| Overseas tour packages | 5% (full amount) | 2% (full amount) | Rate reduced |

The Inoperative PAN Consequence

If your PAN is inoperative — meaning it has not been linked to Aadhaar as required under Rule 114AAA — the higher-rate provision under Section 206CC applies. TCS is collected at the higher of twice the specified rate or 5%, subject to a 20% cap.

In practice:

- 2% categories (education, medical) become 5%

- 20% categories remain 20% (already at the cap)

Linking your PAN with Aadhaar through the Income Tax e-filing portal restores standard rates.

The Aggregate Threshold Rule

The ₹10 lakh exemption is not per transaction, per bank, or per purpose. It is a single annual aggregate per PAN across all authorised dealers and all remittance purposes in a financial year. CBDT Circular No. 10/2023 confirmed this aggregation mechanism. Once your total remittances cross ₹10 lakh in a financial year, TCS applies to every rupee sent after that point — regardless of which bank processes the transaction.

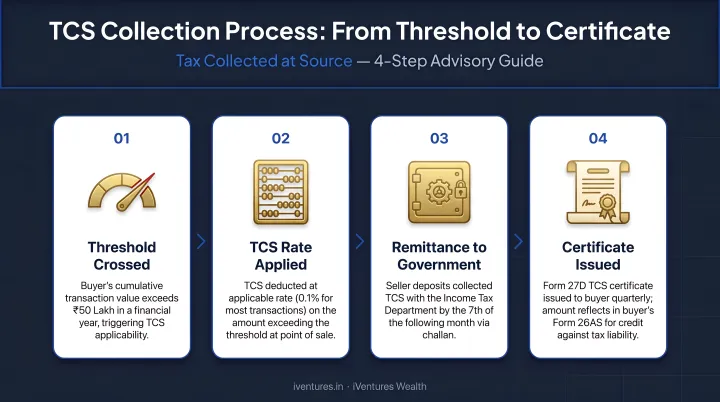

How TCS Is Calculated and Collected

The End-to-End Process

When you initiate an LRS remittance, your bank tracks cumulative outward remittances for the financial year against your PAN. Once your total crosses ₹10 lakh, TCS applies automatically to the amount above the threshold at the rate for your stated purpose.

Here's how the process flows:

- Threshold crossed — Bank flags your PAN once cumulative remittances exceed ₹10 lakh

- TCS collected — Per the Income Tax Department's TCS guide, collection happens at the earlier of account debit or receipt of payment

- Government deposit — Bank deposits TCS with the Central Government and reflects it against your PAN in Form 26AS

- Certificate issued — You receive Form 27D as your TCS certificate for the year

Worked Example 1: Self-Funded Education

A resident Indian remits ₹13 lakh for overseas tuition fees in a single financial year.

- Total remitted: ₹13 lakh

- TCS-free threshold: ₹10 lakh

- Taxable excess: ₹3 lakh

- Applicable rate: 2% (self-funded education)

- TCS collected: ₹6,000

The ₹6,000 is credited to your PAN and can be claimed back in your ITR if your total tax liability is less than the TCS collected.

Worked Example 2: Overseas Investment

A resident Indian remits ₹15 lakh to fund an overseas investment portfolio (no prior remittances in the year).

- Total remitted: ₹15 lakh

- TCS-free threshold: ₹10 lakh

- Taxable excess: ₹5 lakh

- Applicable rate: 20% (investment — "other purposes")

- TCS collected: ₹1,00,000

The same ₹15 lakh remitted for education would generate only ₹10,000 in TCS — a 10x difference driven entirely by purpose coding. Declaring the correct purpose to your bank directly determines which rate applies.

Note: No official CBDT source explicitly specifies a penalty for incorrect purpose coding. However, an incorrect declaration can result in a higher TCS deduction that you then need to recover through your ITR refund process — adding both delay and paperwork.

How to Claim Your TCS Refund

TCS paid under LRS is credited to your PAN as a tax credit. It appears in Form 26AS and the Annual Information Statement (AIS) on the Income Tax e-filing portal. If your total tax liability for the year is less than the TCS collected, you receive the difference as a refund.

Step-by-Step Claim Process

- Obtain Form 27D from your bank or authorised dealer after each TCS-applicable remittance — this is your certificate of collection

- Verify Form 26AS on the Income Tax e-filing portal to confirm the TCS amount is correctly reflected against your PAN

- File your ITR and claim the TCS as a tax credit under the relevant tax details section; any amount exceeding your final tax liability is processed as a refund

- Track your refund through the Income Tax portal's refund status tool once your ITR is processed

Where UHNIs and Affluent Families Face Complexity

For families making multiple large remittances across a financial year — overseas investment portfolios, children's tuition, maintenance of relatives abroad — the challenge is not claiming the credit. It is planning around it.

Consider a family that remits ₹8 lakh for a child's tuition in July, ₹6 lakh for a relative's maintenance in October, and ₹20 lakh for an overseas equity portfolio in January. Each transaction involves different TCS rates, different banks potentially, and the aggregate threshold is consumed early. The ₹20 lakh investment remittance alone generates ₹2 lakh in TCS at 20%.

Managing this across multiple remittance categories requires structured advisory support — not just compliance awareness. iVentures Wealth, a SEBI-registered RIA, works with HNI and UHNI clients on cross-border investment structuring under LRS, coordinating remittance documentation, consolidating capital gains statements, and preparing comprehensive tax reports that simplify ITR filing for chartered accountants.

Their Tax Optimisation service covers FEMA compliance, LRS structuring, and multi-jurisdiction coordination with tax advisors. This is built into their NRI/OCI Wealth Management and Family Office mandates.

Common Misconceptions About TCS on LRS

Common Misconceptions About TCS on LRS

Three misconceptions about TCS on LRS are widespread — and acting on any one of them can cost you money or create compliance gaps.

"TCS is an extra fee on foreign transfers"

No. TCS is advance tax collected on your behalf and deposited with the Income Tax Department against your PAN. If your annual tax liability equals or exceeds the TCS collected, it is fully set off. If your tax liability is lower, the surplus is refunded. For return-filing taxpayers, TCS is a cash flow timing issue — not an additional cost.

"The ₹10 lakh limit applies per bank or per transaction"

This is incorrect, and acting on it can be expensive. The ₹10 lakh threshold is a single annual aggregate per PAN — across all banks and all LRS purposes combined.

Consider a practical scenario:

- You remit ₹8 lakh through Bank A

- You then remit ₹4 lakh through Bank B

- TCS applies on ₹2 lakh at the applicable rate — regardless of which bank processes it

Banks collect this data via your LRS declaration, but tracking your own aggregate is your responsibility.

"NRIs sending money from Indian accounts are subject to TCS under LRS"

LRS is available exclusively to resident Indians, as defined under FEMA. NRIs are not LRS remitters. Repatriation of funds from NRE or NRO accounts is governed by separate RBI frameworks — including Master Direction No. 13 on Remittance of Assets and the Master Circular on NRO accounts. These transactions do not attract TCS under Section 206C(1G).

Frequently Asked Questions

What is LRS in TCS?

LRS (Liberalised Remittance Scheme) is the RBI framework allowing resident Indians to remit up to USD 250,000 abroad per financial year. Under Section 206C(1G) of the Income Tax Act, authorised banks collect TCS on outward remittances exceeding ₹10 lakh annually as advance tax against your income tax liability.

How much can I remit under LRS without paying TCS?

You can remit up to ₹10 lakh per financial year (April–March) across all LRS purposes and all banks combined without attracting TCS. Overseas tour packages are the exception — they carry 2% TCS from the first rupee, with no threshold exemption.

Is TCS on foreign remittance refundable?

Yes. TCS is credited to your PAN and appears in Form 26AS. If it exceeds your income tax liability, the surplus is refunded when you file your ITR — you'll need Form 27D from your bank and Form 26AS to support the claim.

What is the TCS rate for overseas education under LRS?

Loan-funded education remittances (from a specified financial institution) attract 0% TCS. Self-funded remittances above ₹10 lakh attract 2% on the excess, under rates effective April 1, 2026.

Does TCS apply to NRIs making foreign remittances from India?

No. TCS under LRS applies only to resident Indians under FEMA. NRIs are not eligible to remit under LRS and are not subject to LRS-related TCS when repatriating funds from NRE or NRO accounts.

What happens to TCS if my PAN is inoperative?

If your PAN is inoperative (due to non-linking with Aadhaar), Section 206CC applies — TCS on education and medical remittances above ₹10 lakh rises from 2% to 5%, while the 20% rate on other purposes holds. Linking your PAN with Aadhaar via the Income Tax e-filing portal restores standard rates.