Introduction

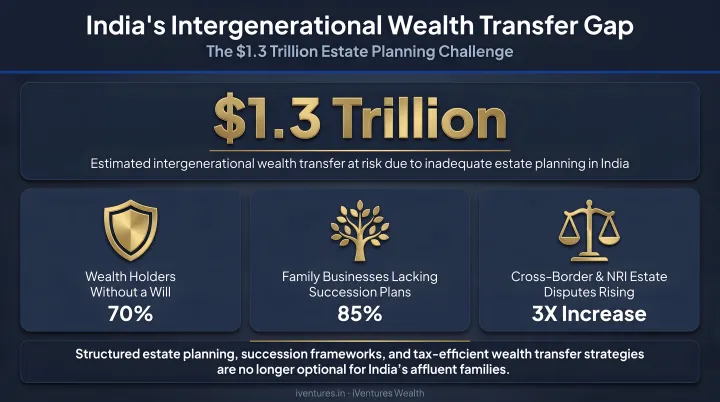

Indian families spend decades building wealth across equities, real estate, businesses, and retirement accounts. Yet according to a 2026 study reported by Mint, 84.8% of Indian households have no will, and 62.5% have no plans to create one.

For affluent families, the stakes are especially high. With multi-entity holdings, NRI beneficiaries, and complex business interests in the picture, an unstructured estate can fracture family relationships and erode generational wealth far faster than any market downturn.

Estate planning in India is more complex than most families recognise. A financial advisor — working alongside legal and tax professionals — plays a critical but often overlooked role: translating a legal document into a living, coordinated plan that actually holds up when it matters most.

Key Takeaways

- A nominee on a bank, mutual fund, or demat account is a custodian, not a legal heir — a will remains essential for proper succession

- Dying without a will means assets are distributed under personal succession law, which may not reflect your wishes

- A financial advisor handles asset inventory, beneficiary alignment, and team coordination; the lawyer handles legal drafting

- India has no inheritance tax, but capital gains and gift tax rules still require careful planning

- Estate plans need review after every major life event, not just when first created

What Is Estate Planning and Why Does It Matter for Affluent Indian Families?

Estate planning is the structured process of deciding how your assets will be managed, protected, and distributed — both during your lifetime and after. It goes well beyond "who gets what." A complete estate plan addresses:

- Healthcare and financial decisions during incapacity

- Business succession and ownership continuity

- Debt settlement and liability ring-fencing

- Tax efficiency across generations

The Nominee Misconception That Costs Families Dearly

Many affluent Indians assume that adding nominees across their accounts is enough. It is not.

The Supreme Court has addressed this twice in landmark rulings. In Sarbati Devi v. Usha Devi (AIR 1984 SC 346), the Court held that a nominee under an insurance policy does not acquire beneficial ownership — succession rights remain governed by succession law. More recently, in Shakti Yezdani v. Jayanand Jayant Salgaonkar (2023 INSC 1076), the Court confirmed that a nominee of shares or securities does not become the absolute owner to the exclusion of legal heirs.

Under SEBI's revised nomination rules effective March 1, 2025, nominees for sole-held demat accounts receive assets as trustees for legal heirs — not as owners. Across all asset classes, the legal position is the same: nominations facilitate collection, not ownership.

What Happens When There Is No Will

If you die intestate (without a will), your assets are distributed according to applicable personal law:

- Hindu Succession Act, 1956 for Hindus, Buddhists, Sikhs, and Jains

- Indian Succession Act, 1925 for others to whom its succession provisions apply

The prescribed order of heirs under these laws may differ substantially from your intentions. Business Standard reports that 30.5% of households have experienced inheritance disputes — a figure that climbs sharply when no succession documentation exists.

Why Affluent Families Face Greater Complexity

Standard succession law frameworks were not designed for:

- HUF structures, private limited companies, LLPs, and family trusts held simultaneously

- Founder stakes in unlisted businesses with no clear market price

- NRI or OCI family members with assets and tax obligations in multiple countries

- Complex beneficiary scenarios involving minor children, special needs dependants, or estranged relatives

EY and Julius Baer estimate India faces a USD 1.3 trillion intergenerational wealth transfer over the next decade, yet only 19% of families have adopted formal structures such as trusts. For affluent families managing layered asset structures, that 81% without formal planning is where disputes, tax drag, and unintended distributions originate.

What Does a Financial Advisor Do in Estate Planning?

A financial advisor acts as the financial coordinator of your estate planning team. The lawyer drafts the documents. The CA handles tax structuring. The advisor ensures the entire plan reflects your complete financial reality — not just isolated accounts.

Building the Asset Inventory

Before any succession structure can be designed, there needs to be a complete picture of what exists. A thorough inventory covers:

- Equity portfolios, demat accounts, and mutual fund folios

- EPF, PPF, NPS, and other retirement accounts

- Life insurance policies (sum assured, ownership, nominees)

- Real estate across multiple cities or countries

- Business interests: private limited companies, LLPs, HUF assets, partnership stakes

- Digital assets and overseas holdings

iVentures Wealth conducts this as a formal Asset Consolidation and Unified Family Balance Sheet exercise — the first step when a new UHNI client joins. The output is a single consolidated view across all asset classes, custodians, family members, and jurisdictions. Without this foundation, even a well-drafted will can leave assets unaccounted for, nominees misaligned, and families unprepared.

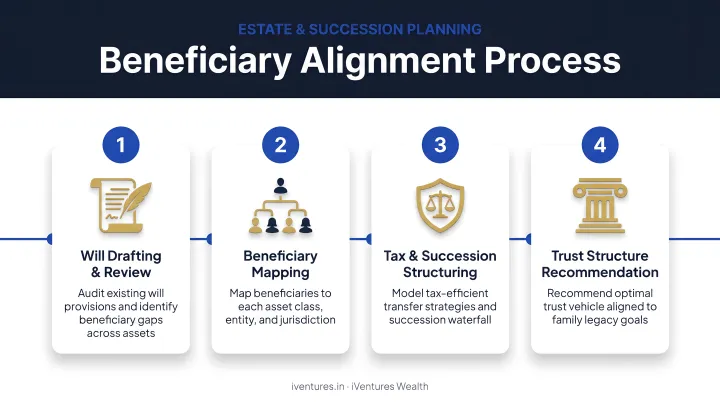

Beneficiary Alignment

With a complete asset picture in hand, the advisor reviews every account and folio to verify that nominations match the client's actual succession intent. These misalignments are common — and they typically go unnoticed for years. When they surface after a death, they cause family conflict, probate delays, and assets frozen in legal disputes.

The corrective process involves:

- Drafting a clear, legally valid will that documents inheritance intent

- Realigning nominations to support that documented intent

- Creating a consolidated asset listing accessible to the family

- Recommending trust structures where assets require additional protection

Coordinating the Planning Team

Estate planning requires at least three professionals working together: the financial advisor, the estate attorney, and the tax consultant. Their roles are distinct, but the plan only holds together when all three are working from the same information.

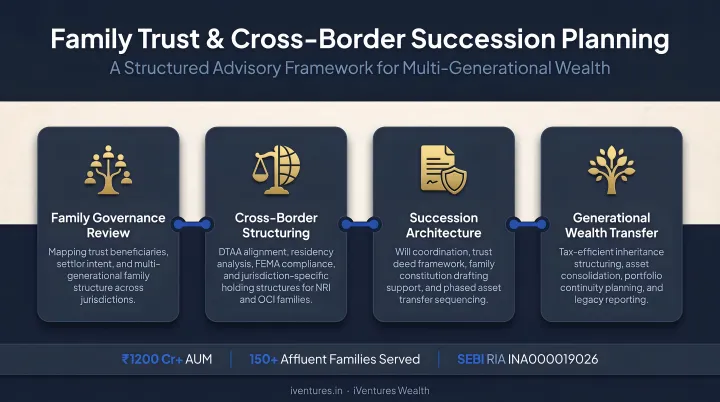

iVentures Wealth takes the coordination role seriously for UHNI and family office clients. The firm works with experienced legal practitioners, including Supreme Court-level counsel, for will drafting and executorship, and coordinates with tax advisors across Indian and foreign jurisdictions.

The financial advisor's specific job in this process is translation — converting the client's full asset picture into a form the lawyer can act on, so legal documents reflect actual holdings rather than a simplified summary.

Ongoing Monitoring

An estate plan written in 2020 may not reflect a 2025 family structure, asset base, or regulatory environment. As assets grow, laws change, family structures evolve, or new entities are formed, the plan needs to keep pace. A financial advisor reviews the plan periodically, flags regulatory changes (such as SEBI's 2025 nomination reforms), and ensures the structure remains implementable.

Key Estate Planning Tools Your Financial Advisor Should Help You Navigate

Wills

A will is the foundational document directing how assets are distributed after death. The Indian Succession Act, Section 2(h) defines a will as the legal declaration of the testator's intention regarding property to take effect after death. Execution requires the testator's signature and attestation by at least two witnesses under Section 63.

While registration is optional under the Registration Act, 1908, a registered will carries stronger evidentiary weight and reduces the risk of challenges. For complex estates, registration is strongly recommended.

Drafting the will is the lawyer's role. The financial advisor's job is to clarify which assets should pass through the will, confirm it aligns with the broader financial strategy, and flag any inconsistencies with existing nominations or trust structures.

Trusts

A private discretionary trust gives affluent Indian families structured, legally sound control over how wealth is distributed across generations. Under the Indian Trusts Act, 1882, a private trust requires certainty of intention, purpose, beneficiary, and trust property. Trusts of immovable property must be declared by a registered instrument or will.

Trusts are particularly useful when:

- Beneficiaries include minor children or dependants who should not receive large lump sums immediately

- Business assets need ring-fencing from personal creditors

- Multiple family members across geographies need structured, phased distributions

- Privacy and probate avoidance are priorities

iVentures structures discretionary, specific, and revocable trusts depending on the family's objectives and asset profile. In one documented case, a business owner with children settled overseas used a family trust to hold key business and property assets, aligned to cross-border tax and succession frameworks for NRI beneficiaries. The financial advisor's role is to assess whether a trust is appropriate given the client's net worth, family dynamics, and goals — and then coordinate with legal counsel to ensure the trust is properly funded and investment-aligned.

Nominations vs. Inheritance

Every financial account — mutual fund folio, demat account, EPF, bank deposit — has a separate nomination process, and each operates under different legal rules. The advisor's job is to map all nominations against the estate plan and explain what each nomination legally means in context.

EPF accounts add a further complication. Under the Employees' Provident Funds Scheme 1952 (Paragraph 61), a nomination in favour of a non-family person becomes invalid once the member acquires a family — and a prior nomination can be voided entirely.

Life Insurance and Power of Attorney

Sorting out nomination gaps often surfaces a related question: does the estate have enough liquid assets to meet immediate obligations? That's where life insurance becomes part of the planning conversation.

Life insurance provides liquidity for heirs to pay debts, taxes, or business obligations without being forced to sell assets. A financial advisor's role here includes:

- Reviewing whether the sum assured is adequate for estate settlement purposes

- Assessing whether the policy structure — term, whole life, keyman — fits the overall plan

- Flagging whether existing policies are correctly nominated and aligned to the will or trust

A financial power of attorney and advance healthcare directive are drafted by legal counsel. The financial advisor typically raises the need for both and ensures they are treated as required — not optional — components of a complete estate plan.

Tax-Smart Estate Planning: Minimising Your Family's Financial Burden

India abolished estate duty in 1985 and currently has no inheritance tax. But tax implications remain relevant in three areas.

Capital Gains on Inherited Assets

Under Section 49(1) of the Income Tax Act, 1961, when a capital asset passes by succession, inheritance, or will, the cost of acquisition for the heir is deemed to be the cost at which the previous owner acquired it. This means an heir inheriting equity or real estate bought decades ago carries the original (often very low) cost basis — and can face substantial capital gains tax when they sell.

Understanding this cost basis issue in advance allows a financial advisor to help families structure phased transfers or hold assets within structures that minimise eventual tax impact.

Gift Tax Treatment

Section 56(2)(x) of the Income Tax Act states that gifts received above ₹50,000 are taxable as income, except when received from specified relatives or through a will or inheritance. Gifts between spouses, parents, children, siblings, and certain extended family members are exempt.

This creates practical planning opportunities:

- Structured annual gifting to family members within exempt categories

- Transfers to adult children before wealth appreciation

- Use of HUF structures for appropriate income splitting

Gifts above ₹50,000 to non-relatives are fully taxable as income for the recipient.

NRI-Specific Considerations

Where NRI or OCI family members are involved, the complexity expands significantly across three dimensions:

- Repatriated inherited Indian assets must comply with RBI and FEMA guidelines — the RBI's Remittance of Assets FAQ covers applicable conditions and documentation

- India has DTAAs with over 90 countries, but capital gains treatment under treaties with the US, UK, and UAE each operate differently, requiring careful structuring before assets are transferred or sold

- The US and UK both impose estate or inheritance taxes; NRIs holding assets in those jurisdictions — or with US-person family members — need specific cross-border tax advice

iVentures coordinates with local counsel in the US, UK, UAE, Singapore, Canada, and Australia for clients with cross-border estate planning needs.

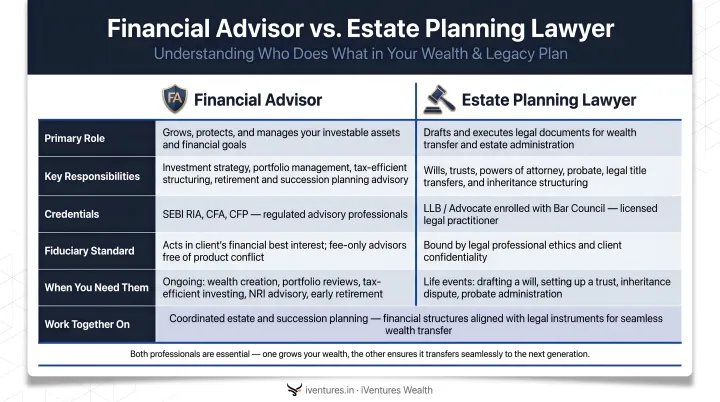

Financial Advisor vs. Estate Planning Lawyer: Who Does What?

The two roles are distinct and complementary. Neither can do the other's job effectively.

| Role | Financial Advisor | Estate Planning Lawyer |

|---|---|---|

| Legal document drafting | ✗ | ✓ Will, trust deed, POA, healthcare directive |

| Asset inventory and valuation | ✓ | ✗ |

| Beneficiary designation review | ✓ | ✗ |

| Structuring asset allocation | ✓ | ✗ |

| Translating financial picture for legal drafting | ✓ | ✗ |

| Enforcing legal documents | ✗ | ✓ |

| Coordinating tax consultant | ✓ | Shared |

| Ongoing plan monitoring | ✓ | Limited |

The table above captures role boundaries, but the more important dynamic is the handoff between them. The financial advisor translates the client's financial reality for the lawyer — communicating the nature of assets, holding structures, and distribution goals in terms that allow accurate, enforceable document drafting. Without this translation layer, lawyers draft documents that may not match what the client actually owns.

This is where the advisor's incentive structure becomes consequential. SEBI's Investment Advisers Regulations 2013 require registered investment advisers to act in a fiduciary capacity and disclose all conflicts of interest. An advisor operating under a distribution model earns commissions from products, which can skew recommendations toward insurance solutions over more appropriate trust or gifting structures.

iVentures charges a transparent advisory fee directly to clients, with no commission income from product manufacturers — ensuring every recommendation is shaped by the client's financial picture, not product margins.

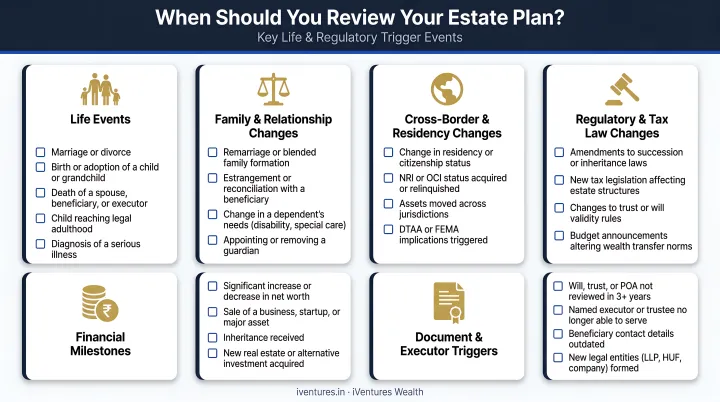

When Should You Review or Update Your Estate Plan?

FPSB India's Practice Standards require financial planning professionals to review and re-evaluate client situations when personal, economic, or legal circumstances change. There is no fixed statutory cadence, but a practical baseline is every three to five years — and immediately after any major life event.

Trigger events that require immediate review:

- Marriage or divorce

- Birth or adoption of a child or grandchild

- Death of a beneficiary or executor

- Significant increase or decrease in net worth

- Sale of a business or receipt of a large inheritance

- An NRI child returning to India or acquiring foreign citizenship

- Changes in applicable succession or tax law

- New regulatory requirements (such as SEBI's 2025 demat nomination reforms)

Three scenarios come up repeatedly for affluent Indian families and warrant extra urgency:

- A business founder listing the company — which changes asset valuation, ownership structure, and succession timelines overnight

- A family receiving assets from a deceased NRI relative, where cross-border estate obligations and repatriation rules apply

- A family member acquiring US citizenship, which shifts DTAA exposure and can create US estate tax liability on Indian assets held through certain structures

If any of these apply, a review shouldn't wait for the next calendar cycle — it should happen within weeks of the event.

Frequently Asked Questions

What is the difference between estate planning and financial planning?

Financial planning focuses on growing and protecting wealth during your lifetime — investments, retirement, insurance, and cash flow. Estate planning focuses on what happens to that wealth when you die or become incapacitated. The two are complementary and should be built together, not treated as separate exercises.

How much does financial advisory for estate planning cost?

Costs depend on estate complexity — will-only mandates, trust establishment, and cross-border coordination are each priced differently. iVentures uses mandate-based pricing for estate planning support, also available as part of its Family Office Service mandates.

Which bank accounts avoid probate in India?

Accounts with valid nominations — savings accounts, FDs, demat accounts, and mutual fund folios — generally allow nominees to claim assets without formal probate. However, nominees are legally required to distribute as per the will or succession law. Nominations simplify asset collection but are not a substitute for a properly drafted estate plan.

Do I need a will if I have nominees on all my accounts?

Yes. Nominees are custodians, not legal heirs under Indian law. Without a will, physical assets (property, jewellery), business interests, and jointly held assets may still be subject to succession laws or disputed claims. A will is essential even when all financial accounts have nominations in place.

When should I update my estate plan?

Trigger an immediate review after any major life event: marriage, divorce, birth of a child, death of a beneficiary, a significant asset change, or a business sale. Beyond that, a general review every three to five years is advisable as tax laws and SEBI regulations evolve.

Can a financial advisor help with succession planning for a family business?

Yes. A financial advisor can help structure how business interests — shares, LLP stakes, or private company holdings — are valued, transferred, and protected across generations, working alongside legal counsel and a CA for tax structuring. iVentures has specific experience with business-owning families, including family trust establishment and succession coordination.