That distinction — between setting a long-term allocation and actively adjusting it — is the core of the Strategic Asset Allocation (SAA) vs Tactical Asset Allocation (TAA) debate. For Indian UHNIs, founders, and affluent families managing ₹5 Cr+ portfolios, getting this right can mean the difference between riding out volatility with confidence or suffering avoidable drawdowns ahead of a critical liquidity event.

Key Takeaways

- SAA sets a fixed long-term target allocation, rebalanced periodically to stay aligned with goals

- TAA makes short-term, research-backed deviations from that baseline to manage risk or capture market opportunities

- SAA suits investors with long horizons who prioritise compounding and cost efficiency

- Those managing near-term risk — particularly ahead of a liquidity event — are better served by TAA

- Sophisticated portfolios use both in tandem: SAA as the structural foundation, TAA as a managed, short-term overlay

Strategic vs Tactical Asset Allocation: Quick Comparison

| Dimension | Strategic Asset Allocation (SAA) | Tactical Asset Allocation (TAA) |

|---|---|---|

| Time Horizon | Long-term (10+ years) | Short-to-medium term (months to 3 years) |

| Approach | Passive, rule-based | Active, research-driven |

| Rebalancing Frequency | Annual or threshold-triggered | Ongoing, as conditions change |

| Risk Management Style | Accept market cycles; rebalance to targets | Proactively reduce or increase exposure |

| Transaction Costs & Tax | Low — fewer short-term capital gains (STCG) events | Higher — frequent shifts can trigger STCG |

| Ideal Investor Profile | Long-horizon, goal-oriented, hands-off | Near-term event, volatile environment, expert-advised |

SAA and TAA aren't competing strategies — they answer different questions. SAA defines where your wealth is anchored long-term; TAA determines how it responds when markets shift. Which one takes precedence depends on your goals, investment horizon, and whether current conditions call for active positioning or disciplined patience.

What is Strategic Asset Allocation?

Strategic Asset Allocation (SAA) is a long-term portfolio framework where an investor sets fixed target allocations across asset classes — say, 60% equities, 30% debt, and 10% gold or alternatives — based on risk tolerance, financial goals, and time horizon. The portfolio is then periodically rebalanced back to those targets regardless of short-term market conditions.

How Rebalancing Works in Practice

Imagine equity markets rally strongly over 12 months. What started as a 60% equity allocation has drifted to 70%. SAA discipline requires selling some equity and buying debt or other assets to restore the original 60% target. Most advisors recommend doing this annually, or when any asset class drifts beyond a set threshold — typically ±5%.

Vanguard's 2022 rebalancing research found that annual rebalancing hits the cost-benefit sweet spot, delivering a 51-basis-point advantage over daily rebalancing, and identified a 3% threshold as optimal for a 60/40 portfolio where tracking error tolerance is tight.

Why SAA Works for Indian Investors

For Indian investors specifically, SAA delivers on three fronts that matter:

- Emotional discipline — removes the temptation to react to Nifty swings or RBI policy announcements

- Tax efficiency — fewer transactions mean fewer Short-Term Capital Gains (STCG) events; post-Budget 2024, STCG on equity funds is taxed at 20% (for transfers on or after 23 July 2024), making unnecessary churn costly

- Simplicity — low monitoring burden, lower advisory costs, and fewer decisions that can go wrong

The Core Limitation

SAA keeps the portfolio fully exposed through every market cycle. During a severe correction, an SAA portfolio absorbs the full drawdown and must wait for recovery. For investors with a 15+ year horizon, that's manageable. For someone 18 months from a business sale or retirement, it isn't.

Where SAA Fits Best

- Long-horizon investors (10+ year runway) building intergenerational wealth

- Family offices and trusts with a wealth preservation mandate

- Founders and CXOs running a diversified allocation across equity, debt, REITs, and international funds — and want compounding without constant intervention

- Investors who prefer a low-monitoring, goal-linked approach

What is Tactical Asset Allocation?

TAA is an active, shorter-term approach where deliberate, temporary deviations are made from the strategic baseline to manage specific risks or capture market opportunities. It is not a wholesale portfolio change — it functions as an overlay on strategy, applied within defined limits.

How TAA Works in Practice

A portfolio manager might overweight short-duration debt and gold ahead of an anticipated rate hike cycle, or temporarily reduce equity exposure when valuations appear stretched. These shifts are triggered by economic indicators, valuation analysis, technical signals, or macro data — not market noise or emotional reactions.

SEBI's September 2024 study found that 93% of individual equity F&O traders incurred losses between FY22 and FY24, with aggregate losses exceeding ₹1.8 lakh crore. While F&O trading differs from TAA, the conclusion applies: undisciplined, ad hoc active positioning destroys capital.

The Case for TAA When Done Right

When executed with discipline, TAA adds a layer of protection and opportunity that a fixed allocation simply cannot provide:

- Reduces downside exposure before market corrections hit

- Captures short-term opportunities a fixed SAA would miss entirely

- Particularly relevant during India's RBI rate cycles and global risk-off phases

The Risks and Costs

TAA is not cheap. More frequent trading increases transaction costs and — critically for Indian investors — can trigger STCG tax at 20% on equity holdings held under 12 months. That tax drag must be factored into any tactical decision.

The SPIVA India Year-End 2025 Scorecard reinforces this caution: 84% of Indian large-cap active funds underperformed their benchmark over 5 years, and 96.5% of composite bond funds underperformed over 10 years. Consistent outperformance through active timing is genuinely difficult — which is why TAA demands rigorous research processes, disciplined execution, and clear decision rules, not just market conviction.

Where TAA Is Most Appropriate

- Investors within 2–3 years of a major liquidity event (business sale, retirement)

- Portfolios requiring active risk management during volatile macro environments

- Clients whose advisors operate with documented, research-driven frameworks — not discretionary calls made under pressure

Illustrative scenario: A business owner is 24 months from selling their company. A pure SAA approach leaves them fully exposed to equity volatility during the run-up to the sale. A TAA overlay that reduces equity exposure, shifts toward sovereign bonds and liquid funds, and adds gold as a hedge protects capital when it matters most — without abandoning the long-term allocation framework.

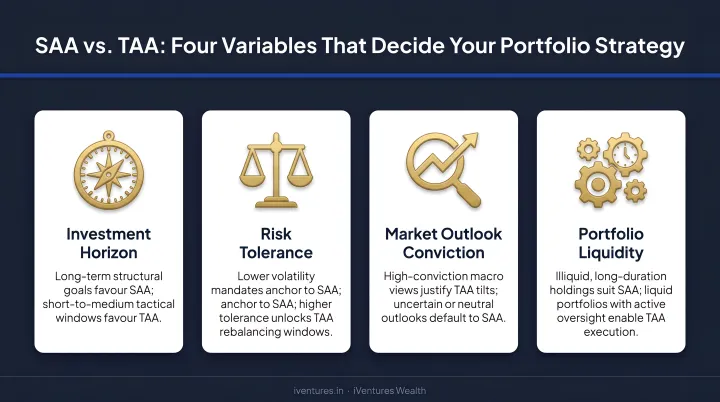

Which Approach Is Right for You?

The answer depends on four variables:

- Investment time horizon — how many years before capital is needed

- Risk tolerance and drawdown capacity — can you absorb a 30–40% equity correction without panic or forced selling?

- Liquidity needs and life events — are you 18 months from a business exit, or 15 years away?

- Access to expert advisory — do you have a disciplined, research-backed advisor, or are you making tactical calls yourself?

Choose SAA If:

- You have a 10+ year horizon

- You prefer compounding over active management

- You have no imminent liquidity needs

- You want low costs and tax efficiency as a priority

Add a TAA Overlay If:

- You are within 3–5 years of a major financial event

- Markets are in an identifiable transitional phase (RBI cutting cycle, stretched valuations, global risk-off)

- You are working with an advisor who has a proven, process-driven approach — and who evaluates every tactical shift net of tax impact

The Case for a Blended Approach

For most sophisticated investors — UHNIs, family offices, and business owners — neither approach works in isolation. The more effective structure uses SAA as the long-term foundation and layers a limited TAA overlay within defined guardrails for risk management and opportunity capture.

The SAA anchors the portfolio to long-term goals. The TAA responds to changing conditions without letting short-term market views override the overall strategy.

iVentures Wealth's CFA-led advisory team builds this kind of blended strategy for affluent clients — combining periodic rebalancing, tactical allocation calls, and a fee-only, open-architecture model that removes product bias. As a SEBI-registered RIA (INA000019026), iVentures does not accept commissions or trail income from product manufacturers. Every tactical recommendation reflects research and client objectives — not distributor economics.

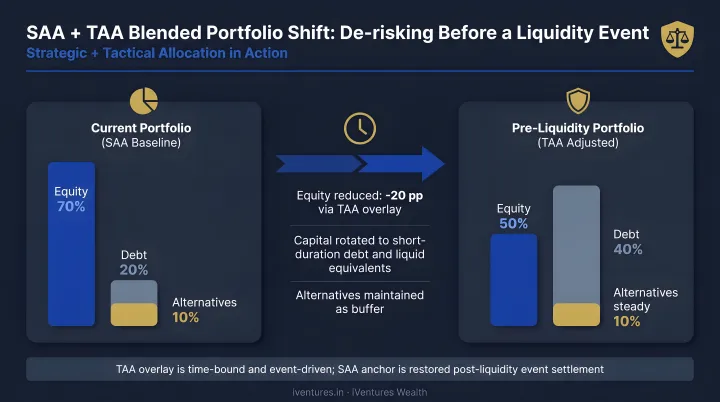

A Real-World Illustration: How a Blended Approach Works

Consider an affluent Indian family with a ₹5 Cr+ portfolio, a 10-year wealth goal, and a business transition expected within 18 months. Their existing SAA — 65% equity, 25% debt, 10% alternatives — was appropriate for a long-horizon investor. But with a liquidity event approaching, the same allocation created meaningful risk.

The Problem With a Static SAA at This Life Stage

A correction of even 30–35% in equity markets 12 months before the business sale would significantly impair the family's financial position at the worst possible moment. The portfolio needed to honour the long-term strategy while acknowledging the near-term reality.

What the Blended Approach Looked Like

The advisory team maintained the core SAA framework — preserving the logic of long-term diversification — while implementing a tactical overlay based on valuation signals and macro analysis:

- Equity reduced from 65% to 45%

- Sovereign bonds and liquid funds increased to provide capital protection and liquidity

- Gold allocation added as a portfolio hedge

This was a structured, research-driven adjustment to reduce drawdown risk ahead of a known capital event — not speculative market-timing. Morningstar's long-run analysis of balanced portfolios shows that when equities had lost 47.2% from a previous high, a diversified 60/40 portfolio had lost just 24.7%. Even a modest allocation shift can materially reduce peak drawdown during severe corrections.

The Takeaway

The most effective portfolios integrate SAA and TAA — not as competing frameworks, but as complementary tools calibrated to each client's life stage. A fiduciary advisor brings the research depth to make tactical shifts credibly and the discipline to avoid making them without cause.

Conclusion

SAA and TAA are tools, not opposites. SAA provides the discipline, long-term goal alignment, and cost efficiency that every wealth-building portfolio needs as its foundation. TAA adds the flexibility to protect capital and capture opportunities when conditions — and the investor's life stage — demand it.

For Indian investors navigating evolving tax rules, RBI rate cycles, and dynamic global markets, a well-structured allocation strategy is essential at the ₹5 Cr+ level. The choice between SAA and TAA depends on knowing your goals, your horizon, and your risk tolerance well enough to build a portfolio that serves your financial life across every phase of it — not just the one you're currently in.

Frequently Asked Questions

What is the difference between SAA and TAA?

SAA sets a fixed long-term target allocation — such as 60% equity and 40% debt — rebalanced periodically back to that baseline. TAA makes active, temporary deviations from that baseline based on market conditions or specific risk events. TAA works best as an overlay on SAA, not as a replacement for it.

Is 70/30 better than 60/40?

Neither is universally superior. A 70/30 portfolio (higher equity) suits investors with longer horizons and higher risk tolerance. A 60/40 split is more appropriate for those closer to capital preservation goals. The right split depends entirely on your specific time horizon, financial objectives, and drawdown capacity.

Can strategic and tactical asset allocation be used together?

Yes — most UHNI and institutional portfolios combine both. SAA forms the long-term foundation, while TAA operates as a disciplined overlay within defined limits, managing risk or capturing short-term opportunities without disrupting the core strategy.

How often should you rebalance under strategic asset allocation?

Most advisors recommend annual rebalancing, or threshold-based rebalancing when any asset class drifts more than 5% from its target. In India, rebalancing frequency matters for tax reasons — frequent rebalancing can trigger STCG at 20% on equity holdings sold within 12 months of purchase.

Is tactical asset allocation suitable for long-term investors?

TAA alone is not well-suited for long-term investors — it adds cost, complexity, and timing risk. A limited TAA overlay on a core SAA framework, however, can add value during specific market phases or key life-stage transitions.

What are the tax implications of tactical asset allocation in India?

TAA's more frequent trading can trigger Short-Term Capital Gains (STCG) tax at 20% on equity sold within 12 months (for transfers on or after 23 July 2024), versus 12.5% LTCG on gains above ₹1,25,000. Every tactical shift should be evaluated net of this tax impact before execution.