But this is also the decade where mistakes are hardest to recover from. A poor investment decision at 35 gives you 25 years to course-correct. The same mistake at 55 gives you almost none.

According to the Axis Max Life India Retirement Index Study 5.0, India's retirement preparedness index stands at just 48 out of 100 — with 31% of urban Indians not having started retirement investments and another 31% unsure their savings will last through retirement. For professionals in their 50s, that gap is unacceptable at this stage.

This guide walks through exactly what to do — step by step — to master financial planning in your 50s, with specific reference to Indian tax rules, investment instruments, and the planning variables that determine how comfortable your retirement will actually be.

Key Takeaways

- Your 50s are your last high-income window — use NPS, VPF, PPF, and equity SIPs to their full potential

- Shift your portfolio from accumulation mode to a preservation-and-growth balance

- Healthcare inflation in India is projected at 13.8% for 2025 (Aon) — plan for it explicitly

- Estate planning, tax restructuring, and a drawdown strategy must be formalised before you retire

- A SEBI-registered fiduciary adviser integrates your net worth, obligations, and tax position into one coherent plan

Why Financial Planning in Your 50s Looks Different

Financial planning in your 30s and 40s is largely about accumulation — building assets, growing income, and riding compounding over long time horizons. Your 50s demand a different mindset entirely.

The priorities shift to three things:

- Consolidation — are your assets structured efficiently, or scattered across dormant folios, overlapping funds, and underperforming FDs?

- Stress-testing — will your corpus sustain 25-30 years of retirement, factoring in healthcare and inflation?

- Transition — moving from income-generating to income-drawing mode requires a plan, not improvisation

The Sandwich Generation Problem

Many professionals in their 50s face simultaneous financial pressure from multiple directions. The Axis Max Life IRIS 5.0 survey identifies India's sandwich generation as having particularly low retirement preparedness — with 76% worried about becoming financially dependent on their children and only **55% feeling secure about future family support**.

Supporting aging parents, funding children's education or weddings, and saving aggressively for retirement all compete for the same cash flows. Without explicit goal separation, retirement savings consistently lose out.

Poor investment decisions, tax inefficiency, or coverage gaps leave far less runway for recovery at this stage than at any earlier one.

How to Master Financial Planning in Your 50s: A Step-by-Step Approach

Step 1: Conduct a Complete Financial Audit

Before you can fix anything, you need a precise picture of where you stand.

Start with your net worth:

- List every asset — mutual funds, stocks, EPF balance, PPF, NPS, real estate, FDs, business equity, overseas holdings

- Subtract all liabilities — home loan outstanding, personal loans, guarantees given

- The resulting number is your starting point

Then calculate your retirement gap:

Estimate your projected monthly expenses in retirement — at today's prices — and adjust upward for India's healthcare and lifestyle inflation. The PGIM India Retirement Readiness Survey 2025 found that only 37% of Indians have a formal retirement plan. A corpus calculator helps you translate your monthly expense target into the lump sum required at retirement, accounting for assumed returns and a planning horizon of age 85-90.

For HNI and UHNI families with assets scattered across brokers, demat accounts, PMS providers, and real estate, this audit goes well beyond a spreadsheet. iVentures Wealth's Asset Consolidation service is designed for exactly this: surfacing dormant accounts, overlapping holdings, and duplicate fees into a single unified family balance sheet before any restructuring begins.

Step 2: Maximise and Accelerate Retirement Contributions

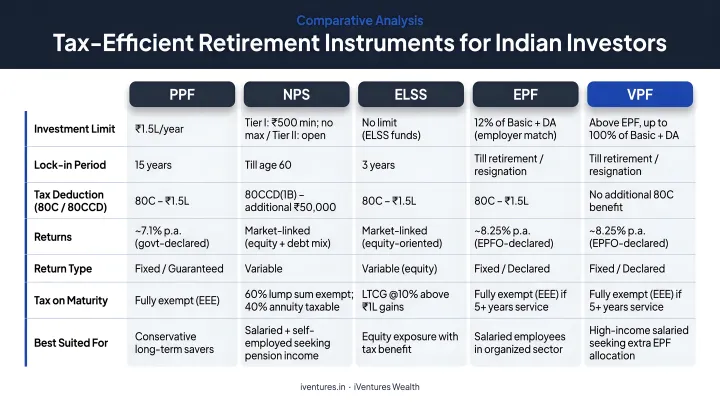

Your 50s are your last real window for large, consistent contributions. Use every tax-efficient instrument available:

| Instrument | Key Benefit | Annual Limit |

|---|---|---|

| NPS (Section 80CCD(1B)) | Additional ₹50,000 deduction over 80C limit | ₹50,000 (extra) |

| NPS Employer (Section 80CCD(2)) | Up to 14% of salary deductible under new regime | Salary-linked |

| PPF | EEE status — contribution, interest, maturity all tax-efficient | ₹1,50,000/year |

| VPF (Voluntary PF) | Same returns and tax treatment as EPF | Up to ₹2.5 lakh/year before taxability threshold |

| ELSS | 80C benefit with equity growth potential | Within ₹1.5 lakh 80C limit |

The concept of "catch-up saving" matters here. If your corpus is behind schedule, increasing monthly SIP amounts meaningfully in your 50s — even with a 10-12 year runway to retirement — can significantly improve the final corpus. Compounding in the final decade is more powerful than most investors expect — consistent contributions now can recover years of underfunding.

Step 3: Restructure Your Portfolio for the Transition Phase

An equity-heavy portfolio that served you well in your 40s needs recalibration in your 50s — but the opposite mistake is equally dangerous.

The balance to strike:

- Staying fully in aggressive equity leaves you exposed: a major downturn 2 years before retirement can permanently damage your corpus

- Fleeing entirely to FDs is equally costly: with retirement lasting 25-30 years, you need real growth to stay ahead of inflation

- Move toward large-cap equity, hybrid funds, and quality debt instruments progressively

Sequence-of-returns risk is the real danger. As the CFA Institute notes, how markets perform in the first few years of retirement disproportionately determines retirement outcomes. Even if markets recover later, early drawdowns on a depleted corpus cannot be fully recovered.

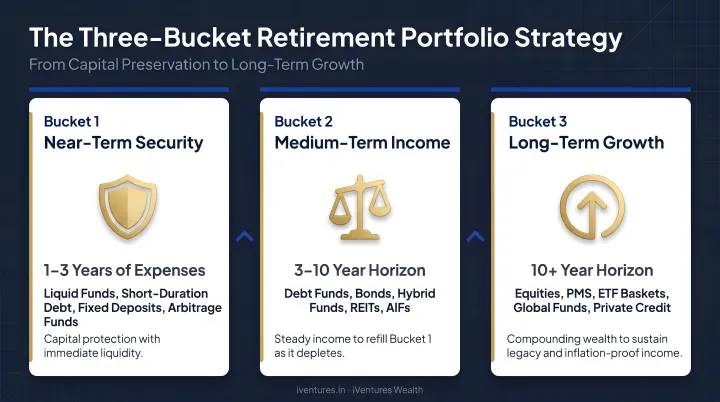

The bucket strategy addresses this directly:

- Near-term (Years 1-3): Keep 2-3 years of expenses in liquid, low-volatility instruments such as liquid funds and short-duration debt

- Medium-term (Years 3-8): Hold 3-8 years of expenses in debt funds and balanced hybrid funds

- Long-term (Year 8+): Leave the remaining corpus in diversified equity, continuing to grow

iVentures Wealth implements this structure for clients transitioning out of active income — including glide-path planning in the 5 years pre-retirement to systematically de-risk into a balanced and debt mix before the drawdown phase begins.

Step 4: Plan for Healthcare and Protection Needs

Healthcare is the biggest financial wildcard in Indian retirement — and the most consistently underestimated.

India's National Health Accounts 2021-22 reports household out-of-pocket expenditure at ₹3,56,254 crore — 39.4% of total health expenditure. Aon's 2025 data projects India's medical trend rate at 13.8%, compared to a global average of 10.4%.

At 13.8% annual medical inflation, a hospitalisation that costs ₹5 lakh today will cost nearly ₹20 lakh in 10 years.

What to do now:

- Secure a comprehensive health insurance policy with a sum insured of ₹25-50 lakh or higher — for yourself and your spouse — before any pre-existing conditions develop

- Build a dedicated medical emergency corpus in liquid assets, separate from your retirement corpus

- Account for healthcare inflation explicitly in your retirement corpus calculation — not just lifestyle inflation

On life insurance: by your 50s, assess whether your existing coverage still fits your situation. If dependents are financially independent and major liabilities are cleared, the need diminishes. If either condition is unmet, ensure adequate term coverage remains in place.

Step 5: Build a Tax Strategy and Estate Plan

On taxation — two critical updates for 2024-25:

- Equity mutual fund LTCG: Gains above ₹1,25,000 are now taxed at 12.5% for transfers on or after July 23, 2024 (previously 10% above ₹1 lakh)

- Debt mutual funds: Units acquired on or after April 1, 2023 no longer benefit from indexation — gains are treated as short-term capital gains under Section 50AA and taxed at your slab rate

Review your debt fund portfolio in light of this change. Existing pre-April 2023 debt fund holdings may have different tax treatment — your adviser should map this before you rebalance.

Tax moves specific to your 50s:

- Compare old vs. new tax regime annually, especially if you claim 80C, 80D, and 80CCD(1B) deductions

- Use Section 80D aggressively — senior citizen parents qualify for up to ₹50,000 deduction on health insurance premiums

- Structure retirement income across NPS annuity, tax-free PPF withdrawals, and SWP from mutual funds to minimise taxable income in retirement

On estate planning:

A Mint report on an India study found that 84.8% of Indian households do not have a Will — and 62.5% have no plans to create one. For HNI families, this is a significant risk.

Estate planning in your 50s must include:

- A current, legally valid Will drafted and registered

- Correct nominees across all financial accounts, insurance policies, and demat accounts

- Clarification on joint ownership structures — nominees are custodians, not legal heirs

- For complex estates with business interests, real estate, and multiple family members: a private trust structure may be appropriate

iVentures Wealth coordinates end-to-end estate planning, including Will drafting vetted by senior legal practitioners, private trust establishment, and cross-border inheritance structuring for NRI families.

Key Factors That Determine How Comfortable Your Retirement Will Be

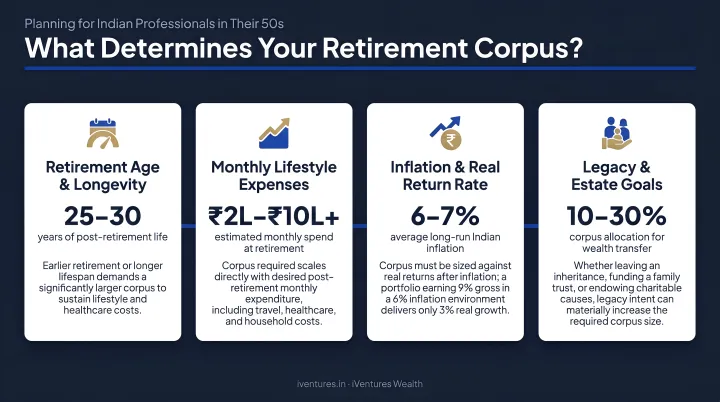

Four variables drive your required retirement corpus — and changing even one significantly alters the number:

- Retirement age — retiring at 55 versus 60 requires a meaningfully larger corpus and 5 fewer years of contribution

- Monthly expenses in retirement — adjusted for healthcare and lifestyle inflation, not just CPI

- Return assumptions — both during accumulation and drawdown phases; The Actuary India estimates India's adjusted safe withdrawal rate at 2.69% after accounting for local inflation and returns

- Life expectancy — plan to age 85-90 for a conservative, responsible estimate

The SWP Advantage Over FDs

A Systematic Withdrawal Plan from a diversified mutual fund portfolio offers several advantages over simply parking money in FDs:

- FD interest is taxed at your slab rate every year; SWP redemptions from equity funds benefit from LTCG treatment above ₹1.25 lakh threshold

- The remaining corpus stays invested and compounds; FD principal is static

- As Mirae Asset Mutual Fund notes, there is no TDS on capital gains from mutual funds for resident individual investors — unlike FDs

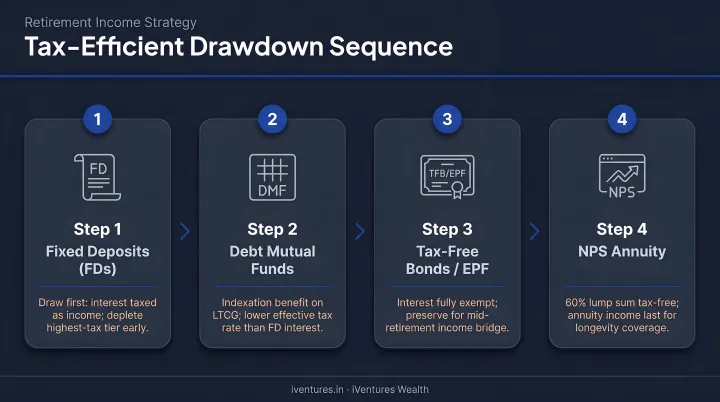

The order in which you draw from these sources matters as much as the sources themselves. A tax-efficient sequencing strategy typically follows this structure:

- Start with taxable sources first (FDs, non-deductible savings)

- Draw from equity mutual funds via SWP through retirement years

- Use PPF corpus last — it's tax-free and benefits from remaining invested longer

- NPS annuity provides regular income but is taxable; factor this into overall income planning

Ring-Fence Your Retirement Corpus

Without deliberate separation, family obligations quietly drain retirement savings. Common culprits include:

- Children's higher education abroad

- Wedding costs

- Aging parent medical expenses

Goal-based investing — with separate, labelled portfolios for each objective — keeps these goals from competing with your retirement corpus.

For affluent families managing complex portfolios across equities, real estate, business equity, and multiple accounts, a consolidated portfolio view is the missing link. iVentures Wealth's unified dashboard spans all asset classes and family members, giving advisers the visibility to reduce tax drag, spot concentration risk, and align the full wealth picture to a single retirement goal.

Common Financial Planning Mistakes to Avoid in Your 50s

Being Overly Conservative Too Soon

Moving everything into FDs at 50 feels safe — but the math works against you. With India's CPI inflation running around 5-6% annually and FD rates pre-tax in the 6-7% range — post-tax real returns can be near zero or negative for those in the 30% tax bracket. A corpus invested only in FDs effectively provides no real growth over a 25-30 year retirement.

Mixing Goals in a Single Corpus

Using one pool of money for retirement, children's education, emergencies, and family events is the most common compounding killer. When a family expense arises or markets fall, money gets pulled from the retirement corpus — destroying the long-term trajectory. Separate, ring-fenced portfolios by goal are not optional; they're structural.

Delaying Estate Planning and Insurance Review

Health conditions that develop in the late 50s can make it impossible to obtain adequate coverage at reasonable premiums. A Will that hasn't been updated in a decade may no longer reflect your actual asset structure. Both become harder — and more expensive — to fix later.

Excluding Healthcare from Retirement Corpus Calculations

Most investors estimate their corpus based on lifestyle expenses and ignore healthcare. Healthcare costs tend to increase exponentially after 65-70 — building a dedicated medical emergency fund alongside comprehensive insurance is simply accurate planning, not excessive caution.

When to Seek Professional Financial Guidance

Financial planning in your 50s involves tax strategy, estate law, insurance, investment rebalancing, and goal mapping simultaneously. A generic approach rarely holds up for affluent individuals with complex financial lives.

That complexity is exactly where a SEBI-registered investment adviser (RIA) operating as a true fiduciary earns its value — advising purely in the client's interest, earning no commissions from product sales. Firms like iVentures Wealth, with 20+ years of experience managing wealth for 150+ affluent families, CEOs, and founders across India, provide this kind of personalised, conflict-free advisory for professionals and families with investable assets of ₹10 crore or more.

Signs it's time to bring in professional guidance:

- Net worth has grown complex — multiple real estate assets, business equity, scattered financial instruments

- You're within 5-10 years of your target retirement date

- Significant family events — inheritance, business sale, divorce — have changed your financial picture

- You're uncertain whether your current corpus will realistically last through retirement

- You've never had a consolidated view of your total assets across all accounts and entities

In your 50s, a poorly structured tax exit or an overlooked estate clause can erase years of careful wealth-building. The right adviser helps you avoid those gaps before they become expensive.

Frequently Asked Questions

What is the best investment at age 50?

There's no single best product. A balanced mix typically includes equity mutual funds for long-term growth, NPS for tax benefits and retirement income, and debt funds for stability. The right split depends on your existing corpus, years to retirement, and risk capacity.

Is ₹2 crore enough to retire at 50?

It depends heavily on your monthly expenses, healthcare costs, life expectancy, and portfolio returns. Mint's analysis of the ₹2 crore retirement question suggests that at modest monthly spends with reasonable inflation and return assumptions, the corpus may last only 15-18 years — making early retirement at 50 risky for most Indian families without additional income streams.

What is the 3-6-9 rule in finance?

The 3-6-9 rule refers to emergency fund sizing: 3 months of expenses for stable single earners, 6 months for families or self-employed individuals, and 9 months for retirees or those approaching retirement. In your 50s, maintaining a 6-9 month emergency buffer in liquid instruments protects your retirement corpus from being disturbed during unexpected events.

What is Warren Buffett's advice for investors over 50?

Buffett advocates staying invested in diversified, low-cost assets for the long term — avoiding market timing, high-fee products, and over-conservative positions driven by short-term volatility. His 2013 shareholder letter directed his wife's bequest be placed 90% in a low-cost index fund and 10% in short-term government bonds, underscoring that equity remains relevant even in later life.

How should I rebalance my portfolio in my 50s?

The general approach is to gradually shift from equity-heavy toward a more balanced equity-debt allocation — but not to exit equities entirely. A rough guide is to use your age as a proxy for your debt allocation (50% debt at age 50), then review annually and adjust based on your specific retirement timeline and risk capacity.

How do I plan for rising healthcare costs in retirement in India?

Secure a comprehensive health policy (₹20-50 lakh sum insured or higher) before any conditions develop, and build a separate medical corpus in liquid assets alongside it. When sizing your retirement corpus, factor in healthcare inflation at 10-14% annually — well above general CPI — to avoid a significant shortfall later.