The process isn't complicated once you understand the rules, but it has enough NRI-specific nuances — residential status, form selection, TDS refunds, DTAA claims — that a generic tax guide won't serve you well. This one will.

Key Takeaways

- ITR filing is mandatory if Indian income exceeds ₹2.5 lakh (old regime) or ₹4 lakh (new regime), or if specific financial thresholds are crossed

- Only income earned or received in India is taxable — your foreign income is not

- NRIs must use ITR-2 or ITR-3, not ITR-1 or ITR-4

- DTAA benefits can prevent double taxation — but only with a valid Tax Residency Certificate and Form 10F

- Voluntary filing — even when not required — helps recover TDS refunds, carry forward capital losses, and build financial credibility in India

Who Needs to File ITR as an NRI?

The Basic Threshold

Under the Income Tax Act, 1961, ITR filing is mandatory when your taxable Indian income exceeds the basic exemption limit. For AY 2026-27, those limits are:

- New regime (default): ₹4,00,000

- Old regime: ₹2,50,000

One common source of confusion: "taxable income" here means gross total income before applying Chapter VI-A deductions (like Sections 80C or 80D) and before capital gains reinvestment exemptions under Sections 54, 54EC, or 54F. Many NRIs underestimate their filing obligation by netting out deductions first.

Additional Mandatory Filing Triggers

Even if income stays below the exemption limit, filing is mandatory when any of these apply:

- Deposits exceeding ₹1 crore in current accounts

- Foreign travel expenses over ₹2 lakh paid from Indian accounts

- Electricity expenditure over ₹1 lakh

- Business turnover over ₹60 lakh or professional receipts over ₹10 lakh

- Aggregate TDS/TCS of ₹25,000 or more

- Savings account deposits of ₹50 lakh or more

That said, one provision carves out a clear exception for passive investors.

When Filing Is NOT Required

Under Section 115G, an NRI need not file if total Indian income consists only of investment income, LTCG, or both — and TDS has already been fully deducted at source under Chapter XVII-B. For example, an NRI holding listed Indian securities whose only Indian income is dividends and LTCG, with TDS correctly deducted by the payer, qualifies for this exemption.

Why Voluntary Filing Makes Sense Anyway

Filing even when exempt often costs less than missing these advantages:

- TDS refunds — NRO interest and rental income are often subject to TDS at 30%, which may exceed actual tax liability

- Carry forward capital losses — losses from Indian investments can offset future gains, but only if a return is filed

- Financial credibility — ITR receipts support visa applications, home loan approvals, and other documentation requirements in India

- Foreign tax credits — your country of residence may require proof of Indian tax paid to allow a credit against your local tax bill

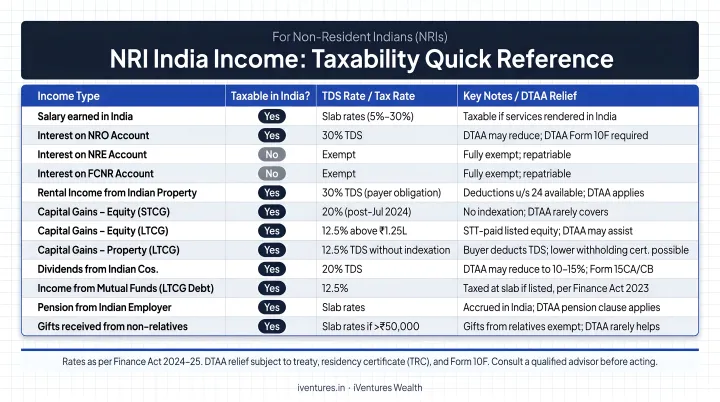

What Income Is Taxable for NRIs in India?

NRIs are taxed only on income that arises or is received in India. Foreign income — salary from a US employer, rental income from a UK property — is not taxed in India at all. This is the sharpest contrast with resident status, where global income is fully taxable.

Income Type Quick Reference

| Income Type | Taxability | Notes |

|---|---|---|

| Salary for services in India | Fully taxable | Taxable regardless of where salary is received or credited |

| Rental income from Indian property | Fully taxable | Standard house property computation applies |

| NRO account interest | Fully taxable | TDS at 30% under Section 195 |

| NRE account interest | Fully exempt | Exempt under Section 10(4)(ii) |

| FCNR account interest | Fully exempt | Exempt under Section 10(15)(iv)(fa) |

| Dividends from Indian companies | Taxable | TDS at 20% under Section 115A/195, subject to DTAA |

| LTCG from Indian property/assets | Taxable | TDS at 12.5% applicable on buyer side |

| STCG on listed equity (STT paid) | Taxable at 20% | Under Section 111A for AY 2026-27 |

Capital Gains: What NRI Sellers Need to Know

When an NRI sells Indian property, the buyer is required to deduct TDS at 12.5% on LTCG. This creates a liquidity impact upfront — the seller receives net proceeds and must claim any excess TDS as a refund through the ITR.

Reinvestment exemptions can reduce or eliminate this tax liability, but they must be actively claimed:

- Section 54: LTCG from a residential house reinvested in another residential house

- Section 54EC: Gains invested in specified bonds within six months of sale

- Section 54F: Gains from long-term assets other than a residential house

These exemptions don't apply automatically. Each requires reinvestment within prescribed timelines and must be claimed in the ITR.

Special Provision: Section 115E

If an NRI invests in specified Indian assets — shares or debentures of Indian companies, government securities — using foreign currency, the resulting investment income is taxed at a flat 20% under Section 115E, without access to Section 80 deductions. If this investment income (or LTCG from these assets) is the NRI's only Indian income and TDS has been fully deducted, the Section 115G filing exemption may apply.

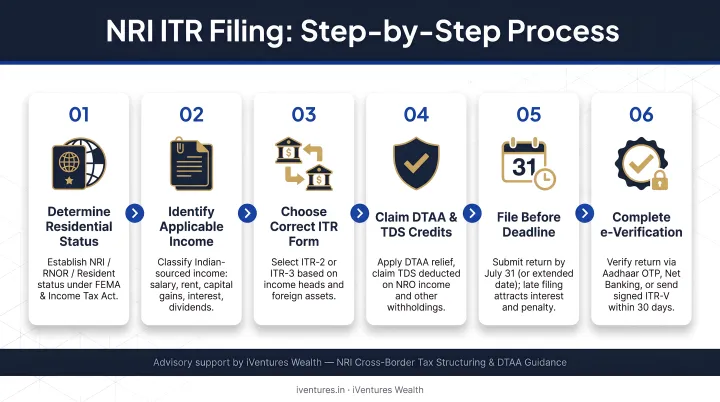

Step-by-Step Guide to Filing ITR as an NRI

The deadline for NRIs without audit requirements is July 31 of the assessment year — identical to the resident deadline. Filing happens on the Income Tax portal at incometax.gov.in. Here's what each step involves.

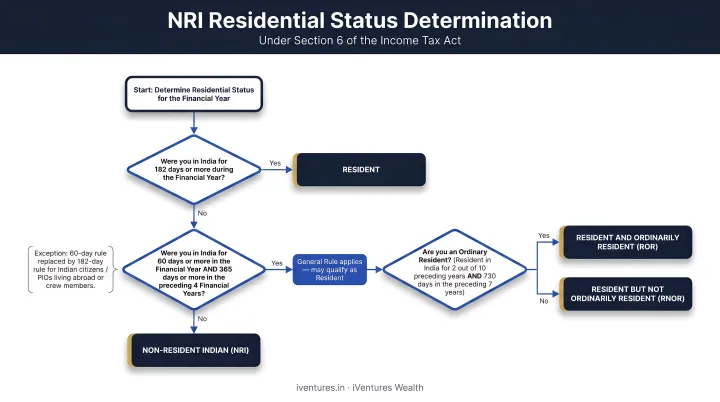

Step 1: Determine Your Residential Status

Under Section 6 of the Income Tax Act, you're classified as a resident if you meet either of these conditions:

- Spent 182+ days in India during the financial year

- Spent 60+ days in the current year AND 365+ days across the preceding four years (general rule)

- For Indian citizens and PIOs visiting India, the 60-day threshold is raised to 182 days; from FY 2020-21, it drops to 120 days if Indian income exceeds ₹15 lakh

Misclassifying residential status is one of the costliest compliance errors NRIs make. Even visits for medical or family reasons count toward the threshold — and crossing it makes global income taxable in India.

Step 2: Compute Total Indian Taxable Income

Total all India-sourced income across every category:

- Salary for services rendered in India

- NRO account interest

- Rental income from Indian property

- Capital gains from Indian assets

- Dividends from Indian equities or funds

NRE and FCNR interest is exempt from tax, but it must still be reported under the "Exempt Income" schedule (Schedule EI) in the ITR.

Before filing, cross-check all figures against Form 26AS and the Annual Information Statement (AIS) on the e-filing portal. Discrepancies between what you report and what these documents show can trigger scrutiny.

For NRIs with multiple Indian income sources — NRO accounts, equities, real estate — consolidating this data accurately before filing is often the most time-consuming part of the process. iVentures Wealth works with NRI clients to prepare clean, consolidated income and capital gains reports, reducing errors and delays during filing season.

Step 3: Choose Your Tax Regime

The new tax regime is the default from FY 2023-24. Key differences for NRIs:

| New Regime | Old Regime | |

|---|---|---|

| Basic exemption | ₹4,00,000 | ₹2,50,000 |

| Section 80C/80D deductions | Not available | Available |

| Section 87A rebate | Not available to NRIs | Not available to NRIs |

The Section 87A rebate is a resident-only benefit. NRIs cannot claim it under either regime — a point many NRIs miss, sometimes resulting in incorrect tax calculations. Compare actual tax liability under both regimes before deciding; the right choice depends on the size and nature of your Indian income and deduction eligibility.

Step 4: Select the Correct ITR Form and File Online

- Log in to incometax.gov.in using PAN credentials

- Select the applicable Assessment Year

- Choose ITR-2 (salary, house property, capital gains, interest — covers most NRIs) or ITR-3 (if business/professional income exists in India)

- Fill in income details across all applicable schedules

- If claiming DTAA benefits, ensure TRC and Form 10F are submitted

Step 5: Enter Bank Account Details Correctly

NRIs must report all Indian bank accounts held during the financial year (except dormant accounts). Refunds can only be credited to NRO accounts — not NRE accounts. If no Indian account exists, foreign bank details can be provided, but the account must be pre-validated and EVC-enabled on the portal.

Step 6: Verify the Filed Return

An unverified ITR is treated as not filed. Verification options include Aadhaar OTP (requires Aadhaar-PAN linkage), net banking, demat account EVC, or Digital Signature Certificate. Without digital access, print and sign the ITR-V and mail it to CPC, Income Tax Department, Bengaluru 560500 within 30 days of filing.

Key Tax Considerations: Old vs. New Regime, DTAA, and Deductions

Deductions Available to NRIs (Old Regime Only)

| Section | Benefit | Limit |

|---|---|---|

| 80C | Life insurance, ELSS, home loan principal | Up to ₹1.5 lakh |

| 80D | Health insurance premiums | ₹25,000–₹50,000 |

| 80E | Education loan interest | No monetary cap |

| 80G | Qualifying donations | Varies by recipient |

| 80TTA | Savings bank interest | Up to ₹10,000 |

What NRIs cannot claim: Sections 80DD, 80DDB, and 80U (disability-related deductions) are for resident Indians only. NRIs also cannot open new PPF accounts or invest in NSC and post office deposit schemes — instruments restricted to residents under 80C.

Under the new regime, most Chapter VI-A deductions are unavailable regardless of residency status — the regime choice, not NRI status, determines this.

Beyond deductions, NRIs with income in multiple countries have another layer of relief available through treaty benefits.

DTAA: How Double Taxation Relief Works

India has signed DTAA treaties with 90+ countries under Section 90 of the Income Tax Act, covering relief across income types including salary, rent, capital gains, and interest. Two methods apply in practice:

- Exemption method: Income is taxed in only one country

- Credit method: Tax paid in India can be offset against tax liability in the country of residence

To claim DTAA benefits, you must submit a Tax Residency Certificate (TRC) from the foreign country's tax authority and Form 10F (self-declaration under Rule 21AB). Without these documents, the standard withholding rate applies, and DTAA benefits cannot be claimed retroactively.

NRIs based in the US, UK, UAE, Singapore, Canada, and Australia face additional complexity — particularly around PFIC/GILTI exposure for US persons — where tax-efficient portfolio structuring (not just treaty claims) becomes critical to minimising overall tax drag.

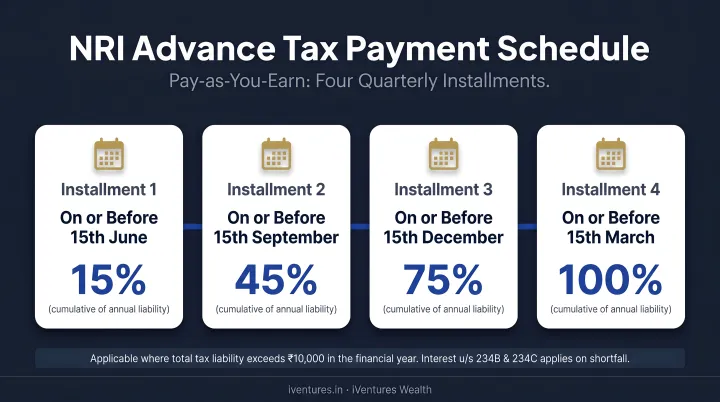

Advance Tax Obligations

If estimated Indian tax liability exceeds ₹10,000 in a financial year, NRIs must pay advance tax in four quarterly instalments:

- 15% by June 15

- 45% by September 15

- 75% by December 15

- 100% by March 15

Failure to pay triggers interest under Sections 234B and 234C. NRIs with rental income or capital gains — where TDS may not have been deducted at the correct rate — are particularly exposed to this obligation.

Common Mistakes NRIs Make When Filing ITR

Most ITR errors made by NRIs fall into three categories: misreading residential status, mishandling the filing and refund process, and misapplying DTAA or deduction rules.

Classification Errors

- Misidentifying residential status: An extended India stay — even for medical, family, or pandemic reasons — can satisfy the 182-day or 120-day threshold and make global income taxable here. Days in India must be tracked across the full financial year

- Claiming the Section 87A rebate: This is a residents-only benefit. NRIs cannot claim it under either regime, and it's one of the more common errors in self-filed returns

Classification errors aside, the filing and refund process itself has several trip points that even experienced NRIs miss.

Filing and Refund Process Errors

- Using an NRE account for refunds: Refunds can only be credited to NRO accounts. Providing NRE details causes the transaction to fail

- Skipping bank account pre-validation on the e-filing portal — this step must be completed before any refund can be processed

- Omitting NRE/FCNR interest from Schedule EI: Even though this income is exempt, leaving it out can trigger scrutiny

- Missing the 30-day ITR verification window: An unverified return is treated as never filed

DTAA and capital gains deductions carry their own layer of complexity, where assumptions tend to be the costliest.

DTAA and Deduction Misconceptions

- Assuming DTAA exemption removes the filing requirement: It does not. Treaty benefits must be claimed through the ITR itself, with the TRC and Form 10F submitted alongside

- Claiming resident-only deductions: PPF, NSC, and Sections 80DD/80DDB/80U are not available to NRIs under either regime

- Missing reinvestment timelines for Sections 54, 54EC, and 54F: These capital gains exemptions are not automatic — reinvestment must happen within prescribed windows or the exemption lapses

Frequently Asked Questions

Can NRIs file ITR in India?

Yes — and they often must. Filing is mandatory if Indian income exceeds the basic exemption limit or if specific high-value transaction thresholds are triggered. Voluntary filing also makes sense to claim TDS refunds, carry forward capital losses, and maintain clean financial records in India.

Which ITR form is required for NRIs?

Most NRIs file ITR-2, which covers salary, house property, capital gains, and interest income. If business or professional income in India is also involved, ITR-3 applies. NRIs cannot use ITR-1 or ITR-4 — both are restricted to resident individuals.

What happens if an NRI files using the wrong ITR form?

Filing the wrong form — for example, using ITR-1 instead of ITR-2 — renders the return defective under Section 139(9). The Income Tax Department issues a defective notice, and the taxpayer must refile using the correct form within 15 days. Persistent non-compliance can lead to the return being treated as not filed, triggering penalties under Section 234F.

What is the due date for NRI ITR filing in India?

The deadline is July 31 of the assessment year for NRIs without audit requirements. Late filing between August 1 and December 31 attracts a penalty under Section 234F (₹5,000, capped at ₹1,000 if total income is under ₹5 lakh). Interest on unpaid taxes accrues separately under Sections 234A, 234B, and 234C.

Can NRIs claim DTAA benefits to avoid double taxation?

Yes, if India has an active DTAA with the NRI's country of residence. To claim relief, the NRI must submit a Tax Residency Certificate from the foreign country and Form 10F at the time of filing. Treaty rates often differ significantly from standard TDS rates — for example, India's DTAA with the UAE provides full exemption on certain income types, while the US treaty caps withholding at 15% on dividends.

Is interest on an NRE account taxable in India?

No — interest on NRE and FCNR accounts is fully exempt from Indian income tax under Sections 10(4)(ii) and 10(15)(iv)(fa) respectively. However, this income must still be reported under Schedule EI (Exempt Income) in the ITR. By contrast, NRO account interest is fully taxable and subject to TDS at 30%.