The challenge is compounded by a structural gap: unlike the US or UK, India has no universal social security net. According to a PFRDA speech citing the India Employment Report 2024, 81% of India's labour force was in the unorganised sector in 2022 — meaning the vast majority of working Indians have no employer-sponsored pension or formal retirement savings at all.

This guide covers the best pension and retirement plans available in India in 2026 — what each plan offers, who it suits, and how to build a strategy that actually holds up over a 20–30 year retirement.

Key Takeaways

- NPS delivers the highest combined tax deduction (up to ₹2 lakh/year) with market-linked growth — best for long-term corpus building

- EPF/VPF offers guaranteed returns with full EEE tax status — the default choice for salaried employees

- PPF is the go-to for conservative, tax-free accumulation among self-employed individuals and business owners

- SCSS provides guaranteed quarterly income at 8.2% p.a. — suited for those already retired

- A blended strategy across NPS, PPF, and equity mutual funds produces the most resilient retirement outcome

Overview of Pension and Retirement Planning in India

India's retirement landscape differs fundamentally from Western models. There is no universal state pension equivalent to the UK's National Insurance or the US Social Security system. The government has expanded coverage through NPS (for government and private sector workers) and Atal Pension Yojana (for unorganised sector workers), but eligibility conditions apply.

Social security coverage has grown significantly — from 19% in 2015 to 64.3% in 2025 per PIB — but that figure includes all forms of formal social protection, not retirement pensions specifically. For most self-employed individuals, gig workers, and small business owners, retirement funding remains entirely self-driven.

Three realities make this gap consequential:

- A ₹1 crore corpus today will be worth roughly ₹55–60 lakh in purchasing power 10 years from now at 5% inflation

- Healthcare costs tend to rise faster than general CPI, adding further pressure

- Retiring at 60 and living to 90 means funding a 30-year retirement — a drawdown challenge most Indians haven't planned for

Given these pressures, choosing the right plan requires more than picking the highest-return option. Each plan reviewed below is assessed across five criteria:

- Regulatory safety — sovereign or SEBI-regulated backing

- Return potential — real returns after inflation

- Tax efficiency — deduction and withdrawal treatment

- Liquidity — access to funds before and after retirement

- Suitability — fit across income profiles and life stages

Best Pension and Retirement Plans in India 2026

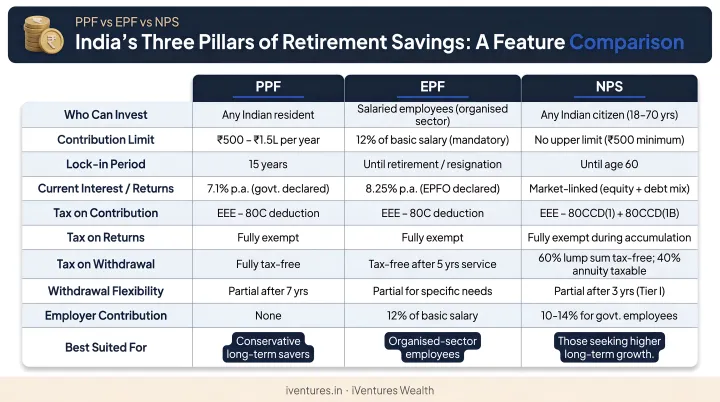

National Pension System (NPS)

NPS is a government-introduced, PFRDA-regulated defined-contribution plan open to Indian citizens and NRIs aged 18–70. Contributions are invested across equity, corporate bonds, and government securities through PFRDA-registered Pension Fund Managers.

What makes NPS stand out:

- Highest combined tax deduction available: ₹1.5 lakh under Section 80C/80CCE plus an exclusive additional ₹50,000 under Section 80CCD(1B) — no other instrument offers this extra deduction

- At retirement (age 60), 60% of the corpus can be withdrawn as a tax-free lump sum under Section 10(12A)

- Low fund management costs compared to most mutual funds

- Self-employed individuals can claim deductions up to 20% of gross income under Section 80CCD(1)

| Feature | Detail |

|---|---|

| Eligibility | Indian citizens and NRIs, aged 18–70 |

| Returns | Market-linked; Scheme E (equity) has historically delivered strong long-term growth |

| Tax Benefits | Deduction up to ₹2 lakh/year; 60% lump sum at retirement is tax-free |

| Withdrawal | Min. 40% used to purchase annuity; premature exit eligibility now 5 years per 2025 PFRDA amendment |

Note on premature exit: A December 2025 PFRDA amendment updated premature exit eligibility to 5 years for the All Citizen Model. Verify current rules directly on the PFRDA website before acting.

Employees' Provident Fund (EPF) / Voluntary Provident Fund (VPF)

EPF is mandatory for salaried employees in organisations with 20 or more employees. Both employee and employer contribute 12% of basic salary each — making it India's closest equivalent to an employer-matched retirement plan. VPF lets EPF members contribute voluntarily above the mandatory 12% at the same interest rate.

The EPF interest rate for FY 2024–25 was 8.25%, and the Central Board of Trustees recommended the same rate for FY 2025–26 (pending final confirmation from EPFO).

Why EPF/VPF works as a retirement foundation:

- Government-guaranteed fixed return — no market risk

- Full EEE (Exempt-Exempt-Exempt) tax status when withdrawn after 5 years of continuous service

- Employer's matching contribution adds approximately 3.67% of basic salary to your EPF account annually (the remainder goes to EPS)

- VPF contributions earn the same guaranteed rate with no additional lock-in complexity

| Feature | Detail |

|---|---|

| Eligibility | Salaried employees in eligible organisations; VPF open to all EPF members |

| Returns | 8.25% p.a. (FY 2024–25 confirmed; FY 2025–26 recommended at same rate) |

| Tax Benefits | Full EEE status on withdrawal after 5 years of continuous service |

| Withdrawal | Full withdrawal at retirement (age 58); partial withdrawals permitted for specific needs |

Public Provident Fund (PPF)

PPF is a 15-year government-backed small savings scheme open to all Indian residents — not NRIs. It is particularly relevant for self-employed individuals, freelancers, and business owners who lack EPF access. The current rate is 7.1% p.a., compounded annually, though rates are reviewed quarterly by the DEA.

PPF is one of the very few instruments in India offering full EEE status: contributions qualify under Section 80C, interest accrues tax-free, and the maturity amount is entirely exempt.

Key structural advantages:

- Contributions of ₹500 to ₹1.5 lakh per year

- 15-year lock-in with partial withdrawals permitted from the 7th year

- Account can be extended in 5-year blocks post-maturity, continuing to compound tax-free

- No market risk — government-backed fixed rate

| Feature | Detail |

|---|---|

| Eligibility | All Indian residents (excluding NRIs); minors via parents |

| Returns | 7.1% p.a. compounded annually (verify latest quarterly DEA circular) |

| Tax Benefits | Full EEE — contribution (80C), interest, and maturity all tax-free |

| Withdrawal | 15-year lock-in; partial withdrawals from 7th year; extendable in 5-year blocks |

Senior Citizens' Savings Scheme (SCSS)

SCSS is designed for retirees, not accumulation. It offers one of the highest guaranteed rates among small savings schemes — currently 8.2% p.a. — with quarterly interest payouts directly to a linked bank account.

Who it suits: Anyone aged 60+ (or 55+ for VRS/superannuation retirees) who needs predictable quarterly cash flow rather than further corpus growth.

| Feature | Detail |

|---|---|

| Eligibility | Indian residents aged 60+; 55+ for VRS/superannuation retirees |

| Returns | 8.2% p.a. with quarterly payouts (verify latest DEA rate before investing) |

| Tax Benefits | Investment qualifies under Section 80C; interest taxable above ₹50,000/year (TDS applies) |

| Withdrawal | 5-year tenure, extendable by 3 years; premature closure allowed with penalty |

| Deposit Limit | Maximum ₹30 lakh per individual |

The TDS caveat is worth noting: for retirees with no other significant income, SCSS interest may stay below taxable thresholds, but high-income retirees will pay income tax on the full interest amount.

Retirement Mutual Funds (SIP-Based Equity and Hybrid Funds)

Equity and hybrid mutual funds are not pension plans in the regulatory sense, but they are widely used — and for good reason — as the growth engine of retirement portfolios, particularly for HNIs, self-employed professionals, and those with a 15–25 year investment horizon.

Why mutual funds belong in retirement planning:

- Long-term equity funds have historically delivered inflation-beating compounding over 15–20 year horizons (verify current CAGR data from AMFI's official fund performance portal)

- Long-term capital gains (LTCG) on equity funds above ₹1.25 lakh are taxed at 12.5% under Section 112A, without indexation — still lower than income tax slab rates applicable to most fixed-income instruments for high earners

- No mandatory lock-in for regular funds; SEBI's dedicated retirement fund category carries a 5-year lock-in or till age 58, whichever is earlier

- The mutual fund industry AUM reached ₹65.74 lakh crore in March 2025

| Feature | Detail |

|---|---|

| Eligibility | Any Indian resident or NRI with valid KYC; no age restriction |

| Returns | Market-linked; historically strong over 15–20 year horizons (verify with AMFI data) |

| Tax Benefits | LTCG at 12.5% above ₹1.25 lakh threshold; no indexation on equity funds |

| Withdrawal | No mandatory lock-in for regular funds; retirement fund category: 5 years or till age 58 |

For HNIs with larger retirement corpora, Portfolio Management Services (PMS) and Alternative Investment Funds (AIFs) — including private credit AIFs targeting consistent quarterly distributions — can complement mutual funds within an advisory framework. iVentures Wealth's advisory team structures such multi-asset retirement portfolios across NPS, equity funds, and private credit for HNI and UHNI clients.

Immediate Annuity Plans (Private Life Insurers)

Immediate annuity plans — offered by LIC (Jeevan Akshay-VII), HDFC Life, ICICI Prudential, and SBI Life — convert a lump sum corpus into a guaranteed lifelong income. They are especially relevant for retirees converting their NPS or EPF maturity proceeds into a predictable monthly pension.

The core tradeoff: annuity income is guaranteed for life (addressing longevity risk directly), but the entire income is fully taxable as per income tax slab under Section 80CCC. For retirees in the 30% bracket, this significantly reduces net yield.

Key considerations before purchasing:

- Annuity rate is locked at purchase — it doesn't change with interest rates later

- Rate depends on age, corpus, insurer, and payout option (life only, joint life, return of purchase price)

- No liquidity post-purchase in most structures; surrender is possible in some policies with penalty

- NPS subscribers are already mandated to use 40% of their corpus to purchase an annuity

| Feature | Detail |

|---|---|

| Eligibility | Typically ages 40–85; varies by insurer and plan option |

| Returns | Fixed annuity rate locked at purchase; varies by insurer and age |

| Tax Benefits | No deduction on lump sum invested (unless from NPS); full annuity income taxable at slab |

| Withdrawal | Generally no withdrawal; surrender available in some plans with penalty |

For high-income retirees in the 30% tax bracket, annuities often lose their appeal on an after-tax basis. Alternatives — Systematic Withdrawal Plans (SWPs) from equity funds, bond ladders using G-Secs and AAA corporate bonds, or private credit AIFs with quarterly distributions — frequently deliver better post-tax income.

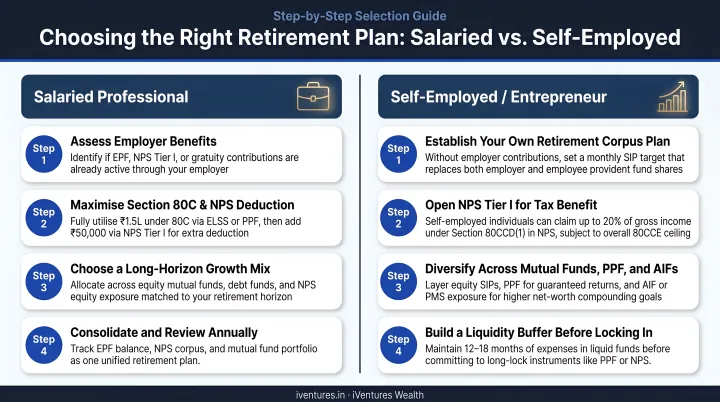

How to Choose the Right Pension and Retirement Plan

The single biggest mistake in retirement planning is treating it as a tax-saving exercise. Picking NPS or PPF purely for Section 80C benefits — without thinking about liquidity, withdrawal structure, or whether the plan generates income or just corpus — is how people arrive at retirement underprepared.

Match Plans to Employment Type

Salaried employees should build in this order:

- Max out EPF/VPF first — guaranteed return, employer match, full EEE status

- Add NPS Tier I for the exclusive ₹50,000 deduction under 80CCD(1B)

- Use equity mutual fund SIPs for surplus beyond the above

Self-employed professionals and business owners have no EPF access and should anchor around:

- NPS — deduction up to 20% of gross income under 80CCD(1) plus ₹50,000 under 80CCD(1B)

- PPF — for tax-free, fixed-return accumulation

- Equity mutual fund SIPs — for long-horizon growth

Accumulation vs. Income — Get the Distinction Right

Two different types of plans serve two different purposes:

- Accumulation vehicles (NPS, EPF, PPF, equity mutual funds): Build corpus during working years

- Income vehicles (SCSS, Immediate Annuity): Generate regular cash flow post-retirement

A complete retirement strategy needs both — something building wealth during your career and something converting it into income after.

Start Early — the Numbers Change Dramatically

A 25-year-old investing the same monthly amount as a 40-year-old into NPS and equity SIPs will accumulate a materially larger corpus by age 60. The difference is exponential, driven by 15 additional years of compounding. The NPS Trust's official calculator at npstrust.org.in lets you model this directly with your own numbers.

Beyond Standard Tax Limits for High Earners

Individuals earning ₹50 lakh+ annually exhaust the ₹80C/80CCD ceiling quickly. A broader retirement strategy for this segment spans multiple layers:

- International diversification through global ETFs and GIFT City funds under LRS

- AIFs targeting consistent cash flows and structured equity strategies

- Real estate income as a hedge against inflation

For NRIs and OCIs, the picture gets more complex — DTAA structuring, NRE/NRO account optimisation, and repatriation planning all need coordinating alongside domestic retirement assets.

That level of complexity is exactly where an independent adviser adds the most value. iVentures Wealth (SEBI RIA No. INA000019026) builds retirement strategies around your actual financial picture — not around product commissions. As a fee-only RIA, iVentures charges a transparent advisory fee with no trail income or kickbacks from product manufacturers.

Conclusion

India in 2026 offers a solid range of retirement instruments — from government-guaranteed options like EPF, PPF, NPS, and SCSS to market-linked choices like equity mutual funds and private annuity plans.

The best outcomes come from blending accumulation and income instruments in proportions suited to your age, income, risk tolerance, and retirement timeline. No single product does all the work.

Review your retirement allocation at least every two to three years, and after significant life events: a salary increase, job change, tax law amendment, or shift in family circumstances can all justify rebalancing.

For HNIs, UHNIs, business owners, and NRIs seeking a retirement strategy beyond standard plan selection, iVentures Wealth offers SEBI-registered advisory with 20+ years of experience and ₹1,200+ crore under advice. The firm's open-architecture model means every recommendation reflects your goals, not distribution incentives. Reach out for a personalised consultation at ria@iventures.in or connect on WhatsApp at +91 99999 85119.

Frequently Asked Questions

Which is the best pension plan for retired persons?

SCSS is the most practical choice for guaranteed quarterly income at 8.2% p.a., while Immediate Annuity Plans suit those deploying a large lump sum corpus. The right combination depends on corpus size, income needs, and tax bracket.

How to get ₹50,000 pension per month in India?

You need a corpus of roughly ₹85–90 lakh at a 7% withdrawal rate, or closer to ₹1 crore at 6%. In practice, blend SCSS payouts, NPS annuity, and SWP from equity or debt mutual funds — calibrated to your tax bracket and liquidity needs.

What is the "Rule of 7" for retirement?

The term is used inconsistently — sometimes referencing a 7% safe withdrawal rate, sometimes a variation of the Rule of 72. In Indian retirement planning, a 6–7% real return above inflation serves as the standard benchmark for sustainable long-term withdrawals, though no regulator has formalised this figure and the right rate varies by portfolio and retirement horizon.

What is the difference between NPS and PPF for retirement planning?

NPS is market-linked with higher return potential and an exclusive ₹50,000 deduction under 80CCD(1B), but requires at least 40% annuitisation on exit. PPF offers a fixed government-declared rate (currently 7.1%), full EEE tax status, and complete withdrawal flexibility post-15 years — making it simpler and more liquid at maturity.

At what age should I start investing in a pension plan in India?

Start as early as possible — ideally by 25–30 — to maximise the compounding effect across a 30–35 year accumulation horizon. Starting at 40 is not too late, but requires higher contributions and a more aggressive equity allocation to reach the same corpus target.

Is NPS a good investment for self-employed professionals in India?

Yes. NPS is particularly well-suited for doctors, founders, and consultants who lack EPF access. The deduction ceiling of 20% of gross income under 80CCD(1), plus the additional ₹50,000 under 80CCD(1B), makes it the most tax-efficient accumulation vehicle available to the self-employed — and the investment mix across equity, corporate bonds, and G-Secs can be adjusted to suit individual risk preference.