Introduction

For decades, the 60/40 portfolio — 60% equities, 40% bonds — was the default framework for affluent investors. It worked well when stocks and bonds moved in opposite directions and fixed income delivered real yields. That assumption broke down badly in 2022, when a U.S. 60/40 portfolio fell 17.5%, driven by simultaneous equity selloffs and bond losses as inflation and aggressive rate hikes pushed stock-bond correlation to positive territory.

Nifty 50's P/E of 20.27 leaves little margin in public equities, and traditional fixed income faces its own headwinds in India. Public markets, at these valuations, offer less room for error.

This is why sophisticated Indian investors — UHNIs, family offices, founders, and CXOs — are looking beyond public markets. This article covers:

- What alternative asset allocation actually means

- Which asset classes are relevant for Indian investors

- How to size an alternatives sleeve within a portfolio

- What risks to plan for before committing capital

Key Takeaways

- The 60/40 portfolio's diversification benefit depends on a negative stock-bond correlation — one that has historically broken down during inflationary and crisis periods

- Alternatives span private equity, real estate, private credit, commodities, and hedge strategies — each serving a distinct portfolio purpose

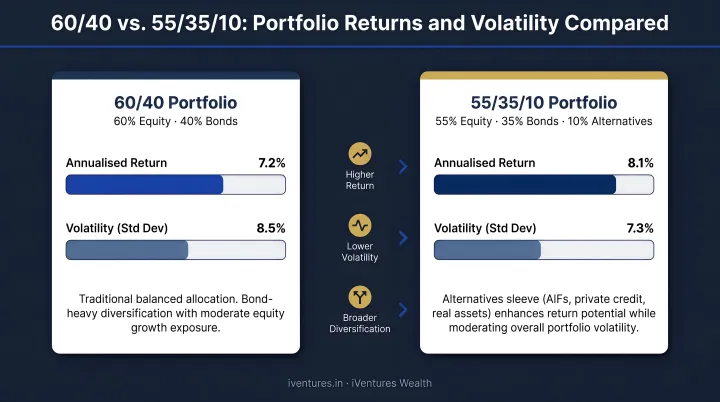

- J.P. Morgan data shows a 55/35/10 portfolio (equities/bonds/alternatives) outperformed a 60/40 with lower volatility from 1998 to 2025

- SEBI-regulated AIFs require a minimum ₹1 crore investment, while REITs and InvITs offer much lower entry thresholds

- Allocation sizing should reflect your liquidity needs, spending rate, and time horizon alongside risk appetite

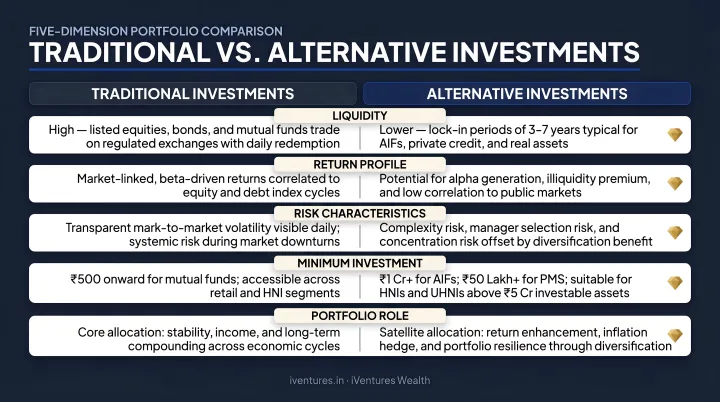

What Is Alternative Asset Allocation and How Does It Differ from Traditional Investing?

Alternative asset allocation is the deliberate inclusion of assets outside traditional stocks, bonds, and cash into an investment portfolio. This spectrum includes private equity, real estate, private credit, commodities like gold and silver, and hedge fund strategies.

The distinction from traditional investing runs deeper than asset class labels. The structural differences are what matter most:

| Dimension | Traditional Investments | Alternative Investments |

|---|---|---|

| Liquidity | Daily liquidity | Largely illiquid (3–10 year lock-ups) |

| Market access | Public markets | Private markets |

| Regulation | Heavily regulated | Less regulated, more complex |

| Correlation to equities | High | Low to negative |

| Minimum investment | No formal minimum | ₹1 crore for SEBI AIFs |

Who Can Access Alternatives in India?

Historically, alternatives were the domain of institutional investors and the wealthiest families. That's changed as SEBI's regulatory framework has expanded access considerably. SEBI's AIF framework, listed REITs, and InvITs have created regulated pathways for affluent Indian investors to access private markets.

- AIFs: SEBI-regulated privately pooled vehicles requiring ₹1 crore minimum per investor — suited for HNIs and UHNIs

- REITs and InvITs: Listed instruments accessible with as little as one unit; REITs and InvITs mobilised ₹1.3 trillion from FY2020 to March 2024, reflecting growing mainstream adoption

- Structured products: Another channel for accessing alternative risk/return profiles within a regulated framework

Alternative allocation doesn't replace stocks and bonds. It adds a purposefully sized position alongside the core portfolio, serving a defined role: return enhancement, income generation, or diversification.

Key Alternative Asset Classes Available to Indian Investors

Private Equity and Venture Capital

Private equity (PE) and venture capital (VC) involve investing in unlisted companies through SEBI-regulated AIF Category I and II structures. Category I covers early-stage ventures, startups, SMEs, and infrastructure. Category II covers PE funds, real estate funds, debt funds, and distressed assets — which SEBI data shows account for commitments of ₹11,64,118 crore out of total AIF commitments of ₹15,74,050 crore as of December 2025.

These investments typically have 5–10 year horizons and are well-suited for founders, CXOs, and UHNIs comfortable with lock-in periods in exchange for the illiquidity premium.

Real Assets: REITs and InvITs

Direct real estate, REITs, and InvITs provide stable income, inflation linkage, and portfolio diversification without requiring active property management.

India currently has 5 REITs and 24 InvITs registered. Embassy REIT distributed ₹2,181 crore (₹23.01/unit) in FY2025, and IndiGrid's DPU grew to ₹16.00/year — demonstrating consistent income generation from listed real assets. SEBI's move to 1-unit market lots has made REITs and InvITs accessible to a much wider investor base.

Private Credit, Gold, and Hedge Strategies

Beyond PE and real assets, three more categories merit attention:

- Private credit: Senior secured loans to mid-market companies through AIF structures, with 2–3x collateral coverage. Indian companies raised $6 billion (~₹50,000 crore) from private credit in H1 2024, up 22.4% year-on-year

- Gold and silver: Gold has delivered a CAGR of 8.1% since 1971 against roughly 3.9% CPI inflation, and the World Gold Council's analysis confirms gold shows predominantly negative correlation with Indian equities — making it a genuine diversifier. iVentures Wealth positions gold and silver as portfolio insurance, not trading vehicles

- Hedge/long-short strategies: Category III AIFs include long-only, long-short, multi-strategy, and quantitative approaches — useful for generating returns in volatile or sideways markets

iVentures Wealth advises on private credit AIFs targeting gross returns in the 13–16% range, with quarterly distributions — structured as a yield substitute for fixed deposits.

The Case for Alternatives: Diversification, Returns, and Income

The Diversification Argument

The quantitative case is straightforward. J.P. Morgan's Guide to Alternatives shows that from Q1 1998 to Q4 2025:

- A 60/40 portfolio returned 7.6% with 9.8% volatility

- A 55/35/10 portfolio (with 10% alternatives) returned 7.9% with 9.4% volatility

Higher returns with lower volatility — the numbers make the argument without embellishment.

Global family offices have already moved in this direction. A 2024 UBS survey of 320 family offices found 42% strategic allocation to alternatives — including 22% private equity, 10% real estate, 5% hedge funds, and 2% private debt.

The Return Enhancement Case

Private equity has delivered higher returns than listed equities, compensating for illiquidity. J.P. Morgan data shows global private equity returned 14% annually from 2005 to 2025 versus 11% for global public equity — net of fees, in USD. Indian investors should note that rupee depreciation against the dollar can compress or inflate these returns in INR terms depending on the period.

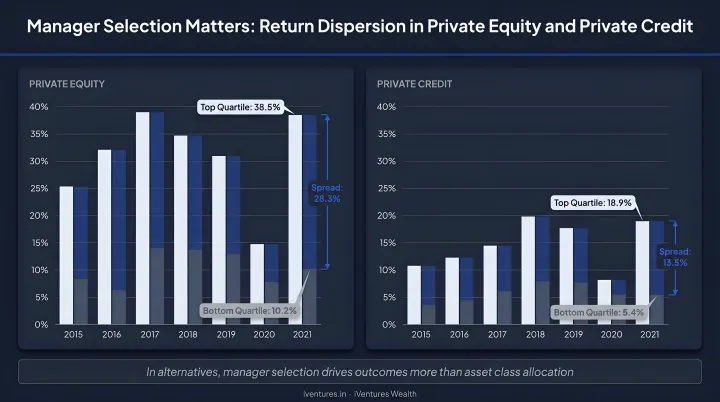

One caveat: manager selection in private markets matters more than in any other asset class. The spread between top-quartile PE managers (20.5% returns) and bottom-quartile (11.4%) over 2016–2026 is nearly 10 percentage points.

That gap is far wider than typical manager dispersion in public equity. Choosing the right fund manager is as important as choosing the right asset class.

Inflation Protection and Income Generation

Real assets and gold have historically held value during inflationary periods in ways that bonds and cash cannot.

For income generation, REITs, InvITs, and private credit AIFs provide regular distributions that can supplement or replace traditional fixed income — particularly useful for family offices, retirees, or any investor with structured cash flow needs.

A Role-Based Framework

Not all alternatives serve the same purpose. Before allocating, map each asset class to a specific objective:

| Alternative Asset | Primary Role in Portfolio |

|---|---|

| Private equity / VC | Long-term growth and net worth compounding |

| REITs / InvITs | Regular income and inflation-linked real asset exposure |

| Private credit AIFs | Yield enhancement; fixed deposit substitute |

| Gold / silver | Portfolio insurance; inflation hedge; equity diversifier |

| Hedge / long-short strategies | Downside mitigation; absolute return in volatile markets |

How to Size and Structure Your Alternative Asset Allocation

Liquidity Is the Starting Point

Sizing an alternatives allocation is not a function of risk appetite alone — it's primarily a function of liquidity needs. An investor drawing 3% annually from their portfolio can sustain a meaningfully larger alternatives sleeve than one drawing 7%, because illiquid investments require sufficient liquid reserves to meet spending without forced redemptions.

Before committing to any illiquid position, answer these questions:

- What is my annual spending requirement from this portfolio?

- What liquid reserves do I need for the next 3–5 years?

- Could any business, personal, or family event require unexpected capital access?

Two Risks to Manage Actively

Too high an allocation to illiquid alternatives creates liquidity shortfall risk — the inability to meet cash needs or capitalise on market dislocations when they arise. Stress-test your portfolio against spending needs and potential capital calls before committing.

Allocation drift is the second concern. Illiquid assets cannot be sold to rebalance, so if private equity appreciates sharply, its effective portfolio weight increases without any ability to trim. Address this before it occurs: use liquid assets to rebalance, and document the plan in advance.

Practical Allocation Ranges

Industry guidance for UHNI investors typically looks like this:

| Investor Profile | Suggested Alternatives Range |

|---|---|

| Moderate-risk HNI/UHNI | 10–20% |

| Aggressive UHNI / Family office | 25–30% |

| Institutional (endowments, pensions) | 23–37% |

In India, the ₹1 crore minimum per AIF investment also shapes practical sizing — a ₹10 crore portfolio can only build a diversified alternatives sleeve of 2–3 positions before liquidity buffers are exhausted.

Personalised Allocation with iVentures Wealth

Arriving at the right alternatives allocation requires more than a generic range — it requires a detailed analysis of your liquidity profile, spending rate, tax situation, time horizon, and existing portfolio structure.

iVentures Wealth, a SEBI-registered investment adviser (INA000019026) with over 20 years of experience and ₹1,200+ crore in assets under management, works with UHNIs, family offices, CXOs, founders, and NRIs to construct personalised alternative allocation strategies. The firm operates on a fee-only model with no AIF placement commissions. Its advisory process covers fund-house due diligence, vintage comparison, GP track-record review, and ongoing performance monitoring across the life of each position.

Risks and Considerations Before Investing in Alternatives

Illiquidity and Lock-Up Risk

SEBI requires Category I and II AIFs to be close-ended with a minimum tenure of 3 years — and in practice, PE and private credit funds typically run 5–10 years. Capital committed to alternatives should be capital the investor is certain won't be needed during that window. Funding alternatives from money earmarked for near-term needs is the single most common structuring mistake.

Cost, Complexity, and Manager Selection

Alternatives carry higher management fees, performance fees (carry), and require substantially more due diligence than public market investments. The performance gap between top and bottom-quartile managers in private markets is also wider than most investors expect:

| Asset Class | Top-Quartile Returns | Bottom-Quartile Returns | Dispersion |

|---|---|---|---|

| Private Equity | ~12.2% | ~5.3% | ~7 percentage points |

| Private Credit | ~10%+ | ~3–4% | ~7 percentage points |

Manager selection is the single most consequential decision in any alternatives allocation — it often determines whether the portfolio outperforms or underperforms public market equivalents.

Indian Regulatory and Tax Considerations

The SEBI AIF framework distinguishes three categories with different regulatory requirements and tax treatment:

- Category I and II AIFs: Pass-through treatment under Section 115UB — most income (other than business income) is taxed at the investor level, preserving the character of returns

- Category III AIFs: Tax treatment is more complex; blanket pass-through does not apply — specific legal and tax advice is required before investing

- REITs and InvITs: Section 115UA governs distributions, which retain their nature in unitholder hands (interest, dividend, rental income, or capital repayment each taxed differently); TDS at 10% applies to specified income for resident unitholders under Section 194LBA

Given the complexity of AIF, REIT, and InvIT tax treatment, structuring any alternative allocation without guidance from a SEBI-registered adviser and a qualified tax professional carries real risk — both regulatory and financial.

Frequently Asked Questions

What is alternative asset allocation?

Alternative asset allocation is the practice of including non-traditional assets — private equity, real estate, private credit, commodities, and hedge fund strategies — alongside stocks and bonds in a portfolio. The goal is to improve diversification, reduce volatility, or enhance returns by accessing return drivers that aren't correlated to public markets.

What are examples of alternative assets?

Key examples include private equity, venture capital, direct real estate, REITs and InvITs, private credit, gold, and hedge fund strategies. In India, SEBI-regulated AIFs are the main vehicle for private market alternatives, with a minimum investment of ₹1 crore per investor.

Is 70/30 better than 60/40?

Neither ratio is universally superior — the right equity-bond split depends on individual risk tolerance and time horizon. The more relevant shift is that both 60/40 and 70/30 are increasingly being supplemented with a third allocation sleeve of alternatives to reduce dependence on the stock-bond correlation holding.

How much of my portfolio should be in alternative assets?

A common starting range is 10–20% for HNI and UHNI investors, rising to 25–30% for more aggressive allocators and family offices. The right figure depends on your liquidity needs, annual spending rate, risk appetite, and time horizon — and should be determined with a qualified investment adviser.

Are alternative investments suitable for all investors?

Alternatives are generally suited to sophisticated, high-net-worth investors with a long time horizon and the ability to tolerate illiquidity. In India, SEBI's ₹1 crore minimum for AIFs sets a clear entry bar — see the question below for a full breakdown of thresholds.

What is the minimum investment for alternative assets in India?

SEBI-regulated AIFs require a minimum investment of ₹1 crore per investor (₹25 lakh for employees or directors of the AIF or its manager). Listed REITs and InvITs have substantially lower entry points — SEBI's 1-unit market lot rule means investors can start with a single unit on the NSE or BSE, making them far more accessible than AIFs.