Introduction

A ₹20 crore portfolio is a milestone — but it doesn't automatically mean you're ready for retirement. Many HNIs discover this only when they try to convert decades of wealth accumulation into sustainable lifetime income, and realize the rules change completely.

The challenge isn't corpus size — it's complexity. Multi-asset portfolios spanning listed equities, real estate, unlisted businesses, and alternatives don't behave like a simple fixed deposit ladder.

Layer on India's evolving tax rules, healthcare inflation running near 9.9% annually according to Mercer Marsh Benefits, and a retirement horizon that could stretch 30+ years — and standard retirement advice breaks down fast.

This guide covers India-specific do's and don'ts for HNIs, founders, CXOs, and affluent families navigating retirement planning. From withdrawal sequencing and tax structuring to estate documents and family governance, the decisions you make now will determine whether your wealth sustains the lifestyle you've built — or quietly erodes it.

Key Takeaways

- Start with a full balance sheet — assets, liabilities, liquidity profiles, and income timelines — not a savings target

- Use NPS, PPF, and ELSS as tax-efficient building blocks within a larger diversified strategy

- Post-July 2024, equity LTCG is taxed at 12.5% above ₹1.25 lakh; build this cost into every withdrawal plan from the start

- Maintain a liquidity ladder covering 12–24 months of expenses to avoid forced asset sales

- Estate documents and family wealth conversations should be in place well before retirement

Retirement Planning Do's for High-Net-Worth Individuals

Do #1: Build a Holistic Balance Sheet Before Setting Goals

Most HNI portfolios aren't just investment accounts — they're a collection of listed equities, real estate, business stakes, unlisted shares, and possibly foreign assets. Each carries a different liquidity profile, tax implication, and income potential.

Starting retirement planning without mapping all of these is like planning a road trip without knowing your fuel level or how far each stop is.

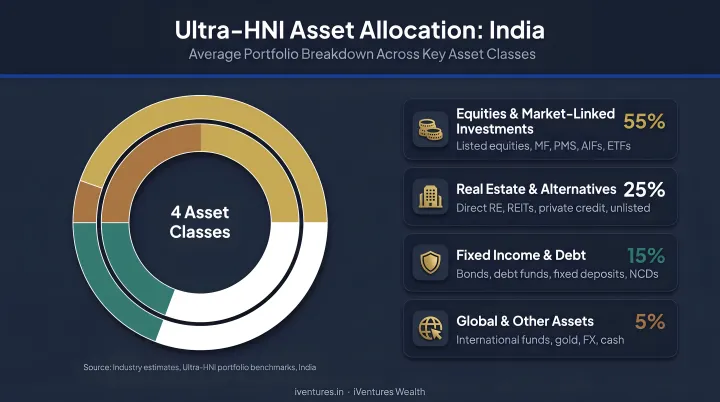

According to Kotak Private's Top of the Pyramid report, the average Ultra-HNI allocation in India sits at 32% equity, 29% real estate, 21% debt, and 18% alternatives. Nearly half of that wealth is in illiquid or semi-liquid assets. For retirement planning, this matters enormously.

What a proper balance sheet includes:

- Current market value of all assets (with realistic liquidity timelines)

- Outstanding liabilities and pledge positions

- Expected income timelines from each asset

- Tax basis and embedded gains

What planners call sequence-of-return risk is the core danger here: a forced asset sale early in retirement can permanently damage your corpus even if markets recover. A founder liquidating real estate at distressed prices in year two doesn't get that loss back. The CFA Institute points to dynamic withdrawals, liquidity laddering, and bucket planning as the primary tools to manage this.

iVentures Wealth addresses this through "Post-Career Financial Architecture" — mapping each rupee to a specific goal, timeline, and liquidity requirement before any drawdown begins.

Do #2: Maximize Tax-Advantaged Retirement Instruments

Indian HNIs often dismiss NPS because the contribution limits seem trivial relative to their wealth. That's a mistake : the tax efficiency is the point, not the absolute amount.

NPS (National Pension System):

- Deduction up to 10% of salary under Section 80CCD(1), within the ₹1.5 lakh Section 80CCE ceiling

- Additional ₹50,000 deduction under Section 80CCD(1B)

- At maturity (age 60): up to 60% lump sum is tax-exempt; 40% must go toward annuity purchase

- Treat NPS as partly liquid (the 60% lump sum) and partly annuitized income — not fully flexible

Complementary instruments worth including:

| Instrument | Current Rate | Lock-in | Key Use |

|---|---|---|---|

| PPF | 7.1% (Q1 FY2026-27) | 15 years | Long-term tax-free compounding |

| SCSS | 8.2% (Q1 FY2026-27) | 5 years | Post-retirement income (up to ₹30 lakh) |

| ELSS | Market-linked | 3 years | Growth + Section 80C deduction |

None of these alone will build corpus at HNI scale. Together, though, they form tax-efficient anchors within a larger strategy: reducing taxable income during accumulation and providing predictable income or growth during retirement.

Do #3: Structure a Sequenced Withdrawal Strategy

Once the accumulation phase is mapped, the next question is sequencing: how and when to draw down. The general principle is to draw first from taxable accounts (to reset cost basis or use lower LTCG rates), then from investment accounts, preserving tax-free growth vehicles like PPF for as long as possible.

This sequencing only works with a retirement income timeline — a year-by-year projection of:

- Annual living expenses, adjusted for inflation

- Planned drawdowns from each asset type

- Large irregular expenses (children's weddings, property purchases, philanthropic gifts)

- Tax liability from each withdrawal source

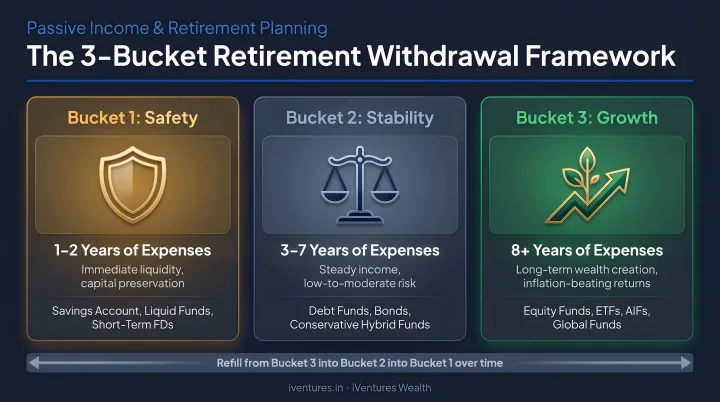

Without this, liquidity crunches happen at the worst times. iVentures has worked with founders post-business-exit using a three-bucket framework: Safety (5–7 years of expenses in high-quality fixed income), Stability (balanced allocation for the 8–15 year horizon), and Growth (AIFs, PMS, private equity). Each bucket serves a distinct purpose in the drawdown sequence.

Do #4: Diversify Into Income-Generating Alternatives for Retirement Cash Flow

Fixed deposits and dividend stocks alone won't sustain a 30-year retirement for an HNI. India's growing alternatives market now offers instruments that previous generations didn't have access to.

Build retirement income through:

- REITs and InvITs — the Nifty REITs & InvITs Index currently has 11 constituents with a 1.96% dividend yield as of May 2026; distributions provide regular quarterly payouts

- Sovereign Gold Bonds — inflation hedging with semi-annual interest

- Private credit / AIFs — SEBI AIF cumulative commitments reached ₹15,74,050 crore as of December 2025; high-quality private credit opportunities offer yield beyond traditional debt

One business owner iVentures works with generates approximately ₹7.5 lakh per month in predictable passive income from a structured portfolio across quality debt, select REITs/InvITs, and income-focused funds. The corpus continues to grow despite regular withdrawals.

Critical rule: Maintain 12–24 months of planned retirement expenses in liquid or near-liquid instruments (liquid funds, FDs, money market funds). This is your buffer against selling growth assets during downturns.

Do #5: Plan for Inflation-Adjusted Lifestyle and Healthcare Costs Over 30+ Years

Many HNIs calculate their retirement corpus in today's rupees. That's a planning error that compounds painfully over time.

World Bank data shows India's life expectancy at age 60 is 19.7 years — and that's the national average. An affluent individual with access to quality healthcare could realistically plan for 25–30 years in retirement.

Healthcare inflation is the steeper concern. Mercer Marsh Benefits forecasts India's employer healthcare cost trend at 9.9% for 2026 — more than double general CPI. A medical expense that costs ₹5 lakh today costs roughly ₹33 lakh in 25 years at that rate.

A practical approach:

- Calculate current annual lifestyle expense

- Apply a blended inflation assumption of 7–8% for general costs and 10% for healthcare

- Project this 25–30 years forward

- Build that inflation-adjusted figure into your corpus target — not today's rupee equivalent

The difference between planning for ₹30 lakh per year today versus ₹1.5 crore per year in 25 years is not a rounding error. It's the difference between financial independence and financial strain in your 80s.

Retirement Planning Don'ts for High-Net-Worth Individuals

Don't #1: Don't Ignore the Full Tax Burden on Retirement Income

HNI retirement income in India is rarely taxed at one clean rate. Here's the current reality post-Budget 2024:

| Income Type | Tax Treatment |

|---|---|

| Equity / equity MF LTCG | 12.5% above ₹1.25 lakh exemption (post July 23, 2024) |

| Equity / equity MF STCG | 20% under Section 111A (post July 23, 2024) |

| Real estate LTCG | 12.5% without indexation; resident individuals/HUFs may opt for 20% with indexation for property acquired before July 23, 2024 |

| Debt mutual funds (acquired post April 1, 2023) | Taxed as short-term capital gains at slab rate under Section 50AA |

| Dividend income | Taxable at slab rate in the investor's hands |

Surcharges compound this further. Under the new regime: 10% surcharge for income ₹50 lakh–1 crore, 15% for ₹1–2 crore, and 25% above ₹2 crore. The old regime adds a 37% surcharge above ₹5 crore (though surcharge on LTCG under Sections 112A and 111A is capped at 15%).

The common mistake: Waiting until retirement to think about tax. Strategic decisions made years before — timing equity sales to stay within LTCG exemption limits, structuring business exits for lower tax, or gifting appreciated assets within exempt thresholds — can materially reduce lifetime tax liability. For HNIs, tax planning is year-round work, not a March deadline.

Don't #2: Don't Maintain the Wrong Asset Allocation into Retirement

Two opposing errors are equally damaging:

Concentration risk — Staying heavily positioned in the asset that built your wealth (a single stock, your business, or specific real estate) through retirement. Kotak data shows Ultra-HNIs average 32% in equity and 29% in real estate. If that equity is a single promoter holding, the retirement risk is enormous.

Over-conservatism — Moving everything into FDs creates inflation erosion over a 30-year retirement. At 6% FD rates and 7% lifestyle inflation, you're losing ground every year.

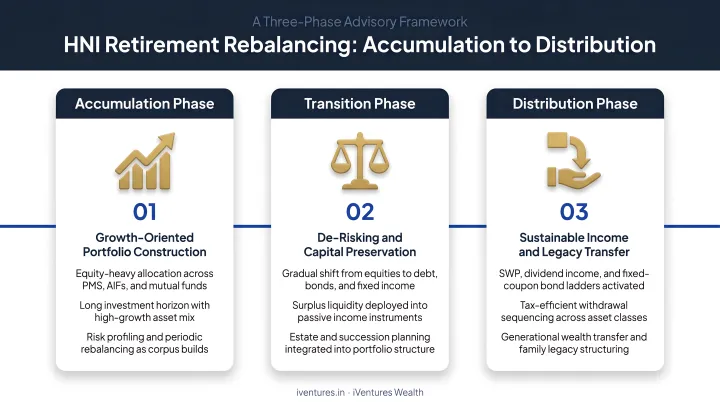

The solution is a staged rebalancing process tied to retirement phase:

- Accumulation phase — Growth-oriented, higher equity allocation acceptable

- Transition phase (5 years before retirement) — Begin reducing concentration, building liquidity buffers, locking in income streams

- Distribution phase — Shift toward income-generating assets while preserving sufficient equity for long-term inflation protection

Don't #3: Don't Let Estate Documents Sit Unreviewed for Years

India abolished estate duty in 1985, so there's no inheritance tax concern. But succession planning remains critical — and more complicated than most HNIs realize.

In Shakti Yezdani v. Jayanand Jayant Salgaonkar (December 2023), the Supreme Court confirmed that a nominee does not acquire absolute ownership to the exclusion of legal heirs. Succession law and valid wills determine beneficial ownership. An outdated nomination — common on demat accounts opened 15 years ago — can trigger significant family conflict.

HUF structures carry a separate risk. The 2005 Hindu Succession Act amendment made daughters coparceners, expanding the coparcener base and raising litigation exposure in poorly documented HUFs.

Review estate documents whenever:

- A major life event occurs (marriage, children, business sale, large asset acquisition)

- More than 3–5 years have passed since the last review

- A family member's financial circumstances change materially

iVentures coordinates with external estate planning specialists, including senior legal counsel, to draft wills and structure trusts — ensuring documents are legally sound and properly maintained over time.

Don't #4: Don't Underestimate Liquidity Risk in an Illiquid Portfolio

With 29% of Ultra-HNI wealth in real estate and 18% in alternatives, Indian HNIs carry significant liquidity risk into retirement. Neither category can be monetized quickly without taking a valuation hit.

A liquidity ladder solves this:

- Tier 1 (0–12 months): Liquid funds, savings accounts, short-term FDs — immediate expense coverage

- Tier 2 (1–3 years): Short-duration bonds, debt mutual funds, REITs/InvITs — accessible within weeks

- Tier 3 (3–7 years): Balanced equity-debt portfolios, listed equity — sell in favorable conditions

- Tier 4 (7+ years): Real estate, AIFs, unlisted equity — long-term growth, not spending assets

The goal is never needing to force-sell a growth or illiquid asset to cover a medical emergency or ordinary retirement expense.

Don't #5: Don't Avoid Family Conversations About Wealth and Succession

PwC India reports that only 63% of Indian family business leaders have formal governance structures — shareholder agreements, family constitutions, or wills. That means more than one in three wealthy Indian families have no documented succession framework.

When estate plans, trust structures, and inheritance expectations go undiscussed, the result is post-retirement regret and post-death conflict — compounded in India by joint family dynamics and overlapping business succession.

Structured family financial conversations — especially with adult children — should cover:

- Inheritance expectations and timelines

- The purpose and rules of any trust structures

- Philanthropic intentions and how they affect the estate

- Who manages what if incapacity precedes death

iVentures has worked with families managing wealth across nine separate relationships with different brokers and banks — no single view, no succession plan. Consolidating into a unified family balance sheet and formalizing a family charter reduced conflict and created clear succession visibility.

Tax-Smart and Wealth Transfer Strategies for Indian HNIs

Tax-Efficient Planning Before and During Retirement

Tax planning works best when it starts years before retirement, not at the filing deadline.

Key strategies:

- LTCG harvesting — Realise equity gains up to the ₹1.25 lakh annual exemption each year to reset cost basis and reduce future tax liability

- Tax loss harvesting — Offset gains by realising losses in underperforming positions before year-end

- Gift timing — Under Section 56(2)(x), gifts above ₹50,000 aggregate in a year are taxable; gifts to specified relatives, or on occasion of marriage, are exempt. Structured gifting to family members within exempt categories reduces the taxable estate over time

- Business exit structuring — Timing a promoter stake sale to optimise between short-term and long-term capital gains treatment can save crores in tax

Where you hold income-generating assets matters just as much as which assets you hold. The right legal structure can meaningfully reduce the tax burden across generations:

- HUF structures — Split income across coparceners, lowering the per-person tax liability

- Revocable trusts — Income is taxed to the settlor under Section 61; useful for flexibility during the settlor's lifetime

- Determinate trusts — Enable beneficiary-level tax treatment, which can be significantly more efficient for large portfolios

Each structure carries its own compliance requirements. A qualified tax advisor should be involved before implementation.

Wealth Transfer and Legacy Planning Tools

India has no estate duty — so the planning challenge isn't a tax bill at death, it's ensuring assets transfer cleanly, without disputes, and with minimal income tax drag along the way.

Primary instruments:

- Private family trusts — Revocable for flexibility during the settlor's lifetime; irrevocable for ring-fencing assets for specific beneficiaries

- HUF structures — Effective for income splitting, though daughters' coparcenary rights post-2005 require careful documentation

- GIFT City structures — IFSCA Fund Management Regulations 2025 govern fund management entities in IFSC, relevant for NRI clients managing international assets

Philanthropy, structured correctly, serves both legacy and tax goals. Charitable trusts registered under Section 12A qualify for income exemption under Section 11. Donating appreciated assets directly to a registered trust avoids the capital gains tax you'd otherwise pay by selling first — making the in-kind donation meaningfully more efficient than writing a cheque from sale proceeds.

The Role of a Trusted Fiduciary Adviser in HNW Retirement Planning

HNW retirement planning spans investment strategy, tax optimisation, estate structuring, insurance decisions, and family governance. No single product provider can cover all of these without conflicts of interest.

The ideal advisory structure for an HNI looks something like:

- SEBI-registered Investment Adviser — fiduciary, fee-only guidance on portfolio construction and withdrawal strategy

- Chartered Accountant — tax planning, gain harvesting strategy, and compliance

- Estate planning lawyer — will drafting, trust structuring, and succession documentation

iVentures Wealth (SEBI RIA INA000019026, registered 2010) operates as the coordinating fiduciary in this model, working alongside external CAs and estate planning specialists — including senior legal counsel with Supreme Court-level experience — to deliver integrated planning end to end.

The firm has served 150+ affluent families over 20+ years, managing ₹1,146+ crore in assets with a team of 20+ qualified professionals led by CFA charterholders and ex-institutional investors.

That coordinating role only works if the adviser is truly independent — which is where the distributor vs. RIA distinction becomes critical. A product distributor earns commissions from fund houses and manufacturers. A SEBI-registered RIA is legally required to act in the client's interest, cannot accept trail income or kickbacks, and charges a transparent advisory fee directly. For an HNI with a multi-crore retirement portfolio, even a modest misalignment of incentives — a slightly higher-commission product here, unnecessary churn there — compounds into significant wealth erosion over a 25-year retirement.

iVentures' Wealth Monitor App (iOS and Android, launched 2020) gives clients a single consolidated dashboard across mutual funds, equities, bonds, FDs, PMS, AIFs, and insurance — covering multiple family members and entities. For HNIs monitoring a retirement drawdown across ten or more accounts, that real-time visibility is a core planning tool, not an add-on.

Frequently Asked Questions

What is the 50-30-20 rule for high earners?

The 50-30-20 rule splits after-tax income into 50% needs, 30% wants, and 20% savings. For HNIs, this framework is largely irrelevant — financial complexity demands personalised planning, not fixed ratios. High earners typically need to save and invest far more than 20% to generate the retirement corpus their lifestyle requires.

What is considered high-net-worth for retirement planning in India?

In India, wealth managers generally consider ₹5 crore or more in investable assets (excluding primary residence) as the threshold requiring specialised retirement planning. Globally, Capgemini pegs the HNWI benchmark at USD 1 million+ in investable assets — both are market conventions, not statutory definitions.

How much retirement corpus is enough for an HNI in India?

A common starting estimate uses 25–30x the first year's planned annual retirement expense. HNIs must also factor in healthcare inflation (near 10% annually), a 30+ year horizon, legacy goals, and philanthropic commitments. A personalised cash flow projection built around your actual income needs will always outperform any rule of thumb.

At what age should HNIs start dedicated retirement planning?

Ideally by the mid-30s for wealth accumulation and asset structuring. For HNIs in their 40s–50s, the priority shifts to the "transition phase" — rebalancing concentrated positions, optimising tax structures, and building reliable income streams before earned income stops.

Should HNIs invest in NPS for retirement?

NPS offers a useful ₹50,000 additional deduction under Section 80CCD(1B) and partial tax-free maturity. However, the mandatory 40% annuity requirement and contribution limits mean it typically functions as one piece of a much larger, diversified retirement strategy, not its foundation.

What are the biggest tax mistakes HNIs make in retirement?

The three most costly: not planning for 12.5% LTCG on equity and real estate, being caught off guard by surcharges that push effective tax rates significantly higher on large income years, and failing to time asset liquidations strategically before retirement. All three are preventable with proactive structuring.