Most investors know what to do — start a SIP, stay invested, diversify. The gap lies in how to do it: which funds to choose, how much to contribute, when to rebalance, and crucially, what not to do when markets fall 30%.

This guide walks through the exact steps, parameters, and common mistakes that determine whether a mutual fund portfolio creates real wealth or merely tracks an index.

Key Takeaways

- Wealth creation through mutual funds depends on consistent SIP contributions, long time horizons, and emotional discipline, not market timing

- SIP top-ups (stepping up contributions annually) compound into significantly larger corpora than flat SIPs over 20+ years

- Fund selection should be based on 5–10 year risk-adjusted returns and benchmark consistency — not last year's rankings

- Direct plans save 0.5%–1.5% annually in expense ratio versus regular plans, saving lakhs in corpus over a 20-year horizon

- LTCG on equity funds beyond ₹1.25 lakh is taxed at 12.5%, while ELSS funds offer Section 80C deductions up to ₹1.5 lakh — use both deliberately

How to Build Wealth Through Mutual Funds: A Step-by-Step Approach

Step 1: Define Your Financial Goals and Risk Profile

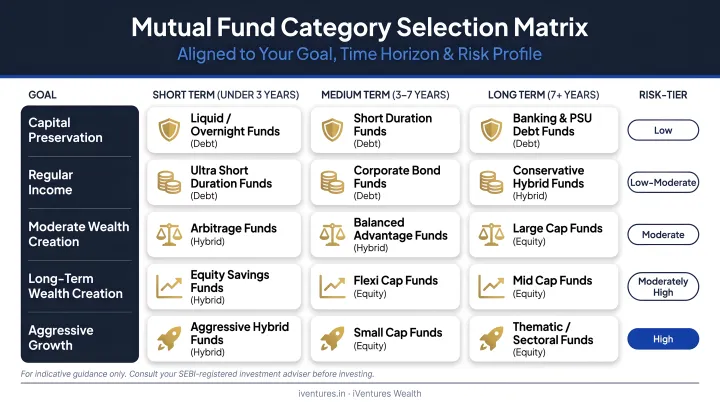

Investing without a target is guesswork. Each goal — retirement corpus, child's education, property purchase — needs three things mapped to it: a target amount, a timeline, and an appropriate fund category.

Goal-to-horizon mapping:

| Goal | Typical Horizon | Suitable Fund Type |

|---|---|---|

| Retirement | 15–30 years | Equity (flexi-cap, mid-cap) |

| Child's education | 10–15 years | Equity + hybrid |

| Property down payment | 3–7 years | Hybrid or debt funds |

| Emergency corpus | Immediate | Liquid funds |

Risk profiling sits alongside goal setting. Key factors include age, income stability, existing EMIs, and how you'd actually behave if your portfolio dropped 25%. These determine the equity-debt split — not a formula, but a calibrated range tied to your specific situation.

Goal-based investing also protects you from reactive decisions during corrections. When every SIP is tied to a named purpose with a defined timeline, a 20% market fall becomes easier to sit through.

Step 2: Choose the Right Type of Mutual Fund for Your Goals

The Indian mutual fund universe covers dozens of categories. For wealth creation specifically, the relevant ones are:

- Large-cap funds — stability, lower volatility, suitable as a core holding

- Mid-cap and flexi-cap/multi-cap funds — higher growth potential, suit 10+ year horizons

- ELSS (tax-saving) funds — 3-year lock-in, Section 80C benefit, equity exposure

- Hybrid funds — equity + debt mix, useful for medium-term goals or moderate-risk investors

- Debt/liquid funds — capital preservation, short-term parking

The active vs. passive debate matters here. SPIVA India Year-End 2025 data shows that 84.4% of active large-cap funds underperformed their benchmark over 5 years, and 76.3% underperformed over 10 years. For large-cap exposure, low-cost index funds increasingly make sense.

That said, mid-cap and flexi-cap categories show more variation — skilled active managers can add value in less efficient segments of the market.

What investors consistently get wrong: selecting funds based on 1-year return rankings. A fund that topped the charts last year often reverts to average. Selection should rest on 5–10 year consistency, risk-adjusted returns (Sharpe and Sortino ratios), and fund manager track record across multiple market cycles.

Step 3: Start a SIP with a Structured Contribution Plan

A SIP invests a fixed amount monthly regardless of market levels. The mechanism — rupee cost averaging — means you automatically buy more units when markets fall and fewer when they rise.

AMFI's explanation illustrates this clearly: a ₹1,000 SIP buys 50 units at NAV ₹20 and 100 units at NAV ₹10, giving 150 units for ₹2,000 at an average cost of ₹13.33. You benefit from volatility rather than being hurt by it.

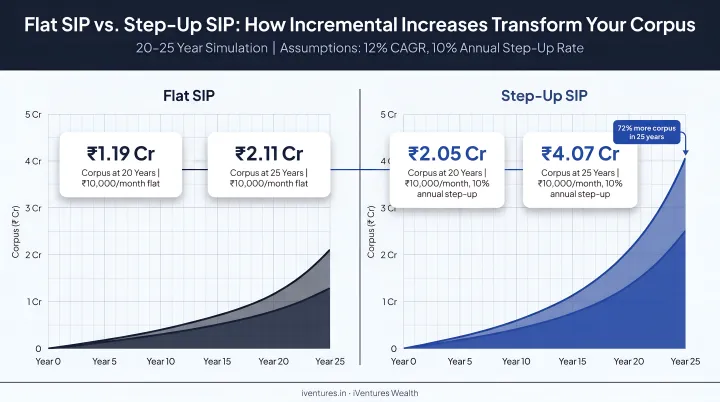

The difference between a flat SIP and a step-up SIP compounds dramatically over time. A ₹10,000/month SIP over 20 years at 12% annual return can accumulate close to ₹1 crore. A step-up SIP starting at the same ₹10,000 but increased 10% annually over 25 years — with the same assumed return — can potentially grow to ₹7–8 crore, according to illustrative examples from Mint. The total invested is higher, but the compounding on larger contributions in later years does most of the work.

When lump sum makes sense instead of (or alongside) SIP:

- Windfall income — annual bonus, sale proceeds, inheritance

- Significant market corrections when equity valuations are attractive

- Fully mature debt instruments being redeployed into equity

For salaried investors with regular monthly income, SIP remains the default. Lump sum works best when combined with a systematic transfer plan (STP) to average entry over 6–12 months.

Step 4: Diversify Strategically — Without Overdoing It

Once your contribution strategy is set, the next question is how to structure the portfolio itself. Diversification doesn't mean owning 15 schemes — it means holding complementary funds across categories with minimal overlap. Owning five large-cap funds does not reduce risk; it creates index-like returns with more paperwork and higher collective costs.

"Diworsification" looks like this:

- Multiple flexi-cap funds with nearly identical top-10 holdings

- Mid-cap and small-cap funds that overlap significantly

- More than 8–10 funds total, many held for vague reasons

A wealth-building portfolio for a 35-year-old investor might look like:

- Core equity allocation: flexi-cap + one mid-cap fund

- Tactical allocation: ELSS (for Section 80C efficiency)

- Stability buffer: one hybrid or balanced advantage fund

- Short-term reserves: liquid or ultra-short debt fund

iVentures Wealth's approach is instructive here — their CFA-led team explicitly "X-rays portfolios for overlap, concentration, and hidden risks, then rebuilds them into a cleaner, goal-linked strategy."

One client case involved consolidating 12 mutual funds and ULIPs accumulated over years, where returns barely beat FDs. After restructuring into a focused set of research-backed funds, the portfolio was aligned to actual goals.

Step 5: Review, Rebalance, and Stay the Course

Monitoring and reacting are different activities — and confusing the two is expensive. Checking quarterly whether your fund tracks its benchmark is monitoring. Switching because a fund underperformed for 8 months is reacting, and it consistently destroys long-term value.

Rebalancing is warranted when:

- Asset allocation drifts materially from target (equity grows from 70% to 85% due to a bull run)

- A life event changes your risk profile — job loss, marriage, approaching retirement

- A fund consistently underperforms its benchmark across multiple market cycles, not just one bad year

The more important discipline is staying invested through corrections. The Sensex fell 38% in 10 weeks during the 2020 COVID crash — and recovered every rupee within eight months. DSP Mutual Fund's Nifty 50 TRI study shows an SIP investor who stayed invested from December 2008 through June 2009 saw their SIP return recover from 11.6% to 21.0% — a 9.4 percentage point difference purely from not exiting at the bottom.

That 9.4 percentage point gap wasn't generated by picking a better fund — it came entirely from staying put when most investors bailed.

Key Parameters That Determine Your Mutual Fund Wealth Creation Results

Two investors can follow identical steps and arrive at very different corpora. The difference comes down to four variables within their control.

Time Horizon

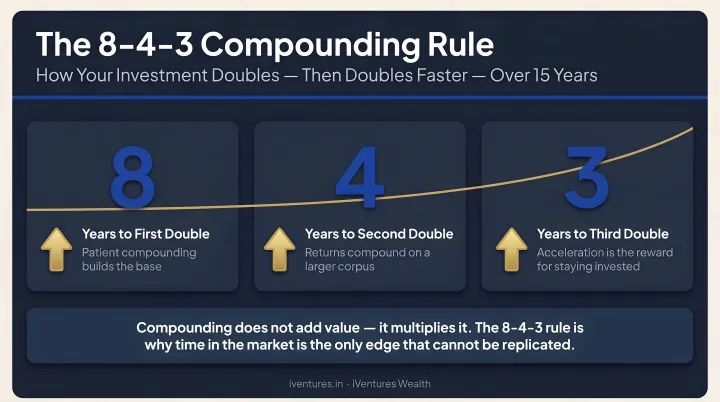

Compounding is non-linear — the gains in years 15–30 dwarf those in years 1–10.

The 8-4-3 rule captures this acceleration clearly. Assuming a consistent 12% annual return (illustrative, not guaranteed):

- Years 1–8: Investment doubles for the first time

- Years 9–12: Doubles again in just 4 more years

- Years 13–15: Doubles a third time in only 3 years

The compounding engine accelerates on its own momentum. Starting early matters more than starting large — a ₹10,000/month SIP for 25 years at 12% produces a materially larger corpus than the same SIP for 15 years, not just proportionally but exponentially, because the final decade does the heaviest lifting.

Contribution Discipline and Top-Up Rate

Skipping SIPs during market downturns or pausing contributions during lifestyle expansions are two of the most common wealth destroyers. Consistency matters more than the starting amount.

Annual SIP step-ups amplify this consistency advantage. A 10% annual increase on a ₹10,000/month starting contribution over 20 years results in a materially larger corpus than a flat ₹10,000/month — because later contributions, when higher, still compound for several years before maturity.

Fund Selection and Expense Ratio

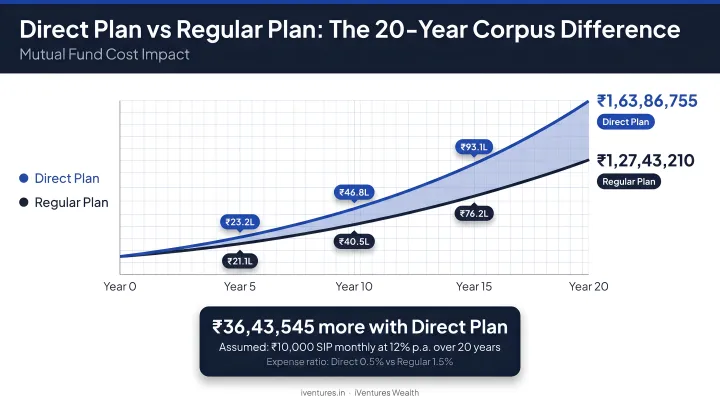

A 1% difference in expense ratio seems small. Over 20 years, it isn't.

Value Research's analysis of a ₹10,000/month SIP over 20 years at 13% gross return shows:

- Regular plan (1.9% TER): ₹84.4 lakh corpus

- Direct plan (0.5% TER): ₹1.07 crore corpus

That's a ₹22.6 lakh difference from expense ratio alone — no additional investment, no timing magic.

Direct plans, available through SEBI-registered investment advisers and direct platforms, consistently outperform regular plans by this margin. iVentures Wealth, operating as a SEBI RIA (INA000019026), recommends direct plans as standard — earning no trail commission, which eliminates the structural incentive that can lead distributors to favour regular plans over client outcomes.

Tax Efficiency

Tax treatment is a wealth multiplier that most investors ignore until they face a large redemption.

Current rates (applicable for transfers on or after July 23, 2024):

- STCG (held less than 1 year): 20% under Section 111A

- LTCG (held more than 1 year) above ₹1.25 lakh: 12.5% under Section 112A

ELSS funds serve dual purposes — they build an equity portfolio and qualify for Section 80C deduction up to ₹1.5 lakh under the old tax regime. For investors eligible to use Section 80C, ELSS is one of the most efficient instruments available.

LTCG harvesting — realising gains below the ₹1.25 lakh annual exempt threshold and reinvesting — can meaningfully reduce accumulated tax liability over time. Done consistently, it can save lakhs in tax over a 15–20 year horizon. Without active tracking, most investors breach the threshold unknowingly and lose the exemption entirely.

Common Mistakes That Derail Mutual Fund Wealth Creation

These four patterns account for the majority of underperformance in retail mutual fund portfolios:

Chasing past performance. Last year's top-ranked fund is the most dangerous choice. Funds frequently top performance charts during momentum-driven markets and then revert. SPIVA India data already shows that most active large-cap funds underperform benchmarks over 5–10 years. Fund selection should rely on risk-adjusted returns across full market cycles, not 12-month rankings.

Panic selling during corrections. Markets fall — regularly, sometimes sharply. Since 2000, the Nifty 50 has dropped 5% in a single day on 31 occasions; on 18 of those 31 days, it recovered 20% within a year.

Selling during a correction locks in losses and breaks the compounding chain. Staying invested — or increasing SIP contributions during dips — is where most long-term gains actually accumulate.

Ignoring total cost of ownership. Most investors track returns. Fewer track the combined drag of expense ratio, exit loads, and tax events. The expense ratio impact over 20 years is shown above. Add to this: approximately 508 of 1,600 active funds still charge ~1% exit load. A 1% exit load on ₹10 lakh is ₹10,000 gone immediately. Frequent switching also triggers STCG at 20%, compounding the cost further.

Over-monitoring and impulsive switching. Checking NAV daily or switching funds after 6–12 months of underperformance is one of the most documented wealth destroyers in behavioural finance. A fund underperforming its benchmark for one year is not a structural failure.

Review triggers should be fundamental — not "it's down this quarter." Ask instead:

- Has the fund's investment process changed?

- Has the fund manager been replaced?

- Has performance lagged across multiple full market cycles?

Conclusion

Wealth creation through mutual funds works. The mechanics are straightforward: clear goals, SIP discipline, appropriate fund selection, low costs, tax awareness, and the patience to stay invested through corrections. Over 15–25 years, these inputs produce meaningful compounding.

Execution is where most investors fall short, not understanding. Emotions, inertia, and information overload consistently derail portfolios that were otherwise well-constructed.

For investors with more complex requirements — retirement planning across multiple goals, tax optimisation, or integrating mutual funds with PMS, AIFs, and global investments — working with a SEBI-registered fiduciary adviser removes the conflicts inherent in distributor-led advice.

iVentures Wealth's CFA-led, research-driven advisory (SEBI RIA INA000019026) operates on this model: direct plans, goal-mapped portfolios, and transparent fees with no commission trail. Every recommendation is made in the investor's interest, not shaped by a product shelf.

Frequently Asked Questions

Frequently Asked Questions

Is mutual fund good for wealth creation?

Mutual funds are one of the most accessible wealth-building vehicles for Indian investors, combining professional management, diversification, and the discipline of SIPs. Results depend on staying invested consistently — a minimum horizon of 10 years is where compounding begins to work in your favour.

What is the 8-4-3 rule for wealth creation?

The 8-4-3 rule illustrates how compounding accelerates: at a consistent 12% annual return (illustrative), an investment doubles in roughly 8 years, doubles again in 4 more years, and doubles a third time in just 3 years. It's a reminder that the later years of an investment do the heaviest compounding work.

What is Warren Buffett's 70/30 rule?

The "70/30 rule" is a misattribution — Buffett's actual guidance (2013 Berkshire Hathaway letter) was 90% in a low-cost S&P 500 index fund and 10% in short-term government bonds. Indian investors should treat this as a directional principle, not a direct template, and calibrate their equity-debt split to their own risk profile and domestic investment universe.

Which type of mutual fund is best for long-term wealth creation?

Flexi-cap, multi-cap, and mid-cap equity funds have consistently delivered the strongest long-term returns in India. ELSS is worth considering if Section 80C tax efficiency matters to you. A SEBI-registered adviser can help match the right category to your specific horizon and risk profile.

How much should I invest monthly in mutual funds to build wealth?

Start with what you can commit to consistently, and step it up annually in line with income growth. The right SIP amount is best calculated by working backward from your target corpus, timeline, and expected return — a SEBI-registered adviser can run this calculation accurately for your specific goals.

How long does it take to create wealth through mutual funds?

Meaningful wealth creation typically requires a minimum of 10 years, with the most significant compounding benefits visible beyond 15–20 years. Equity mutual funds reward patience — the longer the horizon, the more exponential the compounding effect becomes.