The difference runs deeper than minimum ticket size. PMS and AIF diverge on ownership structure, tax treatment, liquidity, and the types of strategies each can access. Choosing the wrong one for your situation doesn't just leave returns on the table — it can create tax inefficiencies and liquidity mismatches that take years to unwind.

This guide breaks down both products clearly, covers the regulatory facts (not the marketing version), and helps you identify which structure — or which combination — fits your corpus, horizon, and goals.

Key Takeaways

- PMS builds a portfolio directly in your demat account; AIFs pool capital from multiple investors into a single fund structure

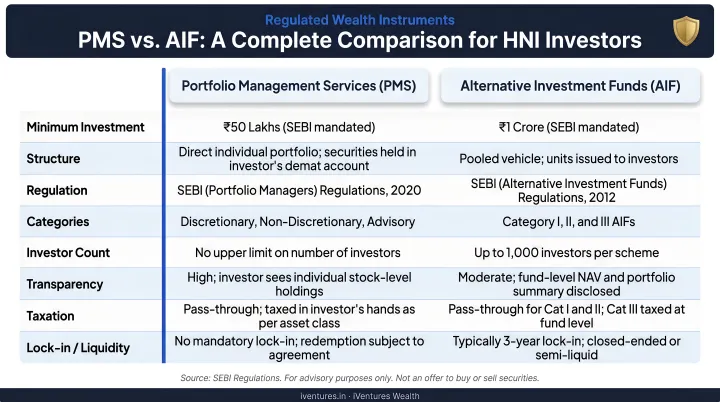

- SEBI mandates ₹50 lakh minimum for PMS and ₹1 crore for AIF

- Taxation differs sharply: PMS follows direct stock ownership rules, while AIF tax treatment varies by category

- Not all AIFs are illiquid — Category III AIFs can be open-ended, giving investors more flexibility than commonly assumed

- Many investors with ₹1 crore+ use both: PMS for a liquid equity core, AIF for alternative strategies

PMS vs AIF: Quick Comparison

| Parameter | PMS | AIF |

|---|---|---|

| Minimum investment | ₹50 lakh (SEBI-mandated) | ₹1 crore (SEBI-mandated) |

| Structure | Individual managed account | Pooled investment vehicle |

| Ownership | Direct securities in your demat | Fund units |

| Transparency | High — you see every holding | Moderate — fund-level reporting |

| Liquidity | Flexible (depends on underlying securities) | Category I/II: closed-ended; Category III: open or closed |

| Asset universe | Listed equities, debt, and related instruments | Private equity, credit, real estate, hedge-fund strategies |

| Taxation | STCG/LTCG as direct investor | Category-specific; pass-through for Cat I/II, fund-level for Cat III |

| Ideal for | Transparent equity investing, ₹50L–₹2Cr+ corpus | Alternative strategy access, longer horizons, ₹1Cr+ |

Quick decision guide:

- PMS suits investors who prioritize transparency, direct ownership, and listed equity exposure

- AIF is the right fit when you need private markets access or strategies outside listed equities

- Both can work together if your goals span liquid equity and alternative returns — and your investable assets support it

What Is PMS?

Portfolio Management Services is a SEBI-regulated investment product governed by the SEBI Portfolio Managers Regulations 2020. A professional portfolio manager builds and manages a customised portfolio — typically of listed equities or debt instruments — held directly in the investor's own demat account.

The critical distinction: you own the securities, not units in a fund. Every stock in the portfolio is registered in your name.

SEBI mandates a minimum investment of ₹50 lakh. In practice, Economic Times Wealth reports that PMS becomes meaningful when an investor has ₹4–5 crore or more, reflecting the real-world economics of concentrated portfolio management.

Types of PMS

SEBI recognises three service models:

- Discretionary PMS — the portfolio manager takes all investment decisions independently; most common for HNI investors who want full delegation

- Non-Discretionary PMS — manager recommends, investor approves each transaction; suits investors who want involvement without doing the research themselves

- Advisory PMS — manager advises only; investor executes trades; suited to those with existing market knowledge who want a second opinion

PMS Fee Structure

Each service model above carries a similar fee framework. Per PMS Bazaar's market data, PMS fees typically include:

- Fixed management fee: 0.25%–2.5% of average portfolio value annually

- Performance fee: Charged above a hurdle rate on a High Water Mark basis — managers earn this only on net new gains, not on recovering prior losses

- Upfront fee: Prohibited by SEBI entirely

PMS Taxation

Because you hold securities directly, each transaction is taxed exactly as it would be in your personal demat account. Under Finance (No. 2) Act, 2024, for transfers on or after July 23, 2024:

- Short-Term Capital Gains (STCG) under Section 111A: 20%

- Long-Term Capital Gains (LTCG) under Section 112A: 12.5% above ₹1.25 lakh

These rates apply to listed equity. Surcharge, cess, and residency status affect your final liability — verify specifics with your tax advisor.

What Is AIF?

Alternative Investment Funds are SEBI-regulated pooled vehicles governed by the SEBI AIF Regulations 2012. Capital from multiple investors is combined and managed as a single fund. Investors receive units in the fund — not direct ownership of the underlying assets.

SEBI mandates a minimum of ₹1 crore per investor, reflecting the sophisticated and institutional nature of AIF investing. As of December 31, 2025, cumulative AIF net commitments stand at ₹15,74,050 crore across all categories, with Category II alone accounting for ₹11,64,118 crore.

AIF Categories in India

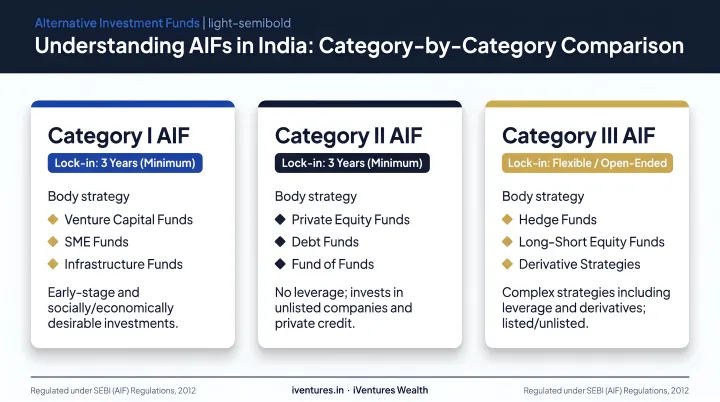

Category I AIFs invest in start-ups, early-stage ventures, SMEs, infrastructure, and social ventures. These carry longer lock-ins (typically 7–10 years) and suit investors with patient, development-oriented capital. All Category I AIFs are closed-ended.

Category II AIFs cover private equity, real estate funds, distressed asset funds, and structured credit — the most common AIF category for UHNI and family office portfolios. Lock-ins typically run 5–7+ years, and no leverage beyond day-to-day operational requirements is permitted.

For HNI investors, Category II is often the core alternative allocation — particularly private credit strategies, which have targeted 12–16% IRR as a fixed deposit replacement with meaningful illiquidity premium.

Category III AIFs use complex or diverse trading strategies — long-short equity, derivatives, quant, absolute return. These can use leverage. One important correction to a common assumption: Category III AIFs can be open-ended or closed-ended, per Regulation 13(1) of the AIF Regulations. Not all AIFs are locked-in products.

AIF: A Structural Advantage

Registered AIFs are classified as Qualified Institutional Buyers (QIBs) under SEBI ICDR Regulation 2(1)(ss). This gives AIF investors preferential access to IPO allocations and institutional placements that PMS structures cannot participate in — a meaningful advantage for certain investment strategies.

AIF Taxation

Beyond access advantages, how returns are taxed varies just as significantly — and the differences by category are often misunderstood. The rules differ sharply:

- Category I and II AIFs: Section 115UB provides pass-through taxation for non-business income — meaning gains retain their character and are taxed in the hands of unit holders as if they had invested directly. Business income is taxed at the fund level, with corresponding unit-holder income exempt.

- Category III AIFs: Section 115UB does not apply. Taxation depends on the fund's legal form, beneficiary structure, and income type.

The blanket claim that "all Category III income is taxed at Maximum Marginal Rate" is not supported by primary tax law — the actual liability depends on fund structure and income classification.

Consult a qualified tax advisor before making Category III AIF investments. Section 194LBB also requires TDS at 10% on distributions to resident unit holders.

PMS vs AIF: Which Is Right for You?

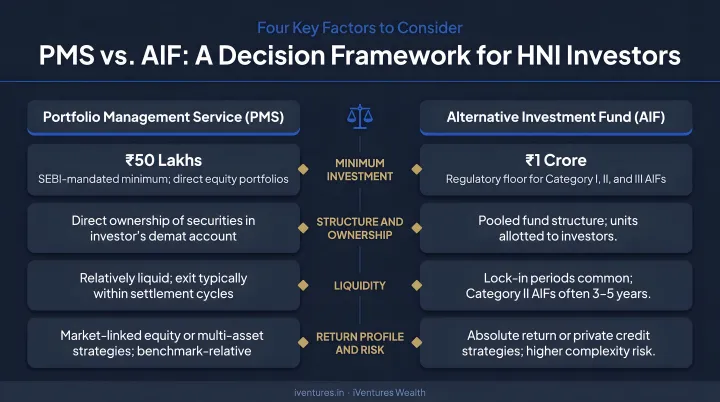

The decision comes down to four factors:

- Corpus size — Can you meet only the ₹50 lakh PMS threshold, or also the ₹1 crore AIF minimum?

- Liquidity needs — Do you need the ability to exit positions within months, or can you commit capital for 5–7+ years?

- Transparency preference — Do you want to see every holding in your demat, or are you comfortable with fund-level reporting?

- Strategy access — Are you satisfied with listed equity exposure, or do you want private equity, credit, or market-neutral strategies?

Situational Recommendations

Choose PMS if:

- Your investable corpus is ₹50 lakh to ₹1 crore

- You want direct ownership of listed equities with real-time visibility

- Flexibility to review and exit positions matters to you

- You want a portfolio tailored to your specific risk profile and goals

Choose AIF if:

- You have ₹1 crore or more and a 5+ year horizon

- You want access to private equity, structured credit, real estate strategies, or hedge-fund-style returns

- QIB privileges and institutional-grade access are relevant to your strategy

- You're comfortable with pooled fund reporting over direct demat visibility

Consider both if:

- Your corpus is ₹2 crore or more

- You want PMS as a liquid, transparent listed equity core alongside an AIF allocation for alternative strategies

- The goal is complementary diversification rather than choosing one product over the other

Whichever path fits your situation, the advisor you choose matters as much as the product. iVentures Wealth operates as a SEBI-registered RIA (INA000019026) on a fee-only model — no distributor commissions, no AIF placement fees accepted. PMS and AIF recommendations are made purely on suitability, not on which product pays the advisor more. With 20+ years advising UHNIs, founders, and family offices, the iVentures team evaluates PMS managers and AIF fund houses using a CFA-led due diligence framework, consolidating both into a single portfolio view through the Wealth Monitor App.

Conclusion

PMS and AIF solve different problems. PMS gives you a transparent, personalised equity portfolio you own directly — well-suited to investors who want visibility, flexibility, and listed market exposure. AIF opens access to private markets, alternative strategies, and institutional privileges that listed equity investing simply cannot replicate.

The right structure depends on your corpus size, how long your capital can stay committed, and what role this allocation plays in your broader portfolio. Both can coexist — and for many HNIs and UHNIs, they do.

If you're working through this decision, the iVentures Wealth team can help you evaluate PMS manager selection, AIF category fit, and liquidity alignment against your specific goals. With over ₹1,200 crore in assets under advice and 20+ years advising HNIs, UHNIs, and family offices across both structures, the team offers a frank, conflict-free assessment — not a product pitch.

Frequently Asked Questions

Is AIF better than PMS?

Neither is universally better. AIF offers access to private equity, credit, and hedge-fund strategies along with QIB privileges, while PMS provides direct ownership, transparency, and listed equity flexibility. The right fit depends on your corpus size, risk appetite, and how long you can stay invested.

What is the minimum investment for PMS and AIF in India?

SEBI mandates ₹50 lakh for PMS and ₹1 crore for AIF. In practice, most investors commit well above these floors — PMS portfolios below ₹1 crore can face limited diversification given concentrated strategy mandates.

How is PMS taxed differently from AIF in India?

PMS is taxed like direct stock ownership — STCG at 20% and LTCG at 12.5% above ₹1.25 lakh (rates as of July 23, 2024). AIF taxation varies by category: Category I and II use pass-through treatment under Section 115UB, while Category III depends on fund structure and income type.

Are AIFs riskier than PMS?

Risk levels vary within both products. PMS focuses on listed equities and is subject to market volatility. AIF risk ranges from moderate (Category I, early-stage or infrastructure) to high (Category III with leverage and derivatives). Evaluate each fund's specific strategy rather than relying on the product label alone.

Can NRIs invest in PMS or AIF in India?

Yes, NRIs and OCIs can invest in both products subject to FEMA guidelines. Tax implications — including TDS and DTAA applicability — differ from those for resident Indians, so consult an advisor with NRI tax structuring experience before committing.

Can I invest in both PMS and AIF at the same time?

Yes. Many investors with ₹2 crore or more hold both simultaneously — PMS for liquid, transparent equity exposure and AIF for alternative strategies. The two are complementary, and a consolidated portfolio view across both can help you track overall allocation and performance in one place.