Introduction

Most affluent Indian investors are told to focus on one thing: returns. Beat the benchmark, find the right fund, time the market correctly. But this framing misses the more important question — what is this wealth actually for?

Goal-based financial planning reframes that question entirely. Instead of asking "how did my portfolio perform this quarter," it asks "am I on track to fund what matters to me?" For HNI and UHNI investors managing multiple priorities at once — funding a next-generation business, planning an early exit, building a family legacy — that distinction matters. It's also a more effective way to manage wealth.

This article explains what goal-based financial planning is, why the conventional return-first model falls short, and the specific, measurable benefits that a structured goals-based approach delivers in practice.

Key Takeaways

- Goal-based planning organises wealth around life milestones — retirement, education, succession, legacy — not abstract return metrics.

- Each goal is matched to the right time horizon, risk level, and funding strategy for a more precise plan.

- Research shows a well-executed goals-based approach can generate 15.09% more utility-adjusted wealth than a return-only strategy.

- Without goal anchors, investors accumulate products instead of building coherent strategy, resulting in fragmentation and reactive decisions.

- The approach works best when reviewed consistently and adapted as life circumstances evolve.

What Is Goal-Based Financial Planning?

Goal-based financial planning starts with a simple but powerful question: what do you want your money to accomplish?

This approach starts with goals — their specific timelines, required corpus amounts, and risk parameters — and builds the portfolio around them. The investment strategy follows the goal, not the other way around.

The CFP Board defines financial planning as advising clients on how to achieve both short- and long-term financial goals by examining their entire financial picture. The CFA Institute describes goal-based portfolio theory as organising resources to maximise the probability of achieving goals, rather than optimising portfolio-level risk and return alone.

How It Differs from Traditional Approaches

Traditional Modern Portfolio Theory builds one portfolio designed to maximise returns at a given risk level. Goal-based planning treats risk differently — as the probability of not achieving a goal, not just portfolio standard deviation. Each goal gets its own funding strategy, time horizon, and risk posture — not a single blended profile applied across the board.

Common Goals in the Indian HNI Context

For affluent investors in India, the goals that typically anchor a financial plan include:

- Children's higher education — domestic institutions (IIT, IIM) and overseas (US, UK, Singapore), each with distinct corpus requirements and currency considerations

- Retirement or FIRE corpus — building sustainable income that doesn't depend on continued active work

- Property acquisition — primary residence, vacation property, or real estate as an asset class

- Business succession or exit — structuring post-liquidity event capital across safety, stability, and growth objectives

- Intergenerational wealth transfer — estate planning, trusts, and legacy structures for family continuity

Each goal carries a different funding timeline and risk tolerance. A well-structured goal-based plan addresses all of them in parallel — without letting one objective crowd out another.

Key Benefits of Goal-Based Financial Planning

Each benefit below is grounded in research and practical evidence — from investor behavior studies to published financial planning journals.

Benefit 1: Clarity, Direction, and Emotional Discipline

When money is tied to a specific goal with a defined timeline, investors gain something that market performance alone cannot provide: a clear sense of purpose. They know why they're saving, what they're working toward, and how to measure progress. That clarity removes the ambiguity that leads to inaction or erratic financial behaviour.

This matters most during market downturns. Morgan Stanley's analysis of over 119,000 financial plans during the 2020 COVID crash found that clients with quantified goals and financial plans stayed more disciplined during market stress than those without structured frameworks. When a short-term market correction is disconnected from a 15-year retirement goal, there is far less reason to act on panic.

The contrast is stark when goals are absent. DALBAR's 2025 investor behaviour report found the average equity investor earned 16.54% in 2024 versus 25.02% for the S&P 500 — an 848 basis point gap. That gap isn't explained by bad fund selection. It's explained by poor timing decisions driven by emotion rather than purpose.

Why this matters for Indian HNI investors specifically:

- HNIs often hold wealth across mutual funds, PMS, direct equity, real estate, FDs, and insurance without a clear, unifying framework

- Without goal-linked clarity, they accumulate products rather than build a coherent strategy

- The result is portfolio fragmentation and decision fatigue, not wealth optimization

iVentures Wealth's approach addresses this directly: every rupee invested is mapped to a specific goal, timeline, and required corpus so clients always know what the money is for and where they stand against each milestone. That clarity replaces reactive decision-making with structured discipline.

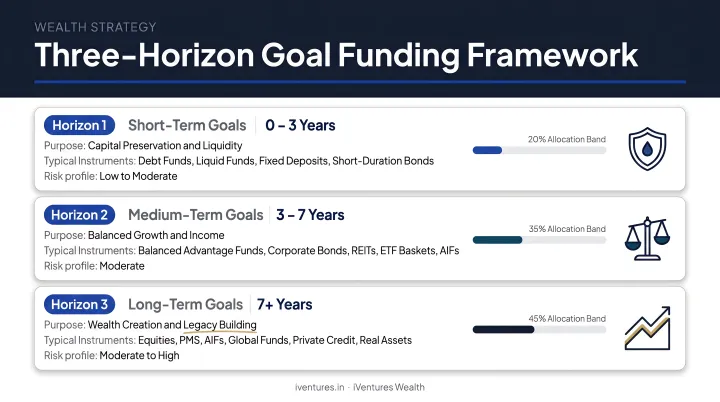

Benefit 2: Smarter Risk Allocation Across Goals

Not all goals share the same time horizon. A corpus needed in three years for a child's overseas education carries a completely different risk profile than a retirement corpus needed in twenty years. Goal-based planning is built around this reality — assigning the right level of risk to each goal rather than applying one blended risk profile across all objectives.

In practice, this means:

- Short-term goals (1–5 years): Funded with lower-volatility instruments : high-quality fixed income, liquid funds, short-duration debt

- Medium-term goals (5–15 years): Balanced, asset-allocated portfolios with moderate equity exposure

- Long-term goals (15+ years): Greater equity allocation to capture compounding and growth

This prevents two common and costly mistakes: being too conservative across the board (leaving long-term wealth under-compounded) or too aggressive (exposing near-term goals to unnecessary drawdown risk).

A 2018 study published in the Journal of Investment Management by Das, Ostrov, Radhakrishnan, and Srivastav found that 92% of clients found goal-probability language clear or quite clear — far higher than the 71% who found individual investment-oriented language clear. When risk is framed as "probability of not achieving your goal" rather than portfolio standard deviation, decision-making becomes more grounded and less reactive.

When this benefit matters most:

- Business owners with simultaneous liquidity events, retirement planning, and succession requirements — each needing distinct risk treatment

- NRIs balancing India and overseas financial obligations across different currency exposures

- Families in the pre-retirement phase, where protecting near-term needs without sacrificing long-term growth is the central challenge

iVentures Wealth operationalizes this through a three-bucket framework: a Safety Bucket (high-quality fixed income, 5–7 years of expenses), a Stability Bucket (balanced allocation, 8–15 year horizon), and a Growth Bucket (select AIF, PMS, and private equity for long-term multiplication). Each bucket exists because the goal it funds has different requirements — not from an arbitrary allocation formula.

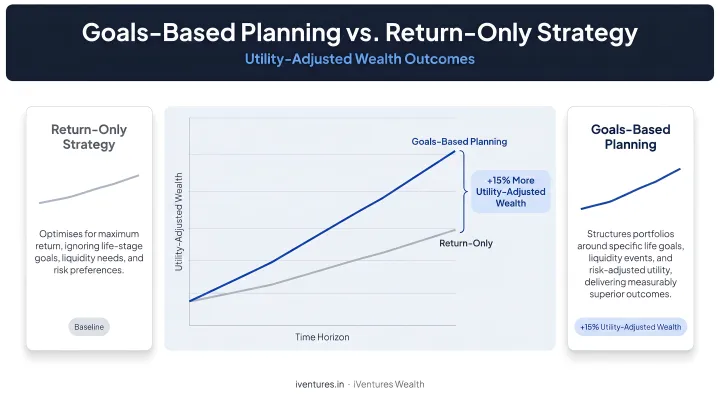

Benefit 3: Measurable Outcomes Beyond Portfolio Returns

In a goals-based framework, success isn't measured by alpha or benchmark outperformance. It's measured by the probability of achieving each specific goal. This shifts the definition of financial success from abstract market metrics to concrete life milestones — and that shift has a measurable financial value.

David Blanchett's 2015 study published in the Journal of Financial Planning found that a goals-based framework can produce 15.09% more utility-adjusted wealth compared to a naive return-only strategy — equivalent to generating an annual alpha of 1.65% per year over an investor's lifetime. This isn't a market-timing edge or a superior fund selection skill. It comes from better structural decisions: choosing which goals to fund, in what order, with what instruments.

Understanding "adviser's alpha" or planning gamma:

This concept — sometimes called Morningstar Gamma or Vanguard Adviser's Alpha — captures the measurable value created by strategic financial planning decisions, independent of investment selection. Vanguard's research estimates advisers can add around 3% in net returns through structured planning, with the benefit most visible during market stress or major life transitions.

What this looks like in practice: An investor who builds a coherent funding strategy for retirement — equity-heavy SIPs in accumulation, glide-path de-risking five years pre-retirement, then SWPs and bond ladders in distribution — will consistently outperform an investor holding the same funds but lacking a withdrawal strategy, rebalancing discipline, or goal-linked allocation logic.

When this benefit compounds most:

- Over long time horizons of 15 years or more

- For families with multiple goals competing for limited capital

- During the transition from wealth accumulation to wealth preservation — when the cost of a poorly structured drawdown plan is highest

What Happens When Goal-Based Planning Is Missing

Without a goal-based framework, portfolios tend to accumulate products rather than purpose — and the gaps show up in ways that are difficult to unwind.

The most common problems iVentures Wealth encounters with new clients arriving without a structured framework:

- Assets scattered across mutual funds, PMS, real estate, FDs, and insurance with no unifying strategy — and no way to assess whether any specific goal is on track

- Every market cycle brings a new "hot" sector or fund; clients enter after the run, exit after the drop, and repeat the cycle

- A single blended risk profile applied across the board leaves near-term goals over-exposed to volatility while long-term goals sit under-invested in growth assets

- According to a 2025 India Wealth Survey by Marcellus Investment Managers and Dun & Bradstreet, over 50% of Indian HNIs allocate more than 20% of wealth to real estate (excluding primary residence) — a concentration that leaves little room for structured, goal-linked diversification

- Kotak Private's 2024 Top of the Pyramid Report found that succession planning is considered critical by 2 in 3 Indian Ultra-HNIs, yet 30% have not yet considered it — a gap that compounds the longer it remains unaddressed

For HNI and UHNI investors, these aren't abstract risks. At larger portfolio sizes, a single misallocated decade — chasing returns without a goal anchor — can mean the difference between a self-sustaining family legacy and one that requires painful restructuring at the worst possible time.

How to Get the Most Value from Goal-Based Financial Planning

Goal-based planning delivers its full value when it functions as an ongoing process, not a one-time document. Three conditions determine whether it actually works:

- Goals are clearly defined and prioritised — with specific corpus targets, timelines, and success criteria for each

- Progress is reviewed regularly — at minimum annually, and after any major life event (business exit, inheritance, career transition, family change)

- The plan is actively updated — as income, priorities, market conditions, and family structures evolve

Meeting these conditions requires more than intent — it requires structure. iVentures Wealth conducts formal portfolio reviews at least quarterly, with active monitoring between cycles. Clients receive monthly consolidated statements and quarterly performance reports through the Wealth Monitor App, covering asset allocation, instrument-wise holdings, XIRR returns, maturity schedules, and benchmarked performance. When goals shift, the funding strategy and asset allocation shift with them.

That reporting infrastructure is only as useful as the advisory relationship behind it. A conflict-free advisory structure — built on planning fees rather than product commissions — ensures that every recommendation serves the plan, not a distributor's trail income.

As a SEBI-registered investment adviser (RIA), iVentures Wealth is legally prohibited from accepting commissions from product manufacturers. Across mutual funds, PMS, AIFs, bonds, and global funds, iVentures selects instruments purely on suitability to each client's goal.

Goal-based planning is not a document filed after an initial meeting — it is an active framework that evolves with income changes, market cycles, and life transitions. Investors who revisit and rebalance consistently tend to reach more milestones, with fewer reactive decisions along the way.

Conclusion

Goal-based financial planning ties every investment decision to a specific outcome — and holds the strategy accountable to that outcome over time, not just at the point of entry.

The benefits accumulate over time: sharper discipline during market volatility, smarter risk allocation across competing priorities, and wealth outcomes measured against real milestones rather than benchmark indices.

The framework scales to fit goals of any complexity, including:

- Building a retirement corpus on a defined timeline

- Funding a child's overseas education

- Executing a business exit or founder liquidity event

- Structuring a lasting family legacy across generations

Working with an independent, fiduciary-minded advisory firm like iVentures Wealth ensures the process stays personalised and accountable across every stage of the financial journey — from goal definition through execution and review.

Frequently Asked Questions

What is the difference between goal-based financial planning and traditional wealth management?

Traditional wealth management typically focuses on maximising portfolio returns relative to market benchmarks. Goal-based planning starts with defining specific life goals — retirement, education, legacy — and builds investment strategy around achieving them. Success is measured by goal completion, not market outperformance.

What types of financial goals does goal-based planning typically cover?

Common goals include retirement corpus, children's education (domestic and overseas), property acquisition, business succession or exit, emergency reserves, and intergenerational wealth transfer. Goals vary by life stage and should be prioritised by timeline, corpus requirement, and relative importance to the investor.

How does goal-based planning handle risk tolerance?

Risk is matched to each goal's specific time horizon and criticality. Near-term goals are funded with lower-risk instruments; long-term goals can tolerate greater equity exposure. This ensures no single risk profile compromises goals with very different timelines and urgency.

How often should a goal-based financial plan be reviewed or updated?

At minimum annually — and after any major life event such as a business exit, inheritance, marriage, or significant change in income. iVentures Wealth conducts formal reviews at least quarterly, with continuous monitoring between scheduled reviews.

Is goal-based financial planning only suitable for very wealthy investors?

No. The core framework — define goals, assign resources, track progress — benefits any investor who wants purposeful rather than reactive financial decisions. It scales particularly well for HNI and UHNI investors managing complex, multi-goal portfolios across multiple asset classes and entities.

What happens if my financial goals change significantly over time?

Goal-based planning is designed to be adaptive. When goals shift in priority, timeline, or scale, the funding strategy and asset allocation are adjusted accordingly. Regular plan reviews and an ongoing advisory relationship make this recalibration structured, not reactive.