Introduction

As your wealth grows, two services start appearing in every financial conversation — wealth management and private banking. Banks use these terms almost interchangeably, and yet choosing the wrong one can leave serious gaps: an unoptimised tax position, no estate structure, and investment advice shaped by product commissions rather than your actual goals.

Both services cater to affluent clients, both involve a dedicated relationship manager, and both promise personalised attention. The underlying purpose, scope, and loyalty structure, however, are not the same.

This article cuts through the overlap — clear definitions, a side-by-side comparison, and a practical framework for deciding what your situation actually requires. It's written for:

- Business founders navigating a post-liquidity event

- NRIs managing cross-border assets across jurisdictions

- CXOs holding a concentrated ESOP portfolio

TL;DR

- Wealth management is a holistic, long-term advisory service covering investment management, tax optimization, estate planning, and succession strategy for growing, protecting, and transferring wealth across generations.

- Private banking is a premium banking service for HNIs: dedicated relationship managers, preferential deposit rates, tailored lending, and exclusive credit facilities.

- The core difference is scope — private banking handles your financial transactions; wealth management designs your entire financial strategy.

- Private banking is limited to one institution's product shelf — independent wealth managers advise across all needs, free of product constraints.

- Many affluent clients use both — but for different purposes. Your financial complexity and long-term goals should guide the choice.

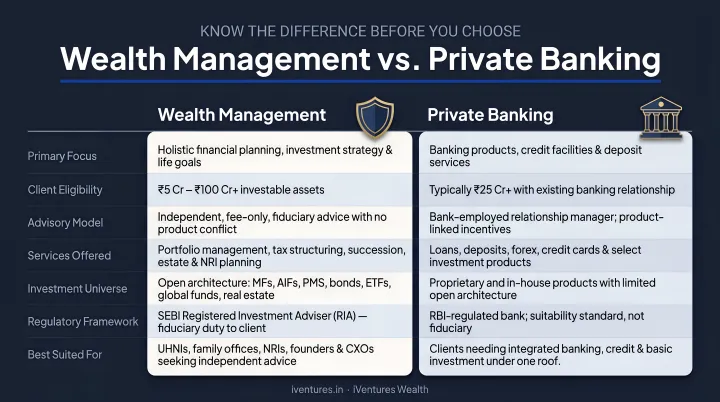

Wealth Management vs Private Banking: Quick Comparison

Here's how wealth management and private banking compare across the dimensions that matter most to HNIs and UHNIs in India.

| Dimension | Wealth Management | Private Banking |

|---|---|---|

| Primary Focus | Holistic financial strategy | Banking convenience and transactions |

| Typical Services | Portfolio management, tax planning, estate planning, succession, NRI advisory | Deposits, lending, mortgages, credit facilities, FX |

| Relationship Structure | Multi-disciplinary team (advisor, tax, estate) | Single relationship manager |

| Time Horizon | Multi-decade, generational | Short to medium term |

| Typical Client Threshold (India) | ₹1–2 Cr investable (deeper services from ₹5 Cr+) | Varies by institution (see below) |

| Fee Model | AUM-based or flat advisory fee, paid by client | Revenue via lending margins and product distribution |

| Fiduciary Standard | SEBI-registered RIAs legally required to act as fiduciaries | No statutory fiduciary obligation to client |

In India, private banking is offered by large banks — HDFC Bank Imperia, ICICI Bank Private Banking, Kotak Private, and Axis Burgundy Private. SEBI-registered investment advisory firms deliver independent wealth management — a structural difference with direct implications for the advice you receive.

Several banks now label their premium banking arms "wealth management." This article distinguishes them not by label, but by the depth and independence of advisory.

What is Wealth Management?

Wealth management is an advisory-driven service that integrates investment management, financial planning, tax optimisation, estate structuring, and succession planning into a single coordinated strategy — built around your life goals and risk profile, not just your asset size.

Core Services

A full-service wealth management mandate covers:

- Portfolio construction across mutual funds, equities, bonds, PMS, AIFs, private credit, and global funds

- Tax planning to minimise liabilities across multiple income streams, including ESOP liquidations, business sale proceeds, and rental income

- Estate and succession planning to structure smooth intergenerational transfers, including private trusts and will drafting

- NRI and cross-border advisory covering DTAA structuring, LRS planning, and multi-jurisdiction compliance

- Family office services for complex multi-entity structures with consolidated reporting across all custodians

The Relationship Model

Clients work with a coordinated team of specialists — an investment advisor, tax expert, and estate planner — rather than a single banker. The team functions as your dedicated financial CFO, managing complexity across disciplines so you don't have to coordinate it yourself.

This is the model iVentures Wealth (SEBI RIA No. INA000019026) has operated since 2005 — serving 150+ affluent families, UHNIs, founders, and CXOs, with ₹1,200 Cr+ in assets under advice through a fee-only, CFA-led team.

Who Needs Wealth Management?

The value isn't only about asset size — it's about complexity. Wealth management is designed for:

- HNIs and UHNIs with investable assets from ₹1–2 Cr (deeper services from ₹5 Cr+)

- Business founders who have exited a stake and need tax structuring, reinvestment strategy, and succession planning

- NRIs managing assets across India and one or more overseas jurisdictions

- CXOs with concentrated ESOP positions requiring tax-efficient liquidation strategies

- Family businesses and family offices requiring multi-generational governance frameworks

The Fiduciary Dimension

This is where wealth management and private banking diverge most sharply. Under Regulation 15(1) of the SEBI Investment Advisers Regulations, 2013, SEBI-registered investment advisers are legally required to act in a fiduciary capacity towards clients. Regulation 15(2) goes further — an adviser cannot receive consideration from any third party for products on which advice is given.

This means SEBI-registered wealth managers cannot earn commissions on what they recommend. Their only revenue comes from the client. That single structural constraint — no product commissions — is what makes the advice structurally different from what a bank relationship manager can offer.

What is Private Banking?

Private banking is a high-touch banking service offered exclusively to HNI clients. A dedicated relationship manager serves as a single point of contact, helping clients bypass standard banking procedures, access preferential rates, and process transactions quickly. The focus is on convenience and exclusivity — not long-term financial strategy.

Typical Services

- Preferential savings and current account terms

- Customised lending, overdraft, and mortgage solutions

- Premium credit facilities and foreign exchange services

- Access to the bank's proprietary investment products

- Basic mutual fund distribution (in some cases)

Minimum Thresholds in India

Entry requirements vary significantly by institution:

| Program | Eligibility Threshold |

|---|---|

| HDFC Bank Imperia | ₹1 Cr TRV; or ₹10 L savings AMB; or ₹30 L combined retail liability value; or ₹3 L monthly salary credit (effective July 2025) |

| ICICI Bank Private Banking | ₹5 Cr relationship value; or ₹50 L deposits plus balance; or ₹8 L net monthly salary credit |

| Kotak Private (Reserve Programme) | ₹7.5 Cr group relationship value plus ₹50 L average yearly savings balance |

| Axis Burgundy Private | ₹5 Cr TRV within 12 months; or ₹10 L net monthly salary credit |

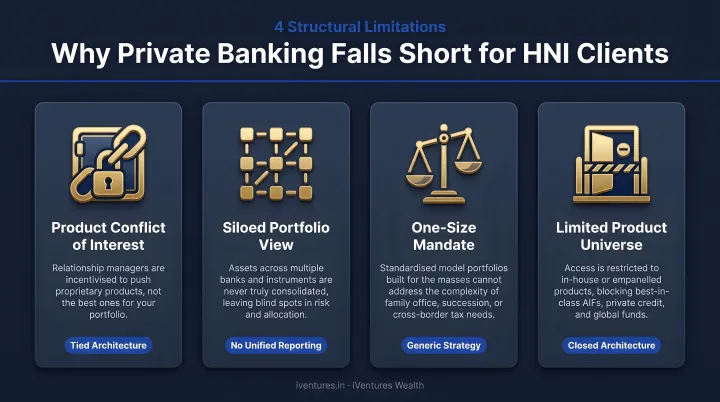

Key Limitations

Private banking is well-suited for banking convenience. It is structurally limited in several ways that matter as wealth grows in complexity:

- The relationship manager's primary obligation is to the bank, not you

- Advice is constrained to the bank's own product shelf — there is no open-architecture access

- RM attrition is a real problem — Mint has reported attrition rates in bank wealth divisions as high as 40%, with firms offering 20–40% salary hikes to poach talent, meaning clients frequently rebuild relationships from scratch

- Comprehensive tax planning, estate structuring, and independent portfolio management are outside the scope of what a private banker can deliver

Key Differences: Wealth Management vs Private Banking

Purpose and Primary Focus

Private banking handles your financial day-to-day: deposits, credit, transactions. Wealth management is built around a different question entirely — what does your money need to do over the next 10, 20, or 30 years?

That distinction sounds straightforward, but it carries real consequences. A business founder who receives ₹100 Cr from a partial stake sale needs tax structuring on the capital gains, a reinvestment framework across multiple asset classes, a family trust to ring-fence the corpus, and a succession plan. A private banker can open an account and suggest a fixed deposit. A wealth manager builds the entire architecture around it.

Scope of Services

Private banking's scope is institution-bound — products the bank offers. Wealth management is open-architecture and comprehensive.

Private banking covers:

- Deposits and account management

- Lending and credit solutions

- FX services

- The bank's own investment products

Wealth management covers:

- Full investment management across all regulated products

- Independent tax planning across income streams

- Estate and succession structuring

- NRI and cross-border advisory

- Consolidated reporting across all custodians and family entities

Fee Model and Transparency

That difference in scope connects directly to how each model earns money. Private banks generate revenue through lending margins and distribution commissions on investment products. Per SEBI's Mutual Fund Investor FAQs, mutual fund distributors — which includes bank-distributed products — receive commissions from fund houses within SEBI's expense ratio rules, and these commissions are disclosed in the Consolidated Account Statement.

SEBI-registered investment advisers operate differently. Under Regulation 15(2) of the 2013 IA Regulations, they cannot accept any consideration from third parties for products advised. Fees are charged directly to the client — AUM-based, flat advisory, or mandate-based — and disclosed transparently in the advisory agreement.

The practical difference: a commission-based model creates incentives to recommend products that generate higher commissions. A fee-only model aligns the advisor's revenue entirely with client outcomes.

Fiduciary Standard and Conflict of Interest

The fiduciary distinction here is legal, not philosophical. The SEBI IA Regulations, 2013 mandate fiduciary duty for registered advisers. Bank-employed relationship managers distributing investment products operate under RBI's banking and distribution framework, which requires disclosure but stops short of mandating that the RM prioritise client interests over the bank's.

In short: a private banker's primary obligation is to the bank. A SEBI-registered investment adviser's obligation is to you — and that's enforceable.

Which One Do You Need?

Decision Framework

Choose private banking if:

- Your primary need is banking convenience — faster transactions, preferential rates, tailored credit

- You already have a robust investment and financial planning strategy in place elsewhere

- Your financial structure is straightforward

Choose wealth management if:

- You need help building or refining your overall financial strategy

- You have complexity — business income, NRI status, ESOP portfolios, estate planning needs, or multiple asset classes

- You want independent advice that isn't shaped by product commissions

Can You Have Both?

Yes — and many affluent clients do. The optimal structure is a SEBI-registered wealth manager handling holistic strategy and portfolio oversight, working alongside a private bank managing banking transactions and credit.

The key condition: ensure your wealth manager is independent of the bank. iVentures Wealth, for instance, works alongside existing private banking relationships, coordinating across custodians through consolidated reporting with no commissions from product manufacturers — keeping advice conflict-free regardless of which bank holds your accounts.

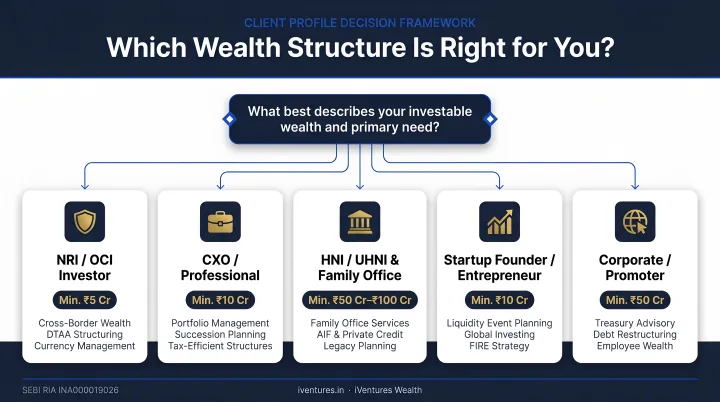

Client Profiles

| Client Profile | Recommendation |

|---|---|

| Business founder post-liquidity event | Wealth management for tax structuring, reinvestment strategy, trust structuring, and succession planning |

| NRI with Indian asset base | Wealth management with dedicated NRI advisory for DTAA structuring, multi-jurisdiction compliance, and cross-border estate planning |

| Senior CXO with concentrated ESOP portfolio | Wealth management for tax-efficient liquidation strategy, diversification framework, and estate planning |

| Established investor needing better banking rates and credit | Private banking may be sufficient if investment strategy is already well-managed independently |

Conclusion

Private banking and wealth management serve different purposes at different stages of financial complexity. Private banking offers convenience and exclusivity. Wealth management offers coordinated financial strategy built around your actual goals — not a product shelf.

For investors whose wealth has grown beyond straightforward banking needs — multiple income streams, business interests, estate concerns, NRI status — wealth management provides the strategic depth and multi-disciplinary expertise that private banking is not structured to offer.

Deloitte India projects demand for wealth management services in India to grow from US$1.1 trillion in AUM in FY24 to US$2.3 trillion by FY29. As India's HNI and UHNI segments expand, the need for genuinely independent, fiduciary-grade wealth management becomes more pressing.

Review your current financial situation against the framework in this article. If you're uncertain which model fits your needs, a SEBI-registered investment adviser like iVentures Wealth can provide a needs assessment without the conflict of a product shelf to sell from.

Frequently Asked Questions

Is private banking under wealth management?

Private banking is sometimes described as a subset of wealth management, but in practice the two are distinct. Private banking focuses on personalised banking services; wealth management is a broader advisory discipline covering investments, tax, estate, and succession. The depth and independence of advice from a bank's wealth arm varies significantly from a standalone SEBI-registered adviser.

What is the minimum amount needed for private banking in India?

Thresholds vary by institution. HDFC Bank Imperia requires ₹1 Cr TRV (or ₹10 L savings AMB as an alternative). ICICI Bank Private Banking requires ₹5 Cr relationship value. Kotak Private's Reserve Programme requires ₹7.5 Cr group relationship value. Axis Burgundy Private requires ₹5 Cr TRV. These figures reflect current official eligibility criteria.

Can I use both wealth management and private banking at the same time?

Yes — many HNIs do. The typical structure is a SEBI-registered wealth manager handling holistic strategy and portfolio oversight, with a private bank managing day-to-day transactions and credit. This works best when the wealth manager is independent of the bank, ensuring advice is not shaped by the bank's product interests.

What is the difference between a private banker and a wealth manager?

A private banker is a bank employee focused on lending, deposits, and credit products, with a primary obligation to the institution. A SEBI-registered RIA is a fiduciary legally required to act in the client's best interest, providing comprehensive advisory across investments, tax, and estate planning.

Is wealth management more expensive than private banking?

Wealth management fees — typically AUM-based or fixed advisory fees — are disclosed upfront. Private banking earns through lending margins and product commissions that are less visible. The right comparison is value delivered relative to cost, not just the fee line.

Are wealth managers fiduciaries in India?

SEBI-registered Investment Advisers (RIAs) are legally required to act as fiduciaries under the SEBI Investment Advisers Regulations, 2013. They must act in the client's best interest, disclose all conflicts, and cannot earn commissions on advised products — the key distinction from commission-based distributors or bank-affiliated advisers.