This article covers what automated portfolio rebalancing is, how portfolio drift erodes wealth, the four primary rebalancing strategies, tax-smart execution in India, and how to choose the right approach for a complex UHNI portfolio.

Key Takeaways

- Automated rebalancing uses algorithmic rules to restore target allocations without manual intervention

- Portfolio drift quietly pushes risk exposure beyond your intended level across multiple asset classes — often before you notice it

- Four primary strategies exist: calendar-based, threshold-based, hybrid, and CPPI/dynamic

- Post-Budget 2024 tax rates — LTCG at 12.5% (above ₹1.25 lakh), STCG at 20% — make a tax overlay essential when rebalancing

- Complex UHNI portfolios benefit most from automation-assisted advisory, not pure automation alone

What Is Automated Portfolio Rebalancing?

Automated portfolio rebalancing uses algorithms and software rules to adjust asset allocation back to a predefined target when it drifts, without requiring the investor to manually calculate and place every trade.

The mechanics are straightforward: an investor or advisor sets a target allocation (for example, 60% equity, 20% debt, 10% gold, 10% alternatives), defines when rebalancing should trigger (by time interval or drift threshold), and the automated system executes adjustments accordingly.

Manual rebalancing, by contrast, requires periodic weight reviews, deviation calculations, and individual buy/sell orders. At scale — a portfolio with 15–25 positions across multiple asset classes and entities — this is time-consuming, error-prone, and typically demands a full day's work per rebalancing event.

What automated rebalancing is not:

- A market-timing tool or active trading strategy

- A guarantee of higher returns

- A replacement for fiduciary judgment

Its core purpose is keeping investors from over-concentrating in recent winners or abandoning underperformers at the wrong moment. The goal is to maintain a consistent risk-return profile aligned with the investor's Investment Policy Statement (IPS) — not to chase performance.

How Portfolio Drift Silently Erodes Wealth

Consider a straightforward example. An investor holds 60% equity and 40% debt. The Nifty 50 rallies 30% over 12 months while debt returns 7%. Equity now represents approximately 68–70% of the portfolio — significantly above target. The investor is now bearing far more equity risk than originally intended, without ever making a conscious decision to increase it.

This unintended tilt is made worse by investor behaviour. Two patterns repeat consistently:

- Rising markets: Investors resist rebalancing because selling winners feels wrong — even when the allocation has drifted well beyond risk tolerance

- Falling markets: The impulse shifts to exiting equity entirely, locking in losses and abandoning the original strategy

Both responses accelerate the drift rather than correct it.

Global data illustrates the cost of this behaviour gap. Morningstar's 2025 Mind the Gap study found investors earned 7.0% annually versus 8.2% for the funds they held over the 10 years ended December 2024 — a 1.2 percentage point gap driven largely by mistimed cash flows and allocation decisions.

Why UHNI Portfolios Face Greater Complexity

A standard two-asset portfolio drifts in one direction. A UHNI portfolio spanning equity, debt, gold ETFs, AIFs, PMS, and international funds drifts in multiple directions simultaneously.

SEBI data shows PMS AUM reached ₹37,80,099 crore as of March 2025, while AIF commitments crossed ₹13,49,051 crore — reflecting how layered these portfolios have become.

A rally in a single PMS or international allocation can throw the entire portfolio off balance in ways that are invisible without consolidated reporting across all entities.

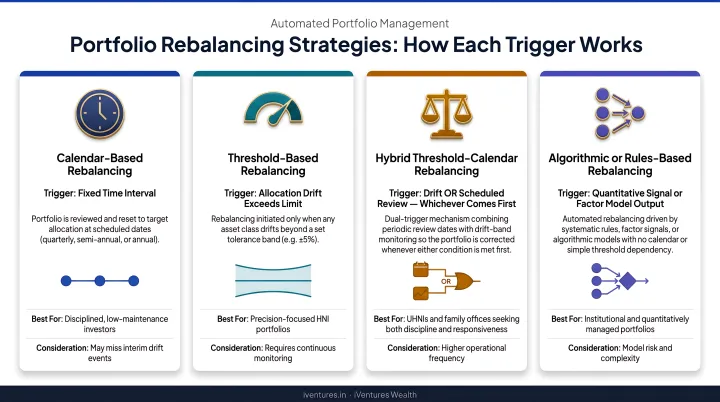

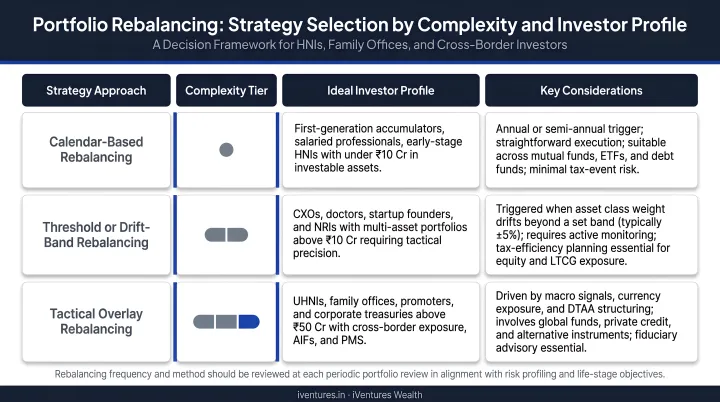

Automated Portfolio Rebalancing Strategies Explained

Four primary automated strategies exist, each with a different trigger mechanism. Sophisticated wealth management approaches typically combine elements of more than one.

Calendar-Based Rebalancing

Calendar-based rebalancing triggers portfolio review and adjustment at fixed time intervals — monthly, quarterly, semi-annually, or annually.

It is simple to systematise and easy to schedule — but it is time-blind to market conditions. A calendar trigger may fire when drift is minimal, generating unnecessary cost and tax, or it may lag significantly after a sharp market move.

Vanguard's 2010 research on rebalancing best practices confirmed that the primary goal of rebalancing is risk control relative to target allocation. More frequent rebalancing often generates transaction costs without proportional risk benefit. Annual reviews remain a sensible baseline for most long-term investors.

Threshold-Based (Constant-Mix) Rebalancing

Threshold-based rebalancing triggers a review only when an asset class drifts beyond a predefined band — for example, equity moves more than 5% above or below its target weight.

This approach is more responsive than calendar-based rebalancing and avoids unnecessary trades during stable markets. The CFA Institute illustrates a practical example: a 60% stock target with a 55%–65% corridor, triggering rebalancing only when the band is breached.

Setting the right band width is the key decision:

- Too narrow → excessive trading and tax events

- Too wide → significant risk drift goes unaddressed

- A ±5 percentage-point band is a research-backed reference point for diversified portfolios, though it should be customised to the investor's risk sensitivity and transaction cost structure

Hybrid (Calendar + Threshold) Rebalancing

The hybrid approach combines both triggers: the portfolio is reviewed on a fixed schedule (for example, quarterly), and rebalancing executes only if drift exceeds a defined threshold at the time of review.

This avoids the two failure modes — unnecessary trades from pure calendar rebalancing and the constant monitoring demand of pure threshold rebalancing. For most UHNI investors with complex, multi-asset portfolios, the hybrid approach is the most practical automated strategy. It ensures regular oversight while filtering out market noise.

CPPI and Dynamic Flow-Based Rebalancing

Constant Proportion Portfolio Insurance (CPPI) sets a floor value for the portfolio and dynamically allocates between risky assets (equities) and safe assets (bonds/cash) based on a "cushion" — the difference between the current portfolio value and the floor.

The core formula: Exposure = Cushion × Multiplier

- As the portfolio grows above the floor, more is allocated to risky assets

- As it approaches the floor, the system shifts toward safety

CPPI is well-suited for investors with capital preservation mandates: family trusts, retirees, or those approaching a major liquidity event such as a business exit. In practice, iVentures Wealth structures similar outcomes for post-liquidity clients through a three-bucket approach — a Safety bucket in high-quality fixed income, a Stability allocation, and a Growth allocation — which creates floor-like protection without requiring a formal CPPI overlay.

Cash-flow-based rebalancing is a distinct and often underutilised technique. Rather than selling overweight positions, it directs new contributions or SIP flows into underweight asset classes — achieving rebalancing without triggering sell-side capital gains. For investors in higher tax brackets, this distinction matters significantly.

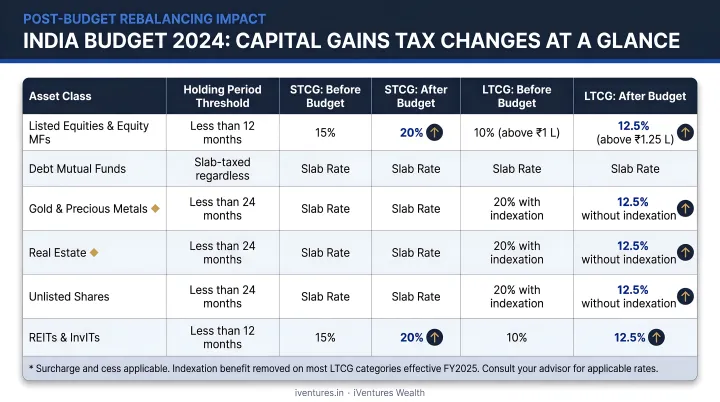

Tax-Smart Rebalancing: What Indian Investors Need to Know

Rebalancing involves selling assets, which triggers capital gains tax. In India, the tax treatment varies significantly by asset class and holding period — and the rules changed materially after Budget 2024.

Current Tax Rates (Post-Budget 2024, Effective July 23, 2024)

| Asset Class | STCG Rate | LTCG Rate | LTCG Threshold |

|---|---|---|---|

| Listed equity / equity-oriented funds | 20% | 12.5% | ₹1.25 lakh per year |

| Debt mutual funds (acquired after Apr 1, 2023) | Taxed at slab rates | Taxed at slab rates | No indexation benefit |

| AIF Category I & II | Pass-through applies (Section 115UB) | Pass-through applies | Per investor's tax status |

Note: These rates are based on Budget 2024 amendments. Verify current rates against the applicable Finance Act before making rebalancing decisions.

The shift in debt fund taxation under Section 50AA is particularly significant. Gains from specified mutual fund units acquired on or after April 1, 2023 are treated as short-term capital gains regardless of holding period, with no indexation benefit available. This fundamentally changes the rebalancing economics for debt-heavy allocations.

Tax-Efficient Rebalancing Techniques

1. Rebalancing through new inflows Direct fresh investments or SIP flows into underweight asset classes rather than selling overweight ones. No sell-side tax event is triggered. This is the primary lever for UHNI investors with large embedded gains.

2. Loss set-off and carry-forward (Sections 70, 71, and 74) Selling underperforming positions to realise losses that offset capital gains elsewhere in the portfolio. Capital losses cannot be set off against other income heads, but unabsorbed losses carry forward for up to 8 assessment years under Section 74 — a meaningful buffer when rebalancing across a multi-year horizon.

3. Holding period management Waiting until a position crosses the one-year threshold before selling can shift the tax rate from 20% (STCG) to 12.5% (LTCG) on equity holdings — a material difference on large lots. iVentures' advisory process applies the same LTCG-efficient lot logic to SWP withdrawals and discretionary rebalancing trades alike.

For UHNI portfolios with large embedded gains, automated rebalancing triggers without a tax overlay can erode the very risk management benefit the rebalance was meant to achieve. Advisory oversight at the trigger level is where tax efficiency is either preserved or lost.

Choosing the Right Rebalancing Approach for Your Portfolio

The right strategy depends on four variables:

- Portfolio complexity — number of asset classes, instruments, and entities

- Risk tolerance and investment horizon — shorter horizons or tighter mandates warrant more responsive systems

- Tax situation — embedded gains, applicable rates, holding periods, and entity-level tax treatment

- Liquidity needs and life-stage goals — retirement proximity, business exits, or inheritance events

A practical framework:

| Portfolio Type | Recommended Approach |

|---|---|

| 2–3 asset classes, smaller AUM | Calendar-based or simple threshold automation |

| Multi-asset, diversified HNI | Hybrid (quarterly review + ±5% threshold) |

| UHNI with AIFs, PMS, international | Hybrid + advisory oversight with tax overlay |

| Capital preservation mandate | CPPI-style or bucket framework with floor protection |

The Role of an Investment Policy Statement

The IPS is the foundation of any disciplined rebalancing programme. It should define:

- Target allocations per asset class and entity

- Drift tolerance bands

- Rebalancing frequency and trigger mechanism

- Tax constraints and holding period rules

- Liquidity reserves and life-stage adjustments

Without a written IPS, even automated systems lack a clear mandate, and rebalancing decisions become reactive. SEBI regulations require Investment Advisers to conduct formal risk profiling and maintain documented client records, making the IPS the natural extension of this compliance foundation into an actionable allocation framework.

When to Escalate from Automated to Advisor-Led Review

Automated triggers should pause for human judgment when:

- A significant life event occurs (retirement, business exit, inheritance, liquidity event)

- The tax cost of executing a rebalancing trade exceeds a meaningful threshold relative to the risk benefit

- Major macro-regime shifts occur (interest rate cycle changes, significant currency moves for NRIs)

- A position is approaching an LTCG threshold that would alter the tax treatment of a sale

iVentures Wealth combines continuous portfolio monitoring with quarterly reviews, triggering rebalancing based on risk, return, and cash-flow needs rather than calendar dates alone. The Wealth Monitor App gives clients and advisors a consolidated, real-time view across mutual funds, equities, bonds, AIFs, PMS, and FDs — so every rebalancing decision starts from a complete picture.

Frequently Asked Questions

What is automated portfolio rebalancing?

Automated portfolio rebalancing uses software or algorithmic rules to adjust a portfolio's asset allocation back to its target weightings when drift occurs — without requiring manual trades for each adjustment. This enforces allocation discipline systematically, maintaining the investor's intended risk-return profile over time.

Is automated portfolio rebalancing a good idea?

For most investors with diversified, multi-asset portfolios, automated rebalancing reduces behavioural drag and maintains consistent risk exposure by removing emotional decision-making from the process. For complex UHNI portfolios with significant embedded gains, automated triggers should be complemented by advisory oversight to manage the tax implications of each rebalancing event.

What is the best way to rebalance a portfolio?

The most effective approach for most investors is a hybrid of calendar and threshold-based rebalancing: reviewing the portfolio at set intervals and acting only when drift exceeds a predefined band. Prioritize directing new contributions to underweight assets before triggering sell-side events to reduce unnecessary capital gains.

How often should a portfolio be rebalanced?

Annual rebalancing is a reasonable baseline for most long-term investors, as more frequent rebalancing can generate unnecessary transaction costs and tax events. Complex portfolios with high volatility or tight risk mandates may warrant semi-annual reviews with threshold triggers that respond to significant market dislocations.

What are the tax implications of portfolio rebalancing in India?

Post-Budget 2024, listed equity STCG is taxed at 20% and LTCG at 12.5% (above ₹1.25 lakh). Debt fund gains (for units acquired after April 1, 2023) are taxed at slab rates with no indexation benefit. Use new-inflow rebalancing and capital loss set-off strategies to reduce the tax cost of rebalancing. Verify current rates against the applicable Finance Act before execution.

What triggers automated portfolio rebalancing?

Automated rebalancing is triggered by two primary mechanisms: a calendar schedule or a drift threshold (when an asset class moves beyond a set percentage from its target weight). Hybrid systems use both, and dynamic systems may also trigger rebalancing through cash flow events such as new deposits or withdrawals directed toward underweight allocations.