Today, investing in foreign stocks from India is legal, accessible, and increasingly common. According to Mint, Indian investors hold an average of 8 global stocks, with top picks including Nvidia, Apple, Tesla, Meta, and Alphabet. That number will only grow.

But accessible doesn't mean simple. The route you choose, your tax compliance, currency exposure, and investment objective all determine whether international investing adds real value to your portfolio — or just adds complexity.

This guide covers every method available to Indian investors, what you need to get started, the factors that genuinely affect outcomes, and the mistakes that cost people money.

Key Takeaways

- Indian residents can invest in foreign stocks legally under RBI's LRS, up to USD 2,50,000 per financial year

- Routes include overseas broker accounts, international mutual funds, India-listed ETFs, and PMS mandates — each with distinct cost, tax, and complexity trade-offs

- Foreign gains are taxable in India; Schedule FA and Schedule FSI disclosure in your ITR is mandatory, not optional

- TCS at 20% applies on LRS remittances above ₹10 lakh, adjustable against your final tax liability

- iVentures Wealth recommends 10–30% global allocation for most HNI portfolios as part of a structured diversification strategy

Ways to Invest in Foreign Stocks from India

Indian investors have both direct and indirect routes available under SEBI and RBI regulations. The right method depends on investment size, how actively you want to be involved, and your tax preferences.

Direct Investing via Overseas or Domestic Brokers with International Tie-ups

This route gives you direct ownership of foreign shares — Apple, Tesla, Nvidia, or any listed US stock. Several Indian brokers have built partnerships specifically for this:

| Indian Broker | International Partner | Fractional Investing |

|---|---|---|

| HDFC Securities | Vested Finance / VF Securities | From 1 cent |

| ICICI Direct | Interactive Brokers LLC | Yes |

| Axis Direct | Vested Finance / DriveWealth | From USD 1 |

| Kotak Neo | Interactive Brokers | No minimum |

Funds are remitted via LRS through an authorised bank. You fill Form A2, send the wire, and the amount counts against your USD 2,50,000 annual LRS envelope.

This is best suited for active, informed investors. Direct ownership means you're also responsible for tracking dividend withholding tax, Schedule FA reporting, and foreign tax credit claims.

International Mutual Funds and Fund of Funds (FoFs)

International mutual funds are India-domiciled funds managed by Indian AMCs that invest in foreign equities. Fund of Funds (FoFs) take it one step further — they invest in overseas mutual fund schemes. Both allow SIP investment in INR, with no need for an overseas account or LRS remittance.

Key points:

- Professional fund management handles stock selection and rebalancing

- INR-denominated, SEBI-regulated — familiar and straightforward

- Expense ratios tend to be higher than domestic funds

- Tax treatment: Under Finance Act 2023's Section 50AA, gains from these funds are generally treated as short-term and taxed at slab rates — they do not receive the equity fund taxation benefit

International ETFs Listed on Indian Exchanges

This is the most accessible route for most retail investors. ETFs like Mirae Asset NYSE FANG+ ETF (NSE: MAFANG) and Motilal Oswal Nasdaq 100 ETF trade on NSE and BSE just like any domestic stock — through your regular demat account, no LRS required.

The Mirae Asset NYSE FANG+ ETF, for example, had an AUM of ₹3,748.74 crore with an expense ratio of 0.66% as of June 2026.

Before investing, check:

- AUM and liquidity (low AUM means wider bid-ask spreads)

- Tracking error relative to the underlying index

- Expense ratio

- Portfolio composition — some "international" ETFs have heavy concentration in 5–10 stocks

Depository Receipts — ADRs, GDRs, and IDRs

Three instruments fall under this category:

- ADRs (American Depositary Receipts) — USD-denominated instruments on US exchanges representing foreign company shares; require LRS remittance

- GDRs (Global Depositary Receipts) — similar structure, traded on European exchanges

- IDRs (Indian Depositary Receipts) — foreign companies raising capital from Indian investors through Indian exchanges in INR

Standard Chartered Bank was India's only notable IDR issuer, but it delisted its IDRs from BSE and NSE effective 22 July 2020. No active foreign-company IDR is currently listed on Indian exchanges.

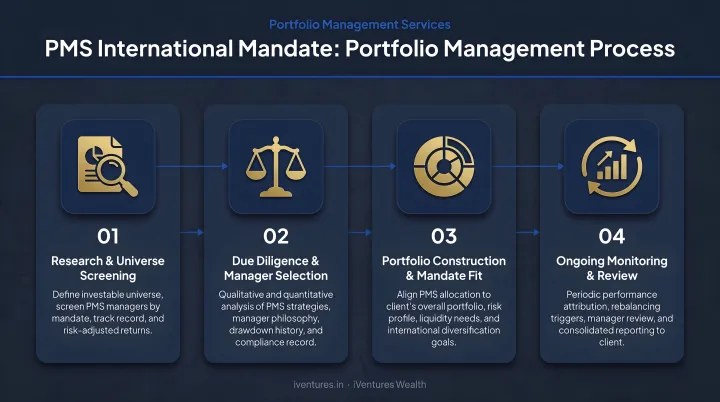

Portfolio Management Services (PMS) with International Mandate

For HNI investors with ₹50 lakh or more, SEBI-registered Portfolio Management Services providers can construct and actively manage a globally diversified portfolio. This is meaningfully different from buying an ETF yourself.

iVentures Wealth, for instance, builds international mandates across US markets (NYSE, NASDAQ), European exchanges, and Asian markets in Hong Kong and Singapore. Their CFA-led team applies a structured research framework that classifies global opportunities across sectors like semiconductors, AI, genomics, and e-mobility.

The service goes beyond stock selection. Execution includes:

- Compliant LRS setup and wire coordination

- Currency-aware portfolio construction

- Schedule FA reporting and DTAA optimisation

- Consolidated reporting across domestic and global holdings

For a globally mobile UHNI with dollar-denominated expenses, this level of coordination — across compliance, currency, and tax — is difficult to replicate independently.

What You Need Before Investing in Foreign Stocks from India

Missing a compliance step early — a wrong account type, an undeclared foreign asset — can trigger penalties that dwarf your investment returns. Here's what to have in place before you wire a rupee abroad.

Regulatory and Account Requirements

For ETF/mutual fund routes:

- PAN card

- Demat and trading account with any SEBI-registered broker

For direct investing via overseas broker:

- PAN card

- LRS-enabled bank account (most banks support this)

- Overseas trading account (opened through Indian broker partnerships or directly with global brokers)

- Form A2 filled for each remittance above the bank's threshold

TCS on LRS remittances: Per the Income Tax Department's 2026 TCS document, TCS is levied at 20% on aggregate LRS remittances (for investment/other purposes) exceeding ₹10 lakh in a financial year. This TCS is creditable against your income tax liability but affects near-term cash outflow — plan accordingly.

KYC and Compliance Readiness

Both your Indian bank/broker and the overseas broker will require KYC documentation. Typically:

- PAN, Aadhaar, proof of address, bank statement, income proof (Indian side)

- Passport copy, proof of address, income proof (overseas broker)

- Form W-8BEN — required by US brokers to certify your non-US status for dividend withholding tax purposes

Tax Registration and Reporting Readiness

Any Indian resident holding foreign assets must declare them in:

- Schedule FA — Foreign Assets (in ITR)

- Schedule FSI — Foreign Source Income (in ITR)

Failure to disclose attracts penalties under the Black Money (Undisclosed Foreign Income and Assets) Act, 2015 — up to ₹10 lakh for non-disclosure, and penalties equivalent to three times the tax on undisclosed assets in serious cases. This is not an optional footnote; it's a legal obligation from the first year you hold a foreign asset.

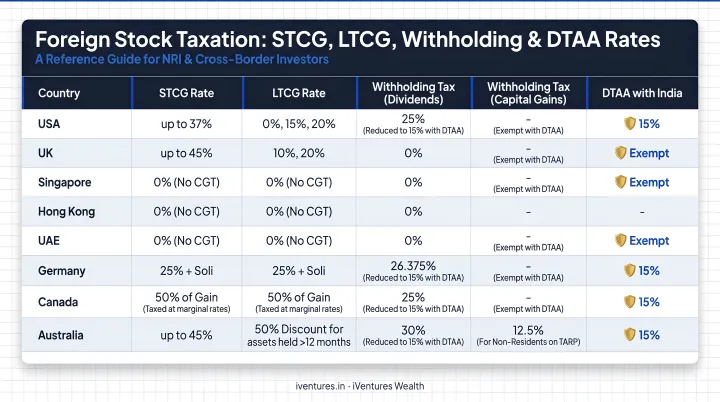

On the tax credit side: India's DTAA with the US reduces dividend withholding tax from the statutory rate to 25% (per Article 10 of the India-US DTAA). That withheld amount can be credited against your Indian tax liability — but only if you file Form 67 under Rule 128 before submitting your ITR. Missing this filing means forfeiting the credit entirely, so build it into your annual compliance calendar.

Key Factors That Affect Your Foreign Stock Investment Outcomes

Currency Risk (INR vs. USD)

Every rupee return on a foreign investment is determined by two things: how the stock performed, and how the INR moved against the USD during your holding period.

Mint reported that the rupee has fallen approximately 30% against the USD since 2014. For investors who held USD-denominated assets over that decade, this depreciation added to their INR returns — even in years where the underlying stock had modest gains.

The reverse is also true. If INR appreciates during your holding period, your converted-back returns will be lower than the stock's performance in USD suggests.

Currency exposure is only one layer. The tax treatment on these gains adds another dimension that catches many investors off guard.

Taxation: Foreign Withholding Tax, LTCG/STCG, and DTAA

Foreign stocks follow a different tax treatment from Indian listed equities. Key points:

| Tax Item | Treatment |

|---|---|

| STCG on foreign shares | Taxed at applicable income tax slab rate |

| LTCG holding period | More than 24 months (not 12 months as with Indian equity) |

| LTCG rate (post 23 Jul 2024) | 12.5% without indexation |

| US dividend withholding | 25% withheld at source under India-US DTAA |

| Foreign tax credit | Claimable via Form 67 under Rule 128 |

Note that the concessional domestic equity rates (20% STCG under Section 111A, 12.5% LTCG under Section 112A for Indian listed stocks) do not apply to foreign stocks.

Broker Selection and Transaction Costs

Transaction costs on international investing stack up quickly:

- Brokerage fees (per trade)

- Currency conversion charges — bid-ask spread on forex

- Annual account maintenance fees for the overseas account

- Wire transfer fees and GST on conversion

For reference, HSBC India charges 1% of gross amount (minimum ₹250) on currency conversion for smaller amounts, plus outward wire transfer charges. On a small investment, these costs can eat into returns before a single share is purchased. Compare fee structures carefully — and factor in Tax Collected at Source (TCS) when sizing your annual remittance.

When Does Investing in Foreign Stocks from India Make Sense?

Global investing adds real portfolio value under the right conditions — and adds friction without proportional benefit under the wrong ones.

It makes sense when:

- You want geographic diversification beyond India's market cycles

- You need exposure to sectors with limited Indian representation — semiconductor manufacturing, hyperscale cloud, frontier AI, global healthcare

- You want to hedge against INR depreciation over a long horizon

- You already have dollar-denominated expenses (education, travel, business)

- Your portfolio is large enough that compliance costs are proportionally small

For portfolios that meet these criteria, iVentures Wealth typically recommends a 10–30% global allocation, calibrated to each client's risk profile and existing India-heavy concentration.

It may not be efficient when:

- The investment amount is small: TCS, conversion costs, and compliance obligations become disproportionately large

- The investor lacks bandwidth to track foreign company fundamentals across time zones

- The investor's domestic ITR is not already structured to handle Schedule FA and FSI declarations

Common Mistakes Indian Investors Make When Investing Abroad

1. Ignoring TCS and the cumulative LRS limit

The USD 2,50,000 annual LRS limit is not investment-specific. It includes overseas travel, education fees, medical expenses, gifts, and family maintenance — all drawing from the same envelope. Investors who don't track cumulative LRS utilisation across all categories risk breaching the limit. Track your LRS usage from April and plan remittance timing accordingly.

2. Not declaring foreign assets in the ITR

Many first-time international investors simply don't know that Schedule FA and Schedule FSI exist. The Black Money Act makes non-disclosure a serious offence. If you held foreign assets in any financial year, those need to be declared — even if you made no gains.

3. Ignoring currency conversion costs and timing

Investors focus on stock price movement while overlooking the bid-ask spread on currency conversion. Buying USD when the INR is at a historically weak point inflates your cost basis. Conversely, timing remittances when INR is relatively stronger reduces entry costs. Neither should be the sole driver of investing decisions, but both deserve attention.

Investing in foreign stocks from India is legal, accessible, and useful for portfolio diversification. The route needs to be chosen deliberately, compliance handled rigorously, and the objective kept long-term.

For investors managing significant wealth, this intersection of global markets, Indian tax law, and cross-border compliance benefits from structured advisory. iVentures Wealth, a SEBI-registered investment adviser, works with HNIs and UHNIs on global allocation — covering LRS documentation, broker setup, Schedule FA coordination, and DTAA-optimised structuring — so the international portion of the portfolio serves its intended purpose.

Frequently Asked Questions

Can I invest in foreign stocks in India?

Yes. Indian residents can invest in foreign stocks through the RBI's LRS, which permits remittances up to USD 2,50,000 per financial year. Routes include overseas broker accounts (via LRS), international mutual funds, and ETFs listed on Indian exchanges, each with different tax and compliance implications.

Which foreign stocks are best to buy?

That depends entirely on your goals, risk tolerance, and investment horizon. Commonly considered names include large-cap US technology and consumer companies, but no specific stock is universally appropriate. A SEBI-registered investment adviser can match global stock selection to your specific goals and risk profile.

Which foreign companies are listed in India?

Very few. Standard Chartered Bank's IDR was the most notable example, but it was delisted in July 2020. Today, no active foreign company IDR trades on Indian exchanges. Investors can access global companies indirectly through international ETFs and mutual funds that are SEBI-regulated and listed in India.

What is the LRS limit for investing in foreign stocks from India?

The RBI's Liberalised Remittance Scheme permits Indian residents to remit up to USD 2,50,000 per financial year for permitted capital and current account transactions, including overseas investments. This limit is cumulative across all LRS uses — travel, education, and investments all count toward the same annual ceiling.

Do I need to pay tax on foreign stock investments in India?

Yes. Capital gains and dividend income from foreign stocks are taxable in India and must be declared in Schedule FA and Schedule FSI of your ITR. Foreign tax withheld on dividends may qualify for credit under applicable DTAA provisions. Consult a qualified tax adviser for your specific situation.

What is the minimum amount to start investing in foreign stocks from India?

There is no regulatory minimum under LRS. Some overseas brokers offer fractional investing from USD 1. However, TCS on remittances above ₹10 lakh, currency conversion charges, and compliance obligations make very small ticket sizes inefficient — a meaningful allocation is needed to justify the setup and ongoing reporting costs.