Introduction

Most Indian business owners pour everything into their company — time, capital, and energy. Personal retirement planning gets treated as something to handle later, once the business is bigger, more stable, or ready to sell.

That instinct is understandable. But it creates a serious vulnerability. Unlike salaried employees, business owners receive no employer-contributed EPF, no structured pension, no safety net built automatically over decades. According to PLFS data, self-employed workers make up over 56% of India's workforce — and the vast majority of them are building retirement wealth entirely on their own, whether they know it or not.

This guide walks through what makes retirement planning structurally harder for business owners, which India-specific instruments to prioritize, how to build personal wealth outside the business, and how to integrate your exit strategy into your retirement plan from the start.

Key Takeaways

- Business owners carry full responsibility for their own retirement corpus — no employer builds it for them.

- India's tax-efficient instruments — NPS, PPF, and ELSS — go well beyond EPF and can meaningfully reduce your retirement funding gap.

- Treating your business as your sole retirement plan is a risk most owners underestimate.

- A retirement strategy that holds combines early action, diversified assets, and a planned business exit — built together, not as an afterthought.

Why Retirement Planning is Uniquely Challenging for Business Owners

No Automatic Safety Net

EPFO covers establishments employing 20 or more persons. A self-employed proprietor, founder, or LLP partner outside that structure has no automatic EPF membership — meaning no employer contributions accumulate passively. Every rupee saved for retirement requires an active, deliberate decision.

That structural gap is just the starting point. Three recurring patterns tend to deepen it.

The Three Traps Business Owners Fall Into

1. Lifestyle dependency on business cash flows

Many founders never separate personal finances from business capital. Household expenses run off business cash flows directly — which works during good years but creates real instability when business cycles turn. The solution isn't complicated: ring-fence a personal corpus into income-oriented investments that generate predictable cash flow independent of business performance.

2. Valuation risk at exit

"My business is my retirement plan" is one of the most common — and dangerous — assumptions iVentures encounters. It sounds logical: build a valuable business, sell it at 60, live off the proceeds.

The problem is that valuations depend on market conditions, buyer availability, and timing — none of which you control. A business with no succession plan, unclear financials, or an unfavourable macro environment may fetch far less than expected, or find no buyer at all.

3. Over-concentration with no diversification

Most business owners hold the majority of their net worth in promoter equity and a few properties, with limited exposure to financial assets. One bad business cycle, one forced sale at the wrong time, and the entire retirement plan is compromised. Personal wealth built outside the business — systematically, year by year — provides the fallback that concentrated ownership cannot.

The Reinvestment Dilemma

Every rupee reinvested into the business to fuel growth is a rupee not compounding in a personal retirement account. There is no perfect answer to this tension. But the practical fix is treating a portion of post-tax business income as non-negotiable personal savings — deployed before the rest gets absorbed by business needs or lifestyle spending.

Setting Clear Retirement Goals

How Much Corpus Do You Need?

The starting point for any retirement plan is a target corpus. Indian financial planners generally use the Rule of 25 as a quick benchmark: accumulate 25 times your expected annual expenses at retirement. Mint's retirement coverage supports this figure, though some planners push it higher — 30x or even 33x — when accounting for a 30-year retirement horizon and India's inflation dynamics.

The arithmetic matters. If you expect to spend ₹15 lakh per year in retirement (in today's money), your target corpus is approximately ₹3.75–5 crore — before adjusting for inflation over your accumulation period. Build in India's long-run CPI target of 4% when projecting what that ₹15 lakh costs at retirement age — and at 4% compounded over 20 years, that ₹15 lakh annual need becomes roughly ₹33 lakh, nearly doubling your required corpus.

Deciding What Retirement Looks Like

For salaried professionals, retirement usually means a clean stop. For business owners, it rarely does. You need to decide whether you want:

- Full exit — sell or wind down, step away entirely

- Semi-active advisory role — stay connected, let others run operations

- Passive ownership — hold equity, receive dividends, no day-to-day involvement

Each scenario requires different financial preparation. A full exit demands a ready buyer and a structured sale. Passive ownership requires strong management beneath you. The earlier you define your version of retirement, the more time you have to build toward it.

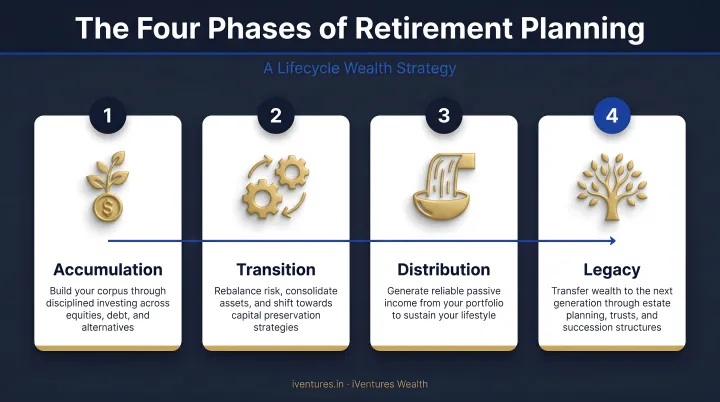

The Four Phases of Retirement Planning

| Phase | What It Means | Key Actions |

|---|---|---|

| Accumulation | Building the corpus while working | SIPs, NPS, PPF, ELSS, systematic surplus deployment |

| Transition | Stepping back from the business | Succession planning, glide path to lower-risk allocation |

| Distribution | Drawing income from the corpus | SWP, SCSS, bonds, passive income structures |

| Legacy | Transferring remaining wealth | Wills, trusts, estate structuring, family governance |

Best Retirement Savings Instruments for Indian Business Owners

No single instrument works for everyone. The right mix depends on your income pattern, tax bracket, and how far away retirement is.

National Pension Scheme (NPS)

NPS is one of the most tax-efficient retirement vehicles available to business owners in India. Key features:

- Section 80CCD(1): Self-employed individuals can claim up to 20% of gross income within the ₹1.5 lakh 80CCE ceiling.

- Section 80CCD(1B): An additional ₹50,000 deduction over and above the ₹1.5 lakh limit — especially valuable for high-income owners.

- Equity allocation: Active Choice allows up to 75% in equities for subscribers under 50, providing meaningful long-term growth potential.

- Tier I vs. Tier II: Tier I is the locked retirement account. Tier II allows flexible withdrawals without lock-in under the All Citizen model.

On exit at age 60, PFRDA's December 2025 amended rules now allow up to 80% as a lump sum with a minimum 20% annuity in specified cases — an improvement from the earlier 60/40 structure. Verify the latest PFRDA guidelines before finalising your NPS exit strategy.

Public Provident Fund (PPF)

PPF offers EEE (Exempt-Exempt-Exempt) tax treatment — contributions qualify under Section 80C, interest accrues tax-free, and maturity proceeds are exempt. It functions as the stable, government-backed debt anchor in a retirement portfolio.

- Annual contribution limit: ₹500 minimum to ₹1.5 lakh maximum

- Lock-in: 15 years, extendable in 5-year blocks

- Current interest rate: 7.1% (quarterly reset by Ministry of Finance — verify before publishing)

Given the ₹1.5 lakh cap, PPF alone won't build a retirement corpus. Its value lies in the guaranteed, tax-free return it provides as the fixed-income component within a broader allocation.

Equity Mutual Funds and SIPs

For long-term corpus growth that outpaces inflation, equity mutual funds are the most accessible route. SIPs suit business owners with irregular income — you can invest consistently in lower-revenue months and scale up during strong periods.

ELSS funds offer a dual advantage: equity market returns plus a Section 80C deduction of up to ₹1.5 lakh, with only a 3-year lock-in — the shortest among 80C instruments. The Nifty 50 Total Return Index delivered approximately 11.8% CAGR over 15 years in NSE's historical analysis, though past performance is not a guarantee.

For business owners, the discipline of investing matters as much as the instrument. iVentures Wealth structures equity investing around systematic surplus deployment — ensuring business cash flows move into high-conviction funds on a fixed schedule, rather than competing with discretionary spending or reactive decisions.

VPF and Superannuation

If you draw a formal salary from your own private limited company or LLP, you may be eligible to contribute to EPF and make additional Voluntary Provident Fund contributions — both tax-efficient. Eligibility depends on whether an employer-employee relationship exists within a covered establishment. A pure proprietor without employee status cannot participate.

Superannuation funds are another option for structured post-retirement benefits — particularly for business owners who want to extend similar benefits to key employees:

- Employer contributions to approved superannuation funds above ₹1.5 lakh are taxable as a perquisite under Income Tax rules

- Below this threshold, contributions remain a tax-deductible business expense and a retirement benefit simultaneously

Fixed Income and Debt Instruments

As you approach retirement, allocating more toward stable, income-generating debt instruments reduces portfolio volatility. Options for the distribution phase include:

- SCSS (Senior Citizens Savings Scheme): Available post-60, current rate 8.2%, maximum deposit ₹30 lakh — verify the quarterly rate reset before acting

- RBI Floating Rate Savings Bonds: 7-year tenure, currently paying approximately 8.05%, linked to NSC rate plus 35 basis points

- Debt mutual funds and corporate bonds: Provide liquidity and diversification within the fixed-income sleeve

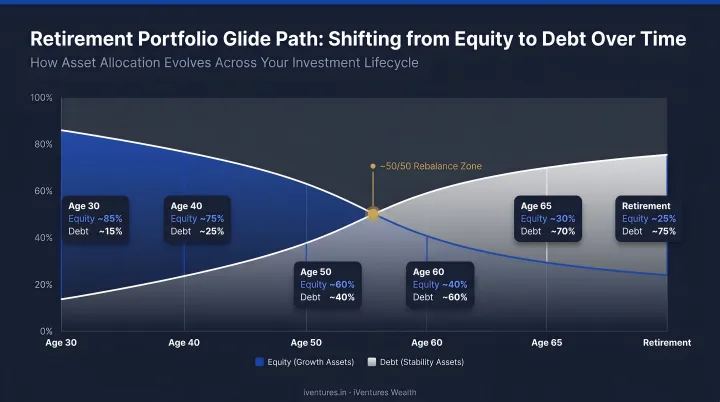

The NPS Auto Choice LC75 lifecycle fund starts at 75% equity and systematically shifts toward debt as you age. This glide path logic — heavier equity in your 40s, heavier debt by your late 50s — is the same principle that should guide your broader retirement asset allocation, regardless of which instruments you hold.

Investment Diversification: Building Wealth Beyond the Business

No retirement portfolio should be heavily concentrated in a single asset — and that includes your own business.

Balancing Business Reinvestment with Personal Wealth

The tension between reinvesting for growth and saving personally has no universal solution. But the structure matters more than the percentage.

iVentures Wealth designs a clear profit-allocation policy for business owner clients: working capital, business reserves, and the promoter's personal share are separated before discretionary spending enters the picture. Each profitable year builds a ring-fenced personal corpus — rather than waiting for surplus to appear after every other use is covered.

Real Estate as a Retirement Asset

Commercial and residential real estate makes up a significant portion of many Indian business owners' net worth. It provides an inflation hedge and rental income, and for many, it represents decades of accumulated wealth.

The caution: real estate is illiquid. You cannot sell 20% of a property when you need funds in retirement, and over-allocation creates concentration risk that mirrors the business risk you are already carrying.

iVentures Wealth evaluates a client's full real estate footprint — across cities and structures — and positions it as one component within the overall wealth plan, not the plan itself.

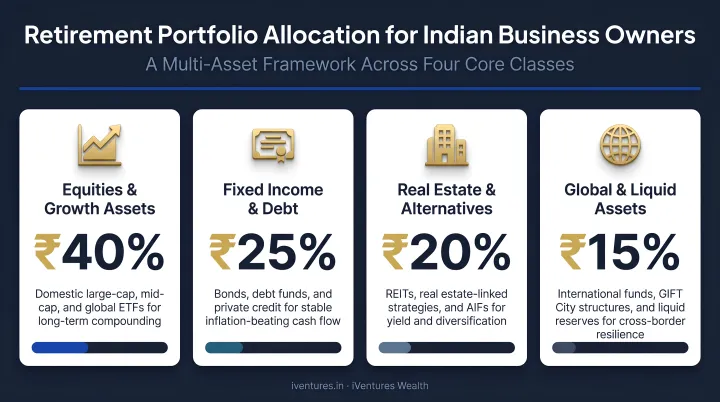

Building a Tax-Efficient Multi-Asset Portfolio

A well-structured retirement portfolio for an Indian business owner typically spans:

- Equity: Mutual funds (including ELSS), direct stocks, PMS

- Debt: PPF, NPS (debt allocation), bonds, SCSS, debt funds

- Gold: Sovereign Gold Bonds offer 2.5% annual interest plus capital appreciation; gains on redemption by individuals are tax-exempt at maturity

- Global assets: International funds and ETFs, providing currency diversification and exposure beyond India

For global allocation, iVentures recommends 10–30% of the total portfolio, depending on risk profile and diversification needs — though individual circumstances vary considerably.

Note: The RBI has not issued new SGB tranches in recent months. Check RBI/MoF notifications for current tranche availability before investing.

Your Business Exit Strategy is Part of Your Retirement Plan

A business with no succession plan, unclear financials, or undefined valuation will either fetch less than expected or find no buyer. The exit is not a separate event from retirement planning — it is a funding event for retirement.

Succession Planning and Business Valuation

According to KPMG India's 2024 research, family-owned businesses account for 80–85% of incorporated businesses in India. Yet Mint reports that only 15% of Indian family businesses have a formal succession plan. That gap between prevalence and preparedness is where retirement risk concentrates.

Key steps to begin years before your planned exit:

- Identify and groom a successor — family member, trusted employee, or external professional hire

- Commission a formal business valuation — understand what you actually have to sell

- Clean up financial records — commingled personal and business finances reduce buyer confidence and valuation

- Improve profitability metrics — EBITDA margins, revenue consistency, and management depth all affect price

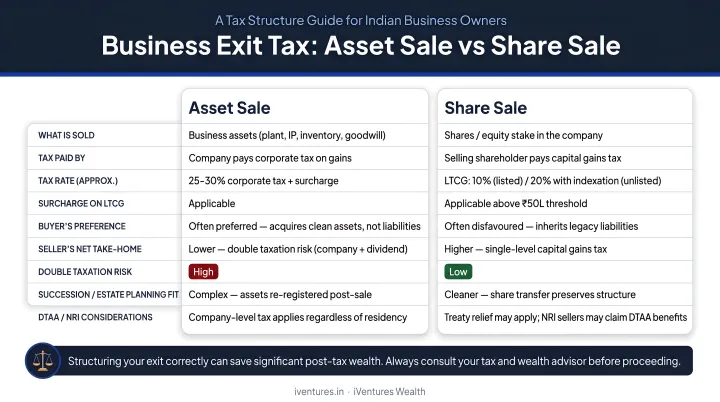

Structuring the Sale or Transfer for Tax Efficiency

Once the business is sale-ready, how the transaction is structured determines how much of the proceeds actually reach your retirement corpus. Key considerations under current Indian tax rules:

- Unlisted equity shares transferred on or after 23 July 2024 are treated as long-term after 24 months of holding; LTCG is taxed at 12.5% without indexation

- Asset sale vs. share sale carry different tax outcomes — slump sale rules under Section 50B apply to asset transfers; depreciable assets may be treated as short-term under Section 50 regardless of holding period

- Transaction timing: the difference between a share sale and an asset sale structure can be material net of tax

Getting this structure right requires a CA and a wealth advisor working in tandem — not sequentially.

iVentures Wealth coordinates directly with clients' CAs during exit transactions, converting a one-time liquidity event into a structured deployment plan. The framework typically separates proceeds into three buckets: safety capital (5–7 years of expenses in high-quality fixed income), stability capital for medium-term needs, and a long-term growth allocation.

Getting Professional Guidance for Retirement Planning

Retirement planning for a business owner spans investment management, tax planning, succession law, and estate planning simultaneously. Treating these as separate conversations — one with your CA, one with a distributor, one with a lawyer — means no one is looking at the full picture.

The advisory team you need includes:

- A SEBI-registered investment adviser for portfolio construction, goal mapping, and conflict-free product selection

- A Chartered Accountant for tax structuring, both personal and business

- A legal advisor specialising in business structures, succession, and estate documentation

iVentures Wealth operates as a SEBI-registered RIA (INA000019026): a fee-only, open-architecture firm that accepts no commissions from product manufacturers. For business owners, this matters. Traditional distributors earn trail income from what they recommend, which creates inherent conflicts when complex, multi-asset structuring is involved.

iVentures' fee-only model removes that conflict, enabling recommendations drawn from the full universe of regulated products — equity, debt, alternatives, global funds, AIFs — based on suitability, not product margins.

With over 20 years advising founders, promoters, CXOs, and UHNI families across India, iVentures' work with business owners typically covers:

- Separating personal and business finances from the outset

- Building a diversified corpus with systematic surplus deployment

- Connecting retirement planning to a structured business exit strategy

The minimum investable asset threshold for individual business owners is ₹10 crore.

Frequently Asked Questions

What is the best retirement plan for a small business owner?

There is no single best plan — most Indian business owners benefit from combining NPS (additional ₹50,000 deduction), PPF (EEE tax treatment), and equity mutual fund SIPs (inflation-beating growth). The right mix depends on income level, tax bracket, and retirement timeline.

What are the four pillars of retirement?

The four pillars are accumulation (building the corpus while working), transition (stepping back from the business), distribution (drawing sustainable income from the corpus), and legacy (transferring remaining wealth to the next generation or chosen causes).

When should a business owner start retirement planning?

As early as possible — ideally from the first year of stable business income. Compounding works most powerfully over long horizons, and starting early leaves room to course-correct if business performance falls short.

How much should an Indian business owner save for retirement?

A common benchmark in India is saving 20–30% of post-tax income, though the exact figure depends on retirement age, lifestyle goals, number of dependents, and expected exit value. For FIRE strategies, savings rates of 50–70% are typical.

Can a business owner rely solely on the sale of their business for retirement?

No. Business valuations depend on market conditions, buyer availability, and timing — all outside your control. Personal retirement savings built separately from the business provide a financial safety net that a potential sale cannot.

How does a business exit affect retirement planning in India?

The exit structure (asset sale vs. share sale), capital gains tax implications, and timing all affect net proceeds. Planning well in advance with a wealth advisor and CA helps ensure more of the sale price reaches your retirement corpus.