This guide is written for UHNIs, NRIs, family offices, and sophisticated investors who've already explored mutual funds and PMS strategies and are now asking: what's next? GIFT City AIFs are drawing serious attention from this audience — and for good reason. The ecosystem has grown to 194 Fund Management Entities and 310 schemes with USD 26.30 billion in commitments as of September 2025, according to the IFSCA's official fund management brochure.

This guide explains what GIFT City AIFs are, how the three categories work, how inbound and outbound structures differ, and what tax advantages are available.

Key Takeaways

- GIFT City AIFs are regulated by IFSCA (not SEBI) and operate in foreign currency — primarily USD — giving them offshore-equivalent status within Indian jurisdiction

- Three AIF categories apply: Category I (venture, infrastructure), Category II (private equity, debt), and Category III (hedge funds, derivatives) — each with distinct tax treatment

- Non-resident investors benefit from significant exemptions: no Indian capital gains tax on specified income, and often no PAN or ITR filing required

- Minimum investment is USD 150,000 per investor per scheme — this is an accredited-investor ecosystem, not a retail one

- Both inbound (foreign/NRI capital into India) and outbound (resident Indians investing globally via LRS) strategies are accessible through GIFT City structures

What Is an AIF in GIFT City?

A GIFT City AIF is a privately pooled investment vehicle registered with the International Financial Services Centres Authority (IFSCA) — India's unified financial regulator established on April 27, 2020 under the IFSCA Act, 2019. GIFT City itself, located in Gandhinagar, Gujarat, hosts India's first and only operational IFSC. These funds can be structured as a company, LLP, or trust — and their legal treatment differs sharply from domestic AIFs in ways that matter for cross-border investors.

How GIFT City AIFs Differ From Domestic AIFs

Under FEMA's IFSC Regulations, recognised IFSC financial institutions are treated as persons resident outside India — giving GIFT City AIFs offshore-equivalent legal status even though they operate within Indian borders.

Key distinctions from domestic SEBI-regulated AIFs:

- Currency: Operate in USD and other foreign currencies, not INR

- Overseas allocation: GIFT City funds can invest 100% of corpus in overseas assets; domestic SEBI AIFs are capped at 25% of investible funds at the scheme level, with an aggregate AIF/VCF overseas limit of USD 1.5 billion set by SEBI's May 2021 circular

- Diversification: No mandatory diversification limits apply

- FEMA compliance: Non-resident investors face reduced compliance friction compared to direct FDI or FPI routes

Compared to mutual funds, GIFT City AIFs serve a fundamentally different investor. Mutual funds carry a ₹500 minimum and offer daily liquidity. GIFT City AIFs start at USD 150,000, involve multi-year lock-ins, and pursue strategies (private equity, credit, hedge) that simply aren't accessible through retail products.

Types of AIFs in GIFT City: Category I, II, and III

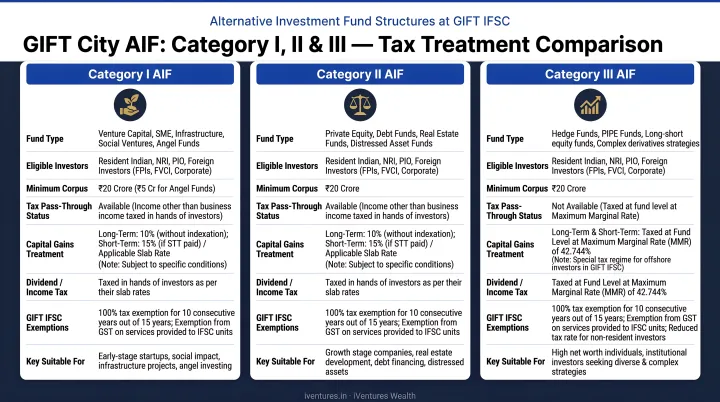

Category I: Venture Capital and Infrastructure

Category I AIFs invest in sectors considered socially or economically desirable: startups, early-stage ventures, SMEs, social enterprises, and infrastructure projects. These funds are close-ended by structure — suited to investors with a development-oriented outlook and time horizons of 7–10 years.

Tax treatment: Category I AIFs benefit from pass-through status under Section 115UB — income is taxed in investors' hands as if they invested directly, not at the fund level (except for business income, which is taxed at the fund).

Category II: Private Equity, Debt, and Real Estate

Category II is the residual category and the most widely used. It covers private equity, private credit, real estate funds, debt funds, and fund-of-funds structures — essentially everything that doesn't qualify as Category I or Category III.

Under IFSCA's Fund Management Regulations 2025, leverage and borrowing are permitted if disclosed. This is a meaningful departure from domestic SEBI Category II AIFs, which restrict leverage to short-term operational needs — and it enables considerably more sophisticated structuring for private credit strategies.

Tax treatment: Category II AIFs receive the same Section 115UB pass-through as Category I — income flows to investors and is taxed in their hands, not at the fund level.

Category III: Hedge Funds and Derivatives

Category III covers Restricted Schemes undertaking diverse or complex trading strategies — including listed and unlisted derivatives, long-short equity, arbitrage, and multi-strategy hedge approaches. Unlike Category I and II, leverage is explicitly permitted here.

Tax treatment: Category III does not receive the general Section 115UB pass-through. Instead, Category III funds qualifying as "specified funds" under Section 10(4D) — including IFSC-located funds regulated by IFSCA — can claim exemptions on specified income for non-resident unit holders. Taxation occurs at the fund level, subject to these exemptions.

Inbound vs. Outbound: The GIFT City Distinction

Beyond the three categories, GIFT City adds another structural dimension that domestic AIFs don't offer — the inbound/outbound split:

| Direction | Who Uses It | Capital Flow | Typical Assets |

|---|---|---|---|

| Inbound | NRIs, foreign nationals | Foreign/NRI capital → Indian assets | Indian equities, mutual funds, private equity |

| Outbound | Resident Indians (via LRS) | Indian capital → global assets | US stocks, global ETFs, foreign bonds |

The RBI's LRS limit of USD 250,000 per financial year per resident individual applies to outbound structures — but GIFT City AIFs provide one of the few regulated, IFSCA-supervised routes for accessing broad offshore equity exposure without the constraints that cap domestic fund overseas allocations.

AIF Category Comparison

| Parameter | Category I | Category II | Category III |

|---|---|---|---|

| Investment focus | Startups, SMEs, infrastructure | PE, credit, real estate, FoFs | Hedge, derivatives, long-short |

| Leverage | Limited | Permitted if disclosed | Permitted |

| Structure | Close-ended | Open or close-ended | Open or close-ended |

| Tax treatment | Pass-through (S.115UB) | Pass-through (S.115UB) | Fund-level, S.10(4D) exemptions |

| Investor profile | Long-horizon, development focus | Core alternative allocation | Sophisticated, risk-tolerant |

How GIFT City AIFs Work: What Investors Need to Understand

The Investment Flow

Investors commit a minimum of USD 150,000 into a scheme managed by an IFSCA-registered Fund Management Entity (FME). Three categories of FME registration exist: Authorised FME, Registered FME Non-Retail, and Registered FME Retail — each with distinct conditions under the IFSCA Fund Management Regulations 2025. The FME deploys capital into a defined strategy and distributes returns in foreign currency, with a minimum corpus of USD 3 million per scheme.

NRI and foreign investors (inbound):

- Capital enters through IFSC Banking Units in USD

- Deployed into Indian assets — equities, mutual funds, private equity

- Exits without the FEMA compliance friction typical of direct FDI or FPI routes

Resident Indians (outbound):

- Capital remitted under LRS flows into a GIFT City AIF

- Deployed into offshore securities — US stocks, global ETFs, foreign bonds

- Bypasses the 25% overseas allocation cap that constrains domestic mutual funds

Governance and Investor Protections

GIFT City AIFs are not unregulated offshore vehicles. IFSCA mandates:

- Independent trustees, custodians, and auditors

- AML/KYC compliance aligned with FATF standards, governed by IFSCA's AML, CFT and KYC Guidelines 2022 (updated February 2026)

- Mandatory FME registration before operations begin

The entire framework operates within Indian jurisdiction, with IFSCA as the unified regulator overseeing banking, insurance, and fund management in the IFSC.

Where Advisory Guidance Matters

That regulatory depth — across FME categories, IFSCA compliance requirements, and cross-border tax positioning — is precisely where independent advisory adds weight.

For UHNIs and family offices evaluating inbound or outbound strategies, fund selection and FME due diligence require more than product familiarity. iVentures Wealth, a SEBI-registered Investment Adviser, advises clients on GIFT City-domiciled funds across all three AIF categories, with particular focus on USD-denominated allocations for NRI and OCI clients and global diversification strategies for resident UHNIs. As a fee-only RIA, the firm's recommendations are grounded in suitability rather than product economics.

Tax Advantages of GIFT City AIFs for Investors

GIFT City's tax framework offers concrete, quantifiable advantages — from zero transaction taxes to a 10-year income deduction for fund managers. Here's how it works across key dimensions.

Pass-Through Taxation: Category I and II

Under Section 115UB of the Income Tax Act, Category I and II AIF income is taxed in the hands of investors as if they invested directly — eliminating double taxation at the fund level. Key pass-through conditions include:

- Non-business losses pass through to investors after a minimum 12-month holding period

- Business losses remain at the fund level (no pass-through)

- For non-resident investors, income from offshore investments through Category I and II AIFs is generally not taxable in India — a meaningful benefit for NRIs deploying capital through inbound structures

Category III: Specified Fund Exemptions

Section 10(4D) exempts specified income of a "specified fund" — including Category III AIFs located in the IFSC and regulated by IFSCA — subject to conditions including non-resident unit ownership and investment in specified eligible instruments. This covers transfers of specified securities, derivatives, and offshore securities for eligible non-resident investors.

PAN and ITR Relief for Non-Residents

Non-resident investors meeting applicable conditions are not required to obtain a PAN card for income from Category I and II AIFs in IFSC — and may be exempt from filing Indian income tax returns. For NRI investors managing multiple jurisdictions, this eliminates a meaningful operational burden.

10-Year Tax Holiday for Fund Managers

Under Section 80LA, eligible IFSC units — including FMEs — receive a 100% deduction on business income for 10 consecutive assessment years out of 15. Fund management services provided to IFSC-based funds are also GST-exempt — saving 18 percentage points on management fees compared to onshore structures.

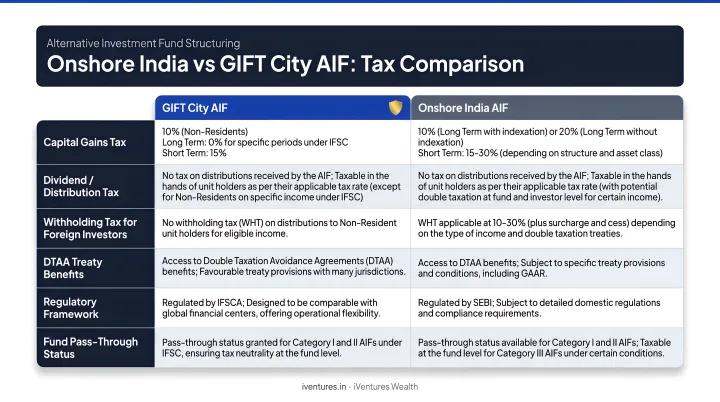

Onshore India vs. GIFT City AIF: Tax Comparison

| Tax Element | Onshore India | GIFT City AIF |

|---|---|---|

| Securities Transaction Tax (STT) | 0.1% on equity delivery | 0% |

| Commodity Transaction Tax (CTT) | Applicable | 0% |

| GST on fund management fees | 18% | 0% (GST-exempt) |

| Stamp duty on securities | Applicable | 0% on specified securities |

| FME income tax | Standard corporate rate | 100% deduction for 10 of 15 years (S.80LA) |

| PAN/ITR for NRI investors | Generally required | Conditional exemption for eligible NRIs |

Note: Capital gains rates under Sections 111A and 112A for domestic investors should be verified against current provisions. GIFT City exemptions for non-residents are subject to specified-fund and offshore-income conditions.

Who Should Consider GIFT City AIFs — and Who Should Not

Investors Well-Suited for GIFT City AIFs

NRIs and foreign nationals are the primary beneficiaries. GIFT City offers the most investor-friendly structure for non-residents who want regulated Indian and global exposure without FEMA compliance burden, PAN requirements, or ITR filing obligations. IFSCA data shows that 57% of current GIFT City fund investors are NRIs or OCIs.

UHNIs and family offices seeking global diversification can access US equities, global ETFs, and international private equity through outbound GIFT City AIF structures, without routing capital through Singapore or Mauritius. This matters most when building multi-geography portfolios with USD-denominated benchmarking — a priority for family offices consolidating global wealth under a single regulated framework.

Resident Indians with LRS capacity who want structured, regulated outbound exposure beyond what domestic funds can legally provide will find GIFT City AIFs one of the few compliant routes to broad international equity allocation.

When GIFT City AIFs May Not Be the Right Fit

- Ticket size below USD 150,000: The minimum investment makes this unsuitable for smaller portfolios. Domestic AIFs (₹1 crore minimum) or PMS strategies may be more appropriate starting points.

- Short-term liquidity needs: Category I and II AIFs are close-ended with multi-year lock-ins. Committing capital here without a matching time horizon is a structural mismatch.

- Limited familiarity with alternative risk: GIFT City AIFs carry market, credit, currency, and liquidity risks that differ materially from mutual funds. Without experienced guidance, the complexity can outweigh the tax advantages.

Frequently Asked Questions

Which AIFs are available in GIFT City?

As of September 2025, the IFSCA reports 310 schemes across 194 Fund Management Entities with USD 26.30 billion in total commitments and 4,733 investors. Schemes span venture capital, infrastructure, private equity, debt, hedge funds, and derivatives — across both inbound and outbound structures.

What are Category I, Category II, and Category III AIFs?

Category I covers startups and infrastructure; Category II covers private equity, debt, and real estate — both receive Section 115UB pass-through tax treatment. Category III targets hedge funds and derivatives, with fund-level taxation and Section 10(4D) exemptions available to non-resident investors.

What is the IFSC in GIFT City?

GIFT City IFSC is India's only operational International Financial Services Centre, located in Gandhinagar, Gujarat. It operates as a special economic zone where transactions occur in foreign currency, IFSC entities are treated as non-residents under FEMA, and IFSCA (established 2020) serves as the unified regulator for banking, insurance, and fund management.

Can NRIs and foreign investors invest in GIFT City AIFs?

Yes. NRIs, OCIs, and foreign nationals make up 57% of the current investor base per IFSCA data. They invest through IFSC Banking Units in USD, with reduced FEMA compliance friction and key exemptions — including no Indian capital gains tax on specified income.

What is the minimum investment for a GIFT City AIF?

The minimum is USD 150,000 per investor per scheme, with a lower threshold of USD 40,000 for employees or directors of the FME. Each scheme must meet a minimum corpus of USD 3 million.

How are GIFT City AIFs taxed differently from domestic AIFs?

Domestic AIFs carry STT at 0.1%, 18% GST on management fees, and standard capital gains rates. GIFT City AIFs eliminate all three — and add further benefits:

- Pass-through treatment for Category I and II (with NRI offshore-income exemptions)

- Section 10(4D) exemptions for Category III non-resident investors

- Zero stamp duty on specified securities

- 10-year business income tax holiday for the FME under Section 80LA