The answer is more nuanced than most people expect. RSUs and ESOPs have different tax trigger points, different taxable amounts, and different planning opportunities. Confusing the two — or simply not planning — can cost lakhs in avoidable liability.

This article breaks down exactly how each instrument is taxed in FY 2025-26, where the real differences lie, and how to structure your decisions for maximum net-of-tax wealth.

Key Takeaways

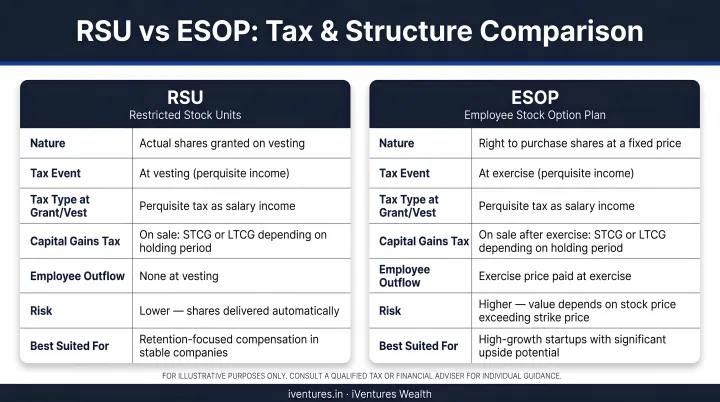

- ESOPs grant the right to buy shares at a fixed price; RSUs deliver shares automatically at vesting — no purchase required

- RSUs trigger tax at vesting on the full FMV; ESOPs trigger tax at exercise on the spread (FMV minus exercise price)

- Both instruments face capital gains tax at sale — holding period from exercise/vesting determines STCG vs LTCG rates

- Eligible startups under Section 80-IAC can defer ESOP TDS for up to 48 months; RSUs carry no equivalent deferral

- Which instrument suits you depends on company stage, liquidity, and your personal tax position — the answer varies by situation

RSU vs ESOP: Quick Comparison

Before diving into the mechanics, here's the side-by-side picture:

| Dimension | ESOP | RSU |

|---|---|---|

| Nature | Right to purchase shares | Promise to deliver shares |

| Employee cost | Must pay exercise price | Zero cash outflow |

| Tax trigger | At exercise | At vesting/settlement |

| Taxable amount | FMV minus exercise price | Full FMV |

| TDS deferral | Available (eligible startups) | No general deferral |

| Typical users | Early-stage startups, VC-backed firms | MNCs, listed companies, senior hires |

Capital gains treatment at sale is identical for both instruments. Where RSUs and ESOPs diverge is at the access event — exercise for ESOPs, vesting or settlement for RSUs — not at the point of sale.

What Is an ESOP?

An Employee Stock Option Plan gives you the contractual right to purchase company shares at a pre-determined exercise price (strike price) after a vesting period. Critically, no ownership is created until you actively exercise the option by paying the exercise price. That voluntary element gives you timing control — which is where most of the tax planning opportunity lies.

The ESOP Lifecycle

| Stage | Tax Event | Cash Flow |

|---|---|---|

| Grant | None | None |

| Vesting | None | None |

| Exercise | Perquisite income taxed | Pay exercise price + TDS |

| Sale | Capital gains taxed | Receive sale proceeds |

Taxation at Exercise

Under Section 17(2)(vi) of the Income Tax Act, the perquisite value at exercise is:

(FMV on exercise date − Exercise price) × Number of shares

This amount is added to your salary income and taxed at your marginal slab rate. For FY 2025-26, under the new regime, the top rate is 30% for income above ₹24 lakh, with 4% cess on top. Your employer deducts TDS under Section 192.

To illustrate: if FMV is ₹6,500 and the exercise price is ₹500 on 100 shares, the Income Tax Department's own ESOP guidance confirms the perquisite is ₹6,00,000 — added entirely to salary income that year.

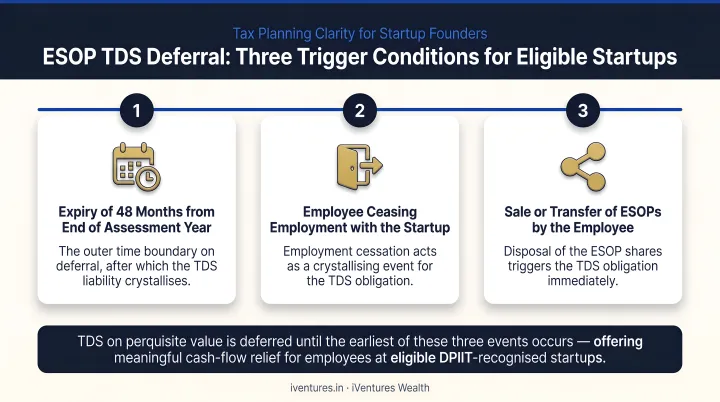

The DPIIT Startup TDS Deferral

This is where ESOPs have a significant advantage for startup employees. Under Section 192(1C), employees of eligible startups (as defined under Section 80-IAC) can defer TDS payment until the earliest of:

- 48 months from the end of the assessment year in which shares are allotted

- Date of sale of the securities

- Date the employee leaves the company

This eliminates the painful situation of paying large tax bills on shares you cannot yet sell — a common problem in pre-IPO companies. Worth checking carefully: not every DPIIT-recognised startup automatically qualifies. The company must meet Section 80-IAC eligibility specifically, so confirm this with your employer before factoring the deferral into your planning.

Capital Gains at Sale

Under Section 49(2AA), your cost of acquisition for capital gains purposes is the FMV on the exercise date — the same value used for the perquisite calculation. Any appreciation above that FMV is taxed as capital gains.

For listed shares, the holding period threshold is 12 months. Gains above ₹1.25 lakh are taxed at 12.5% LTCG (Section 112A); short-term gains are taxed at 20% STCG (Section 111A). For unlisted shares, the LTCG threshold is 24 months, also at 12.5% post-Budget 2024.

When ESOPs Make Sense

ESOPs work best when:

- Exercise price is low (seed/early-stage grant)

- You have a 4–7 year horizon to a liquidity event

- You can time the exercise to manage perquisite income across tax years

- Your company qualifies for Section 80-IAC TDS deferral

The wealth creation potential is real. Freshworks' Nasdaq listing made more than 500 employees crorepatis, with 76% of employees owning shares. Nykaa's top six employees were set to make over ₹850 crore through vested options at IPO.

Both outcomes share a common thread: low early-stage exercise prices created a large spread, and employees who planned their exercises carefully captured most of it.

What Is an RSU?

A Restricted Stock Unit is a company's promise to deliver actual shares once defined vesting conditions are met. There's no purchase price. No cash outflow from the employee. Ownership is created automatically at each vesting date.

The RSU Lifecycle

| Stage | Tax Event | Cash Flow |

|---|---|---|

| Grant | None | None |

| Vesting/Settlement | Full FMV taxed as salary | Employer deducts TDS |

| Sale | Capital gains on appreciation above vesting FMV | Receive sale proceeds |

The critical distinction from ESOPs: you have no discretion over when Stage 1 tax hits. It happens automatically at each vesting date, regardless of whether you want to hold or sell.

Taxation at Vesting

Since there's no exercise price to offset, the perquisite value equals the full FMV of shares on the vesting date. Under the same Section 17(2)(vi) and Rule 3 framework, this is taxed as salary income immediately, with employer TDS deducted under Section 192.

This is why RSUs typically carry a larger upfront TDS burden than comparable ESOPs — there's nothing to subtract from FMV when calculating the taxable amount.

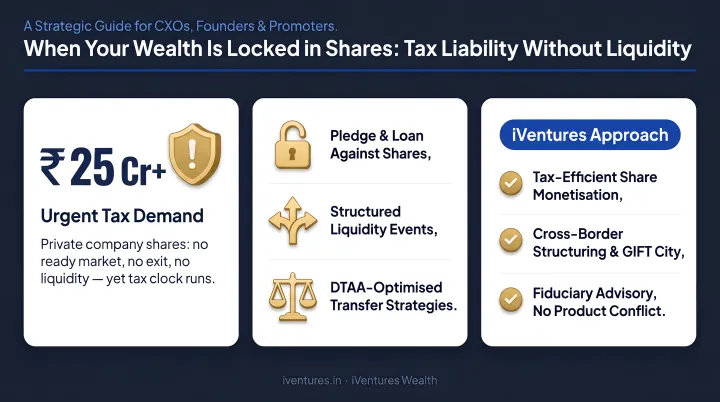

The Private Company Cash Flow Problem

For employees holding RSUs in private (unlisted) companies, there is no TDS deferral mechanism equivalent to the ESOP/Section 80-IAC provision. The tax bill falls due at vesting even if shares cannot be sold on any market, and employees must fund TDS from salary or personal savings.

This is the central planning risk for anyone in a private company RSU plan: the tax liability is real and immediate even when the wealth is entirely illiquid.

Cross-Border RSUs: Additional Complexity for NRI and CXO Clients

The cash flow problem above is compounded for Indian employees receiving RSUs from a foreign-listed parent — common in US-based tech multinationals — where two tax jurisdictions now apply simultaneously:

- The foreign jurisdiction may deduct withholding tax at vesting

- The same income is also taxable in India as salary perquisite

- To avoid double taxation, employees must file Form 67 to claim a Foreign Tax Credit (FTC) under the applicable DTAA — this is governed by Rule 128 and must be filed before the relevant assessment year end

- All foreign RSU holdings and foreign brokerage accounts must be disclosed in Schedule FA in the annual ITR

Non-disclosure carries serious consequences. Under the Black Money (Undisclosed Foreign Income and Assets) Act, Section 42 and Section 43 penalties for failure to furnish or inaccurately disclose foreign assets are ₹10 lakh each, unless the aggregate value of non-immovable property assets does not exceed ₹20 lakh.

Filing Form 67 is the only compliant route to offset overseas withholding against Indian tax liability. It is a legal obligation, not a discretionary planning step.

When RSUs Make Sense

RSUs are the right instrument when:

- Liquidity is readily available (listed company shares)

- Guaranteed value matters more than asymmetric upside

- Simplicity of grant administration is a priority

- The employee is senior enough that a guaranteed compensation component is appropriate

Infosys granted 3,744,345 equity-settled RSUs under its 2019 Plan in FY 2025, with CEO grants structured across performance-based, ESG, TSR, and time-based RSUs. HCLTech operates its RSU Plan 2021 and 2024 under SEBI's Share Based Employee Benefits and Sweat Equity Regulations 2021. At this seniority level, RSUs serve as guaranteed long-term compensation — structured wealth, not speculative upside.

RSU vs ESOP Taxation: Which Works Better for You?

Head-to-Head Tax Comparison

Assume: 1,000 shares, FMV at access event ₹1,000/share, exercise price (ESOP only) ₹200/share, sale price ₹1,200/share, 30% marginal slab.

| Item | ESOP | RSU |

|---|---|---|

| Exercise/vesting perquisite | ₹8,00,000 (₹800 × 1,000) | ₹10,00,000 (₹1,000 × 1,000) |

| Tax on perquisite @ 30% + cess | ~₹2,49,600 | ~₹3,12,000 |

| Capital gains (₹200 gain × 1,000) | ₹2,00,000 | ₹2,00,000 |

| LTCG tax @ 12.5% | ₹25,000 | ₹25,000 |

| Cash outflow: exercise price | ₹2,00,000 | Nil |

| Total cash outflow (tax + exercise) | ~₹4,74,600 | ~₹3,37,000 |

The ESOP has a lower perquisite tax — because the exercise price reduces the taxable spread. But the cash outflow is higher once you factor in the exercise price payment. The RSU has a higher tax bill but zero exercise cost. Which produces better net wealth depends on the actual exercise price, share price trajectory, and whether you can hold long enough for LTCG treatment.

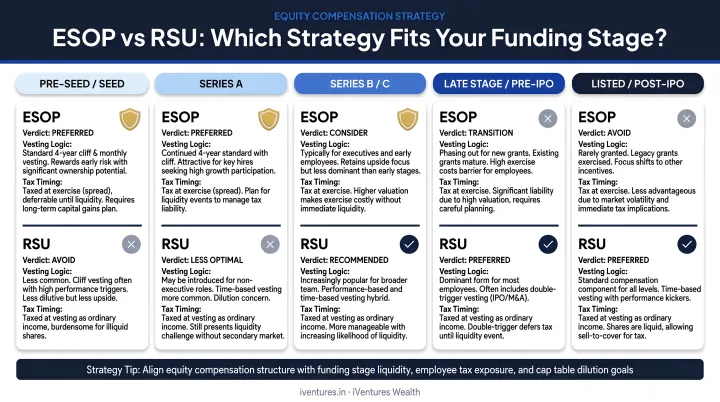

Strategy by Company Stage

- Seed to Series B: ESOPs with low exercise prices. Maximum upside, tax-efficient if deferral available, planning horizon of 5-7 years

- Growth/Series C-D: Hybrid approach — ESOPs for broad team grants, RSUs for senior hire retention where guaranteed value matters

- Pre-IPO/post-IPO: RSUs or Performance RSUs become the standard. Liquidity is near-term, certainty of value is prioritised, and the ESOP TDS deferral benefit has less relevance

Holding Period as a Tax Lever

This applies to both instruments and can materially change your net return:

- Listed shares: Holding 12+ months from exercise/vesting date converts STCG (20%) to LTCG (12.5%)

- Unlisted shares: 24-month threshold for the same conversion

- On a ₹50 lakh capital gain, the difference between STCG and LTCG rates is approximately ₹3.75 lakh in tax saved

At crore-scale equity positions, the timing of this decision — planned well before a liquidity event, not after — is often where the largest tax differences are made.

On Double Taxation

For domestic RSUs, the employer's TDS at vesting covers the salary tax component. There is no double taxation risk if the ITR is filed correctly — you are not paying income tax again on the same amount.

For foreign RSUs, the DTAA-based FTC mechanism through Form 67 is the legal route to offset overseas withholding against Indian tax. This is not a planning strategy to be explored or a grey area — it is a compliance requirement that must be executed before the assessment year end.

For CXOs, founders, and UHNIs, the combined tax exposure across exercise timing, capital gains sequencing, and foreign withholding can run into crores. Getting each component right requires coordinating across tax years, not just optimizing individual events in isolation.

iVentures Wealth's CXO & Professional advisory practice works with clients on precisely this: structuring exercise timing, sequencing capital gains across years, and integrating equity income into the broader portfolio — in coordination with the client's CA and tax counsel where needed.

Conclusion

ESOPs and RSUs serve different purposes at different stages of a company's life and an employee's career. The right instrument is the one that aligns with your liquidity timeline, tax capacity, and wealth goals at this specific moment.

Planning quality is what separates good outcomes from poor ones. The same RSU or ESOP can produce dramatically different net wealth depending on when you exercise and how long you hold. Whether you claim eligible credits and how equity income integrates into your broader financial picture matters just as much as the instrument itself.

That kind of integrated planning requires more than tax knowledge alone. For CEOs, CXOs, startup founders, and UHNIs navigating these decisions, iVentures Wealth offers equity compensation advisory covering vesting-schedule planning, exercise-timing analysis, post-liquidity diversification, and cross-border FTC coordination. The advisory is fee-only, with no product commissions, and structured for clients with ₹10 crore and above in investable assets. To discuss your situation, write to info@iventures.in.

Frequently Asked Questions

Are ESOPs better than RSUs?

Neither is universally better. ESOPs suit early-stage startup employees — higher upside, lower perquisite tax on the spread. RSUs work better in listed companies or for senior hires who value guaranteed value and simplicity. The right choice turns on company stage, liquidity, and your personal tax position.

Are RSUs taxed differently?

Yes. RSUs are taxed at vesting on the full FMV as salary income, with no exercise price to offset the taxable amount. ESOPs are taxed at exercise only on the spread (FMV minus exercise price), which is typically a smaller taxable amount. Both are then subject to capital gains tax at the point of sale.

Is ESOP taxable in income tax?

Yes — at two stages. First at exercise, where the spread between FMV and exercise price is treated as salary income subject to employer TDS under Section 192. Second at sale, where any further appreciation above the exercise-date FMV is taxed as capital gains under the Income Tax Act.

How do you avoid RSU double taxation?

For domestic RSUs, employer TDS at vesting covers the salary tax — no double taxation if the ITR is filed correctly. For foreign RSUs from a US-listed parent, file Form 67 before the assessment year end to claim a Foreign Tax Credit under the applicable DTAA and offset overseas withholding against your Indian tax liability.

What is the holding period for LTCG on RSUs and ESOPs in India?

For listed shares, 12 months from exercise (ESOPs) or vesting (RSUs); for unlisted shares, 24 months. Long-term gains above the ₹1.25 lakh annual exemption are taxed at 12.5% under the post-Budget 2024 regime, effective 23 July 2024.

Can NRIs receive ESOPs or RSUs from Indian companies?

Yes, subject to FEMA and Non-debt Instruments Rules compliance. Income from exercise or vesting may be taxable in both India and the country of residence — DTAA planning, Schedule FA disclosure, and cross-border tax structuring are essential steps for NRI employees to avoid excess liability.