This gap is what HNI financial planning actually addresses. According to Knight Frank's Wealth Report 2025, India had 85,698 HNWIs in 2024 — up 6% year-on-year — with projections pointing to nearly 94,000 by 2028. That's a fast-growing population with increasingly complex financial needs and, too often, advice that hasn't kept pace.

This guide covers the core pillars of HNI financial planning in India — asset allocation, tax efficiency, estate structuring, and international diversification — plus a framework for evaluating whether your current advisor is genuinely equipped to handle the complexity your wealth demands.

Key Takeaways

- HNI planning requires integrating tax, investment, estate, and risk management simultaneously — not as separate exercises

- SEBI-regulated access thresholds include ₹50 lakh for PMS and ₹1 crore for AIFs

- Capital gains tax changed post-Budget 2024: listed equity LTCG is now 12.5% with a ₹1.25 lakh annual exemption; STCG is 20%

- Estate planning without a registered will and updated nominees leaves wealth vulnerable to probate delays

- A SEBI-registered RIA with fiduciary duty is structurally different from a commission-earning distributor — the distinction matters more than most HNIs realise

What Sets High Net Worth Financial Planning Apart?

Standard financial planning — save consistently, buy term insurance, invest in diversified mutual funds — is sound advice for most people. For HNIs, it's the starting point, not the finish line.

The Layers That Compound With Wealth

As net worth grows, so does complexity. A typical HNI portfolio involves:

- Multiple income streams: salary, dividends, rental income, business profits, ESOPs

- Concentrated positions in a single stock, sector, or property

- Cross-entity ownership across personal, HUF, company, and trust structures

- Multi-generational goals that require estate and succession planning today

The cost of getting any one of these wrong scales proportionally. A poorly timed asset sale can trigger lakhs in avoidable tax. A missing nominee on a demat account can tie up crores in probate for years.

Challenges Specific to Indian HNIs

Portfolio complexity is only part of the picture. Indian HNIs also navigate a distinct regulatory environment:

- SEBI product thresholds: PMS requires a minimum ₹50 lakh investment; AIFs require ₹1 crore — these aren't available to mass-market investors and come with their own due diligence requirements

- Advisor conflicts: Most relationship managers at banks and brokerages earn commissions from products they recommend — a structural misalignment that generic financial advice rarely acknowledges

- Cross-border complexity: NRIs and OCIs face FEMA regulations, dual-will requirements, and LRS compliance that standard advisors aren't equipped to handle

- Succession law variation: India's succession framework differs by religion — the Hindu Succession Act (amended 2005, giving daughters equal coparcenary rights) applies differently than the Indian Succession Act for others

Who This Guide Is For

SEBI doesn't publish a single universal "HNI" definition. In practice, regulated access thresholds are the clearest markers: ₹50 lakh for PMS, ₹1 crore for AIFs. Wealth management firms, including iVentures Wealth, typically define HNI clients as those with ₹5 crore or more in investible assets, while UHNI clients hold ₹50 crore or more.

This guide is most applicable to investors in the ₹1 crore+ investable asset range seeking to build a coordinated, goal-driven financial strategy.

Key Pillars of a High Net Worth Financial Plan

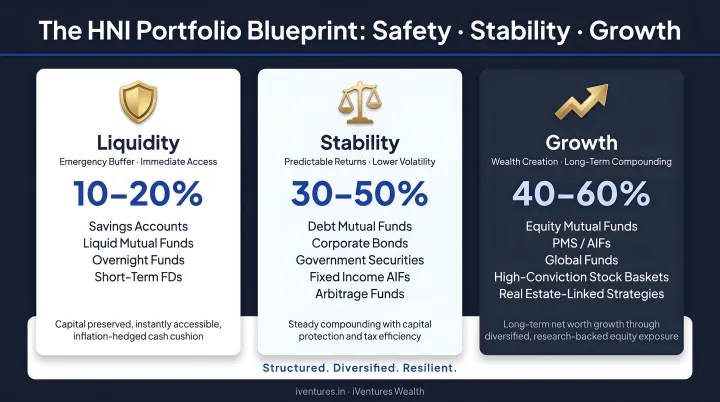

Liquidity and Cash Flow Management

Even a large portfolio can create problems if liquidity isn't structured deliberately. Forced asset sales — whether during a market downturn or in a high-tax period — are expensive mistakes that proper planning prevents entirely.

A practical approach uses a three-bucket structure:

- Safety bucket: 5–7 years of lifestyle expenses and anticipated large expenditures in high-quality liquid instruments (liquid funds, short-duration debt)

- Stability bucket: A balanced, asset-allocated portfolio with an 8–15 year horizon

- Growth bucket: Long-lock, higher-return allocations — AIFs, PMS, private equity

For corporate clients and business owners, a cash ladder and maturity tracking system ensures capital is available for expansion, distributions, or capital calls without disrupting long-term investments.

Diversified Asset Allocation

HNI portfolios should extend well beyond mutual funds and fixed deposits. An appropriate allocation considers:

- Equities: Direct stocks, high-conviction baskets, equity mutual funds, ETFs

- Debt: Bonds, NCDs, debt funds (with updated tax treatment post-April 2023)

- Alternatives: PMS, AIFs across all three SEBI categories, private equity

- Real estate: Direct property, REITs, InvITs for regulated liquid exposure

- International assets: Global equities and ETFs via LRS

- Gold: Sovereign Gold Bonds, gold ETFs

The right mix isn't fixed — it evolves with risk profile, time horizon, liquidity needs, and tax situation. A FIRE-oriented accumulator in their 40s needs a very different allocation than a business owner who has just exited a promoter stake and received ₹100 crore in liquidity.

Tax-Efficient Planning

For HNIs, tax planning runs year-round — embedded in every investment decision, not relegated to a March-end scramble.

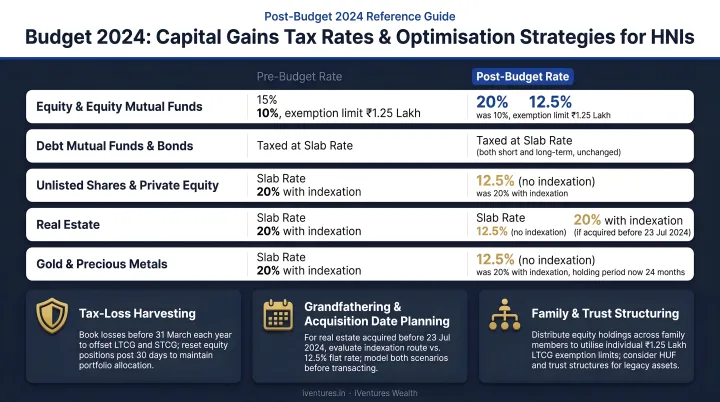

Key concepts post-Budget 2024:

- Listed equity LTCG: 12.5% with a ₹1.25 lakh annual exemption, replacing the earlier 10% rate

- Listed equity STCG: Now 20% under Section 111A

- Debt mutual funds: Gains on funds acquired on or after April 1, 2023 are treated as short-term under Section 50AA — removing the earlier indexation-based LTCG treatment entirely

- Surcharge: Applies progressively for high-income taxpayers; the effective rate varies by income level, regime, and asset class — not a single flat number

Practical strategies include booking LTCG up to the ₹1.25 lakh exemption threshold each year, timing realisation across financial years to manage taxable income, and avoiding unnecessary short-term churn.

Risk Management and Asset Protection

Risks that are manageable at smaller wealth levels become genuinely threatening at the HNI tier:

- Concentration risk: A large portion of net worth in one stock, sector, or property

- Litigation and liability exposure: Particularly relevant for business owners and directors

- Insurance gaps: Many HNIs are underinsured relative to their net worth because they underestimate liability exposure — Directors & Officers (D&O) insurance is often absent entirely

Asset protection tools in India include private discretionary trusts, LLP structures, and adequate life, health, and liability coverage.

For founders carrying a large promoter stake, a structured multi-year diversification plan — executed in tranches — reduces concentration exposure without triggering unnecessary tax events in a single year.

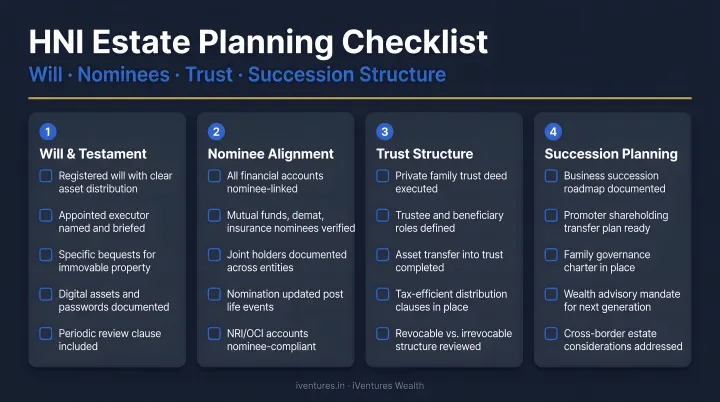

Estate Planning and Succession

For HNIs, estate planning begins with a registered, updated will — and extends significantly beyond it.

Without proper structuring:

- Wealth can get tied up in probate proceedings for years

- Missing nominee designations on demat accounts or insurance policies create immediate family vulnerability

- Cross-border assets create jurisdictional conflicts that a single Indian will cannot resolve

The 2005 amendment to the Hindu Succession Act gave daughters equal coparcenary rights by birth — a material factor for joint family succession planning. Any estate structure that doesn't address this explicitly leaves the door open to disputes that courts, not families, end up resolving.

Investment Strategies and Asset Classes for HNIs in India

Portfolio Management Services (PMS)

PMS is available to individuals investing a minimum of ₹50 lakh. Unlike mutual funds, PMS holds securities directly in the investor's name — offering personalised portfolio construction and higher transparency, but also greater concentration and no SEBI-mandated diversification floors equivalent to mutual fund regulations.

When evaluating a PMS provider, look beyond absolute returns. Key due diligence criteria include:

- Risk-adjusted returns: Sharpe and Sortino ratios, not just point-to-point performance

- Fee structure: Management fees, performance fees, hurdle rate design, and exit loads — always evaluate against net-of-fee returns, not gross performance numbers

- Investment philosophy consistency: How has the manager behaved across market cycles?

- Concentration and sector exposure: How much single-stock risk does the portfolio carry?

Fee structures themselves vary — fixed, profit-sharing, or hybrid — and each design creates different incentives. Understand what you're paying before comparing performance.

Alternative Investment Funds (AIFs)

AIFs are SEBI-regulated pooled investment vehicles requiring a minimum of ₹1 crore per investor. SEBI organises them into three categories:

| Category | Examples | Key Characteristics |

|---|---|---|

| Category I | Venture capital, infrastructure, SME, social impact | Longer lock-ins, early-stage exposure |

| Category II | Private equity, real estate, debt funds | Core mid-conviction HNI/UHNI allocation |

| Category III | Hedge funds, long-short, multi-strategy | Absolute return focus, more complex strategies |

AIFs carry illiquidity risk and longer lock-ins — often 5–7 years. They suit HNIs who can genuinely absorb the illiquidity, not those using them as a substitute for liquid equity exposure.

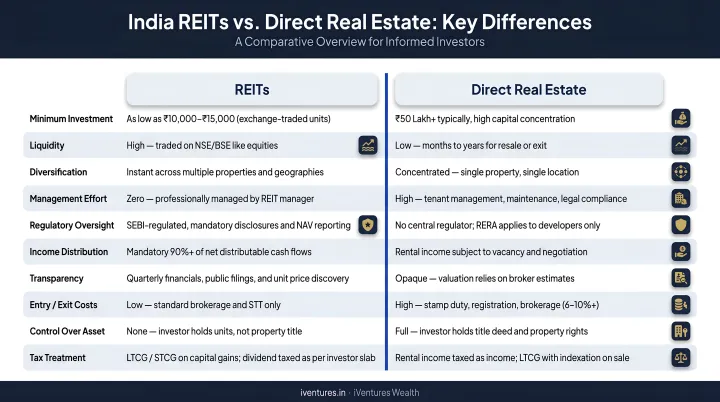

Real Estate, REITs, and InvITs

Direct property remains a major asset class for Indian HNIs, but the friction is real: stamp duty, registration costs, low rental yields (typically 3–4% for residential), and concentrated capital requirements that limit flexibility.

REITs and InvITs address most of these constraints — SEBI-regulated, exchange-listed vehicles providing liquid access to commercial real estate and infrastructure income. Key facts:

- India's listed REIT market cap stood at ₹39,839 crore as of March 31, 2026 (Indian REITs Association)

- Trading lot is now 1 unit, making REITs accessible without large upfront capital

- REITs must distribute at least 90% of net distributable cash flows to unit holders

- REITs typically target 6–8% yields from Grade-A commercial properties

For most HNIs, a combination of direct property (where specific projects make sense) and REIT/InvIT exposure (for liquidity and income) is more practical than concentrating capital in a single asset.

International Diversification via LRS

Resident Indians can remit up to USD 250,000 per financial year under RBI's Liberalised Remittance Scheme to invest in foreign equities, bonds, and real assets. For a family of four, that's USD 1 million in annual deployment capacity.

International diversification serves three distinct purposes that domestic portfolios can't replicate:

- Currency exposure: Natural hedge against rupee depreciation over long holding periods

- Sector access: Global themes — semiconductors, AI infrastructure, genomics, e-mobility — remain thinly represented on Indian exchanges

- Concentration reduction: Limits the portfolio's dependence on a single regulatory and macroeconomic environment

Compliance requirements to track:

- TCS: 20% above the ₹10 lakh threshold (raised from ₹7 lakh in Budget 2025), creditable against tax liability at filing

- Schedule FA: Foreign asset holdings must be disclosed in ITR using Schedule FA — ITR-1 and ITR-4 do not contain this schedule

- Capital gains: Short-term gains at slab rates; long-term (held 24+ months) at 12.5% without indexation

Tax Planning Strategies for HNIs in India

Capital Gains Optimisation

The post-Budget 2024 rate changes make capital gains management more critical than ever:

- Book equity LTCG up to ₹1.25 lakh annually — tax-free under the exemption, and harvesting gains each year resets the cost basis

- Time realisations across financial years to smooth taxable income and avoid surcharge threshold breaches

- Avoid unnecessary short-term churn: at 20% STCG, the drag compounds quickly against a buy-and-hold approach

- Re-evaluate debt fund exposure: the removal of indexation for debt funds acquired post-April 2023 changes the after-tax return calculus

HUF as a Separate Taxpayer

A Hindu Undivided Family (HUF) is recognised by the Income Tax Department as a distinct filing unit — separate PAN, separate basic exemption slab, separate tax computation. For Hindu, Sikh, Buddhist, and Jain families, this means income and capital gains validly belonging to the HUF are assessed at the HUF level, not added to the individual's income.

This is a legitimate legal structure — not a workaround — that requires a formal HUF deed, proper accounting, and CA guidance from inception.

The benefit is meaningful only when income is genuinely attributable to the HUF. Simply rerouting individual income through the HUF does not hold up under scrutiny.

Private Family Trusts

Private discretionary trusts are primarily estate and succession planning instruments. Income in an irrevocable private trust can attract maximum marginal rate taxation depending on structure and beneficiary share. The real value lies in controlled, legally defensible wealth transfer across generations, creditor protection, and privacy — not tax reduction.

Trust structures become particularly relevant for UHNI families (₹50 crore+) where family office governance, business succession, and multi-generational wealth transfer are core objectives. At iVentures Wealth, trust structuring is integrated into Family Office mandates, coordinated with qualified external legal counsel for deed drafting and execution.

Charitable Giving

Donations to 80G-registered entities reduce taxable income by 50% or 100% depending on the organisation, with some categories subject to qualifying limits.

For HNIs with larger philanthropic goals, establishing a private charitable trust or Section 8 company creates both a tax-efficient giving vehicle and a family legacy structure. Key considerations by donor profile:

- Resident Indians: Standard 80G deductions apply; no FCRA implications for domestic donations

- NRIs donating from personal savings via normal banking channels: Treated differently from foreign citizens or OCIs — the receiving organisation's FCRA eligibility must be verified before any donation is made

Estate Planning and Generational Wealth Transfer

The foundation is documentation most HNIs still haven't completed: a registered, updated will, nominee designations across all financial assets (mutual funds, demat, bank accounts, insurance), and a power of attorney for financial decisions in the event of incapacitation.

Business Standard reports that even with a valid will, missing paperwork, nominee confusion, and executor disputes can delay inheritance claims for years. This is entirely avoidable.

Private Discretionary Trusts

A properly structured trust lets the settlor (wealth creator) define exactly how and when wealth reaches beneficiaries — controlling distributions to protect against imprudent spending, creditor claims, or premature transfer.

Assets that can be held within a trust structure include:

- Real estate and immovable property

- Listed and unlisted shares or business interests

- Mutual funds, bonds, and other financial assets

- Intellectual property and family heirlooms

The trust deed must be drafted by qualified legal counsel. This is not a DIY exercise.

NRI and OCI Estate Planning

NRI/OCI estate planning is routinely overlooked in HNI financial planning — and the consequences of that gap are significant.

Key considerations:

- Inherited Indian assets: NRIs/OCIs can acquire property in India by inheritance from residents or from non-residents who held it under foreign exchange law

- Repatriation: RBI guidelines allow up to USD 1 million per financial year from inherited assets, subject to documentation requirements

- Dual wills: Multiple wills are recommended when assets span jurisdictions — probate rules differ between India, the US, UK, UAE, and other countries

- FEMA compliance: Inbound and outbound investment structuring for NRIs must follow RBI/FEMA guidelines on account types and remittance rules

iVentures Wealth's NRI estate planning practice coordinates with local counsel across the US, UK, UAE, Singapore, Canada, and Australia. This gives clients a consolidated view of cross-border assets with repatriation and inheritance pathways structured to align with each jurisdiction's residency rules and legal requirements.

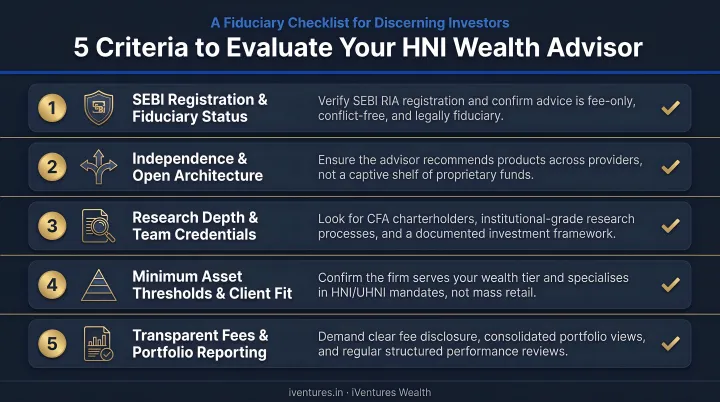

How to Choose the Right Wealth Advisor as an HNI

The Question That Reveals Everything

Ask any advisor two questions: "Are you a SEBI-registered investment adviser?" and "Do you earn commissions on the products you recommend?"

As of June 2026, SEBI lists 1,044 registered investment advisers across India. A SEBI RIA operates under Investment Advisers Regulations 2013, which restricts receiving consideration from anyone other than the client in an advisory context. A mutual fund distributor or bank relationship manager earns trail commissions from product manufacturers — a structural conflict that rarely gets disclosed proactively.

The distinction isn't subtle. A distributor recommending a regular-plan mutual fund over a direct plan costs you 0.5–1.0% annually in trailing commission — compounded over 15 years, on a ₹10 Cr portfolio, that's meaningful capital lost before compounding even begins.

What to Look for in an HNI Wealth Advisor

Beyond SEBI registration and fee transparency, look for:

- CFA or relevant investment credentials: Signals rigorous investment training and analytical depth

- HNI/UHNI-specific experience: Not retail clients — complex concentrated positions, business succession, AIF due diligence

- Open-architecture access: Can the advisor recommend any SEBI-regulated product, or are they constrained to a proprietary shelf?

- Coordination capability: Can they work alongside your CA, lawyer, and family office rather than operating in isolation?

- Reporting infrastructure: Consolidated dashboards across multi-entity, multi-asset holdings — not just a single demat view

These criteria are easy to state and harder to find in practice. iVentures Wealth (SEBI RIA: INA000019026) was built specifically around them: fee-only advisory with no commissions, trail income, or placement fees, with open-architecture access across mutual funds, PMS, AIFs, bonds, and private credit. Founded in 2005, the firm's CFA-led team manages ₹1,200+ crore across 150+ HNI and UHNI families.

Practical Questions to Ask Any Advisor

Before committing to an advisory relationship:

- How exactly are you compensated — and do any of those payments come from product manufacturers?

- What investment options beyond mutual funds can you access and conduct due diligence on?

- How do you coordinate with my CA and legal advisors on tax and estate planning?

- How often will we formally review the financial plan — not just the portfolio?

- What is your process when markets drop 30%?

These questions separate advisors with genuine HNI depth from those primarily engaged in product distribution.

Frequently Asked Questions

What is considered high net worth in financial planning?

Globally, HNWI typically refers to someone with investable assets of $1 million (approximately ₹8–9 crore) or more. In Indian wealth management practice, firms often apply HNI strategies starting at ₹1 crore in investable assets, with many firms — including iVentures Wealth — setting their working HNI threshold at ₹5 crore or more in investible surplus.

Who qualifies as an HNI in India?

SEBI defines eligibility by product: PMS requires ₹50 lakh minimum, AIFs require ₹1 crore, and IPO Non-Institutional Investor status applies to applications above ₹2 lakh. In wealth management practice, HNI typically means ₹5 crore or more in investable assets, with UHNI defined as ₹50 crore or more.

What investment options are available for HNIs beyond mutual funds in India?

Key options include:

- PMS — ₹50 lakh minimum, direct stock ownership

- AIFs — all three SEBI categories, ₹1 crore minimum

- REITs and InvITs — real estate income exposure

- Structured products and direct bonds

- International equities and ETFs — via the LRS (USD 250,000/year per individual)

Each comes with distinct risk, liquidity, and tax profiles.

How is tax planning different for high net worth individuals?

HNIs face higher marginal rates, surcharges on income above ₹5 crore, and more complex capital gains across multiple asset classes. They also have more to gain from HUF structures, family trusts, and strategic asset location. Tax planning must integrate with investment decisions year-round, not just at financial year-end.

What is the difference between an HNI and a UHNI?

HNI generally refers to those with ₹5–50 crore in investable assets; UHNI refers to those with ₹50 crore or more. UHNIs typically require more sophisticated structures — family offices, private trusts, pre-IPO access, and multi-jurisdictional estate planning — that are neither practical nor necessary at lower wealth levels.

What documents does every HNI need in their estate plan?

At minimum: a registered, updated will; nominee designations across all financial accounts and policies; and a power of attorney for financial decisions. Beyond these, a private discretionary trust becomes relevant for complex multi-asset or multi-beneficiary scenarios, particularly where NRI beneficiaries or business succession is involved.