This scenario plays out across India more often than most investors realise. Founders post-exit, senior executives managing ESOPs, UHNIs consolidating family wealth — all vulnerable to advice that is suitable rather than optimal.

The difference comes down to one word: fiduciary.

This article covers what a fiduciary financial advisor actually is, how they differ from non-fiduciary advisors, what services they provide, how they are compensated, and how to verify one in India.

Key Takeaways

- A fiduciary advisor is legally obligated to act in your best interest — not just recommend something suitable

- SEBI Registered Investment Advisers (RIAs) are India's regulatory equivalent of fiduciaries

- RIAs cannot earn commissions from product manufacturers — fees come directly from clients

- Only 927 registered IAs served over 12 crore securities-market investors as of August 2024

- Verify any advisor's SEBI RIA status in minutes on the SEBI public registry

What is a Fiduciary Financial Advisor?

A fiduciary is an individual or organisation with a legal obligation to act in another party's best interests. In financial advisory, this means the advisor must prioritise your financial wellbeing above their own gain, any third party's interests, and any product manufacturer's incentives.

The word "fiduciary" is not a job title anyone can claim — it reflects a specific legal standard of conduct. The key distinction is between two competing standards:

- Suitability standard — the advisor must recommend products that are suitable for you, given your profile

- Fiduciary standard — the advisor must recommend what is genuinely optimal for you, and cannot let personal gain influence that recommendation

Most bank relationship managers, mutual fund distributors, and insurance agents operate under the suitability standard. A fiduciary advisor operates under a higher legal bar.

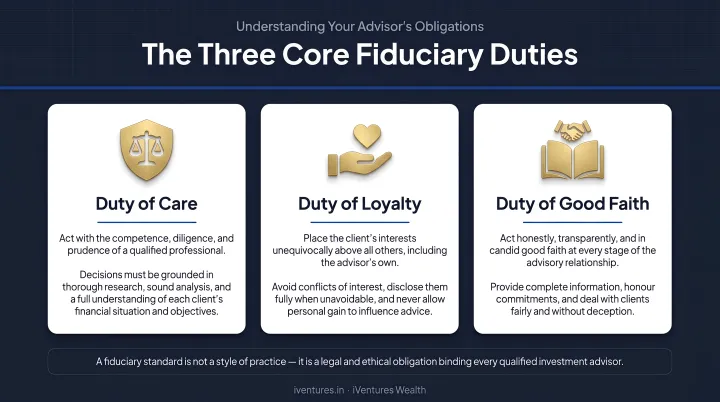

Fiduciary Duty: The Legal Foundation

Fiduciary duty has three core components:

- Duty of Care — The advisor must thoroughly understand your financial situation, goals, risk tolerance, time horizon, family structure, and tax position before making any recommendation

- Duty of Loyalty — The advisor must place your interests ahead of their own compensation, commissions, or third-party incentives

- Good Faith & Confidentiality — The advisor must proactively disclose conflicts of interest and keep your financial information private

Consider a common example: an advisor recommends a regular plan mutual fund to earn a 1–1.5% annual distributor commission, when a direct plan of the same scheme is available at a fraction of the cost. That recommendation directly conflicts with fiduciary duty. Under SEBI's Investment Adviser Regulations, a SEBI Registered Investment Adviser is legally prohibited from doing exactly this.

Fiduciary Financial Advisor vs. Non-Fiduciary: Key Differences

Not all financial advisors are fiduciaries — and in India, the majority are not. Understanding the structural difference matters before you place significant wealth with anyone.

The Commission Conflict

India's advisory ecosystem is dominated by mutual fund distributors (MFDs), bank relationship managers, and insurance agents. These intermediaries operate under the suitability standard: they must recommend products appropriate for you, but they are not legally required to recommend the best option. They earn commissions from product manufacturers — and that creates an inherent structural conflict.

The scale of this is substantial: per AMFI's FY2024-25 commission disclosure data, distributors collectively received approximately ₹21,217 crore in gross commissions from fund houses in a single financial year.

In practical terms, a distributor may:

- Recommend a regular plan mutual fund (earning 1–1.5% annual trail) over an identical direct plan with no commission

- Steer clients toward higher-fee PMS products that carry placement fees

- Prioritise insurance-linked investment products that generate upfront commissions

The "Free Advice" Illusion

Non-fiduciary advisors often appear to offer advice at no cost — because their compensation is embedded in product costs. SEBI's own illustration makes the impact tangible: a regular plan with a 1.5% expense ratio reduces a 10% gross return to 8.5%, while a direct plan at 0.5% delivers 9.5%. Over a 15-year horizon on a ₹1 crore portfolio, that 1% annual gap compounds into a material difference in terminal wealth.

A fiduciary advisor charges you directly and transparently — the fee appears on your invoice. With a distributor, the cost is embedded in your fund's expense ratio, deducted silently every year regardless of performance. The table below captures where these two models structurally diverge.

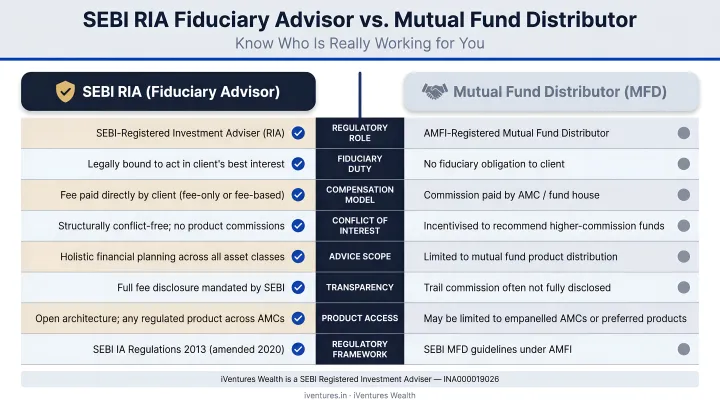

A Side-by-Side Comparison

| Factor | SEBI RIA (Fiduciary) | Mutual Fund Distributor |

|---|---|---|

| Legal obligation | Act in client's best interest | Recommend suitable products |

| Compensation | Direct client fee only | Commissions from fund houses |

| Direct plan access | Yes | No incentive to recommend |

| Conflict of interest | Structurally eliminated | Structurally present |

| Regulatory standard | Fiduciary | Suitability |

This is not a moral judgment against all distributors — many are experienced professionals who genuinely serve their clients well. The distinction is structural, not personal. Goodwill is not the same as a legal obligation, and the fiduciary standard exists precisely to close that gap.

What Does a Fiduciary Financial Advisor Do?

A fiduciary financial advisor's role is advisory and relationship-driven — not transactional. They build a financial plan and execute it on your behalf across your entire financial life — without the conflict of a product sale driving the recommendation.

Core Services

- Investment portfolio management — asset allocation, fund selection, rebalancing, all aligned to your specific goals and risk profile

- Comprehensive financial planning — covering tax optimisation, retirement planning, and estate structuring

- Ongoing monitoring and reassessment — portfolios are reviewed as markets move and as your life circumstances evolve

- Written advice and documentation — a fiduciary advisor provides recommendations in writing, not just verbal suggestions

The Discovery-First Approach

The fiduciary standard mandates that an advisor start with deep discovery — not product pitching. Before any recommendation is made, they gather your complete financial picture, including:

- Income sources and existing portfolio

- Outstanding liabilities and family structure

- Tax position and applicable jurisdiction

- Risk tolerance and investment time horizon

- Long-term goals and succession considerations

This is a legal obligation under the fiduciary standard — not a courtesy.

Family Office-Style Services for UHNIs

For UHNIs and affluent families, fiduciary advisors often extend into family office territory. This includes:

- Consolidated portfolio views across multiple entities, accounts, and geographies

- Succession and estate planning — wills, private trusts, cross-border inheritance structures

- Multi-generational wealth governance — family constitutions, next-generation planning

- Tax optimisation across jurisdictions, including FEMA-compliant overseas structures

- Philanthropic structuring

At this level of complexity, full alignment with client interests is non-negotiable. Any product-driven incentive would compromise the integrity of the advice.

According to EY India, Indian family offices grew from approximately 45 to around 300 between 2018 and 2024. This growth reflects rising demand for structured, independent wealth governance among India's most affluent families.

The Fiduciary Standard in India: SEBI RIA Regulations

India's regulatory equivalent of the fiduciary standard sits within the Securities and Exchange Board of India (Investment Advisers) Regulations, 2013, first notified on January 21, 2013, with a significant strengthening amendment on July 3, 2020.

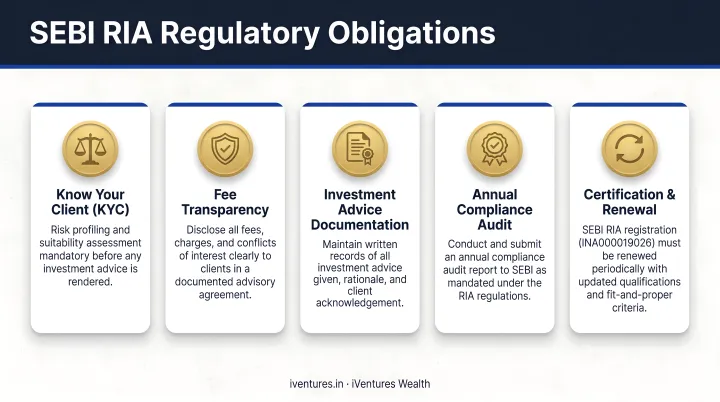

What SEBI RIA Regulations Require

Under Regulation 15(1), an investment adviser must act in a fiduciary capacity toward clients. The SEBI Code of Conduct further requires IAs to act honestly, fairly, and in the client's best interests. Key provisions include:

- Commission prohibition — an IA cannot receive consideration, remuneration, or commission from anyone other than the client for advised products

- Advisory-distribution segregation — an advisor cannot simultaneously act as a distributor for the same client

- Written client agreement — required before any advisory service commences

- Conflict of interest disclosure — must be proactive, not reactive

- Annual compliance audit — mandatory

SEBI RIAs vs. Mutual Fund Distributors

MFDs are registered with AMFI and earn trail commissions from fund houses. AMFI's own FAQ states explicitly that MFDs are not permitted to provide investment advice unless separately registered with SEBI as Investment Advisers.

MFDs serve a legitimate function in product distribution — but they are not fiduciaries and are not legally required to prioritise your interests above their commission income.

iVentures Wealth: A SEBI-Registered Fiduciary in Practice

iVentures Wealth (SEBI RIA No. INA000019026, registered since 2010) operates under this fiduciary framework. The firm provides fee-only advisory to UHNIs, family offices, and corporates, with a CFA-led research team, transparent AUM-based fees, and a regulatory prohibition on earning commissions from any product manufacturer.

How Are Fiduciary Financial Advisors Compensated?

SEBI RIAs charge clients directly. No commissions, no trail income, no placement fees. SEBI's September 2020 guidelines specify two permitted fee modes:

- Fixed fee — capped at ₹1,25,000 per annum per client

- AUA-based fee — capped at 2.5% of assets under advice per annum

Fee-Only vs. "Free" Advice

The fee-only model means transparency: you know exactly what you are paying and why. With a distributor, the cost is embedded in the product's expense ratio — invisible in your statement, but compounding against your returns every year.

The numbers make this concrete: a 1% annual cost difference between a regular and direct plan, sustained over 10–15 years, quietly erodes terminal wealth on any portfolio above ₹1 Cr. The advisor's fee is disclosed upfront. Distributors rarely disclose their commission at all.

Transparency of compensation is itself a fiduciary obligation — not a marketing differentiator. That distinction matters when the advisor sitting across from you is recommending where your wealth goes.

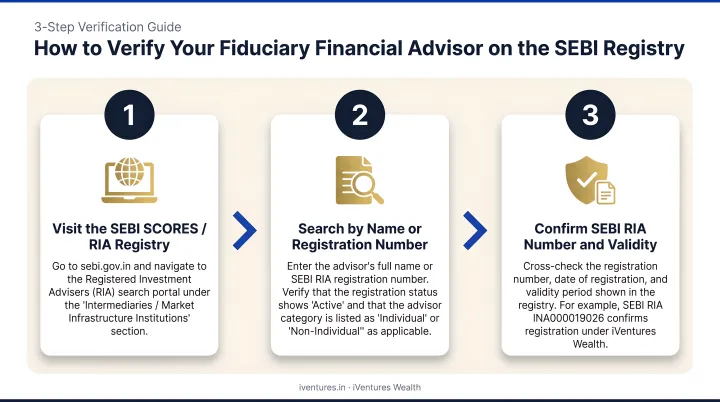

How to Find and Verify a Fiduciary Financial Advisor in India

Verification is straightforward. Follow these steps:

- Check the SEBI RIA registry — SEBI maintains a public list at SEBI's RIA public registry. Search by name or registration number. If the advisor is not on this list, they are not a fiduciary under Indian law

- Ask directly about compensation — a genuine fiduciary will answer directly

- Review the fee disclosure — it must be in writing, before any investment is made

Once you've confirmed an advisor is SEBI-registered, these questions help you go deeper into how they actually operate.

Questions to Ask Any Potential Advisor

- Are you a SEBI Registered Investment Adviser? What is your registration number?

- How are you compensated — do you earn any commissions from product manufacturers?

- Will you provide your advice and recommendations in writing?

- What is your fee structure, and is it disclosed upfront?

- Do you have any conflicts of interest I should know about?

To see how this verification process works in practice, you can look up iVentures Wealth on the SEBI RIA registry under registration number INA000019026 — a firm that has operated as a SEBI-registered fiduciary since 2010. Use the same registry check and the questions above with any advisor you're considering.

Frequently Asked Questions

What does a fiduciary financial advisor do?

A fiduciary financial advisor manages investments, creates financial plans, and provides ongoing wealth guidance across your entire financial life. They are legally obligated to act in your best interests, disclose all conflicts of interest, and recommend options that are genuinely optimal — not just suitable.

Is it better to have a fiduciary or a financial advisor?

A fiduciary is a type of financial advisor — the distinction is the legal standard they operate under. For significant wealth decisions, a fiduciary advisor provides a legal guarantee of client-first advice that non-fiduciary advisors cannot match, regardless of good intentions.

What is the difference between a SEBI RIA and a mutual fund distributor in India?

A SEBI Registered Investment Adviser is legally barred from earning commissions and must act in the client's best interest. A mutual fund distributor earns trail commissions from fund houses and is only required to recommend suitable products, which may not always be the most optimal choice for you.

How are fiduciary financial advisors compensated in India?

SEBI RIAs charge clients directly through fixed fees (capped at ₹1,25,000 per annum) or AUA-based fees (capped at 2.5% per annum). They cannot earn commissions from product manufacturers. This fee-only model means your advisor profits only when your portfolio does.

How can I verify if my financial advisor is a fiduciary in India?

Check the SEBI RIA public registry to confirm registration status. Ask the advisor directly about their compensation structure. A genuine SEBI RIA will confirm they earn no commissions and will share their fee schedule upfront.

Do fiduciary financial advisors only work with ultra-wealthy clients?

No. While fiduciary advisory is especially valuable for complex, high-value situations, SEBI RIAs work across a range of clients. The fiduciary standard is about the quality and alignment of advice — not the size of the portfolio.