Introduction

Managing significant wealth demands more than picking the right funds. Most affluent individuals, business owners, and families eventually discover that owning good investments without a coordinating framework means paying more in tax than necessary, leaving estate planning unfinished, and holding a portfolio no one truly oversees end-to-end.

That gap is more common than it looks.

The wealth management process is the structured answer to that problem. It integrates investment planning, tax strategy, estate structuring, risk management, and succession planning into a single, continuously managed engagement — not a series of disconnected transactions.

This article breaks down that process across its three life-stage goals and six sequential steps, so founders, CXOs, HNIs, and families can assess what genuinely integrated advisory looks like — and whether they're currently receiving it.

Key Takeaways

- Wealth management follows a six-step cycle — from data gathering and goal setting through to implementation and ongoing monitoring

- It operates across three life stages: accumulating wealth, preserving and growing it, and distributing it purposefully

- True wealth management integrates investments, taxes, insurance, and estate planning — not just fund selection

- SEBI-registered RIAs are legally required to act in your best interest and cannot earn product commissions

- Rigorous risk profiling, tax efficiency, and fiduciary alignment separate plans that protect wealth from those that merely manage it

What Is the Wealth Management Process?

The wealth management process is a structured advisory framework built around the client's entire financial life — not a single product or account. A wealth manager gathers comprehensive financial information, builds a personalised plan spanning investments, taxes, insurance, and estate matters, then executes and monitors it continuously.

The goal is not simply the highest return. It is maximising after-tax, risk-adjusted wealth in alignment with each client's specific goals at each life stage.

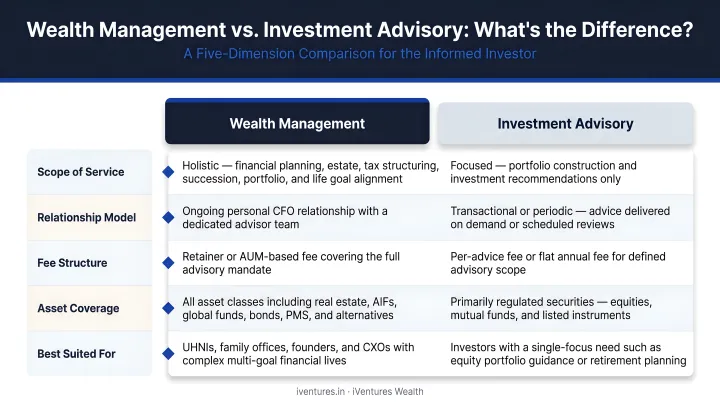

How It Differs from Standalone Investment Advisory

A standalone investment adviser typically addresses one dimension: which funds to hold or how to allocate across equity and debt. Wealth management coordinates multiple disciplines at once:

- Constructs and rebalances portfolios across asset classes (mutual funds, AIFs, PMS, bonds, equities)

- Optimises taxes through LTCG/STCG strategies, post-2023 debt fund treatment, HUF and trust structures

- Plans estate and succession through wills, family trusts, and wealth transfer structuring

- Identifies insurance gaps, concentration risk, and stress-tests portfolios against adverse scenarios

- Maps every rupee to a specific goal, timeline, and required corpus

iVentures Wealth, a SEBI-registered RIA (INA000019026) based in Gurugram, describes this as a "personal CFO" model. It works alongside the client's chartered accountant and legal counsel rather than replacing them — covering strategy, allocation, and governance where the CA handles compliance.

The Three Goals That Drive the Wealth Management Process

Every wealth management engagement is organised around three life-stage goals. They reflect how financial priorities genuinely shift as wealth and age evolve.

Wealth Accumulation

During peak earning years, particularly for founders, senior executives, and professionals, the primary objective is growing assets as efficiently as possible. A longer time horizon allows for greater equity exposure and deliberate risk-taking.

At this stage, a wealth manager typically helps with:

- Building high-conviction equity portfolios aligned with risk profile and income trajectory

- Managing ESOPs and RSUs — vesting-schedule planning, exercise-timing tax optimisation, post-vesting diversification

- Systematic deployment of bonuses and irregular cash flows into structured investment frameworks

- AIF and global fund exposure for diversification beyond domestic equities

- Salary and savings structuring to maximise post-tax wealth accumulation (including NPS contributions)

Wealth Preservation

As wealth grows, protecting it becomes as important as growing it. Market volatility, inflation, tax drag, and unforeseen events can steadily erode a portfolio that is not actively managed.

The preservation strategy progressively shifts toward:

- A three-bucket asset allocation framework: Safety (5–7 years of expenses in high-quality fixed income), Stability (balanced portfolio across an 8–15 year horizon), and Growth (select AIFs, PMS, and private equity)

- Diversification across equity, debt, real estate, alternatives, and international assets to eliminate single-stock and single-sector concentration risk

- Private credit and AIF instruments targeting inflation-beating returns (typically 12–16% IRR ranges) where appropriate

- Tax-efficient structures — LTCG planning, indexation-aware portfolio design, and family trust or HUF considerations

- Estate planning reviews to ensure the wealth already built transfers smoothly

Wealth Distribution

The distribution phase focuses on deploying wealth purposefully — for retirement income, philanthropic giving, or transferring assets to heirs — in a tax-efficient and legally sound way.

In the Indian context, this involves:

- Withdrawal strategy optimisation: bucket strategies, systematic withdrawal plans (SWPs) calibrated to LTCG-efficient lots, dividend and bond-ladder income structures

- Private family trust establishment — discretionary, specific, and revocable structures — to ring-fence corpus and formalise distribution rules

- Will drafting, registration, and custody with periodic updates; executorship support for beneficiaries

- Cross-border inheritance coordination for NRI/OCI families with assets in multiple jurisdictions

- Family governance protocols and next-generation training for families managing business wealth

Morningstar's Gamma study estimated that goal-optimised retirement planning strategies generate approximately 22.6% more certainty-equivalent retirement income compared to unstructured approaches. That gap is the difference between a plan that responds to life stages and one that simply chases returns.

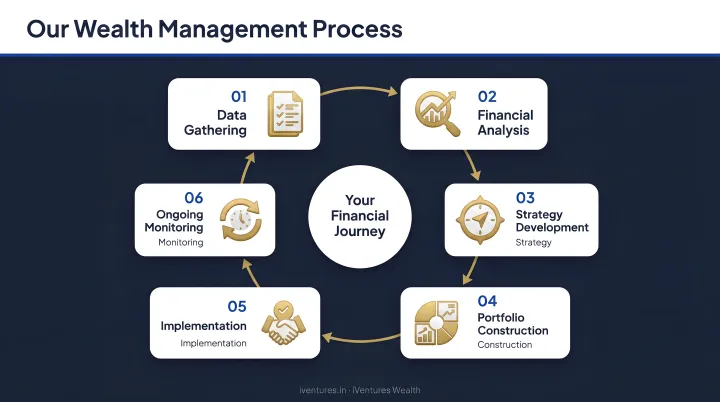

The 6 Steps of the Wealth Management Process

These six steps represent the complete lifecycle of a wealth management engagement, from the first discovery conversation to ongoing partnership. They are not linear or finite — they repeat as a client's circumstances change.

Step 1: Gathering Financial Data

The process begins with a comprehensive discovery session. The advisor collects all relevant financial information across:

- Income sources, business interests, and cash flow patterns

- All assets and liabilities: equity holdings, debt instruments, real estate, and international assets

- Existing insurance policies, provident fund balances, and retirement accounts

- Tax filings, estate documents, and any existing wills or trust structures

No plan can be sound without an accurate and complete financial picture. This step is as much about understanding values, family dynamics, and life priorities as it is about numbers.

At iVentures Wealth, this discovery feeds directly into a unified family wealth dashboard: operating businesses, real estate, financial portfolios, and international assets consolidated into a single net-worth and cash-flow view.

Step 2: Establishing Financial Goals

Once the financial picture is clear, the advisor works collaboratively with the client to define and prioritise goals. These might include:

- Early retirement or FIRE (Financial Independence, Retire Early)

- Funding children's or grandchildren's education

- A business exit or IPO liquidity event

- Philanthropic giving or legacy endowments

- Building generational wealth through structured inheritance

Goals must be specific, time-bound, and ranked by importance. A plan built around generic benchmarks (rather than the client's actual priorities) will consistently misallocate resources.

Step 3: Analysing the Portfolio and Financial Position

Before making a single recommendation, the advisor conducts a thorough audit of current holdings. This analysis covers:

- Asset allocation vs. stated risk tolerance : identifying over- or under-exposure

- Concentration risk: single-stock, single-sector, single-geography exposures

- Performance relative to benchmarks and stated goals (including opportunity cost analysis)

- Tax inefficiencies: unrealised gains, suboptimal fund structures, missed LTCG harvesting windows

- Insurance and estate coverage gaps

iVentures Wealth's CFA-led team describes this as "X-raying the portfolio" : surfacing the overlaps, redundancies, and hidden risks that a client's existing holdings may carry before any restructuring begins.

Step 4: Creating a Comprehensive Financial Plan

The plan encompasses multiple coordinated domains:

- Investment recommendations: asset allocation, product selection across mutual funds, PMS, AIFs, bonds, and global funds

- Tax optimisation: LTCG/STCG planning, post-2023 debt fund treatment under Section 50AA (Finance Act 2023, effective 1 April 2024), HUF structures, family trust planning, and DTAA structuring for NRIs

- Retirement income projections: SWP design, 4% rule implementation, inflation-adjusted corpus modelling

- Estate planning coordination: will drafting, family trust establishment, beneficiary updates

- Succession planning: family governance framework, business transition structuring

- Insurance gap analysis: identifying under-coverage relative to current net worth and income

Russell Investments' 2026 Value of an Advisor Study estimates total advisor value at approximately 4.92% annually: asset allocation (0.26%), behavioural coaching (2.30%), customised family wealth planning (1.13%), and tax-smart investing (1.23%).

These are model-based estimates, not guarantees. But they show where structured advisory creates compounding value well beyond fund selection alone.

The plan is presented for discussion and refinement — not handed over as a finished document. It evolves with the client's life.

Step 5: Implementing the Plan

Implementation involves coordinated execution across multiple dimensions:

- Opening or restructuring investment accounts and demat folios

- Rebalancing portfolios to target allocations with tax-efficient sequencing

- Setting up tax-saving structures : HUFs, trusts, GIFT City vehicles where applicable

- Updating wills, estate documents, and beneficiary designations

- Activating or revising insurance coverage to close identified gaps

- Coordinating with chartered accountants on capital gains reporting, ITR preparation, and FEMA-compliant remittance routing

The wealth manager acts as the central coordinator : ensuring execution is integrated rather than siloed across providers. iVentures Wealth prepares standardised reports for clients' CAs, summarising income, gains, and holdings by PAN, which reduces errors and simplifies ITR filing. For NRI/OCI families, the team coordinates with local counsel in relevant jurisdictions for cross-border assets.

Step 6: Ongoing Monitoring and Review

Without active monitoring, even a well-constructed plan loses alignment over time. iVentures Wealth conducts quarterly formal portfolio reviews as a minimum standard, covering:

- Performance analysis against benchmarks and goals

- Asset allocation alignment and rebalancing needs

- Tax optimisation opportunities (including budget-driven rule changes)

- Liquidity planning and income adequacy

- Adjustments triggered by major life events: business sale, inheritance, marriage, regulatory changes

The firm also distinguishes proactive monitoring from reactive management. Proactive monitoring means the advisor team identifies emerging issues : concentration drift, tax inefficiency, market regime change — and acts before they impact the client. Reactive management, by contrast, responds only after problems materialise.

Between formal reviews, iVentures Wealth's Wealth Monitor App (launched in 2020) gives clients consolidated, real-time visibility into mutual funds, equities, bonds, FDs, PMS, AIFs, and insurance (all family members under a single login), making portfolio oversight a continuous process rather than a quarterly event.

Key Factors That Shape Wealth Management Outcomes

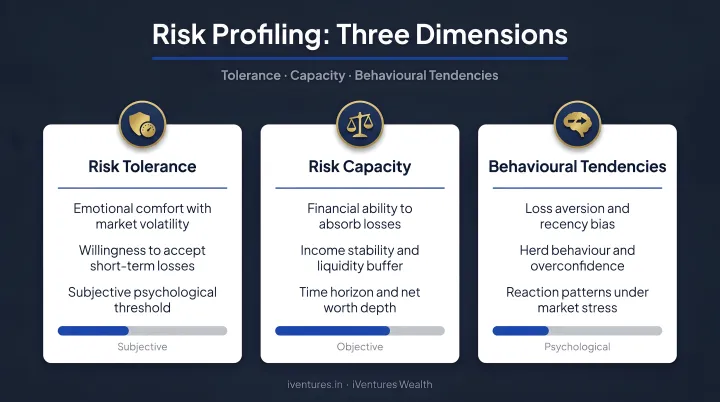

Risk Profiling Accuracy

If a client's actual risk tolerance is misread, the entire asset allocation will be misaligned — producing either excessive volatility or insufficient growth. Effective risk profiling goes beyond a standard questionnaire. It assesses:

- Risk tolerance: emotional and psychological capacity to withstand drawdowns

- Risk capacity: financial ability to absorb losses without affecting life goals

- Behavioural tendencies: susceptibility to return-chasing, panic selling, or concentration bias

At iVentures Wealth, risk profiling feeds directly into personalised asset allocation — not generic model portfolios. The analysis examines how different equity-debt-alternatives combinations behave across volatility scenarios, with specific attention to non-linear risk relationships.

Tax Efficiency

Tax drag is one of the most impactful, and most underutilised, levers in wealth management. Vanguard's 2025 tax-aware portfolio research found that tax-aware construction projected a 5.5% median after-tax return for top earners versus 5.0% for tax-agnostic portfolios — a 0.5% annual gap that compounds into material wealth differences over decades.

That principle holds directly in India, where the key levers include:

- LTCG/STCG treatment across equity and debt instruments

- Section 50AA's post-2023 debt fund reclassification

- HUF structures and family trusts for income splitting

- DTAA-based planning for NRI investors

Fiduciary Alignment

The advisor's incentive structure determines whose interests are actually being served. In India, SEBI-registered investment advisers are legally required — under the Investment Advisers Regulations (last amended November 25, 2025) — to act in a fiduciary capacity and receive remuneration only from clients, not from product manufacturers.

That regulatory distinction matters in practice. As of June 2026, only 1,044 advisers held SEBI RIA registration — a small number given India's wealth management scale. Mutual fund distributors operate under a separate framework, earning trail commissions that can create structural conflicts with client outcomes.

Verifying RIA registration before engaging is a critical first step. iVentures Wealth's registration (INA000019026) is publicly verifiable on the SEBI registry.

Common Misconceptions About the Wealth Management Process

Several assumptions keep investors from accessing the full value of structured advisory. Here are three worth examining closely.

"Wealth management is just portfolio management."

Investment selection is one component. The compounding value lies in integrating tax planning, estate structuring, insurance coverage, and goal-based planning into a strategy that holds together across market cycles and life transitions. A portfolio review is an input — not the output.

"Wealth management is only for the ultra-wealthy."

Knight Frank's 2025 Wealth Report defines HNWIs as those with assets exceeding US$10M — but structured advisory generates disproportionate value at lower thresholds when complexity increases. iVentures Wealth's minimum thresholds reflect this:

- NRIs/OCIs: ₹5 Cr (where cross-border tax and FEMA complexity justify early engagement)

- CXOs and professionals: ₹10 Cr

- Corporates: ₹50 Cr

- Family businesses/family offices: ₹100 Cr

"My CA or bank RM provides an equivalent service."

A CA's mandate is tax compliance and filing — not strategic asset allocation or estate structuring. A bank relationship manager typically recommends from a proprietary product shelf, with recommendations influenced by trail revenue.

A fiduciary wealth manager's scope is broader: conflict-free, integrated planning across the full financial picture. iVentures Wealth explicitly coordinates with clients' CAs — preparing standardised reports to streamline ITR filing — rather than replacing them.

Frequently Asked Questions

What are the steps of the wealth management process?

The six sequential steps are: financial data gathering, goal setting, portfolio analysis, plan creation, implementation, and ongoing monitoring and review. These steps repeat iteratively as a client's circumstances — income, family structure, tax environment, and goals — evolve over time.

What is the difference between a wealth manager and a financial advisor?

A wealth manager provides broader, integrated services — covering investments, tax planning, estate planning, insurance, and legacy goals — across a client's full financial picture. A financial advisor typically focuses on a narrower scope. Wealth managers serve clients with complex financial needs that require coordinated advisory rather than transactional product guidance.

Who should consider professional wealth management services?

Individuals with significant investable assets, complex tax situations, multiple income streams, business ownership, or estate and succession planning needs benefit most. In India, NRIs and OCIs with cross-border holdings, FEMA obligations, and DTAA considerations often reach the complexity threshold for structured advisory earlier than they expect.

How often should a wealth management plan be reviewed or updated?

Most wealth managers recommend quarterly formal reviews, with additional check-ins triggered by major life events such as a business exit, inheritance, marriage, or new tax legislation. The CFP Board and CFA Institute both treat ongoing monitoring as a required process step — not a one-time activity.

What is fiduciary duty and why does it matter in wealth management?

A fiduciary is legally required to act in the client's best interest. In India, SEBI-registered investment advisers operate under this obligation and cannot receive product commissions. Verifying SEBI RIA registration is a practical first step when evaluating any wealth management firm's alignment.

How is the wealth management process different from investing in mutual funds or stocks?

Investing in mutual funds or stocks addresses only asset accumulation. The wealth management process additionally covers tax planning, risk management, insurance gap analysis, estate structuring, and goal-based planning — so wealth is grown, protected, and structured efficiently at every stage of life.