The concept sounds straightforward. The execution isn't. The right route depends on your investor category, ticket size, tax situation, and whether you want direct stock ownership or managed exposure. Picking the wrong vehicle can meaningfully affect both returns and compliance.

This guide covers the full picture: how GIFT City works, the three investment routes available, step-by-step account setup, tax implications for resident Indians and NRIs, and the mistakes most investors make.

Key Takeaways

- GIFT City operates as an offshore jurisdiction under FEMA — meaning resident Indians can invest here without breaching domestic investment restrictions

- Access to US stocks runs through three routes: UDRs on NSE-IX, India INX Global Access, and GIFT City-domiciled feeder funds or AIFs — each suited to different ticket sizes and goals

- Resident Indians can remit up to $250,000 per year under LRS; NRIs invest without this cap

- Tax treatment is not automatic here — resident Indians owe Indian capital gains tax, while NRIs face outcomes that vary by fund structure and their country of residence

- Minimum investment thresholds vary sharply by route — from a few thousand dollars for exchange-traded UDRs to ₹1 Cr+ for GIFT City AIFs

What Is GIFT City and Why It Matters for US Stock Investments

GIFT City (Gujarat International Finance Tec-City) sits between Ahmedabad and Gandhinagar, but operates as an offshore financial jurisdiction — comparable in structure to Singapore's financial district or Dubai's DIFC, while remaining physically inside India. It functions within a Special Economic Zone (SEZ) and is regulated by the International Financial Services Centres Authority (IFSCA), established on 27 April 2020 under the IFSCA Act, 2019.

What makes this distinct is the regulatory model itself.

Domestic Indian finance operates under multiple regulators: SEBI, RBI, IRDAI. GIFT City consolidates all of this under a single authority, reducing friction for institutions and investors operating across asset classes or jurisdictions.

Why It Solves a Real Problem

Before GIFT City became operational, Indian investors had two options for US stock exposure:

- Domestic international mutual funds — many are currently restricted due to SEBI's aggregate industry cap of $7 billion for overseas securities, with lump-sum investments stopped in many schemes from early 2026

- Direct US broker accounts (Schwab, Interactive Brokers) — functional but outside India's regulatory perimeter, with inheritance and estate access complications for HNI families

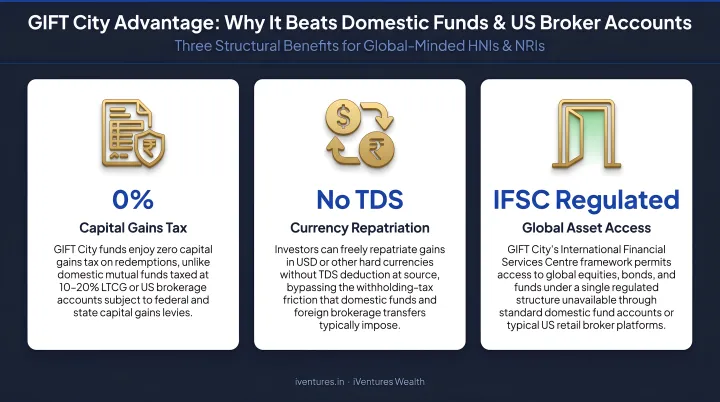

GIFT City fills this gap by combining three features that neither option above offers together:

- IFSCA-regulated infrastructure — investments made within India's legal perimeter

- Demat-based holding — assets held in Indian demat accounts, simplifying estate access

- USD-denominated exposure — a natural hedge against the rupee's long-term depreciation against the dollar

How to Invest in US Stocks via GIFT City: Step-by-Step

The account opening process differs by route and investor type — but the core sequence below applies across all three vehicles.

Step 1: Choose Your Investment Route First

Before opening any account, decide which vehicle suits your situation:

| Route | Best For | Minimum Entry |

|---|---|---|

| UDRs on NSE-IX | Direct stock ownership, smaller portfolios | Fractional — very low |

| India INX Global Access | Broader US securities range | Varies by broker |

| GIFT City Feeder Fund / AIF | Managed exposure, HNIs and UHNIs | US$10,000–US$150,000+ depending on structure |

Step 2: Open a GIFT City Demat and Trading Account

Your existing domestic demat account — whether with Zerodha, Groww, or any SEBI-registered broker — cannot be used. You need a separate demat account with an IFSCA-registered broker in GIFT City.

Documents for Resident Indians:

- Aadhaar or valid photo ID

- PAN card

- Income proof

- Video KYC

Documents for NRIs:

- PAN card

- Passport

- Foreign identity proof

- Foreign address proof

- Notarisation or in-person verification (video KYC not available for NRIs as of 2024)

All investors must submit Form W-8BEN, which certifies foreign status to the IRS and enables DTAA treaty benefits on dividend withholding.

Step 3: Fund Your Account via LRS (Resident Indians)

For resident Indians, funds sent to GIFT City for UDRs or fund investments fall under the Liberalised Remittance Scheme (LRS). Key parameters per RBI's LRS guidelines:

- Annual cap: $250,000 per person per financial year (April–March)

- TCS: 20% applies on LRS remittances above ₹10 lakhs (creditable against your final tax liability, though it temporarily reduces investable capital)

- Cumulative tracking required: The $250,000 limit covers all LRS purposes combined, not just investments

NRIs can fund their GIFT City account directly from a foreign bank account or NRE account — no LRS, no TCS implications.

Step 4: Select Your US Stocks or Fund

For the UDR route (NSE-IX): US stocks trade as fractional depository receipts. Settlement is T+3 versus T+1 on US markets directly. The trading window runs 7:00 PM to 1:30 AM IST during US daylight saving hours, aligning with NASDAQ and NYSE sessions.

For feeder funds or AIFs: You allocate to a GIFT City-domiciled fund managed by an IFSCA-registered Fund Management Entity, which pools and deploys capital into US equities or global indices.

iVentures Wealth assists clients selecting this route with fund manager due diligence, risk profiling, lot-sizing, and ongoing monitoring — particularly for NRI and UHNI clients where USD-denominated tracking and DTAA-efficient structuring matter.

Step 5: Monitor Your Holdings

After purchase, UDRs are credited directly to your GIFT City demat account — not held in a broker pool as with direct US brokerage. For fund investments, NAVs are published in dollar terms, which simplifies performance tracking for investors monitoring returns in USD.

The Three Investment Routes for US Stocks in GIFT City

Selecting the wrong route is one of the most common mistakes investors make — each of the three vehicles works differently in terms of access, ownership structure, minimums, and who it suits best.

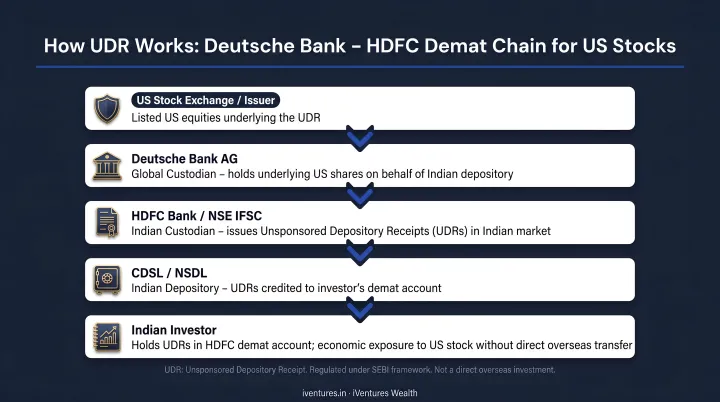

Route 1: UDRs on NSE-IX (NSE IFSC Receipts)

NSE IFSC launched trading in Unsponsored Depository Receipts on 3 March 2022, starting with 8 US stocks including Apple, Microsoft, Tesla, Amazon, Alphabet, Meta, Netflix, and Walmart. The catalog is expected to grow over time.

How the structure works:

- The underlying US share is held by Deutsche Bank AG, New York as sub-custodian

- HDFC Bank's IFSC Banking Unit serves as the primary Indian custodian

- Investors hold UDRs in their GIFT City demat account — not the actual US share

- Fractional ratios (for example, 1:100 or 1:200 relative to the underlying share value) make high-priced stocks accessible at small amounts

Practical limitations: The current catalog covers select large-cap US stocks. Investors wanting mid-caps, sector ETFs, or a broader universe will find this route restrictive.

Route 2: India INX Global Access

India INX — BSE's GIFT City subsidiary — offers a Global Access platform connecting investors to more than 130 international exchanges, including US markets. This works through an introducing broker/Global Access Provider model rather than direct listing.

This route suits investors who need wider reach than the UDR catalog currently offers:

- Access to a broader range of US securities and sector-specific instruments

- Exposure to markets beyond the US — other geographies via the same platform

- Entry point for instruments not yet listed as UDRs on NSE-IX

Route 3: GIFT City Feeder Funds and AIFs

For investors who prefer managed exposure over picking individual stocks, GIFT City-domiciled funds offer a third path. Indian AMCs and fund managers pool capital and deploy into US equities or global indices — structured as standalone funds or feeder-master arrangements, these are managed vehicles, not direct ownership.

Key regulatory minimums per IFSCA:

- Restricted Schemes (AIFs): US$150,000 minimum

- Venture Capital Schemes: US$250,000 minimum

- Retail schemes: Generally no minimum, except certain close-ended structures at US$10,000

- PMS: US$75,000 minimum

This route is most practical for HNIs, UHNIs, and family offices who prefer managed exposure over self-directed stock picking. It also bypasses the domestic mutual fund overseas cap — GIFT City-domiciled funds are not subject to SEBI's US$7 billion aggregate limit.

Each route carries a distinct risk profile, cost structure, and suitability threshold — understanding these differences is the foundation for making the right choice.

Tax Implications of Investing in US Stocks via GIFT City

The most common misconception: GIFT City is a tax-free zone. It isn't — at least not for investors.

The actual tax benefit is that services provided to SEZ units for authorised operations qualify as zero-rated supplies under IGST Section 16, meaning management fees within GIFT City are not subject to GST — investment gains are taxed separately.

For Resident Indians

Capital gains on GIFT City investments (UDRs or feeder funds) are taxed in India:

- LTCG: 12.5% (without indexation) — applicable after the relevant holding period

- STCG: As per income tax slab — for shorter holding periods

- Holding period classification for NSE IFSC UDRs should be confirmed with a tax adviser, as these are not domestic listed securities

On dividends: US withholding tax of 25% applies at source per the India-US DTAA (15% for certain qualifying corporate holders). Resident Indians can claim a foreign tax credit under DTAA to offset the US withholding tax against their Indian tax liability.

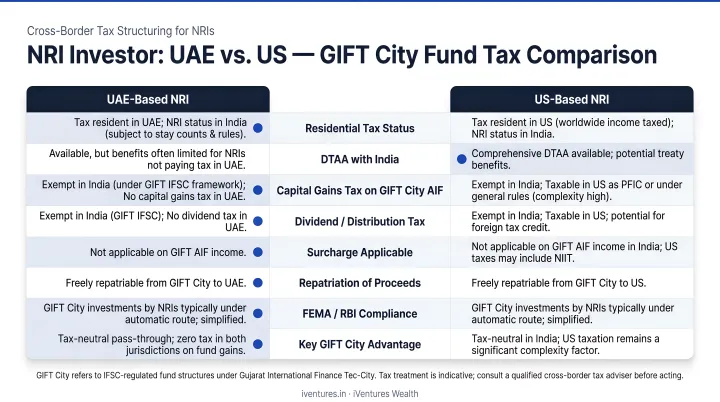

For NRIs

NRIs investing through qualifying GIFT City structures face a different — and in some cases more efficient — tax picture.

When investing through a GIFT City fund structure (Category III AIF meeting specified conditions), non-residents may qualify for an exemption from filing Indian tax returns on that income under Section 10(4D) of the Income Tax Act. The fund handles Indian tax obligations at the fund level; the NRI investor files only in their country of residence.

A practical illustration:

- An NRI in the UAE (no personal capital gains tax) investing via a qualifying GIFT City fund may only bear the fund-level Indian tax

- An NRI in the US would owe the differential between what was paid at the fund level in India and the applicable US rate

This conditional exemption does not apply to all GIFT City structures — the specific fund category and compliance conditions matter. iVentures Wealth coordinates DTAA structuring and cross-border tax mapping for NRI clients, working alongside their tax counsel to clarify fund-level versus investor-level obligations.

Note: Tax rules are subject to budget changes. Consult a tax adviser before making any GIFT City investment decisions.

Common Mistakes to Avoid

Assuming GIFT City Is Tax-Free

The "no GST on management fees" benefit gets misreported as a blanket tax exemption. Resident Indians owe Indian capital gains tax. NRIs file in their country of residence. Assuming otherwise leads to material planning errors.

Using the Wrong Vehicle for Your Ticket Size

- UDRs on NSE-IX — suitable for direct access with smaller amounts; fractional structure keeps entry accessible

- Feeder funds — suited for mid-to-large investors wanting managed exposure; check fund-specific minimums

- AIFs — Restricted Schemes require US$150,000 minimum; better suited to UHNIs and family offices with larger global allocations

Ignoring LRS Limits and TCS Impact

Resident Indians who don't track cumulative LRS usage across all purposes — education, travel, investments — risk breaching the $250,000 annual cap. The 20% TCS on amounts above ₹10 lakhs is recoverable against final tax liability but temporarily reduces the capital you can deploy.

A subtler mistake is defaulting to a direct US broker without evaluating whether GIFT City suits your situation better. The platform offers structural advantages in specific cases:

When GIFT City Makes More Sense Than a Direct US Broker

- Domestic international mutual fund schemes are closed to fresh lump-sum inflows

- You're an NRI wanting a single IFSCA-regulated platform for both India and global assets, with USD-denominated reporting

- You value demat-based holding security — UDRs sit in your own demat account, unlike the broker pool structures used by most US-facing platforms

- You need DTAA-efficient structuring as part of a broader cross-border portfolio

A SEBI-registered investment adviser can assess which route fits your residency, portfolio size, and tax profile — then position GIFT City as one piece of a coordinated global strategy rather than a standalone product decision.

Frequently Asked Questions

What is GIFT City trading?

GIFT City trading refers to financial transactions conducted through exchanges and regulated entities within GIFT City's IFSC: buying and selling securities, currencies, and other instruments. Though physically located in India, it functions as an offshore jurisdiction regulated by IFSCA, separate from domestic Indian capital markets.

Is it good to invest in GIFT City?

GIFT City is a credible avenue for regulated access to global markets, currency diversification, and US equities. Suitability depends on your ticket size, tax residency, and whether you want direct stock ownership or managed exposure. It's particularly useful when domestic international schemes are restricted.

Who are the big 4 in GIFT City?

"Big 4" is informal shorthand — no official designation exists. In practice, the dominant global banks operating in GIFT City include JP Morgan, Deutsche Bank, HSBC, and Standard Chartered. Domestic AMCs and global family offices are also establishing a presence, making it an active hub for both inbound and outbound capital flows.

What is the minimum amount to invest in US stocks via GIFT City?

Through UDRs on NSE-IX, fractional ratios of 1:100 relative to the underlying share value make even high-priced stocks accessible. For feeder funds and AIFs, minimums range from US$10,000 (certain retail schemes) to US$150,000+ for Restricted Schemes and AIFs.

Do I need a separate demat account for GIFT City?

Yes. A separate GIFT City demat account with an IFSCA-registered depository participant is required. Your existing domestic demat account cannot be used for GIFT City investments. Additional documentation including Form W-8BEN is required during account opening.

Is investing in US stocks via GIFT City tax-free for Indian residents?

No. Resident Indians owe Indian capital gains tax — LTCG at 12.5% after the applicable holding period, STCG as per income tax slab for shorter holds. The tax benefit is GST zero-rating on services to SEZ units for authorised operations, not exemption from capital gains on investment profits.