Introduction

Most CFOs and business owners know interest rates matter — but treating them as a number the bank hands you is a costly oversight. Whether your company is drawing on a working capital line, pricing a bond issue, or deciding whether a new plant makes financial sense, interest rates sit at the heart of every calculation.

The rate environment in India has shifted significantly in recent years. The RBI's repo rate climbed from 4.40% in May 2022 to 6.50% by February 2023, then eased to 5.50% by June 2025 — a full 200 basis points of easing that has direct consequences for corporate borrowing costs, investment thresholds, and portfolio positioning.

What follows is a practical breakdown — from the mechanics of rate types to how Indian corporates and investors can position themselves across rate cycles.

Key Takeaways

- Interest rates are the price of borrowed capital — they directly affect every corporate finance decision, from debt issuance to project appraisal

- Each rate type — fixed, floating, nominal, or real — has distinct implications for cash flow predictability and financial planning

- The RBI's repo rate, inflation, and credit demand are the three primary drivers of borrowing costs in India

- Rising rates compress investment returns and strain leveraged balance sheets; falling rates do the opposite

- Tracking RBI rate cycles allows corporates and investors to time debt structuring and position fixed income portfolios more effectively

What Are Interest Rates in Corporate Finance?

In corporate finance, the interest rate is the contractual cost of debt capital — expressed as a percentage of the principal, typically annualised. For a business, this applies to bank loans, working capital facilities, bonds, debentures, and lease financing.

Interest rates carry a dual nature worth understanding:

- For borrowers (corporations): it is the cost of debt — the price paid for using someone else's capital

- For lenders and investors: it is the return on capital deployed

This duality makes interest rates central to investment appraisal, DCF valuation, and portfolio construction simultaneously.

Rates are almost always stated on an annual basis, even when applied monthly or quarterly. A rate quoted monthly must be correctly annualised before comparing loan products or evaluating fixed-income yields — otherwise, the comparison produces distorted results.

Interest rates are also proportional to risk. Lenders charge higher rates to borrowers with weaker credit profiles, shorter operating histories, or more volatile cash flows.

CRISIL's January 2025 data puts a number to this: a 10-year AAA-rated PSU bond yielded 7.18%, with AAA issuances accounting for 73.8% of the market. Lower-rated issuers face meaningfully wider spreads — which means a corporate's credit profile directly determines its cost of capital, and by extension, its investment feasibility.

Types of Interest Rates Corporate Finance Teams Should Know

Not all interest rates behave the same way. The type embedded in a loan agreement or bond structure determines how cash outflows are calculated and where risk sits between borrower and lender.

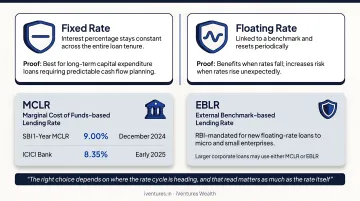

Fixed vs. Floating Interest Rates

Fixed rates keep the interest percentage constant across the entire loan tenure. This gives businesses predictable debt servicing costs — valuable for long-term capital expenditure loans where cash flow planning requires certainty.

Floating (variable) rates are linked to a benchmark and reset periodically. In India, two benchmarks matter most:

- MCLR (Marginal Cost of Funds-based Lending Rate): SBI's one-year MCLR stood at 9.00% as of December 2024; ICICI Bank's was 8.35% as of early 2025

- EBLR (External Benchmark-based Lending Rate): RBI mandates external benchmarks for new floating-rate loans to micro and small enterprises; larger corporate loans may use either MCLR or EBLR

Floating rates benefit borrowers when rates are expected to fall, but increase financial risk when rates rise unexpectedly. The right choice depends on where the rate cycle is heading — and that read matters as much as the rate itself.

Simple vs. Compound Interest

Simple interest is calculated only on the original principal:

SI = P × R × T

If a company borrows ₹1 crore at 9% for 2 years, simple interest = ₹18 lakhs. Common in short-term trade finance or bridge loans.

Compound interest is calculated on the principal plus accumulated interest from prior periods:

A = P(1 + r/n)^(nt)

At the same 9% over 2 years with annual compounding, the total interest is approximately ₹18.81 lakhs — a difference that becomes material over longer tenures. Relevant for corporate bonds, fixed deposits, and long-term debentures.

Nominal vs. Real Interest Rates

The nominal rate is what's stated on a loan document. The real rate adjusts for inflation:

Real rate ≈ Nominal rate − Expected inflation

If a company borrows at 8% nominal while inflation runs at 5%, its real borrowing cost is only 3%. RBI's 2024-25 Annual Report pegs average CPI inflation at 4.6% for FY2024-25. That figure changes the calculus: debt that looks expensive at 8% nominal may be comparatively cheap once purchasing power is factored in.

How Interest Rates Shape Corporate Finance Decisions

Rate movements ripple through every major corporate finance function — from how cheaply a company funds growth to how attractive its equity looks to investors.

Cost of Borrowing and Debt Management

When interest rates rise, the cost of new debt increases directly:

- Higher EMIs on working capital loans

- Costlier coupon payments on new bond issuances

- Elevated refinancing risk for existing floating-rate debt

For leveraged companies — those with high debt-to-equity ratios — even a modest rate increase can materially compress net profit margins. The reverse is equally true: falling rates reduce interest burden and free cash flow for reinvestment.

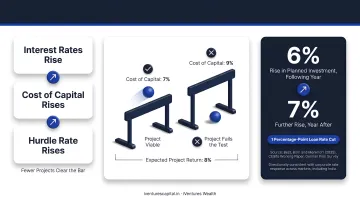

Capital Investment and Project Viability

The hurdle rate is the minimum return a project must clear to be worth pursuing. It moves with the cost of capital — which moves with interest rates.

When rates rise, the hurdle rate rises too. Projects that looked viable at 7% cost of capital may fail the test at 9%. When rates fall, previously marginal investments in capacity, R&D, or acquisitions become worth pursuing again.

Evidence from a 2025 CESifo working paper by Best, Born and Menkhoff using a German firm survey found that a 1 percentage-point loan rate cut raises planned investment by approximately 6% in the subsequent year and another 7% the year after. The study uses a German context and the magnitudes won't transfer directly to India — but the directional finding aligns clearly with how corporates respond to rate changes across markets.

Bond Prices, Equity Valuations, and Capital Markets

Two inverse relationships define how rates affect capital markets:

Bonds: When market rates rise, existing bonds with lower coupons become less attractive — their prices fall. When rates fall, bond prices rise. For corporates timing debt raises through the capital markets, this matters significantly.

Equities: Higher discount rates (driven by higher interest rates) reduce the present value of future cash flows in DCF models, putting downward pressure on stock valuations. This affects decisions around equity fundraising, IPOs, and share buybacks. Growth-oriented companies — where valuations depend heavily on distant future cash flows — feel this most acutely.

Debt Servicing and Cash Flow Pressure

For companies carrying existing floating-rate debt, rising rates directly increase monthly interest outflows with no immediate revenue offset. This is particularly acute for SMEs and mid-market companies that depend heavily on bank credit for working capital.

One practical response: ensure surplus cash is deployed — in liquid funds, overnight funds, or short-duration debt instruments — rather than sitting idle while interest costs compound on the borrowing side of the balance sheet.

Key Factors That Influence Interest Rates in India

The RBI and Monetary Policy

The RBI's Monetary Policy Committee (MPC) — six members, three from RBI and three appointed by the Central Government — sets the repo rate, the benchmark at which RBI lends to commercial banks. Its statutory CPI target is 4% with a ±2 percentage point tolerance band.

The repo rate trajectory since 2022 charts India's rate cycle since 2022:

| Period | Repo Rate |

|---|---|

| May 2022 | 4.40% |

| February 2023 – December 2024 | 6.50% (peak) |

| February 2025 | 6.25% |

| April 2025 | 6.00% |

| June–October 2025 | 5.50% |

These changes cascade into MCLR adjustments, raising or lowering corporate loan costs across Indian banks. The primary force driving those rate decisions is inflation — which is why CPI data matters as much to CFOs as it does to central bankers.

Inflation

Higher CPI inflation compels the RBI to raise rates to protect purchasing power. Lower inflation allows rate cuts to stimulate activity. India's CPI averaged 4.6% in FY2024-25 — within the tolerance band and a key factor behind the subsequent easing cycle.

For corporate borrowers, tracking CPI trends helps anticipate rate moves before they hit loan repricing cycles — giving treasury teams a window to lock in fixed rates or defer variable-rate drawdowns.

Credit Demand, Liquidity, and Capital Flows

Inflation and policy rates don't operate in isolation. Several structural and flow-based factors also shape where rates settle:

- Credit demand: During infrastructure booms or pre-election cycles, rising credit demand firms up rates; excess bank liquidity eases them

- Government borrowing: Central government gross market borrowing was approximately ₹14.01 lakh crore in 2024-25, influencing sovereign yields

- Foreign capital flows: India recorded US$17.4 billion of FPI debt inflows in 2024-25, partly driven by Indian government bonds' index inclusion — a demand-side factor that helps contain sovereign yields

Interest Rates, WACC, and Capital Structure Decisions

Understanding WACC

The Weighted Average Cost of Capital (WACC) is the blended cost a company pays for all its capital, weighted by its usage:

WACC = (E/V × Re) + (D/V × Rd × (1 − T))

Since the cost of debt (Rd) is directly tied to prevailing interest rates, rising rates increase WACC — which raises the return threshold for every capital investment the business considers.

The Debt-Equity Trade-Off Across Rate Cycles

- Low-rate environments: Debt financing becomes attractive. Cheap leverage can amplify returns on equity without excessive interest burden

- High-rate environments: Expensive debt pushes companies toward equity financing — but equity dilutes existing shareholders

Corporate finance teams must optimise this mix dynamically as the rate cycle evolves, rather than locking in a static capital structure.

The Tax Shield Advantage

That debt-equity balance also depends on how tax treatment affects the real cost of borrowing. Interest payments are tax-deductible for Indian corporates, which partially offsets the nominal borrowing cost. Under the Section 115BAA regime (base rate 22%, plus 10% surcharge and 4% cess), the effective tax rate is approximately 25.17%.

A practical illustration: if a company borrows at 9%, the after-tax cost of debt is:

9% × (1 − 0.2517) = approximately 6.73%

For a CFO weighing debt against equity, this 230-basis-point reduction matters — especially in moderate-rate environments where the headline borrowing cost alone might appear unattractive.

How Corporates and Investors Can Navigate Interest Rate Cycles

Rate Cycle Positioning for Corporates

In a rising rate environment:

- Lock in fixed-rate debt before further hikes

- Refinance floating-rate obligations where possible and economical

- Reduce unnecessary leverage to limit interest exposure

- Deploy surplus cash into short-duration instruments to capture rising yields

In a falling rate environment (like the current cycle):

- Consider switching to floating-rate structures to benefit from declining benchmarks

- Evaluate refinancing high-cost legacy debt with lower-rate facilities

- Capture the window to lock in private credit yields before they compress further

iVentures Wealth's corporate treasury advisory covers this full scope for promoter-led businesses, family enterprises, and SMEs with assets above ₹50 crores: refinancing strategy, tenor matching, lender negotiation, and capital structure optimisation. As a SEBI-registered, product-neutral advisor (INA000019026), every recommendation is governed by what serves the client's balance sheet — independent of lender relationships.

Portfolio Positioning for UHNI Investors

Interest rate shifts affect fixed income, equities, and real estate yields simultaneously. A practical framework:

| Rate Environment | What Typically Benefits |

|---|---|

| Rising rates | Short-duration bonds, floating-rate funds, banking sector equities |

| Falling rates | Long-duration gilts, dynamic bond funds, growth equities |

| Current easing cycle | Private credit AIFs (13–16% contractual yields), gilt funds for duration play |

For UHNIs in high tax brackets, private credit AIFs deserve particular attention in the current easing cycle — they offer contractual yields well above FD rates before the full easing plays out, with quarterly distributions and secured collateral structures.

Proactive Monitoring

Interest rate risk is not solely a treasury concern. It touches valuation, fundraising strategy, and investor returns across the board. Working with a SEBI-registered investment adviser to model rate scenarios on your debt portfolio and capital allocation — before rates move, not after — is what separates structured financial decision-making from reactive damage control.

Frequently Asked Questions

What is investment in corporate finance?

In corporate finance, investment refers to allocating capital toward assets, projects, or securities with the expectation of future returns. This includes capital expenditure, financial investments in bonds or equities, and working capital deployment — each evaluated against the cost of capital.

What is the Rule of 72 in finance?

The Rule of 72 estimates how long an investment takes to double: divide 72 by the annual interest rate. At 8% per annum, an investment doubles in approximately 9 years (72 ÷ 8). A practical mental shortcut — precise enough for quick comparisons across investment options.

Is 1% per month the same as 12% per annum?

No — not when compounding is involved. Simple interest gives 12% annually, but with monthly compounding, the effective annual rate (EAR) is (1.01)^12 − 1 = approximately 12.68%. This gap matters when evaluating loan costs or short-tenure financing where compounding frequency directly affects total repayment.

How do rising interest rates affect a company's stock price?

Rising rates pressure stock prices through two channels: higher discount rates reduce the present value of future earnings in DCF models, and higher borrowing costs compress profit margins for debt-dependent companies. Growth and technology stocks are most sensitive because their valuations depend heavily on cash flows discounted over long periods.

What is the difference between fixed and floating interest rates on corporate loans?

Fixed rates stay constant for the entire loan tenure, providing cash flow certainty. Floating rates are linked to a benchmark like the repo rate or MCLR and reset periodically — beneficial when rates fall, but a risk when they rise. Companies seeking predictable outflows prefer fixed; those expecting an easing cycle often favour floating.

How does the RBI repo rate affect corporate borrowing costs in India?

The repo rate is the benchmark at which RBI lends to commercial banks. When RBI raises it, banks' funding costs rise, which flows through to higher MCLR-linked corporate loan rates. A repo rate cut does the opposite — reducing borrowing costs for businesses across India and stimulating corporate credit demand and investment activity.