The numbers reflect how common this situation is. According to IndiaSpend's analysis of Census data, India had 71.4 million single women in 2011 — a 39% rise over the preceding decade. And globally, nearly 40% of women over 35 regret not investing for retirement sooner, according to Fidelity research cited by CNBC. The regret is predictable. The planning doesn't have to wait.

This guide covers seven financial planning strategies tailored specifically to single women in India — from building a financial foundation and investing smartly, to planning for retirement, protection, and estate transfer.

Key Takeaways

- Build an emergency fund covering 6–9 months of essential expenses — the higher end matters when there's no backup income

- Start SIPs early — equity mutual funds and ELSS are among the most accessible wealth-building tools for consistent, long-term growth

- Retirement planning must account for longer life expectancy and no partner's pension, so your corpus needs to be built larger and earlier

- Health insurance and critical illness cover are non-negotiable when you're your own financial backup

- A will and updated nominations are essential; without them, default succession laws determine who inherits your assets

Why Financial Planning Looks Different for Single Women

The Sole Decision-Maker Reality

Every financial decision — from choosing a home loan to deciding when to retire — falls entirely on one income and one person's judgment. There's no second salary during a job change, no partner's EPF balance in reserve. Economists call this the "singles cost": single individuals typically pay more per person for housing, utilities, and insurance than dual-income households.

The longevity factor compounds this. World Bank data for 2022 shows female life expectancy in India at approximately 70.5 years versus 67.1 years for men. For single women, those extra years must be funded entirely from a self-built corpus — no partner's pension, no shared household to reduce costs.

Structural Challenges Worth Naming

Indian working women face specific headwinds that make deliberate planning critical:

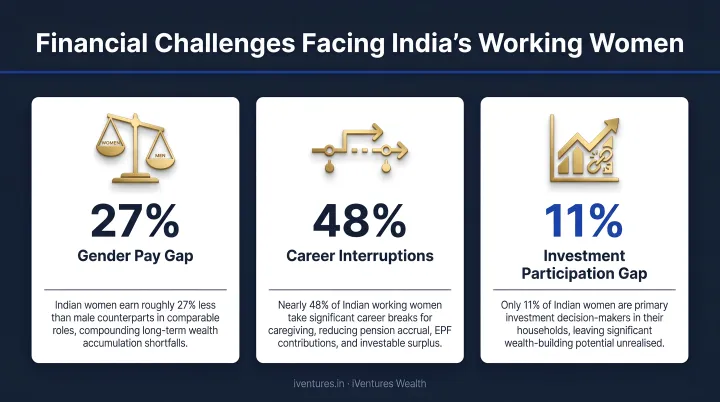

- Earnings lag from the start — PLFS 2023-24 data shows men in regular salaried roles averaging ₹22,375/month versus ₹17,034 for women, a gap that widens significantly across a full savings career

- Caregiving forces career interruptions for a majority — 57% of women job aspirants in one Kerala survey cited this as their primary reason for stepping out of the workforce

- Investment awareness trails at 58% among women versus 66% among men, per the SEBI Investor Survey 2025 — and only 8.5% of Indian households hold any securities-market products at all

Each of these gaps is closeable — but closing them requires an intentional strategy, not a default one.

Build Your Financial Foundation: Budgeting, Emergency Fund, and Debt

Choose a Budgeting Framework That Works for You

A budget gives you control over where your money goes — not the other way around. Three frameworks work well for single women, depending on where you are financially:

| Framework | Split | Best For |

|---|---|---|

| 50-30-20 Rule | 50% needs / 30% wants / 20% savings & investments | Starting out; straightforward income management |

| 70-20-10 Rule | 70% living expenses / 20% savings & investments / 10% debt or discretionary | Managing existing debt while beginning to invest |

| 70-10-10-10 Rule | 70% expenses / 10% retirement / 10% short-term savings / 10% discretionary | Disciplined multi-goal planning on a single income |

On a single income, consider pushing the savings allocation to 25–30% wherever possible — there's no second salary to fall back on.

Emergency Fund: Go Higher Than the Standard Guideline

The general guidance is 3–6 months of essential expenses. For single women with no partner's income as backup, the target should be the higher end — ideally 6–9 months — held in a liquid, interest-bearing instrument such as a liquid mutual fund or high-yield savings account.

Build this before aggressively investing. Without a buffer, a single job loss or medical event can force you to liquidate investments at the worst possible time.

Tackle High-Interest Debt First

Once your emergency fund reaches a minimum of 3 months, shift focus to clearing high-cost debt before increasing investment contributions:

- Credit card balances (typically 36–42% annual interest)

- Personal loans

- Any informal high-cost borrowing

Debt consolidation — combining multiple liabilities into a single lower-interest loan — reduces both complexity and interest burden. Once high-cost debt is cleared, redirect those EMI amounts directly into investments.

Smart Investment Strategies to Grow Wealth on Your Own Terms

Why Staying in Cash Is a Risk, Not Safety

Keeping money in savings accounts or fixed deposits while inflation runs at 4-6% annually means your purchasing power shrinks every year. For a single woman, investment growth is effectively your closest equivalent to a second income — it's the mechanism that makes your money work alongside you.

Accessible Investment Options in the Indian Context

| Instrument | Best For | Key Feature |

|---|---|---|

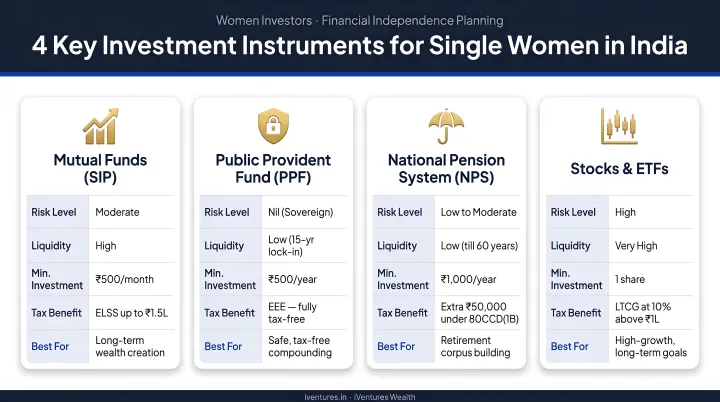

| SIPs in Equity Mutual Funds | Long-term wealth building | Rupee cost averaging; start with ₹500/month |

| ELSS Funds | Tax saving + growth | Deduction under Section 80C (up to ₹1.5 lakh); 3-year lock-in |

| PPF | Risk-free, long-term savings | 7.1% p.a. (subject to revision); 15-year lock-in; tax-exempt returns |

| NPS | Retirement corpus | Additional deduction up to ₹50,000 under Section 80CCD(1B); 40% must go to annuity at exit |

Women's SIP net inflows reached ₹54,495 crore in FY2025, according to AMFI — a clear sign that more women are using systematic investing as a wealth-building tool.

Build a Goal-Based Portfolio, Not a Product Collection

The most common mistake is mixing up investment purposes. A structured approach separates:

- Short-term goal fund (1–3 years): Debt mutual funds, liquid funds — capital preservation matters more than growth

- Medium-term goal fund (3–7 years): Hybrid or balanced advantage funds — suitable for goals like a property down payment or business capital

- Long-term corpus (7+ years): Equity-heavy allocation — retirement, financial independence

This separation prevents one of the most damaging patterns in personal finance — withdrawing long-term investments to meet short-term needs.

Where Expert Guidance Adds Real Value

Building this strategy in isolation is harder than it looks — especially balancing tax efficiency, risk, and timeline across multiple goals on a single income.

For women who have built a meaningful asset base and want to structure it with intent, iVentures Wealth's Investments for HER programme offers dedicated advisory support. Their CFA-led team maps each component of your portfolio to a specific goal, timeline, and required corpus — whether that means consolidating a concentrated real estate position, restructuring fixed income exposure, or building a tax-efficient equity allocation across asset classes.

Retirement Planning When You're Your Own Safety Net

The Longevity Maths

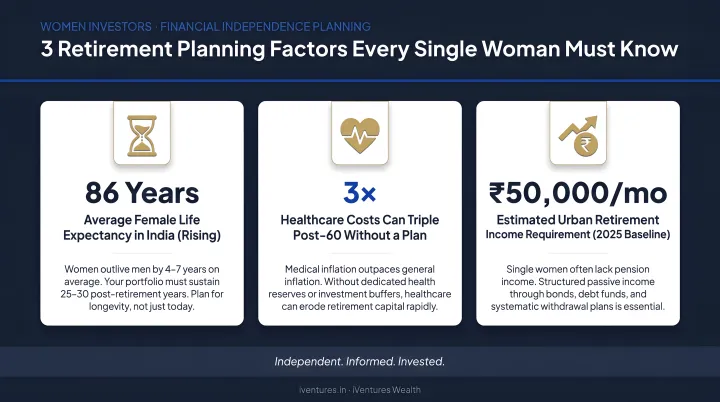

Consider this scenario: retire at 60, live to 82. That's 22 years of expenses, healthcare, and lifestyle to fund — entirely from your own corpus. No partner's EPF, no shared household costs, no supplementary pension. The numbers must work harder for a single woman than for almost any other investor profile.

The commonly cited rule of thumb is accumulating **20–25 times your expected annual retirement expenses**. But for single women, that figure should sit at the higher end, factoring in:

- Healthcare cost inflation: Aon projects India employer medical plan costs rising 11.5% in 2026 — healthcare consistently inflates faster than general CPI

- Solo aging costs: Without a partner, professional care (home nurses, assisted living) becomes a more likely requirement

- No supplementary income sources: Every rupee must come from your own corpus or government instruments

Key Retirement Building Blocks

- EPF: Maximise contributions and avoid premature withdrawals — even a partial early withdrawal significantly erodes compounding

- NPS: Provides a pension-like structure with an additional ₹50,000 tax deduction under Section 80CCD(1B), building corpus with built-in discipline

- SCSS: After 60, the Senior Citizen Savings Scheme offers 8.2% p.a. (subject to revision) with a ₹30 lakh maximum — a practical capital preservation tool

- Equity-debt portfolio: Build the bulk of your corpus here across working years, then shift gradually toward debt as retirement approaches

Starting early is the single most powerful lever. Starting SIPs at 28 versus 35 can translate to 40–50% more corpus at retirement, with no additional effort — just time and compounding doing the work.

For single women, retirement planning isn't a variation on the standard template — it requires its own framework, built around longer timelines, solo healthcare costs, and income streams that don't depend on anyone else.

Insurance and Protection: Safeguarding Your Future Solo

When you are your own financial safety net, a single uninsured health event can erase years of savings. This is not hypothetical — India's out-of-pocket health expenditure stood at 47.1% of total health spending in 2019, meaning most medical costs still land directly on individuals.

Coverage Types Every Single Woman Should Understand

Sound financial planning requires knowing which insurance layers you need — even before selecting specific products. Work with a licensed insurance advisor to evaluate the right policies; your wealth plan should then be structured around these protections.

Key coverage areas to review with your insurance advisor:

- Health insurance (personal policy): Employer cover ends when employment does. A personal policy with ₹10–25 lakh sum assured (depending on city) closes that gap.

- Term life insurance: Relevant if you have financial dependents — parents, siblings — or carry a significant liability like a home loan.

- Critical illness cover: Pays a lump sum on diagnosis of cancer, cardiac events, or kidney failure, bridging the income loss that standard health policies don't cover.

- Disability income insurance: If you cannot work, there is no backup income. Disability cover protects your earning capacity — a risk that's heightened when you're the sole earner.

Plan for Long-Term Care Early

Women aging alone face a statistically higher probability of needing professional care — home nursing, assisted living, or rehabilitation services. These costs are substantial and rarely covered by standard health policies.

The most controllable lever here is building a dedicated healthcare corpus early. Starting a separate investment pool specifically for future care costs — separate from your emergency fund and retirement portfolio — gives you options regardless of what insurance products exist when you need them. This is an area where structured investment planning, started early, makes a meaningful difference.

Estate Planning: Leaving a Legacy That Reflects You

Why This Matters Even Without Dependents

Many single women assume estate planning is irrelevant without a spouse or children. It isn't — it's more important. Under Section 15 of the Hindu Succession Act, 1956, if a Hindu woman dies intestate (without a will), her assets devolve first to children and husband, then to the husband's heirs, then to parents. For a single woman, this means assets could pass to relatives she barely knew, while people she genuinely cared for receive nothing.

A will changes that entirely.

Essential Estate Planning Documents

- Will: Specifies exactly who inherits your assets — parents, siblings, friends, charitable causes — on your own terms

- Updated nominations: Banks, demat accounts, PF, and insurance policies all require separate nominations; nominees are custodians, not legal heirs, but updated nominations avoid disputes

- Power of attorney: Designates someone to manage your financial and medical decisions if you are incapacitated

- Healthcare proxy / advance medical directive: Documents your medical preferences if you cannot communicate them

Getting each of these documents right requires more than intent — it requires legal clarity on how they interact.

iVentures Wealth's estate planning support, offered under their Investments for HER programme, covers this ground directly: drafting legally valid wills, aligning nominations across accounts, and building consolidated asset listings so your wishes are on record and legally enforceable. In one client case, joint holdings and nominations had been assumed sufficient; iVentures identified the legal gaps and restructured the documentation so assets transferred as intended.

The freedom in estate planning for single women is real. Without the complexity of dividing assets between a spouse and children, you can direct your wealth precisely — to people and causes that reflect your values.

Frequently Asked Questions

How to survive financially as a single woman?

Start with an emergency fund covering 6–9 months of essential expenses, then budget using a framework like the 50-30-20 or 70-20-10 rule. Invest consistently in goal-aligned instruments — SIPs, ELSS, PPF — and prioritise health and critical illness coverage. Review your plan annually as income and goals evolve.

What is the 70-10-10-10 rule for money?

The 70-10-10-10 rule splits income into 70% for living expenses, 10% for long-term savings or retirement, 10% for short-term savings or emergency funds, and 10% for discretionary spending or giving. For single women managing multiple goals on one income, this structured split helps prevent any single priority from being neglected.

What is the 70/20/10 rule for money?

The 70/20/10 rule directs 70% of income to everyday needs, 20% to savings and investments, and 10% to debt repayment or donations. Single women without a second income may benefit from pushing the savings slice to 25–30% once high-interest debt is cleared.

How much should a single woman save for retirement in India?

Aim to accumulate at least 25 times your expected annual retirement expenses — the higher end of the standard range. Single women should also account for above-average healthcare costs, a longer post-retirement horizon, and the absence of a partner's pension or EPF to supplement the corpus.

Do single women need life insurance in India?

Life insurance is most critical when others depend on your income — parents, siblings, or anyone you support financially. Single women without dependents may prioritise health and critical illness coverage first, but a term plan remains advisable if you carry significant financial liabilities such as a home loan.

What is the best investment for a single working woman in India?

A combination approach works best: SIPs in diversified equity mutual funds for long-term growth, ELSS for tax-saving under Section 80C, PPF for stable long-term returns, and NPS for retirement income. The right mix depends on your age, income, and risk tolerance — a SEBI-registered adviser can help tailor the allocation to your specific goals.