Introduction

A salary is one of the most predictable income streams available — yet according to PGIM India's Retirement Readiness Survey 2025, only 37% of Indian salaried professionals had a retirement plan in 2025, down sharply from 67% in 2023. The same survey found households now allocate 65% of income to monthly expenses, up from 59% two years prior.

The gap between earning well and building wealth is real — and it widens every year you delay.

2026 adds fresh urgency. The new tax regime is now the default, with revised slabs and a ₹75,000 standard deduction. Cost of living continues rising. And expanded NPS benefits have shifted what optimal planning looks like.

This guide covers what matters most for salaried employees in 2026:

- Five practical steps for financial planning

- Budgeting frameworks built for Indian salaries

- 2026 tax-saving strategies under the new regime

- Emergency fund benchmarks

- Investment basics for long-term wealth building

Key Takeaways

- Follow a structured 5-step process: assess, budget, save, invest, and review

- Use the 50/30/20 or 70-10-10-10 rule to allocate take-home salary deliberately

- Choose between the old and new tax regimes before the financial year begins — it defines your 2026 tax liability

- Build 3–6 months of expenses as an emergency fund; insurance coverage is the floor beneath every plan

- SIPs, EPF, and NPS build long-term corpus while keeping entry simple for salaried professionals

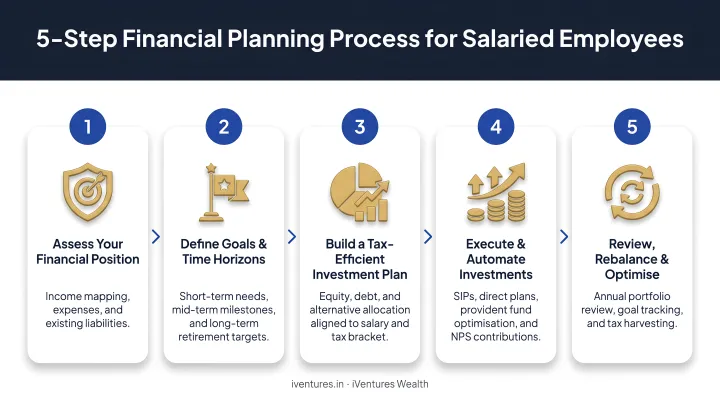

The 5 Steps of Financial Planning for Salaried Employees

Step 1: Assess Your Current Financial Position

Before any plan, you need a clear snapshot. Most employees skip this and jump straight to picking investments — that's how portfolios end up scattered across random FDs and forgotten SIPs.

Document the following:

- Income: In-hand monthly salary, expected bonus, any side income

- Assets: EPF balance, savings account balance, existing mutual funds, fixed deposits

- Liabilities: Outstanding EMIs (home loan, car loan, personal loan), credit card dues

- Monthly expenses: Fixed (rent, EMIs, insurance premiums) vs. variable (groceries, dining, subscriptions)

This one-page financial snapshot is the starting point for every decision that follows.

Step 2: Define Goals With Numbers and Timelines

Vague goals don't get funded. Attach a ₹ amount and a target date to each:

| Goal Type | Example | Timeline |

|---|---|---|

| Short-term | Emergency fund of ₹3 lakh | 0–2 years |

| Medium-term | Home down payment of ₹20 lakh | 3–7 years |

| Long-term | Retirement corpus of ₹2–3 crore | 20–30 years |

Only 48% of Indian professionals surveyed by PGIM knew the corpus they'd need for retirement — with the average target cited at just ₹74 lakh, well below the ₹2–3 crore most planners recommend for a comfortable retirement.

Step 3: Create and Follow a Budget

A budget is not a restriction — it's the operating system for your finances. Without one, spending expands to fill income. Specific frameworks are covered in the next section, but the core principle is simple: decide where your money goes before it arrives.

Step 4: Build a Goal-Linked Savings and Investment Plan

Once a budget creates a monthly surplus, direct it toward specific goals — not a default savings account. Leaving it idle earning 3–4% while inflation runs above that is effectively a wealth leak.

Link each investment to a specific goal:

- Emergency fund → liquid mutual fund or high-interest savings account

- Medium-term goals → debt funds or balanced allocation

- Long-term goals → equity SIPs, EPF top-ups, NPS contributions

Step 5: Review, Adjust, and Protect

A financial plan created once and never revisited is no plan at all. Review annually — and immediately after major life events:

- Marriage, divorce, or a new child

- A significant salary hike or job change

- Inheritance or a large one-time cash inflow

Protection matters equally. Insurance doesn't build wealth, but a single health event or death can dismantle everything you've built without it. Treat adequate term and health cover as a non-negotiable foundation, not an afterthought.

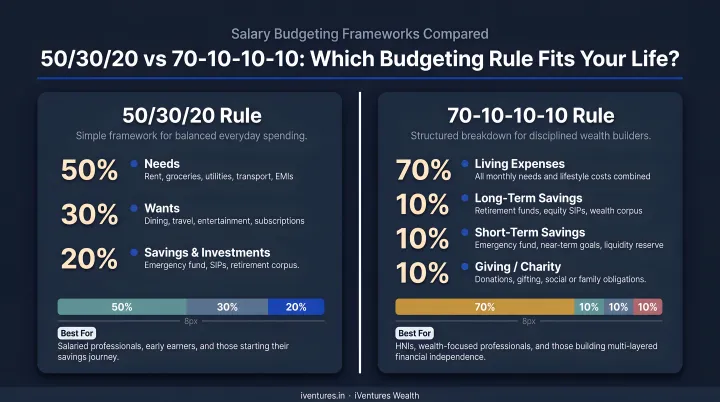

Budgeting Rules Every Salaried Employee Should Know in 2026

The 50/30/20 Rule

Allocate take-home salary into three buckets:

- 50% → Needs: rent, groceries, EMIs, utilities

- 30% → Wants: dining, entertainment, travel

- 20% → Savings and investments

Illustration — ₹80,000/month take-home salary:

| Category | Percentage | Amount |

|---|---|---|

| Needs | 50% | ₹40,000 |

| Wants | 30% | ₹24,000 |

| Savings/Investments | 20% | ₹16,000 |

This framework works well for mid-career employees with moderate fixed obligations.

The 70-10-10-10 Rule

Better suited to those starting out or carrying higher fixed costs:

- 70% → All living expenses (fixed + variable)

- 10% → Savings (emergency fund, liquid instruments)

- 10% → Investments (SIPs, NPS, EPF top-up)

- 10% → Discretionary or charitable goals

Pay Yourself First

The most reliable way to build savings is automation. Set up an auto-debit SIP or EPF voluntary contribution to execute on salary day — before discretionary spending begins. Once that transfer clears, sizing your emergency reserve becomes the natural next step.

The 3-6-9 Emergency Benchmark

Emergency fund sizing depends on your situation:

- 3 months of expenses: No dependents, stable government/PSU employment

- 6 months: Family with dependents, private sector employment

- Up to 9 months: Variable income, IT sector, startup environment, or single-income household

Track Before You Choose a Rule

Before committing to any framework, track all expenses for one month — using an expense-tracking app or spreadsheet. Most employees find 10–15% of their spending is absorbed by subscriptions and impulse purchases that deliver little value. Fix the leakage before picking the percentage.

Tax Planning Tips for Salaried Employees in 2026

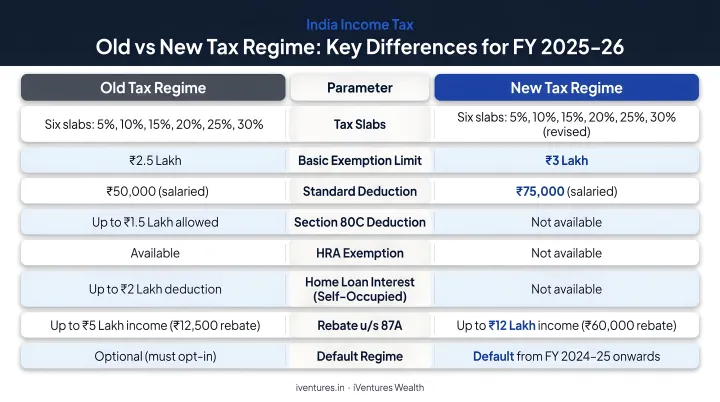

Old vs. New Tax Regime: The Decision You Must Make

The new tax regime is now the default for salaried taxpayers under FY 2025-26 / AY 2026-27. If you don't actively choose the old regime, TDS is calculated under the new regime automatically. Getting this wrong means overpaying TDS for the entire year with no way to recover it mid-year.

FY 2025-26 Tax Slabs — Side by Side:

| Income Range | Old Regime | New Regime |

|---|---|---|

| Up to ₹2.5 lakh | Nil | — |

| Up to ₹4 lakh | — | Nil |

| ₹2.5–5 lakh | 5% | — |

| ₹4–8 lakh | — | 5% |

| ₹5–10 lakh | 20% | — |

| ₹8–12 lakh | — | 10% |

| Above ₹10 lakh | 30% | — |

| ₹12–16 lakh | — | 15% |

| ₹16–20 lakh | — | 20% |

| ₹20–24 lakh | — | 25% |

| Above ₹24 lakh | — | 30% |

Key differences:

- New regime: ₹75,000 standard deduction; Section 87A rebate up to ₹60,000 for income up to ₹12 lakh

- Old regime: ₹50,000 standard deduction; most deductions (80C, 80D, HRA) apply

- The old regime is typically more beneficial when total deductions exceed ₹3–4 lakh annually

Inform your employer of your regime choice early — otherwise TDS defaults to the new regime.

Section 80C: Maximise the ₹1.5 Lakh Deduction (Old Regime)

The 80C limit remains unchanged at ₹1,50,000. Commonly used instruments:

- EPF employee contribution (automatic)

- ELSS mutual funds (shortest lock-in: 3 years)

- PPF contributions

- Life insurance premiums

- Home loan principal repayment

ELSS deserves priority once EPF contributions are accounted for: the 3-year lock-in is the shortest among 80C instruments, and equity exposure gives it the highest return potential in the category.

Section 80D: Health Insurance Premium Deduction

- Up to ₹25,000: Premiums for self, spouse, and children

- Up to ₹50,000: Additional deduction for senior citizen parents

This deduction reduces your tax liability while securing health coverage. Most employees with senior citizen parents can claim ₹75,000 total — a meaningful reduction that's easy to overlook.

HRA Exemption: How It's Calculated

HRA exemption is the least of these three amounts:

- Actual HRA received from employer

- Rent paid minus 10% of salary (basic + DA)

- 50% of salary if in Delhi, Mumbai, Kolkata, or Chennai; 40% elsewhere

Example: Basic salary ₹40,000/month, HRA ₹20,000/month, rent paid ₹18,000/month (Delhi):

- Actual HRA: ₹20,000

- Rent – 10% of salary: ₹18,000 – ₹4,000 = ₹14,000

- 50% of salary: ₹20,000

Exempt amount: ₹14,000/month (the lowest of the three)

Employees with home loans can separately claim Section 24(b) deductions on home loan interest: up to ₹2,00,000 annually for self-occupied property.

NPS: Extra ₹50,000 Deduction Under Section 80CCD(1B)

NPS contributions under Section 80CCD(1B) give you an additional ₹50,000 deduction beyond the ₹1.5 lakh 80C ceiling, bringing combined deductions from these two sections to ₹2 lakh — but only under the old regime.

Under the new regime, employer NPS contributions under Section 80CCD(2) remain deductible, up to 14% of salary. This makes employer NPS one of the few substantive deductions that survives under the new regime.

Building Your Financial Safety Net

Emergency Fund Basics

Before investing in equity or locking money into long-term instruments, build a liquid buffer. Most financial planners recommend 3 to 6 months of household expenses as a baseline — and closer to 12 months if your income is variable, you're in a senior role with longer re-employment timelines, or you're supporting dependents on a single salary.

Park this in:

- Liquid mutual funds (T+1 redemption, better returns than savings account)

- High-interest savings accounts

Avoid: Equity funds, long-term FDs, or any instrument with lock-in or capital risk.

Life Insurance: Term Cover, Not Investment Plans

A pure term insurance plan is the right tool for income replacement — not ULIPs or endowment plans. Those blend insurance with investment inefficiently and at high cost.

Standard rule of thumb: coverage of at least 10–15x annual income. For a salaried employee earning ₹12 lakh per year, that means a ₹1.2–1.8 crore term cover. Premiums also qualify for deduction under Section 80C.

Health Insurance: Don't Rely Solely on Employer Cover

India's out-of-pocket health expenditure reached ₹3,56,254 crore in FY 2021-22, representing 39.4% of total health expenditure. Medical inflation ran at 12% in 2024 and was projected at 13% for 2025, according to Milliman.

Employer group health insurance terminates on your last working day. This creates real gaps:

- Job transitions: You're uninsured between your last day and the new employer's policy activation

- Medical emergencies during gaps: Any hospitalisation in that window is fully out of pocket

- Career breaks or voluntary exits: Leaving employment means losing cover entirely

A personal health insurance policy in your own name ensures continuity, regardless of what happens at work.

Investment and Retirement Planning on a Salary

Start With What You Already Have: EPF

Most salaried employees underestimate EPF as a wealth-building tool. Both employer and employee contribute 12% of basic salary, with the employee's full 12% going into EPF. The EPF interest rate for FY 2024-25 is 8.25%, compounding annually with zero market risk and full government backing.

For a mid-career employee, this is often the largest single financial asset they hold — yet most never track its balance or project its compounding trajectory. Use EPFO's official EPF calculator at epfindia.gov.in to run a projection based on your current balance and expected salary growth.

Layer SIPs for Goal-Linked Investing

Systematic Investment Plans in equity mutual funds are the most accessible entry point for long-term wealth creation. The mechanics:

- Fixed monthly amount invested regardless of market level

- Rupee cost averaging reduces timing risk

- Compounding works more powerfully over longer horizons

To estimate how a monthly SIP of ₹10,000 grows over 15–20 years at various return assumptions, use the Mutual Funds Sahi Hai SIP calculator. Note that mutual funds do not offer fixed returns — avoid any projection based on unverified average return claims.

A practical habit: increase your SIP amount by 10% with every annual salary increment. This step-up approach significantly accelerates the long-term corpus without feeling like a sacrifice.

That SIP discipline compounds even further when started early. Here's the math.

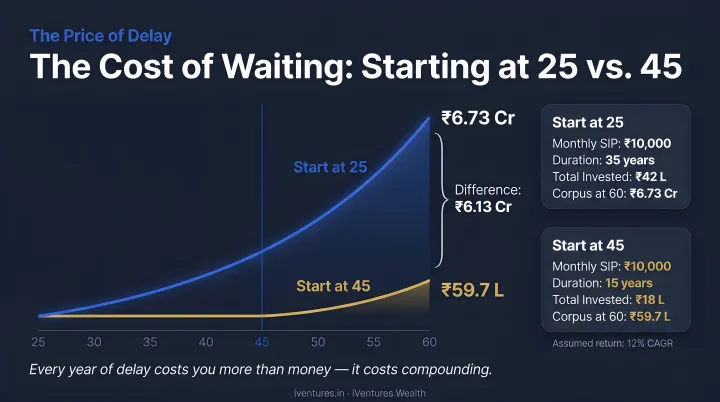

Start Early: The Cost of Delay Is Measurable

According to a PFRDA retirement education illustration using a 10% assumed return and retirement at age 60:

| Starting Age | Monthly Contribution | Estimated Corpus |

|---|---|---|

| 25 | ₹2,236 | ₹85 lakh |

| 30 | ₹2,942 | ₹67 lakh |

| 45 | ₹7,720 | ₹32 lakh |

Starting at 25 versus 45 means contributing less than a third the monthly amount to build nearly three times the corpus. Every year of delay is compounding you no longer get back.

Diversify as Income Grows

Early career: EPF + equity SIPs is sufficient.

As income scales, add layers:

- Debt funds: liquidity management, capital preservation for 1–3 year goals

- NPS: tax efficiency plus retirement corpus

- Direct equities or ETFs: for investors who develop market knowledge

- PMS or AIFs: appropriate only at higher wealth levels, typically ₹50 lakh+

As portfolios grow more complex — multiple instruments, significant EPF balances, ESOP grants, variable pay — structured guidance becomes genuinely useful. For professionals who reach that stage, a SEBI-registered investment adviser operating on a fee-only model ensures recommendations are never driven by product commissions. iVentures Wealth (Reg. No. INA000019026), with 20+ years of experience, works with CXOs and professionals whose investable assets have scaled to ₹10 crore or more.

When Should You Consult a Financial Advisor?

DIY financial planning works well in the early stages. It stops being enough when decisions become complex enough that the cost of a wrong move exceeds the cost of advice.

Triggers that typically warrant professional guidance:

- Significant salary jump (above ₹30–40 lakh annual CTC)

- Marriage or first child

- Home purchase decision

- ESOP or RSU vesting at a growing company

- Inheritance or large lump-sum event

- Approaching retirement within 10 years

Choosing the Right Advisor: SEBI RIA vs. Distributor

Here's how they differ:

| SEBI-Registered Investment Adviser (RIA) | Mutual Fund Distributor (MFD) | |

|---|---|---|

| Compensation | Fee paid by client | Commissions from fund houses |

| Fiduciary obligation | Yes — mandated by SEBI regulations | No |

| Product recommendations | From full universe | Limited to distribution shelf |

| Conflict of interest | None structurally | Incentive to push higher-commission products |

SEBI's investor education guidelines explicitly note that, unlike mutual fund distributors who earn commissions from fund sales, registered investment advisers charge fees directly from clients.

For senior professionals and CXOs navigating ESOP vesting, bonus deployment, and long-horizon wealth decisions, working with a fee-only SEBI RIA removes the commission conflict entirely. iVentures Wealth, for instance, operates on this model — covering investment strategy, salary structuring optimization, and wealth creation across a 20–30 year career arc without earning placement fees from product manufacturers.

Frequently Asked Questions

What are the 5 steps of financial planning?

The five steps are: assess your current financial position, set goals with target amounts and timelines, build a working budget, create a goal-linked savings and investment plan, and review regularly — with adequate insurance protecting the plan throughout.

What are common budgeting rules for salaried employees?

The most common frameworks are the 50/30/20 rule (needs, wants, savings) and the 70-10-10-10 rule (expenses, savings, investments, discretionary goals). The 3-6-9 emergency benchmark determines how many months of expenses to hold liquid. The right rule depends on your income level, family obligations, and job stability.

How much of my salary should I save each month?

At least 20% of take-home salary is the standard starting point. Those beginning late — in their 40s or beyond — will need to save 30–40% to catch up, and the rate should rise in step with every salary increment.

What is the best tax-saving investment for salaried employees in India?

Under the old tax regime, ELSS mutual funds offer the shortest lock-in among 80C instruments at three years. NPS provides an additional ₹50,000 deduction under Section 80CCD(1B) beyond the 80C limit. Health insurance premiums under Section 80D reduce tax while providing essential coverage — up to ₹25,000 for self and family, and ₹50,000 for senior citizen parents.

How do I start investing on a salaried income?

The simplest starting point is automating a monthly SIP in a diversified equity mutual fund on salary day, while ensuring EPF contributions continue uninterrupted. Increase the SIP amount by a fixed percentage with every annual salary hike. Avoid trying to time the market — consistency matters more than timing at the early stages.

What is the difference between EPF and NPS for retirement planning?

EPF is mandatory, government-guaranteed, and provides a fixed interest rate (8.25% for FY 2024-25) with full corpus withdrawal at retirement. NPS is market-linked with potentially higher long-term returns but requires partial annuitisation at maturity and carries market risk. They serve complementary roles — EPF as the stable base, NPS as the growth layer with additional tax benefits.