Introduction

Financial independence isn't just about accumulating wealth — it's about reaching the point where your portfolio sustains your lifestyle without requiring you to show up. For India's founders, CXOs, and affluent families, that distinction matters enormously. Many high earners generate significant income but stay trapped in dependency on it, with no coordinated plan to make their wealth self-sustaining.

The core problem is structural: scattered investments across platforms, no defined target corpus, and tax planning that happens in March rather than throughout the year. The outcome is predictable — people who earn well but never quite reach the freedom they're working toward.

This article covers seven practical strategies — from calculating your personal FI number to building passive income streams and structuring tax-efficient wealth — to help you move from high earner to financially independent.

Key Takeaways

- Financial independence means your passive income fully covers your lifestyle costs, with no dependence on a salary or active business income

- Your FI number is the single most important calculation here: every other decision follows from it

- Diversified portfolios, multiple passive income streams, and proactive tax planning are the three pillars that actually move the needle

- Regular reviews with a SEBI-registered fiduciary advisor are what separate those who reach FI from those stuck in accumulation mode

What Financial Independence Really Means for Affluent Indians

Financial independence has a precise definition: the point at which your passive income fully covers your desired cost of living — without requiring you to actively work. But it's worth separating FI from two concepts it's often confused with:

- Being "rich" — High net worth doesn't equal freedom. A ₹100 Cr portfolio tied up in illiquid assets or a running business doesn't pay your lifestyle costs.

- Retirement — Financial independence doesn't mean you stop working. It means you work by choice, not necessity.

- Financial independence — Passive income from investments, dividends, rental income, or business distributions sustains your life indefinitely.

The FIRE Framework in the Indian Context

The FIRE (Financial Independence, Retire Early) movement originated in the West, but applying it to India requires meaningful adjustments. India's headline CPI inflation ran at 6.7% in FY2022-23, 5.4% in FY2023-24, and 4.6% in FY2024-25 according to the RBI Annual Report 2024-25 — already higher than the assumptions embedded in Western FIRE calculations. Healthcare costs are a separate problem: healthcare inflation in India is rising at 14% annually, according to the ACKO India Health Insurance Index 2024. That's not a rounding error — it's a planning variable that can derail an otherwise solid FI plan.

For HNIs, founders, and family business owners, financial independence also carries an additional dimension: legacy planning. The goal isn't just sustaining your own lifestyle indefinitely — it's structuring wealth to support future generations. That demands a fundamentally different portfolio architecture — one that typically involves multi-generational trust structures, AIF and private credit allocations, and business succession layers that standard retirement planning never accounts for.

Define Your Financial Independence Number and Set Clear Goals

Calculating Your FI Number

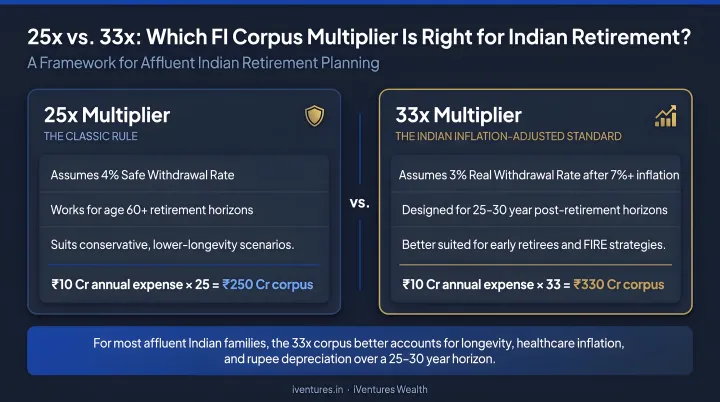

The most widely used starting point is the 25x rule: multiply your expected annual post-FI expenses by 25. This is derived from a 4% safe withdrawal rate — the assumption that a diversified portfolio can sustain 4% annual withdrawals indefinitely.

In the Indian context, this calculation deserves scrutiny. Mint's analysis of Indian retirement planning suggests Indian retirees may need to use a 3% to 3.5% withdrawal rate instead of 4%, citing a 2022 study where 4% withdrawals depleted portfolios in nearly one-third of simulated scenarios. At a 3% rate, the implied corpus multiplier rises to 33x annual expenses —a gap that materially changes how much you need to accumulate before calling it done.

What goes into your annual expense estimate:

- Core living costs (housing, food, utilities, transport)

- Healthcare and insurance premiums — modelled at 14% inflation, not CPI

- Children's education costs

- Travel and discretionary spending

- Any EMIs still running in early retirement years

- A buffer for irregular large expenses

Setting SMART FI Goals

Once you have a target corpus in mind, structure it as a goal that actually drives action. Vague intentions don't move money. The SMART framework does:

- Specific: "Build a ₹5 Cr liquid investment corpus by age 45"

- Measurable: Track net worth, investable assets, and passive income quarterly

- Attainable: Benchmark against current income, savings rate, and realistic return assumptions

- Relevant: Tied to actual lifestyle costs, not aspirational ones

- Time-bound: Set a target FI date and work backward to annual milestones

Track short-term goals (₹30–50 lakh emergency corpus, eliminating high-interest debt) and long-term goals (full FI corpus, passive income streams) simultaneously. Neglecting one for the other creates blind spots.

Your FI number is not static. Review it every two to three years as lifestyle costs shift, tax laws change, and family circumstances evolve. Healthcare costs in particular tend to be chronically underestimated. Build them in explicitly, not as an afterthought.

Build a Diversified, Growth-Oriented Investment Portfolio

Accumulation Phase vs. Distribution Phase

Your portfolio needs two modes. During the accumulation phase, the objective is maximising long-term growth — higher equity exposure, reinvested returns, disciplined SIPs. As you approach FI, the portfolio transitions toward the distribution phase: maximising stable, predictable income without depleting principal.

Getting the timing of that transition wrong — either too early (sacrificing growth) or too late (taking sequence-of-returns risk) — is one of the most common planning errors among affluent investors.

Key Instruments for an FI-Oriented Portfolio

| Instrument | Role in FI Portfolio | Key Consideration |

|---|---|---|

| Direct equities & equity mutual funds | Long-term growth engine | Nifty 50 TRI delivered ~15.23% CAGR over 20 years (Mirae Asset) |

| Bonds, G-Sec, NCDs | Stability and predictable income | 10-year AAA PSU bonds at 7.43% (CRISIL, Mar 2024) |

| REITs / InvITs | Passive income with quarterly distributions | 6–8% distribution yields; ₹1.3 lakh crore mobilised since 2019 |

| PPF / NPS | Tax-efficient retirement corpus | PPF at 7.1% p.a.; NPS offers meaningful 80CCD deductions |

| PMS / AIFs | Alpha generation for HNI portfolios | Private credit AIFs targeting 12–16% IRR |

Why Timing Your Start Matters as Much as Instrument Selection

To reach a ₹5 Cr corpus at a 12% CAGR assumption, the required monthly SIP differs dramatically by timeline: approximately ₹50,500/month over 20 years versus roughly ₹2.17 lakh/month over 10 years. Starting a decade earlier more than halves the monthly commitment — which means choosing the right instruments and starting early are equally non-negotiable decisions.

Tracking whether your portfolio stays on that trajectory is where discipline often breaks down. iVentures Wealth's Wealth Monitor App gives clients a consolidated view of all holdings across accounts and asset classes in real time — tracking current value, daily changes, CAGR, and allocation by category — so portfolio drift is caught before the next formal review, not after.

Create Passive Income Streams That Work for You

Passive income directly reduces the corpus you need for FI — every rupee it covers in monthly expenses is one less rupee your portfolio has to generate through withdrawals. The more your assets pay you, the smaller the gap your corpus needs to bridge.

Relevant Passive Income Sources for Indian HNIs

From financial assets:

- Dividend income from equity portfolios (Nifty 50 dividend yield: 1.35% as of May 2026 — useful for cash flow supplementation, not as a standalone income source)

- Bond and NCD interest income — investment-grade corporate bonds yielding 7–8%+

- REIT/InvIT distributions at 6–8% quarterly yields

From real estate:

- Residential rental yield: 3–4% gross in most metros

- Premium commercial and pre-leased Grade-A commercial: 8–12%

- Fractional commercial ownership: 9–12%

From business interests: For founders, structuring the business to generate passive distributions — rather than treating all cash flows as active income — is a practical and frequently overlooked path to FI. This doesn't require selling the business.

One approach iVentures has implemented: ring-fencing a dedicated corpus into income-oriented portfolios across high-quality debt, REITs/InvITs, and income-focused funds, with defined withdrawal rules. In one documented case, this structure generated approximately ₹7.5 lakh per month in predictable passive income — with the corpus continuing to grow despite regular withdrawals.

Tax Efficiency Matters for Passive Income

Not all passive income is taxed the same way — and the difference matters at scale. Key treatments to know:

- Rental income: 30% standard deduction on net annual value under the Income Tax Act

- Equity LTCG: Taxed at 12.5% above ₹1.25 lakh (effective July 23, 2024)

Your income mix determines your actual post-FI net income. That's the number your lifestyle runs on.

Optimise Taxes and Manage Debt Strategically

Tax Optimisation for HNIs

For HNIs on the FI path, proactive tax planning — not March-deadline filing — is the difference between reaching your corpus target on time or falling short. Tax inefficiency left unaddressed compounds across decades.

Key strategies worth structuring around:

- LTCG harvesting: Realise long-term gains up to ₹1.25 lakh annually tax-free under the current regime, systematically

- Tax-loss harvesting: Offset gains by booking losses in underperforming positions before year-end

- HUF structuring: An HUF is a separate tax entity with its own exemption limit (₹4 lakh under the new regime per ClearTax) — relevant for family wealth planning

- Timing capital gains realisations: Spreading large redemptions across financial years to manage the applicable tax bracket

NPS as a Dual-Purpose Tool

For salaried professionals and CXOs, the National Pension System deserves a deliberate place in FI planning — not just as a retirement product, but as a tax-efficiency vehicle.

The deduction mechanics are worth knowing precisely: employee contributions are deductible up to 10% of salary under Section 80CCD(1), with an additional ₹50,000 available under Section 80CCD(1B). Employer contributions under the new tax regime qualify at 14% of salary. Together, they deliver meaningful tax savings while building a dedicated retirement corpus.

Debt and Estate Planning

Carrying high-interest debt while building a FI corpus is mathematically counterproductive. The priority sequence:

- Eliminate credit card balances and personal loans first

- Redirect that cash flow into wealth-building investments

- Evaluate structured debt (a well-structured home loan) only where investment returns clearly outpace borrowing costs

Once high-cost debt is cleared, estate and succession planning becomes the next layer to address. Without proper will, trust, and nominee structures, accumulated wealth faces unnecessary tax leakage and legal friction at transfer.

This is especially relevant for affluent families and family offices — and getting the structure right early saves substantial costs later.

Review Your Plan Regularly and Work With a Fiduciary Advisor

Why Annual Reviews Are Non-Negotiable

Financial independence is not a set-and-forget plan. Life events — career transitions, business exits, health changes, market cycles, new tax regulations — each require recalibration. A formal annual review should cover:

- Progress toward FI number and corpus milestones

- Portfolio allocation drift vs. target

- Tax planning opportunities for the coming year

- Changes in lifestyle costs or family obligations

Beyond the annual cycle, event-triggered reviews matter: a liquidity event, a major health development, or a significant market correction all warrant a fresh look at the plan.

The Behavioral Guardrail Problem

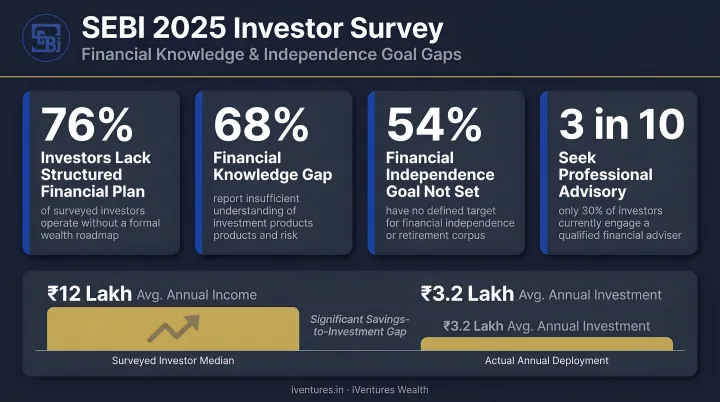

One of the less-discussed risks on the path to FI is emotional decision-making — panic selling in downturns, chasing recent outperformers, abandoning an SIP during volatility. The SEBI Investor Survey 2025 found that even among affluent households earning over ₹12 lakh annually, only 53% demonstrated high to moderate market knowledge, and just 7% identified financial independence as a primary financial goal. These gaps have real consequences for long-term portfolio outcomes.

A fiduciary advisor's value isn't just in selecting the right instruments — it's in keeping clients anchored to the plan when markets create pressure to deviate. Systematic rebalancing rules, goal-linked investment mapping, and regular communication during volatility all serve as structural guardrails against costly emotional decisions.

iVentures Wealth's Approach

iVentures Wealth (SEBI RIA INA000019026) was founded in 2005 by Nirmal A Bansal and has grown to manage over ₹1,200 Cr+ across 150+ affluent relationships. The firm's CFA-led team operates on a structure designed specifically to remove the conflicts that make behavioral guardrails difficult to enforce:

- Fee-only advisory with no commissions or trail income

- Open-architecture recommendations drawn from the full regulated product universe

- All fees disclosed upfront — no product placement incentives

For founders, CXOs, and affluent families, this structure means the advisor's interest is aligned with staying the course — not with switching products or chasing the next outperformer.

Frequently Asked Questions

What is financial independence planning?

Financial independence planning is the structured process of identifying your target corpus, designing an investment strategy, and building passive income streams. The goal: your assets fully cover your living expenses, freeing you from dependence on any single income source.

What is the 70-10-10-10 rule for financial independence planning?

The 70-10-10-10 rule is a budgeting framework where 70% of income covers daily expenses, 10% goes to savings, 10% to investments, and 10% to debt repayment or giving. It offers a simple starting structure for wealth building, particularly for those early in the FI journey.

What is the 3-6-9 rule for financial independence planning?

The 3-6-9 rule guides emergency fund sizing: 3 months of expenses for single earners with stable income, 6 months for most households, and 9 months for those with variable income or dependents. It establishes the liquidity foundation before aggressive wealth-building begins.

What are the 7 steps of financial independence planning?

The seven core steps: define your FI number, set SMART goals, build a diversified portfolio, create passive income streams, optimise taxes, eliminate high-interest debt, and review the plan regularly with professional guidance.

How much corpus do I need to achieve financial independence in India?

Apply the 25x rule to your annual lifestyle expenses as a starting point — but given India's inflation dynamics, stress-testing with 28x–33x (implying a 3–3.5% withdrawal rate) provides a more conservative and appropriate buffer for Indian conditions.

When is the right time to start planning for financial independence?

The best time is as early as possible. Compounding rewards early starters disproportionately. That said, a well-structured 10–15 year plan can meaningfully accelerate FI even for those starting in their 40s or 50s.