Disclosure: iVentures Wealth is a SEBI-registered Investment Adviser. SEBI RIA Registration No.: INA000019026.

Many Indian HNI portfolios look diversified on paper. There may be equities, real estate, fixed deposits, gold, business interests, and mutual funds. But if most of that wealth is still tied to India, the rupee, and the same domestic economic cycle, the portfolio may be diversified by product, not by geography.

International portfolio diversification helps reduce that single-country dependence. For Indian residents, the Liberalised Remittance Scheme allows eligible resident individuals to remit up to USD 250,000 per financial year for permitted current or capital account transactions, including overseas investments. But global investing should not be done just because foreign markets are trending. It should be structured around risk, currency needs, tax treatment, costs, and the role international assets play in the larger portfolio.

Key Takeaways on International Portfolio Diversification

What it means: International diversification means spreading part of your portfolio across countries, currencies, and markets instead of relying only on domestic assets.

Why it matters: It can reduce concentration risk, add foreign-currency exposure, and give access to sectors or companies that may be limited in Indian markets.

What to check first: Before investing globally, review your existing India exposure, risk profile, time horizon, tax position, remittance route, and future foreign-currency goals.

The core rule: International investing should not replace one concentration with another. The aim is a structured global allocation, not simply adding a US fund or foreign ETF.

What Is International Portfolio Diversification?

International portfolio diversification means investing part of your wealth outside your home market, across different countries, currencies, sectors, and asset classes. The basic idea is simple: if one economy, currency, or market cycle weakens, your entire portfolio should not be forced to move with it.

This is different from only buying Indian companies that earn revenue abroad. A domestic stock may have global customers, but it is still listed in India, priced in rupees, and affected by Indian market sentiment, liquidity, taxation, and regulation. True international exposure gives you access to foreign-listed assets, foreign currencies, and markets that may behave differently from India.

Why correlation matters

Diversification works best when different parts of a portfolio do not move in the same direction at the same time. Investor.gov, the investor education website run by the U.S. SEC, explains diversification as spreading investments across asset categories so that a fall in one area may be offset by better performance elsewhere.

For Indian investors, this matters because domestic assets often share common risk drivers: RBI policy cycles, rupee movement, local inflation, Indian corporate earnings, and domestic political or regulatory developments. International exposure can add a second engine to the portfolio, but only if it is chosen deliberately.

What this means

A portfolio is not globally diversified just because it has many products. It is globally diversified when country, currency, sector, and market-cycle risks are spread with a clear purpose.

This is especially important for HNIs and globally mobile families because income, property, business interests, and investments may already be concentrated in one geography without it being obvious.

Why Indian HNIs Should Look Beyond Domestic Diversification

Many Indian HNI portfolios look diversified on paper. But the real question is not just how many asset types you own. It is how many risks your portfolio depends on.

You may need international diversification if most of your wealth is tied to:

- Indian equities or mutual funds

- Indian real estate

- fixed deposits or rupee debt

- business income from India

- ESOPs linked to Indian or India-heavy companies

- future inheritance or family assets in India

- expenses, goals, or liabilities that may arise outside India

This is where product diversification can be misleading. A portfolio with stocks, property, FDs, gold, and business assets may still depend heavily on one country, one currency, and one domestic economic cycle.

Home bias is natural. Familiar assets feel safer because investors understand them better. But for families with children abroad, overseas education goals, global lifestyle needs, or cross-border succession plans, a domestic-only portfolio may not match how their life is actually structured.

So the question is not whether India should remain part of the portfolio. For most Indian HNIs, it will. The sharper question is: how much of your wealth should depend only on India?

For investors already thinking about wealth growth beyond a domestic-only portfolio, international diversification becomes a portfolio design decision, not a trend to follow.

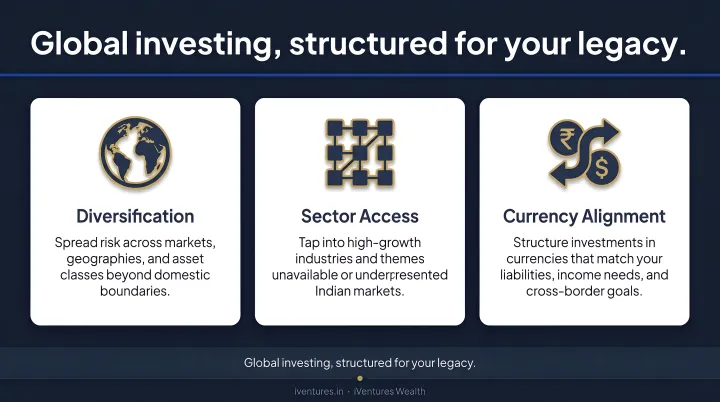

Benefits of International Portfolio Diversification

International diversification does not mean foreign markets will always outperform India. It simply reduces the pressure on one country, one currency, and one market cycle to carry the entire portfolio.

Key benefits include:

- Lower country concentration: If most wealth is in Indian equities, real estate, fixed income, and rupee cash flows, the portfolio is exposed to the same domestic forces. Global exposure can add markets that respond differently to rates, inflation, earnings cycles, and policy changes.

- Access to sectors underrepresented in India: Some themes, such as semiconductors, global cloud infrastructure, advanced manufacturing, biotech, large-scale consumer technology, and global healthcare leaders, are better represented outside Indian exchanges.

- Currency diversification: Foreign assets add exposure to currencies such as the dollar, pound, euro, dirham, or Singapore dollar. This can help if future expenses are also in those currencies. But currency movement cuts both ways, so it should be planned, not treated as a guaranteed hedge.

- Better alignment with global life goals: Many affluent Indian families already have global financial lives: children studying abroad, overseas retirement plans, family members in different countries, or future cross-border inheritance. International exposure can help the portfolio reflect that reality.

Portfolio note: If your long-term goals include overseas education, global retirement planning, or multi-country family wealth, international exposure should be reviewed as part of your broader wealth growth strategy, not added as a one-off product.

Risks of International Investing

Global exposure can improve portfolio design, but it also adds new risks. These should be understood before investing.

| Risk | What to watch |

|---|---|

| Currency risk | Returns depend on both asset performance and currency movement. A foreign fund can perform well, but INR returns may change if the rupee strengthens or weakens. |

| Market and country risk | Foreign markets can face recessions, rate changes, geopolitical events, sector bubbles, tax changes, and regulatory restrictions. |

| Tax and reporting complexity | Foreign dividends, capital gains, withholding tax, DTAA treatment, and Indian reporting rules can affect net returns. For foreign tax credit claims, the Income Tax Department notes that Form 67 is required under Rule 128. |

| Higher costs | Forex conversion, remittance charges, brokerage, custody fees, fund expenses, and tax friction can reduce returns. |

| US-only concentration | Buying only US exposure is not the same as global diversification. It may reduce India concentration but create a new single-country concentration. |

The better approach is to define the role of international exposure first: currency matching, global sector access, risk reduction, future foreign expenses, or long-term wealth diversification.

How Indian Residents Can Invest Internationally

For Indian residents, global investing has to happen through permitted routes. The main route is the Liberalised Remittance Scheme, under which resident individuals, including minors, can remit up to USD 250,000 per financial year for permitted current or capital account transactions.

Route 1: Direct overseas investing through LRS

Resident individuals can use LRS to invest in overseas assets such as foreign stocks, ETFs, mutual funds, and other permitted securities. This route gives wider access, but it also brings more responsibility: remittance documentation, currency conversion, tax reporting, and platform selection.

This is usually more relevant for investors who want control over the specific markets, sectors, or securities they access.

Route 2: International mutual funds or feeder funds in India

Some Indian mutual funds provide global exposure by investing in overseas funds, indices, or feeder structures. This can be simpler because the investment happens through an Indian mutual fund route.

The limitation is availability. Overseas investment limits for Indian mutual funds can affect whether a scheme accepts fresh lumpsum investments or restricts inflows. SEBI’s circular on investments in overseas mutual funds/unit trusts is an example of how these routes remain subject to regulatory limits and conditions.

Route 3: ETFs and exchange-listed options

Investors may also access certain global themes through ETFs listed on Indian or overseas exchanges. These can be useful for broad market exposure, but the investor still needs to check costs, liquidity, tracking difference, taxation, and currency impact.

Route 4: GIFT City and advanced structures

For eligible investors, GIFT City and other regulated structures may offer access to USD-denominated funds or global strategies. These routes are more relevant for larger portfolios, NRIs/OCIs, or investors who need a more structured cross-border setup.

Global access is easier than before. Choosing the right route is still the hard part. If your portfolio already includes Indian equities, property, business wealth, and rupee assets, iVentures Wealth can help review how international exposure should fit into the larger structure.

How Much International Allocation Is Right?

There is no fixed percentage that works for every investor. A 25-year-old professional, a founder with most wealth tied to an Indian business, a retiree with rupee expenses, and a family planning overseas education cannot use the same global allocation rule.

The right allocation should come from the portfolio you already have, not from a generic number.

Start with your existing India exposure

Before deciding how much to invest abroad, check how much of your current wealth already depends on India.

This includes:

- Indian equities and mutual funds

- Indian real estate

- fixed deposits and debt investments

- business ownership or promoter equity

- salary or professional income in India

- future inheritance or family assets in India

If most of these are India-linked, even a small international allocation may improve the portfolio structure. If you already have foreign income, foreign assets, or overseas liabilities, the allocation needs a different lens.

Match the allocation to actual goals

International exposure should have a job.

It may be used for:

- overseas education planning

- future foreign-currency expenses

- global retirement needs

- reducing dependence on Indian market cycles

- accessing sectors not available domestically

- balancing family wealth across countries

Without a clear purpose, international investing can become portfolio clutter. The investor may own foreign funds, but still not know whether they are reducing risk, matching currency needs, or simply chasing recent performance.

Avoid copying standard allocation rules

Rules like “put 10% or 20% abroad” are easy to remember, but they are rarely enough for serious portfolios. The number should change based on domestic concentration, liquidity needs, tax treatment, risk tolerance, and time horizon.

For HNIs, the better question is not “What percentage should I invest internationally?” It is: what risk or goal is this international allocation supposed to solve?

Strategy: How to Build a Smarter Global Portfolio

International diversification should start with a role, not a product. Before choosing a US fund, global ETF, feeder fund, or direct stock route, decide what the allocation is meant to do inside the portfolio.

Decide the role of global exposure

For one investor, international exposure may be about reducing dependence on Indian markets. For another, it may be about matching future dollar expenses. For a third, it may be about accessing sectors that are underrepresented in India.

The same fund can be useful in one portfolio and unnecessary in another. The difference is the role it plays.

Diversify beyond one country

A common mistake is to treat US investing as international diversification. US exposure can be valuable, but it should not automatically become the entire global allocation.

A more deliberate approach may include a mix of developed markets, selective emerging markets, global sectors, and currency exposure, depending on the investor’s risk profile and goals. The point is not to own every geography. It is to avoid replacing India concentration with another single-country bet.

Choose the vehicle carefully

The route should match the investor’s size, tax position, reporting comfort, and need for control.

A small allocation may work through a simpler fund route. A larger or more complex portfolio may need closer review of LRS usage, tax reporting, cost, currency exposure, and family-level visibility.

Review and rebalance

Global allocations drift. A strong rally in one market, a currency move, or a change in family goals can shift the portfolio away from its intended structure.

Reviewing the portfolio periodically helps answer three questions:

- Is international exposure still serving its original role?

- Has one country, sector, or currency become too large?

- Do taxes, costs, or reporting needs still justify the route being used?

A smarter global portfolio is not built by adding foreign exposure once. It is built by giving that exposure a clear purpose, then reviewing whether it continues to serve that purpose.

Where iVentures Wealth Fits Into Global Diversification Planning

Global investing is easier to access today. The harder part is deciding what it should do inside your portfolio.

For many HNIs, the issue is not whether they can invest abroad. It is whether global exposure is being added with a clear purpose, or simply because a foreign market, index, or theme has performed well recently.

The Problem Is Usually Not Access

Investors now have several ways to access international markets: LRS, international mutual funds, feeder funds, ETFs, direct overseas platforms, and advanced structures for eligible investors.

But access does not automatically create diversification. A portfolio can still become concentrated if it is tilted too heavily toward one country, one currency, one sector, or one investment theme.

iVentures’ Advisory Lens

iVentures Wealth helps affluent investors look at international diversification as part of the full wealth picture: Indian equities, real estate, fixed income, business wealth, family assets, tax position, liquidity needs, and future global goals.

That matters because a global allocation should not sit separately from the rest of the portfolio. It should answer practical questions:

- Does it reduce existing concentration?

- Does it match future foreign-currency needs?

- Does it improve access to missing sectors?

- Is the route tax-efficient and reportable?

- Does the family have visibility across domestic and international assets?

From Scattered Exposure to Structured Allocation

The aim is not to add foreign funds for the sake of it. The aim is to build a portfolio where each geography, currency, and asset class has a clear role.

For investors who already hold Indian assets across equities, property, FDs, mutual funds, and business interests, iVentures can help review whether international exposure belongs in the portfolio, how much is appropriate, and which route fits the investor’s broader wealth management strategy.

Common Mistakes to Avoid

International diversification works only when it improves the portfolio structure. If it is added casually, it can create more clutter than clarity.

| Mistake | Why it matters |

|---|---|

| Investing only because foreign markets are trending | Turns diversification into performance chasing. |

| Buying only US exposure | Reduces India concentration but may create another single-country concentration. |

| Ignoring currency movement | INR returns can differ sharply from foreign-currency returns. |

| Forgetting tax and reporting | Dividends, capital gains, foreign tax credit, and disclosures can affect net returns. |

| Spreading small amounts across too many products | Costs, tracking, and reporting can become inefficient. |

| Not defining the purpose of global exposure | The portfolio gets more products, but not necessarily better diversification. |

Advisor Note

The goal is not to own more markets for the sake of it. The goal is to know why each geography, currency, and asset class exists in the portfolio.

For serious portfolios, international diversification should be reviewed like any other allocation decision: what risk does it reduce, what opportunity does it add, what cost does it bring, and how does it fit the family’s long-term wealth plan?

FAQs on International Portfolio Diversification

What is international portfolio diversification?

International portfolio diversification means investing part of your portfolio across countries, currencies, and markets outside your home country. For Indian investors, this may include foreign stocks, international mutual funds, feeder funds, ETFs, or other permitted overseas investment routes.

Why is international diversification important for Indian investors?

It helps reduce dependence on one economy, one currency, and one market cycle. This is especially relevant for HNIs whose wealth may already be concentrated in Indian equities, real estate, fixed income, business assets, and rupee-denominated cash flows.

How can Indian residents invest internationally?

Indian residents can invest abroad through permitted routes such as the Liberalised Remittance Scheme, international mutual funds, feeder funds, ETFs, and certain exchange-listed or overseas investment platforms. The route should be chosen based on cost, tax treatment, reporting needs, and suitability.

What are the main risks of international investing?

The main risks include currency fluctuation, foreign market volatility, country-specific regulation, taxation, reporting requirements, and additional costs such as forex conversion, brokerage, and fund expenses. These risks do not make global investing unsuitable, but they need to be planned for.

How much of a portfolio should be invested internationally?

There is no universal percentage. The right allocation depends on existing India exposure, risk profile, time horizon, liquidity needs, tax position, and future foreign-currency goals. A family with overseas education goals may need a different allocation from a retiree whose expenses are entirely in India.

Disclaimer

This article is for educational purposes only and should not be treated as personalized investment, tax, legal, or financial advice. International investing involves market risk, currency risk, tax implications, reporting requirements, and regulatory considerations. Investment decisions should be made after reviewing your risk profile, goals, liquidity needs, tax position, country of residence, and applicable regulations. Please consult a qualified investment adviser, tax professional, or legal expert before acting.