These are exactly the questions many NRIs get wrong, sometimes at real financial cost. The rules around PPF for NRIs have tightened considerably, and the 2026 position is clear: NRIs are in a "manage and close" situation, not a "grow and extend" one.

This guide covers the official 2026 stance on NRI PPF eligibility, contribution rules, withdrawal mechanics, tax treatment in India and abroad, and the alternatives worth considering once your PPF matures.

Key Takeaways

- NRIs cannot open new PPF accounts — only accounts opened as a resident Indian can be maintained

- Existing accounts can be contributed to until the 15-year maturity, with no extension permitted after that

- Contributions must come from an NRO account, not an NRE or FCNR account

- At maturity, proceeds are credited to the NRO account and are repatriable subject to RBI limits

- Failing to notify your bank of NRI status risks a rate reduction to the POSA rate (4.0% p.a.)

Can NRIs Invest in PPF in 2026? The Official Stance

The answer is unambiguous: NRIs and OCIs cannot open new PPF accounts.

This restriction applies regardless of whether you hold a PAN card, maintain NRE/NRO accounts, or have an active banking relationship in India. The Public Provident Fund Scheme, 2019, notified by G.S.R. 915(E) and amended in May 2020, limits new account opening to resident citizens of India.

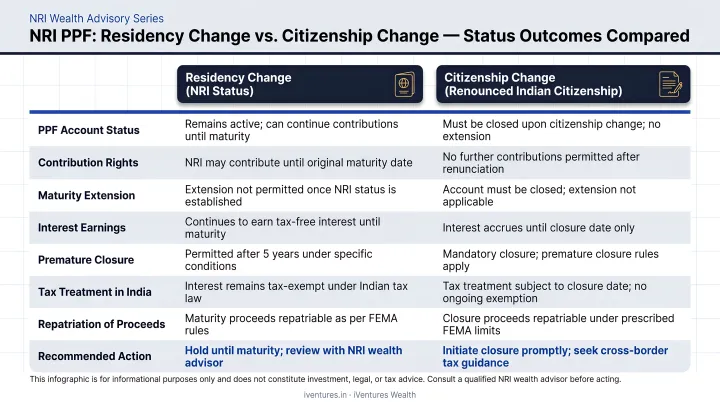

The Grandfather Rule

If you opened a PPF account while you were a resident Indian and subsequently became an NRI, that account can continue. You may contribute to it and earn interest until the original 15-year maturity date — but you cannot extend it beyond that point. Resident Indians can renew in 5-year blocks; NRIs cannot.

What About OCI Cardholders?

OCIs fall into the same category as NRIs for PPF purposes. They cannot open new accounts. If an OCI holds a valid grandfathered account (opened before acquiring OCI status), the same rules apply: maintain until maturity, then close.

If You Change Citizenship

Changing nationality triggers the strictest outcome. If an NRI's nationality changes from Indian to another country's, the PPF account is treated as closed from the last day of the preceding month. Interest from that point onwards applies at the Post Office Savings Account (POSA) rate — currently 4.0% p.a., compared to PPF's 7.1%. On a corpus of ₹50 lakh, that gap compounds to a significant shortfall over 3–5 years.

A separate rule — currently suspended: A 2017 notification (G.S.R. 1237(E)) would have deemed PPF accounts closed simply upon acquiring NRI status. That rule was kept in abeyance by a Ministry of Finance Office Memorandum dated 23 February 2018 and remains suspended. NRI status alone does not close a PPF account.

The Notification Obligation

The rules above only work in your favour if you act on them. NRIs must inform their bank or post office when their residency status changes. Contributions made post-status change without proper notification may have interest recalculated at POSA rates until the discrepancy is corrected — retroactively. Notify your account-holding institution promptly and keep written confirmation of that notification.

PPF Rules for NRIs in 2026: What Stays and What Has Changed

For NRIs with valid grandfathered accounts, the core mechanics remain intact — contribution limits, interest rates, and loan eligibility all apply as they did at account opening, subject to the compliance conditions below.

Contribution Limits and Account Rules

| Rule | Detail |

|---|---|

| Minimum annual contribution | ₹500 |

| Maximum annual contribution | ₹1,50,000 |

| Account tenure | 15 complete financial years from end of opening year |

| Extension option | Not available for NRIs |

| Contribution source | NRO account only (not NRE or FCNR) |

The NRO-only contribution requirement is a common point of confusion. Many NRIs assume they can use their NRE account since it's also an Indian account — they cannot.

Account Tenure and Extension Rules

The 15-year maturity is a hard endpoint for NRIs. Unlike resident Indians who can extend in 5-year blocks (with or without fresh contributions), NRIs must close the account at maturity. Plan accordingly: the maturity date should be on your radar at least 6–12 months in advance to allow time for proper closure and fund repatriation planning.

Loan Against PPF

NRIs can avail a loan against their PPF balance between the 3rd and 6th financial years. The maximum loan is 25% of the balance at the end of the 2nd financial year preceding the loan application year.

Quick example: If you're applying for a loan in FY 2025-26, the limit is 25% of your balance as of 31 March 2023. So if your balance then was ₹4,00,000, the maximum loan is ₹1,00,000.

Interest Rate in 2026

According to India Post's current savings page, the PPF interest rate stands at 7.1% p.a. for FY 2025-26, compounded annually. The Government of India reviews this quarterly, though it has remained at 7.1% for several consecutive quarters.

This rate applies equally to resident Indians and NRIs — provided compliance rules are followed. Non-compliance (meaning, failing to notify the bank of NRI status) can revert the applicable rate to the POSA rate of 4.0% p.a.

Withdrawals, Maturity, and Repatriation: How NRIs Access Their PPF Funds

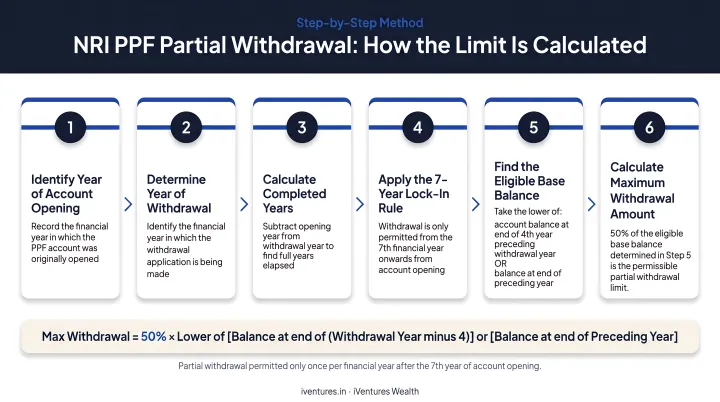

Partial Withdrawals

Partial withdrawals are permitted from the 6th financial year onwards (after 5 full years from account opening). The rules:

- Maximum withdrawal: 50% of the lower of — the balance at the end of the 4th preceding year, or the balance at the end of the preceding financial year

- Only one withdrawal is permitted per financial year

Example: Applying for a withdrawal in FY 2025-26, you compare your balance at end of FY 2021-22 versus end of FY 2024-25, and take 50% of whichever is lower. If those balances were ₹5,00,000 and ₹8,00,000 respectively, your maximum withdrawal is ₹2,50,000 (50% of ₹5,00,000).

Premature Closure

Premature closure is allowed after 5 completed financial years, subject to:

- A 1% interest penalty applied to the entire period from account opening

- Valid grounds: life-threatening illness (account holder or family), higher education (account holder or dependent), or change in residency status

Maturity Closure

At the 15-year mark, NRIs must close the account. The full maturity amount is credited to the NRO account. Leaving funds to earn interest indefinitely is not permitted for NRIs; that option is available only to resident Indians.

Repatriation Process

Once the maturity proceeds are credited to your NRO account, repatriation follows standard RBI rules. RBI's FAQs on non-resident accounts confirm NRO balances are remittable up to USD 1 million per financial year (April–March).

Two forms govern the process:

- Form 15CA: Required before every remittance

- Form 15CB: A Chartered Accountant certificate needed when the remittance is taxable and exceeds ₹5 lakh in the financial year; non-taxable remittances use Part D of Form 15CA instead

Documents Required: Premature vs. Maturity Closure

| Document | Premature Closure | Maturity Closure & Repatriation |

|---|---|---|

| PPF closure/withdrawal form | ✓ | ✓ |

| Passbook or account statement | ✓ | ✓ |

| PAN and photo ID | ✓ | ✓ |

| Cancelled cheque (NRO account) | ✓ | ✓ |

| Proof of NRI status (passport, visa stamps, overseas address) | ✓ | ✓ |

| Medical authority certificate and supporting bills | For illness ground | — |

| Admission or fee receipts | For education ground | — |

| Passport/visa stamps or ITR evidencing residency change | For residency ground | — |

| Form 15CA/CB | — | ✓ |

Tax Treatment of PPF for NRIs: India and Abroad

In India — EEE Still Applies

PPF retains its EEE (Exempt-Exempt-Exempt) tax status for NRI account holders. As confirmed by the Income Tax Department's exempt income guidance:

- Contributions qualify for Section 80C deductions (up to ₹1.5 lakh), applicable where the NRI has Indian taxable income

- Interest earned is exempt under Section 10(11)

- Maturity proceeds are fully tax-exempt in India

Outside India — The Picture Changes

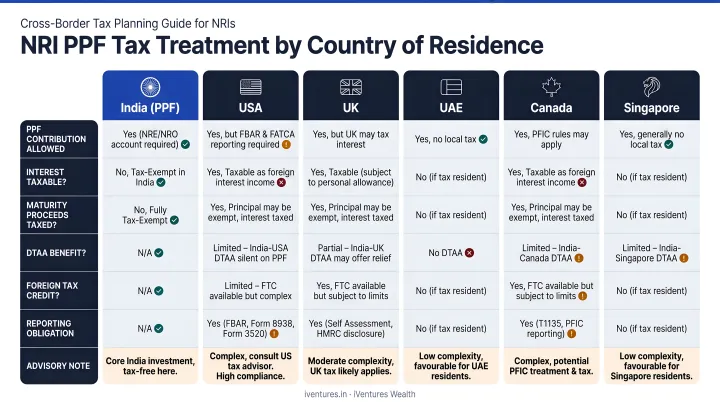

Indian tax exemption does not travel. NRIs must separately assess their host country's tax obligations on PPF returns.

The US is the clearest example of this gap. The IRS requires US citizens and resident aliens abroad to report worldwide income, meaning PPF interest — though exempt in India — is generally taxable in the US. The India-US DTAA contains general interest provisions, but no PPF-specific exemption.

Since India doesn't tax PPF interest, there's limited foreign tax credit available to offset US tax on the same income.

The situation varies by country:

| Country | Key Consideration |

|---|---|

| USA | Worldwide income reporting; PFIC rules may apply to mutual funds; DTAA offers limited relief on PPF |

| UK | India-UK DTAA covers interest income; domestic UK rules govern exemption eligibility |

| UAE | No personal income tax currently; generally less complex for PPF reporting |

| Canada/Singapore | DTAA provisions apply; country-specific domestic tax analysis needed |

For NRIs in most countries, the practical answer is the same: get advice from a cross-border tax professional who understands both jurisdictions. Generic assumptions about DTAA coverage can be expensive mistakes.

iVentures Wealth works with NRIs across the US, UK, UAE, Singapore, and Canada on exactly this kind of cross-border complexity — coordinating DTAA structuring and tax compliance alongside broader investment planning.

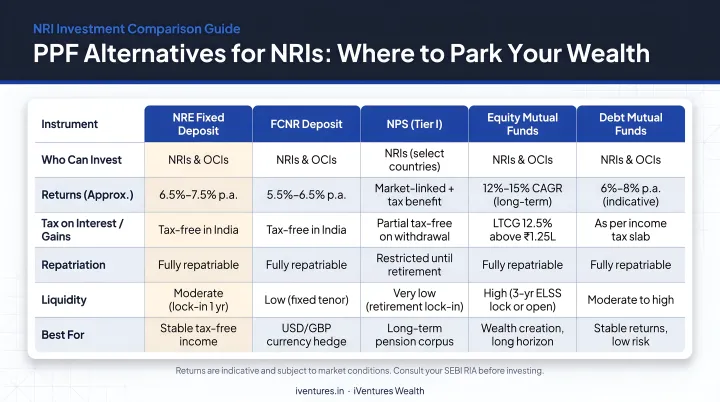

PPF Alternatives NRIs Should Consider in 2026

Since NRIs cannot open new PPF accounts and existing ones must close at maturity, deploying those proceeds — and any new savings — into suitable alternatives matters.

Here's a structured overview of the main options:

| Alternative | Key Feature | India Tax | Repatriable? | Watch Out For |

|---|---|---|---|---|

| NRE Fixed Deposits | Rupee FDs; SBI/HDFC rates ~6.25–6.50% for 1–5 year tenures | Interest tax-free in India | Yes, freely | Rate risk at renewal |

| FCNR(B) FDs | Foreign currency deposits (USD, GBP, EUR, etc.) | Interest tax-free in India | Yes, in foreign currency | Currency and rate trade-offs |

| NPS (Tier I) | Equity-linked retirement corpus; PFRDA allows NRIs/OCIs aged 18–85 | Section 80CCD benefits may apply | Retirement withdrawal rules apply | Not a liquidity substitute for PPF |

| Equity/Debt Mutual Funds | Higher return potential; open-architecture options | Varies by fund type | Subject to FEMA rules | US-based NRIs face PFIC reporting complexity |

NRE FDs are the most direct substitute for NRIs who need repatriable, rupee-denominated returns. FCNR deposits suit those wanting currency protection. NPS is a retirement-specific allocation — treat it as such, not as a like-for-like PPF replacement.

For US-based NRIs, Indian mutual funds require careful analysis under IRS Form 8621 (PFIC rules). Before allocating to any fund, confirm how it's classified under PFIC reporting and what the tax drag looks like on your US return — the headline India return can look very different after IRS treatment.

Getting this mix right — across tax efficiency, repatriation flexibility, and return potential — requires coordinating Indian and overseas tax positions simultaneously. iVentures Wealth works with NRIs and OCIs on exactly this: structuring post-PPF allocations with DTAA, TDS, and repatriation documentation factored in from the outset.

Frequently Asked Questions

Can NRIs invest in PPF?

NRIs cannot open new PPF accounts. However, if a PPF account was opened while the person was a resident Indian, it can be maintained and contributed to until the original 15-year maturity. After that, the account must be closed — no extension is permitted for NRIs.

What is the PPF interest rate for NRIs?

The rate is the same for NRIs and residents: 7.1% p.a. for FY 2025-26, reviewed quarterly by the Government. Failure to notify your bank of your NRI status can cause the rate to revert to the POSA rate of 4.0% p.a.

Can NRIs extend their PPF account after maturity?

No. NRIs cannot use the 5-year block extension facility available to resident Indians. The 15-year maturity date is the closure point — the account must be closed at that time.

What happens to an NRI's PPF account at maturity?

The full maturity amount is credited to the NRO account. Repatriation to a foreign account is then permitted subject to the RBI's USD 1 million per financial year limit, with Form 15CA/CB documentation.

Can NRIs make partial withdrawals from their PPF account?

Yes, from the 6th financial year onwards. The maximum withdrawal is 50% of the eligible balance — calculated as the lower of the 4th preceding or the preceding year-end balance — once per financial year.

Which bank account should NRIs use to contribute to their PPF?

Contributions must come from an NRO account. Contributions from an NRE or FCNR account are not permitted — verify this with your bank before making any deposit.