Key Takeaways

- Indian REITs trade on NSE/BSE — you can start with a single unit at ₹130–375, making real estate accessible at any capital level.

- Direct property investment requires 20–25% down payment plus 5–7% in stamp duty and registration charges — budget for both.

- RERA registration is mandatory protection for under-construction buyers; skipping this check is where many beginners get hurt.

- Tax benefits are significant: Section 24(b) deductions, LTCG treatment after 24 months, and Section 54 reinvestment exemptions reduce your liability substantially.

- Real estate works best inside a diversified portfolio, not as a standalone bet on a single property.

Real estate occupies a unique place in the Indian investor's mind. It feels tangible, it's something you can drive past and point to, and for decades it has rewarded patient buyers in cities like Delhi NCR, Mumbai, and Gurugram. Yet many affluent investors — even those with substantial equity and mutual fund portfolios — hesitate at the threshold. Where do you start? How much capital do you actually need? What are the tax implications?

According to ANAROCK Research, seven major Indian cities recorded 53% aggregate price appreciation between 2019 and Q4 2024, with micro-markets like New Gurugram delivering over 76% in the same period. Those numbers make a case for paying attention.

This guide covers the full spectrum — from listed REITs you can buy today for under ₹400, to direct property investment and the legal checks that protect you. By the end, you'll have a clear framework for evaluating which approach fits your goals, capital, and timeline.

Why Real Estate Is a Powerful Wealth-Building Asset

Real estate generates returns through two distinct mechanisms, and understanding both is essential before committing capital.

Rental income provides predictable cash flow — monthly rent from a tenant. Capital appreciation is the increase in property value over time. In well-chosen micro-markets, these two streams compound: the property earns rent while simultaneously growing in value.

What makes this combination valuable for investors with concentrated equity portfolios is that property values don't move in lockstep with stock markets. When equity markets correct sharply, a well-located residential or commercial property typically holds its value better than listed securities.

That said, real estate is not risk-free — it carries its own risks, discussed below. But the return profile differs from equities in ways that genuinely reduce overall portfolio volatility.

The Micro-Market Matters More Than the City

That volatility-dampening quality is only realized when you pick the right location. ANAROCK data illustrates this clearly: seven-city average appreciation was 53% over five years, but New Gurugram alone delivered 76%. Broad statements about "Indian real estate" appreciating tell you little — specific locality analysis is what drives actual returns.

Two properties in the same city can have vastly different yield and appreciation profiles. The factors that separate them include:

- Proximity to employment hubs and commercial corridors

- Upcoming metro connectivity and infrastructure pipelines

- Supply constraints and new inventory pipeline in the micro-market

- Builder quality and delivery track record

Choosing a city is just the starting point. Choosing the right pocket within that city is where the return is actually determined.

Types of Real Estate Investments for Beginners in India

India's real estate investment options range from outright property ownership to exchange-listed instruments accessible with a few hundred rupees. Your choice comes down to three variables: capital available, how hands-on you want to be, and your risk appetite.

Direct Property Investment (Residential & Commercial)

Buying physical property — an apartment, independent house, or commercial space — is the most direct path. You own the asset outright, control it, collect rent, and benefit from appreciation. The trade-off is capital intensity and illiquidity.

Financial reality of direct purchase:

- Down payment: typically 20–25% of property value

- Stamp duty: 4–6% in Delhi, 5% in Maharashtra (with a 1% concession for women buyers)

- Registration charges: 1% in Delhi, capped at ₹30,000 in Maharashtra

- GST: applicable on under-construction properties

- Brokerage: 1–2% of transaction value

- Annual maintenance: can add ₹5,000–₹25,000+ per month in gated communities

Commercial real estate offers higher rental yields than residential — documented examples from Gurugram's Cyber City have achieved 12% rental yields alongside substantial capital appreciation — but entry costs are higher and vacancy periods can be longer.

Real Estate Investment Trusts (REITs)

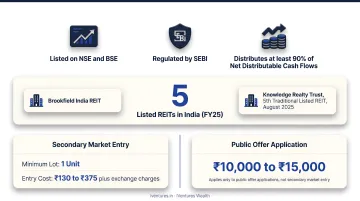

REITs are listed on NSE and BSE, regulated by SEBI, and must distribute at least 90% of net distributable cash flows to unit holders. They offer institutional-quality commercial real estate exposure without the capital requirement of direct ownership.

India's listed REITs (as of FY25):

| REIT | Focus | Market Cap | Unit Price (March 2025) |

|---|---|---|---|

| Embassy Office Parks REIT | Grade-A office | ₹34,645 Cr | ₹365.49 |

| Mindspace Business Parks REIT | Grade-A office | ₹22,829 Cr | ₹374.70 |

| Nexus Select Trust | Retail-led | ₹19,731 Cr | ₹130.20 |

Brookfield India REIT is also listed, and Knowledge Realty Trust became the fifth traditional listed REIT in August 2025. On the secondary market, the minimum lot is one unit — so your actual entry cost is roughly ₹130 to ₹375 plus exchange charges. The ₹10,000–15,000 figure you may see elsewhere applies only to public offer applications.

Fractional Ownership and SM-REITs

SEBI's March 2024 framework created Small and Medium REITs (SM-REITs) — a regulated structure that allows multiple investors to co-own commercial properties through listed schemes. Key parameters:

- Minimum application: ₹10 lakh

- Each scheme: ₹50 crore to below ₹500 crore in assets

- Must distribute at least 95% of net distributable cash flows

- At least 95% of assets must be in completed, revenue-generating property

Important: A legacy fractional platform interest is not automatically an SM-REIT. Verify the SEBI registration number and scheme offer document before investing.

For investors evaluating which of these structures fits their portfolio, iVentures Wealth provides real estate investment advisory — covering REIT selection, SM-REIT due diligence, and how real estate exposure fits within a broader wealth strategy — as part of its SEBI-registered advisory mandate.

How to Get Started: A Step-by-Step Guide

These five steps follow a deliberate sequence. Skipping financial assessment or legal due diligence — the two areas where most first-time buyers lose money — is rarely recoverable without significant cost.

Step 1: Define Your Goals and Strategy

Different objectives require different approaches:

- Regular passive income → REITs or rental residential property in high-demand localities

- Capital growth over 5–10 years → Buy-and-hold in emerging micro-markets with strong infrastructure pipelines

- Short-term profit through flipping → Higher risk, higher execution complexity; not recommended as a first investment

Be honest about your time horizon. A five-year commitment in an illiquid asset requires genuine patience — especially if the property needs to be sold in a soft market.

Step 2: Assess Your Financial Readiness

Before looking at any property, confirm you have:

- Down payment capital (20–25%) held separately from your emergency fund

- A credit score of 750+ (HDFC's benchmark for "excellent" creditworthiness)

- Budget that fully accounts for stamp duty, registration, GST, brokerage, maintenance reserves, and potential vacancy period

- Existing EMI obligations that won't strain cash flow when a home loan is added

A useful planning benchmark: total EMI obligations should not exceed 40% of monthly take-home income. This isn't an RBI rule — it's a lender-specific assessment — but it's a reasonable buffer to plan around.

Step 3: Research the Market

Evaluate each target locality on these factors:

- Infrastructure pipeline (upcoming metro lines, expressways, commercial hubs)

- Employment hub proximity and employer concentration

- RERA registration status for any under-construction project

- Builder track record and delivery history

- Rental yield data from PropTech platforms, compared against your target return

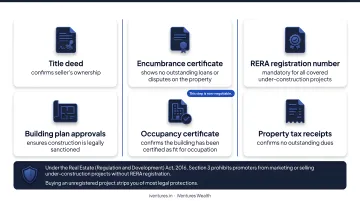

Step 4: Conduct Legal Due Diligence

This step is non-negotiable. Engage a real estate lawyer to verify:

- Title deed — confirms seller's ownership

- Encumbrance certificate — shows no outstanding loans or disputes on the property

- RERA registration number — mandatory for all covered under-construction projects

- Building plan approvals — ensures construction is legally sanctioned

- Occupancy certificate — confirms the building has been certified as fit for occupation

- Property tax receipts — confirms no outstanding dues

Under the Real Estate (Regulation and Development) Act, 2016, Section 3 prohibits promoters from marketing or selling under-construction projects without RERA registration. Buying an unregistered project strips you of most legal protections.

Step 5: Build Your Advisory Team

Once legal diligence is complete, you need the right professionals in place before signing anything. Four roles matter here:

- Real estate lawyer — reviews title, flags encumbrances, and signs off on documentation before funds move

- Mortgage adviser or banker — structures the loan to fit your income profile, tax position, and repayment timeline

- Property manager — manages tenant sourcing, rent collection, and maintenance if you're renting the property out

- SEBI-registered investment adviser — ensures the real estate allocation fits within your broader portfolio across equity holdings, tax exposure, and long-term financial goals

iVentures Wealth evaluates real estate as one component of a client's full financial picture — assessing how a property investment interacts with existing equity positions, tax liabilities, and income requirements before any commitment is made.

Financing Your First Real Estate Investment

Home Loan Basics

RBI's LTV matrix for residential properties:

| Loan Amount | Maximum LTV |

|---|---|

| Up to ₹30 lakh | Up to 90% |

| ₹30 lakh to ₹75 lakh | Up to 80% |

| Above ₹75 lakh | Up to 75% |

Note: stamp duty and registration are not included in the financed cost. Obtain a written investment-property sanction from your lender before paying any non-refundable deposit.

Alternative Financing Options

- Loan Against Property (LAP): For investors with existing unencumbered assets — useful if you need liquidity without selling

- NRI home loans: Available from HDFC, ICICI, SBI; require passport, visa/work permit, NRE/NRO statements, overseas credit report, and sometimes a notarized Power of Attorney

- Developer payment plans: Construction-linked (payments tied to construction milestones) vs. time-linked (fixed schedule regardless of progress) — construction-linked generally carries less risk

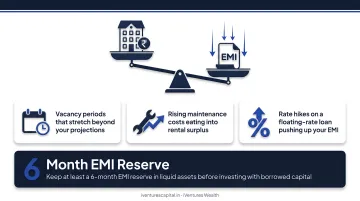

The Over-Leveraging Risk

Taking the maximum available loan makes sense on paper when rental income covers the EMI. That logic unravels quickly under three common conditions:

- Vacancy periods that stretch beyond your projections

- Rising maintenance costs eating into rental surplus

- Rate hikes on a floating-rate loan pushing up your EMI

Rule of thumb: Keep at least a 6-month EMI reserve in liquid assets before investing with borrowed capital.

Tax Benefits of Real Estate Investing in India

Section 24(b): Home Loan Interest Deduction

For a let-out (rented) investment property, the full interest paid on the home loan is deductible against rental income — there's no property-level cap. Key limits to know:

- If house property income turns negative after deduction, the cross-head loss set-off against other income is capped at ₹2 lakh per year

- The remaining loss carries forward for up to 8 years

- For self-occupied property, the deduction is capped at ₹2 lakh in aggregate across qualifying properties

Long-Term Capital Gains (LTCG) Tax

Property held for more than 24 months qualifies as a long-term capital asset.

Post July 23, 2024 (Budget 2024 changes):

- Transfers on or after July 23, 2024: 12.5% LTCG without indexation

- For property acquired before that date by a resident individual or HUF: the law protects the taxpayer where the older 20% with indexation computation produces a lower tax outcome

Always run both calculations before selling. The interaction between acquisition date, transfer date, and the applicable computation can materially change your after-tax proceeds.

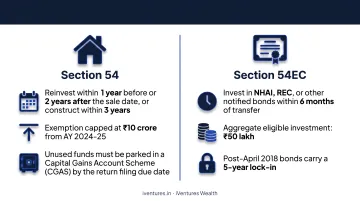

Reinvestment Exemptions: Sections 54 and 54EC

These exemptions exist precisely to reduce the LTCG tax burden calculated above — but timing and eligibility conditions matter.

Section 54: Sell a long-term residential property and reinvest the capital gains into another residential property in India to claim exemption. Conditions:

- Reinvest within 1 year before or 2 years after the sale date, or construct within 3 years

- Exemption is capped at ₹10 crore from AY 2024-25

- Unused funds must be parked in a Capital Gains Account Scheme (CGAS) by the return filing due date

Section 54EC: Invest eligible land/building LTCG in specified bonds (NHAI, REC, or other notified issuers) within 6 months of transfer. The aggregate eligible investment is ₹50 lakh, and post-April 2018 bonds carry a 5-year lock-in.

REIT Tax Treatment

REIT distributions are not a single tax category — each component is taxed differently:

- Interest from SPV and rent from directly held property: Retain their character, taxable to the unit holder; TDS is typically 10% for residents

- SPV dividend: Generally taxable when the SPV uses Section 115BAA; otherwise may be exempt

- Return of capital: Tested under Section 56(2)(xii) — the excess of cumulative covered distributions over issue price and amounts already taxed

Read each distribution statement component by component. At HNI and UHNI holding sizes, the difference in tax treatment across these components can run into several lakhs annually — making the structure of your REIT holdings as important as the allocation itself.

Common Mistakes to Avoid as a First-Time Investor

Most first-time real estate investors in India lose money not from bad luck, but from avoidable mistakes. Here are the three that show up most often.

Buying on emotion, not metrics. A property that feels right is not the same as one that works financially. Calculate gross rental yield (annual rent ÷ total acquisition cost) and compare it against alternative investments before committing. The US-origin "2% rule" (monthly rent = 2% of purchase price, implying 24% annual gross yield) is not achievable in Indian metros — don't use it as a benchmark here.

Ignoring hidden costs. First-time buyers routinely underestimate total acquisition cost. Beyond the purchase price, budget for:

- Stamp duty (4–6% depending on state and buyer gender)

- Registration charges

- GST on under-construction properties

- Brokerage (1–2%)

- Interior fit-out or renovation

- Annual maintenance charges

- Property management fees if outsourced

Once you have the numbers right, the legal side deserves equal rigour.

Skipping legal and RERA checks. Title disputes and unregistered properties can result in years of litigation — and no rental income while the case progresses. RERA registration for under-construction projects is buyer protection mandated by law. There's no shortcut worth taking here.

Frequently Asked Questions

Can I invest ₹10,000 in real estate?

Yes — listed REITs trade on NSE/BSE as single units, with prices ranging from approximately ₹130 to ₹375 per unit as of early 2025. SEBI-regulated SM-REITs require a minimum ₹10 lakh application. Both routes provide real estate exposure without direct property ownership.

What is the best real estate investment for a beginner?

For most beginners, REITs offer the best starting point — low capital requirement, daily liquidity, and no property management burden. Those with sufficient capital may prefer a buy-and-hold residential property in a well-researched micro-market for direct ownership benefits. Your choice should reflect available capital, time horizon, and whether you prioritise current income or long-term appreciation.

What is the 2% rule for properties?

The 2% rule is a US real estate screening tool: monthly rent should equal at least 2% of a property's purchase price (24% gross annual yield). This benchmark is not achievable in Indian metros, where residential yields run far lower. Use it as a directional filter for comparison, not a pass/fail criterion in India.

How much money do I need to start investing in real estate in India?

The spectrum is wide: REITs require one exchange unit (₹130–375 as of March 2025); SM-REITs require ₹10 lakh minimum; fractional platforms vary. Direct residential property in major metros typically requires a ₹20–50 lakh down payment or more — before stamp duty and other transaction charges.

What is the difference between REITs and direct real estate investing?

Direct investment means owning a physical property — full control, higher capital requirement, illiquidity, and active management responsibility. REITs offer exchange-traded exposure to a diversified commercial property portfolio, with daily liquidity and no management burden, but no direct ownership or control over individual assets.

What are the main tax benefits of investing in real estate in India?

Three primary benefits apply to Indian real estate investors:

- Section 24(b): Home loan interest deduction against rental income

- LTCG treatment: Applies after 24 months of holding, with indexed computation protecting pre-July 2024 acquisitions

- Section 54 exemption: Defers capital gains tax when proceeds are reinvested in another residential property within the prescribed timeframe