The term comes up regularly in UHNI and family office conversations, yet most investors encounter it without a clear picture of how the mechanics actually work. What does a feeder fund do? What does it cost? And what should an investor scrutinise before committing capital?

This article answers those questions directly — covering the master-feeder structure, the genuine advantages it offers, the risks that deserve serious attention, and how feeder funds differ from fund-of-funds.

Key Takeaways

- A feeder fund pools capital from multiple investors and channels it into a single master fund that handles all investment activity

- The structure lets individual investors access high-minimum institutional funds — private equity, hedge funds, VC — that would otherwise be out of reach

- Core benefits: access to institutional-grade strategies, economies of scale, and targeted sector exposure

- Key risks: illiquidity (often 7–10 years), layered fees, and tax complexity for cross-border structures

- Feeder funds and fund-of-funds are not the same — feeder funds target one master fund; fund-of-funds diversify across many

What Is a Feeder Fund and How Does It Work?

A feeder fund is an investment vehicle that pools capital from a group of investors and directs that collective capital into a single, larger master fund: the entity where all portfolio decisions, trading activity, and asset management actually take place. The feeder itself holds no investments directly — it is a conduit.

Mayer Brown describes a feeder as an investment vehicle — typically a limited partnership — that pools investor commitments and invests that capital into a master fund directing the portfolio.

The structure is most commonly used in:

- Private equity funds (SEBI Category II AIFs in India)

- Hedge funds (SEBI Category III AIFs)

- Venture capital funds (SEBI Category I AIFs)

The rationale is practical: professional asset managers need to serve different investor types — domestic taxable, tax-exempt, non-resident — without running separate strategies for each. A single master fund makes that possible, and the mechanics of how capital flows through it are straightforward.

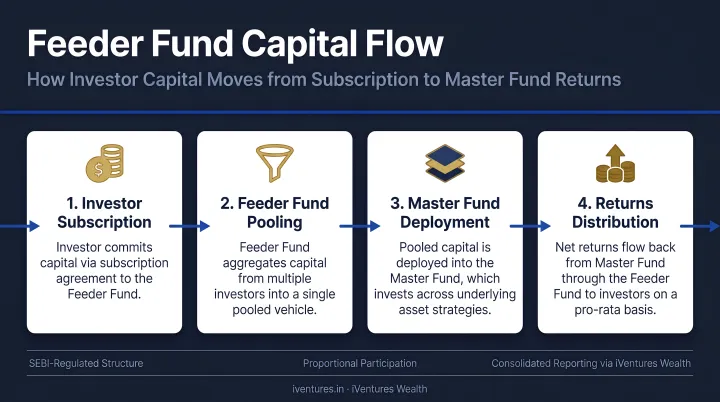

How Capital Flows Through the Structure

The two-tier flow is straightforward:

- Investors contribute capital to their respective feeder fund

- The feeder pools contributions from all its participants

- Pooled capital flows into the master fund, which deploys it across investments

- Returns flow back down — the master fund allocates income, gains, and distributions proportionally to each feeder based on its share

One master fund can connect to multiple feeders simultaneously. Each feeder can serve a different investor profile — domestic taxable investors, tax-exempt institutions, NRIs — with different fee structures, minimum investment amounts, and legal domiciles, while the master fund remains centralised and unified.

For an individual investor, the feeder fund is the practical entry point. Without it, the minimum ticket to participate directly in a top-tier PE or hedge fund would typically run into several crores. That threshold puts direct access out of reach for most — and out of proportion with what any single strategy should represent in a well-diversified portfolio.

Key Benefits of Investing Through Feeder Funds

The advantages below are operational and outcome-based — how feeder funds change what an investor can access, how efficiently capital is deployed, and what portfolio goals become achievable.

Access to Institutional-Grade Investment Opportunities

Top-tier private equity and hedge funds impose minimum commitments that have historically excluded individual investors. According to Preqin's private capital fund terms data, funds managing over $1 billion carry a median minimum LP commitment of $5 million (roughly ₹40–42 crore at current rates). SEBI's AIF regulations set the minimum per-investor threshold at ₹1 crore — the regulatory floor, not the practical reality of top-quartile fund access.

Feeder funds resolve this by aggregating commitments from multiple investors. The combined pool meets the master fund's threshold; each individual investor participates in proportion to their contribution.

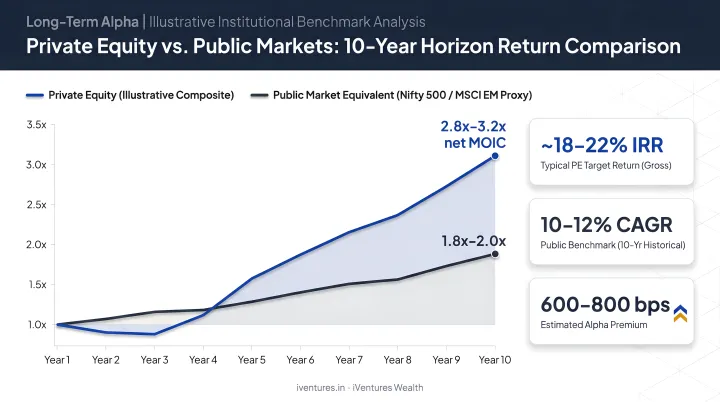

Why this matters: Cambridge Associates data shows the US private equity 10-year horizon return stood at 15.05% as of June 2024, with a 276-basis-point value-add over the Russell 3000. For UHNIs and family offices focused on wealth compounding over multi-decade horizons, this return differential is material, and feeder structures are often the only way to access it.

When this matters most: Investors with ₹1–5 crore available for alternatives who lack the ₹20–50 crore typically required to access a top-tier PE or hedge fund directly. The feeder structure bridges that gap.

Economies of Scale and Cost Efficiency

By consolidating capital into a single master fund, the structure reduces per-investor trading costs, administrative duplication, and counterparty management overhead. The SEC confirmed that master-feeder structures spread fixed costs across a larger asset base, enabling smaller funds to access advisory fee breakpoints that would otherwise be out of reach.

The master fund benefits from:

- Better execution prices on larger trade sizes

- More favourable broker terms from scale

- Streamlined portfolio operations across a single unified vehicle

Fee trends confirm the pressure: Preqin data shows mean management fees for 2024-vintage buyout funds fell to 1.74%, down from 1.85% in 2023 — in part driven by the scale dynamics that feeder structures help create.

When this matters most: When alternative allocations are significant enough that cost drag becomes meaningful. For UHNIs building structured alternative sleeves across multiple vehicles, the efficiency difference compounds over a 7–10 year fund life.

Targeted Portfolio Positioning and Sector Exposure

Feeder funds are typically tied to master funds with a specific mandate: a particular geography, sector (AI, healthcare, infrastructure), or strategy (buyout, secondaries, venture capital). Where a diversified fund spreads capital across many sectors and themes, a feeder fund enables a precise, thesis-driven allocation — Indian infrastructure growth, global secondaries, or healthcare technology — with a dedicated position sized to conviction.

For portfolio construction, this lets UHNIs and family offices add deliberate "accents" to their asset mix: exposures that align with thematic or cyclical views and don't overlap with positions already held. That correlation benefit is something broad diversification cannot replicate.

This approach is most relevant for investors with an already well-diversified core portfolio seeking high-conviction alternative exposure. The specific mandate ensures the allocation adds something genuinely new — not a dressed-up version of what they already own.

Risks and Limitations Investors Should Understand

Illiquidity and Lock-Up Periods

FINRA states that feeder funds investing in private capital may have lock-up periods extending 10 years or longer. Hedge fund structures typically offer redemption windows only monthly, quarterly, or annually — and often impose a minimum lock-up of one year.

Beyond standard lock-ups, fund managers can impose redemption gates during volatile market periods, further restricting access. Investors must treat feeder fund capital as unavailable for the full investment horizon.

The rule is simple: only commit capital you can afford to leave entirely untouched for 7–10 years.

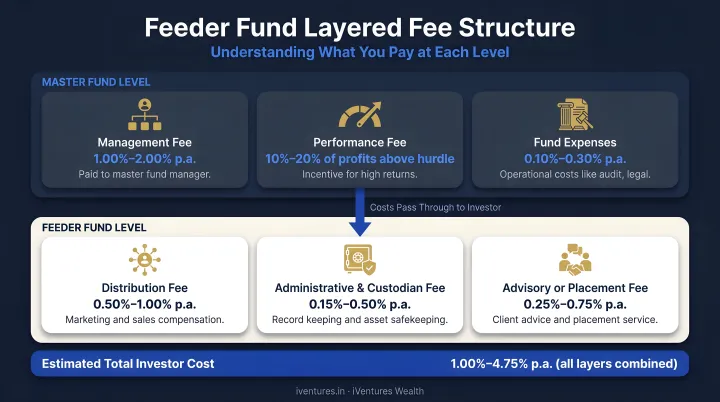

Layered Fees and Cost Complexity

The master-feeder structure introduces two distinct layers of fees:

| Fee Layer | Typical Range |

|---|---|

| Master fund management fee | 1.6%–2.0% annually |

| Master fund performance fee (carry) | 20% of profits, often with 8% hurdle |

| Feeder fund administrative costs | Variable — added on top of master-level fees |

Preqin data shows 82% of recent direct private capital funds use a 20% carry structure, and 52% include an 8% hurdle rate. When feeder-level administrative costs layer on top, net returns to the end investor are meaningfully lower than gross fund performance.

Review the offering documents. The combined fee burden — not just the headline management fee — is what determines net returns.

Transparency and Tax Complexity in India

Unlike listed funds, feeder funds are not publicly traded and offer limited visibility into the master fund's underlying holdings. In India, this complexity compounds when cross-border structures are involved:

- Domestic feeder funds investing into Indian AIFs fall under SEBI's AIF Regulations, with Category I/II funds required to be close-ended with a minimum 3-year tenure

- Cross-border structures routing capital into offshore PE or hedge funds are subject to FEMA guidelines, RBI's Liberalised Remittance Scheme (LRS limit: USD 250,000 per financial year for resident individuals), and SEBI's AIF overseas investment cap of 25% of investible funds

- For NRIs who are US tax persons, offshore feeder fund investments may trigger PFIC (Passive Foreign Investment Company) classification, requiring IRS Form 8621 reporting — with separate QEF and mark-to-market election considerations

Each of these dimensions carries distinct compliance obligations and tax consequences that vary by investor residency status. Given the jurisdiction-specific implications, consulting a SEBI-registered investment adviser and qualified tax professional before committing capital is essential. iVentures Wealth works with NRIs and UHNIs on exactly this type of cross-border structuring — covering DTAA optimisation, FEMA compliance, and PFIC/GILTI exposure management.

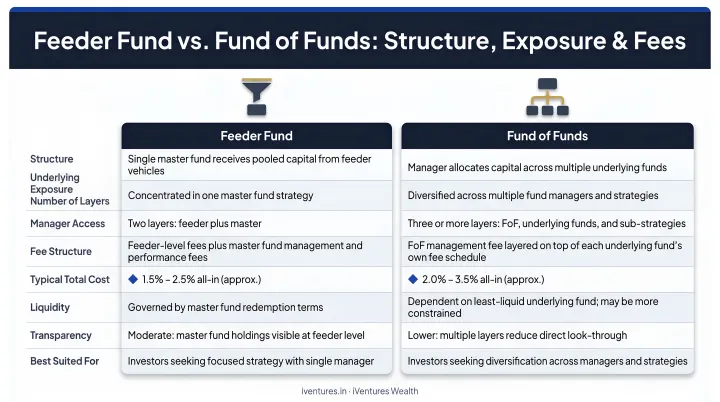

Feeder Funds vs. Fund of Funds: Understanding the Difference

These two structures are often conflated. They work differently.

| Feeder Fund | Fund of Funds | |

|---|---|---|

| Invests in | One master fund | 10–20 underlying funds |

| Exposure type | Concentrated, single strategy | Diversified across managers |

| Return potential | Higher if master fund performs strongly | Moderate — upside diluted by diversification |

| Concentration risk | Higher | Lower |

| Fee layers | Master + feeder | FoF + all underlying funds |

SEBI defines a Fund of Funds as an AIF that invests in another AIF — the distinguishing characteristic being that it spreads capital across multiple underlying funds and managers rather than channelling everything into one.

In practice, both structures serve distinct roles in a well-constructed portfolio. Family offices and HNIs often anchor their alternatives allocation in a FoF for broad diversification, then layer in feeder funds to express high-conviction, thematic views. The FoF provides stability; the feeder fund carries the targeted upside.

How to Get the Most Value from Feeder Fund Investments

Feeder fund investing works best as part of deliberate portfolio construction — not as a reactive or opportunistic allocation. Before committing, assess:

- Overall asset allocation — does the feeder fund fill a genuine gap or duplicate existing exposure?

- Liquidity requirements — can you sustain the 7–10 year lock-up without stress?

- Risk tolerance — the concentrated nature of feeder funds amplifies both upside and downside

Due diligence on the master fund is non-negotiable. The 2018 Cayman Grand Court ruling in In the Matter of Ardon Maroon Asia Master Fund illustrates why documentation matters: a $15 million redemption request failed because the feeder fund did not serve a separate written notice on the master as required by its constitutional documents. The court applied the plain meaning of the fund documents — not industry practice — and ruled the redemption ineffective.

Minimum due diligence checklist for the master fund:

- Track record across full market cycles, not just peak-performance periods

- Fund manager credibility, team stability, and succession

- Investment strategy, mandate clarity, and portfolio concentration

- Fee structure — management fee, carry, hurdle rate, and feeder-level costs

- Legal robustness of the feeder arrangement and documentation protocols

That checklist looks different depending on where you sit. For UHNIs, NRIs, and family offices in India, feeder fund selection also involves SEBI compliance, cross-border tax structuring, and AIF-specific regulatory considerations. iVentures Wealth — a SEBI-registered RIA with a CFA-led research team and 20+ years of fiduciary advisory experience — guides investors through AIF selection, alternative investment due diligence, and cross-border structuring to ensure the chosen arrangement fits both financial goals and regulatory requirements.

Frequently Asked Questions

What is a feeder fund?

A feeder fund pools capital from multiple investors and routes it into a larger master fund, where all investment decisions are made. This structure lets individual investors access institutional-grade PE or hedge funds that would otherwise require commitments beyond their individual capacity.

What is the difference between a feeder fund and a normal fund?

A normal standalone fund directly manages its own portfolio of assets. A feeder fund does not hold investments directly — it collects investor capital and routes it into a master fund that manages the actual portfolio. The feeder is a conduit; the master fund is where the investment activity happens.

What is the difference between a feeder fund and a fund of funds?

A feeder fund invests all capital into a single master fund, giving concentrated exposure to one strategy and manager. A fund of funds diversifies across 10–20 underlying funds, offering broader risk distribution but typically lower concentration-driven upside and an additional layer of fees.

Is a feeder fund the same as a bank account?

No. A feeder fund is a structured investment vehicle — typically a limited partnership or similar legal entity — that pools investor capital and invests it into a master fund. Unlike a bank account, it is illiquid, carries full investment risk, and is subject to fund-level regulatory and tax obligations.

What are the typical fees in a feeder fund structure?

Feeder structures carry two layers of costs: master fund charges (typically a 1.6%–2% management fee and 20% performance/carry fee) plus feeder-level administrative costs. Review the combined fee burden in the offering documents carefully — it directly affects your net returns.

Are feeder funds regulated for investors in India?

Domestic feeder funds investing into Indian AIFs fall under SEBI's AIF Regulations (2012). Cross-border structures are also subject to FEMA guidelines, RBI's LRS framework, and SEBI's overseas investment limits. Given the multi-regulatory overlap, work with a SEBI-registered adviser before investing.