The problem is not that the form is complex. It is that errors in it — a wrong purpose code, an inflated cumulative figure, a missing prior transaction — can trigger incorrect TCS deductions, delay the remittance, or in serious cases, create FEMA compliance exposure. For affluent investors making high-value overseas remittances, the stakes are higher still.

This guide covers what the LRS Declaration is, why it exists, how to complete it correctly, and the misconceptions that cause most errors.

Key Takeaways

- The LRS Declaration (Form A2) is a FEMA-mandated document your AD bank requires for every outward remittance under LRS

- The annual limit is USD 2,50,000 per resident individual — cumulative across all banks, tracked via PAN

- From April 1, 2025, TCS is waived on general LRS remittances up to ₹10 lakh per financial year

- Errors in purpose codes or prior transaction amounts directly affect TCS calculation

- The AD bank certifies the form, but compliance responsibility always rests with the remitter

What Is the LRS Declaration?

The LRS Declaration is the formal document a resident individual submits to their Authorised Dealer (AD) bank each time they remit foreign exchange abroad. Its legal basis is FEMA 1999: Section 5 governs current account transactions (education, travel, medical treatment), while Section 6 governs capital account transactions (overseas investments, foreign bank accounts).

The operational form is RBI's Form A2, titled "Application for Remittance Abroad," with an extended version — Annexure V, titled "Form A2 – Application cum Declaration" — used by AD banks as the standard submission format.

What the Form Captures

Per RBI's Form A2 and Annexure V, the declaration requires:

- Remitter identity — full name, PAN (mandatory for all LRS transactions), account number, and address

- Purpose of remittance — selected from RBI's prescribed purpose code list

- Amount and currency — in foreign currency with the rupee equivalent

- Beneficiary details — name, bank, and account details of the recipient abroad

- Aggregate remittance declaration — confirmation that total foreign exchange remitted through all sources in the current financial year (April–March) is within the prescribed annual limit of USD 2,50,000

Understanding where these fields sit within the broader framework matters: LRS is the RBI policy that permits outward remittances, while Form A2 is the operational instrument through which each remittance under that framework is authorised and documented.

Responsibility Split: Remitter vs. AD Bank

The AD bank certifies the declaration based on documents submitted. The remitter signs a declaration that the purpose stated is accurate and that the funds will be used only for that purpose. FEMA compliance responsibility sits with the remitter — an incorrect or false declaration carries regulatory consequences for the remitter, not the bank.

One specific rule worth noting: when the remitter is a minor, the natural guardian must countersign the Form A2 and assumes legal responsibility for FEMA compliance.

Why the LRS Declaration Is Required

The RBI mandates this declaration for three distinct reasons, each serving a different regulatory function.

1. Annual cap monitoring. Per the RBI's LRS FAQ, the USD 2,50,000 annual limit applies per resident individual, per financial year, across all banks. PAN is mandatory for all LRS transactions, and RBI's daily reporting framework for AD banks enables cross-bank monitoring of cumulative remittances against this limit.

2. Purpose verification. Every outward remittance must be for a purpose permissible under FEMA. The purpose code the remitter selects on Form A2 determines which regulatory schedule applies — and directly affects TCS.

3. TCS calculation. The declared purpose and the cumulative remittance figure together determine how much Tax Collected at Source the AD bank must collect. An incorrect purpose code or a misstated cumulative figure will produce the wrong TCS deduction.

Understanding TCS calculation is particularly important given recent legislative changes. Here's the current framework.

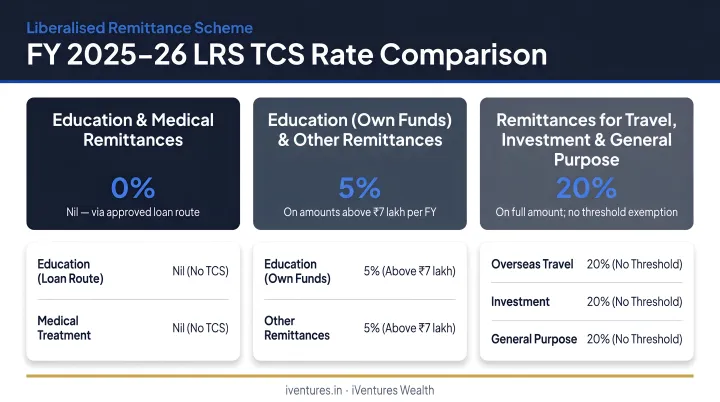

FY 2025-26 TCS Framework

Union Budget 2025 raised the TCS threshold on LRS remittances, effective April 1, 2025. The current rates:

| LRS Category | Threshold | TCS Rate Above Threshold |

|---|---|---|

| General remittances | ₹10 lakh aggregate per financial year | 20% |

| Self-funded education or medical | ₹10 lakh aggregate per financial year | 5% |

| Education funded by a Section 80E loan | No threshold | No TCS collected |

For capital account transactions — overseas equity investments, foreign bank accounts, immovable property abroad — the AD bank must also verify the source of funds. Per the RBI's LRS FAQ, banks may request bank statements for the previous year or copies of the latest income tax assessment order or return filed by the remitter.

This documentation requirement is one reason remitters making capital account transactions benefit from structured advisory support. iVentures Wealth's global investing service includes LRS declaration submission and PAN detail coordination as part of the advisory process, helping ensure TCS compliance from the outset.

How to Complete the LRS Declaration

The form is submitted each time a remittance is made through the designated AD bank. Some banks accept digital submissions; others require physical forms. The core information required is consistent across formats.

Step 1: Remitter and Beneficiary Details

Enter the remitter's full name, PAN, account number, and address. Add the recipient's name, bank name and address, and account number abroad. For capital account transactions, the AD bank will typically also ask for the previous year's bank statements or the latest ITR as source-of-funds evidence.

Step 2: Purpose Code

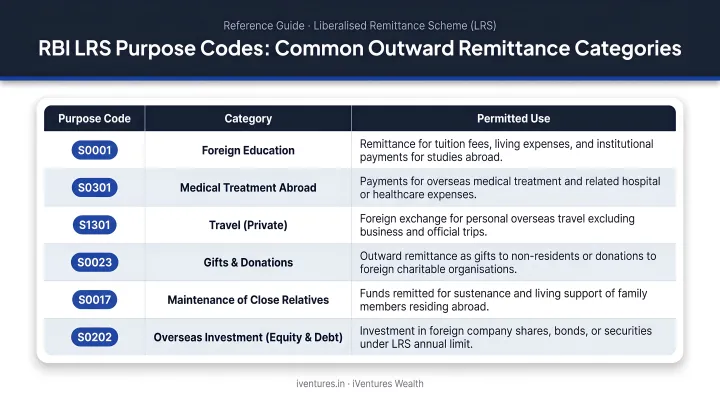

Select the correct RBI purpose code. This is not a formality — it determines the applicable TCS rate and the regulatory schedule under which the remittance is processed.

Commonly used purpose codes include:

| Purpose | RBI Code |

|---|---|

| Education (fees and hostel) | S0305 |

| Medical treatment abroad | S0304 |

| Family maintenance | S1301 |

| Overseas equity investment | S0001 |

| Overseas debt securities | S0002 |

| Personal gifts and donations | S1302 |

Selecting the wrong code — for example, coding an overseas equity investment as family maintenance — will produce incorrect TCS treatment and may flag the transaction for review.

Step 3: Prior Remittances in the Current Financial Year

Declare all previous outward remittances made via bank transfer in the current financial year (April–March), including the date, amount in foreign currency, and the AD branch details for each.

What must NOT be included here:

- Credit or debit card international transactions

- The current remittance being submitted

Including the current transaction inflates the cumulative figure. Card transactions are tracked separately and are not part of this declaration table.

Step 4: Supporting Documents and Submission

Documents typically required alongside the form:

- PAN card — mandatory for all LRS transactions

- Passport — required for identification

- Valid ID with address proof — note that PAN is not accepted as address proof for remittances

- Purpose-specific documents — admission letter or fee invoice for education; property agreement or investment account opening documents for capital account transactions

Once documents are verified, the remitter signs the declaration — digitally or physically — and submits it to the AD bank before payment instructions are finalised.

For HNI and UHNI clients making overseas investment remittances, the steps extend beyond the standard form. iVentures Wealth supports clients through each stage of this process:

- KYC completion with the AD bank

- Opening a global trading and custodian account

- Submitting the LRS declaration with PAN for TCS compliance

- Transferring funds via wire transfer

iVentures Wealth handles the documentation advisory at each stage, reducing errors and ensuring the remittance is structured correctly from the outset.

Key Factors and Common Misconceptions

Several errors appear consistently in LRS declarations, particularly among individuals remitting without professional guidance. The four misconceptions below account for the majority of compliance failures.

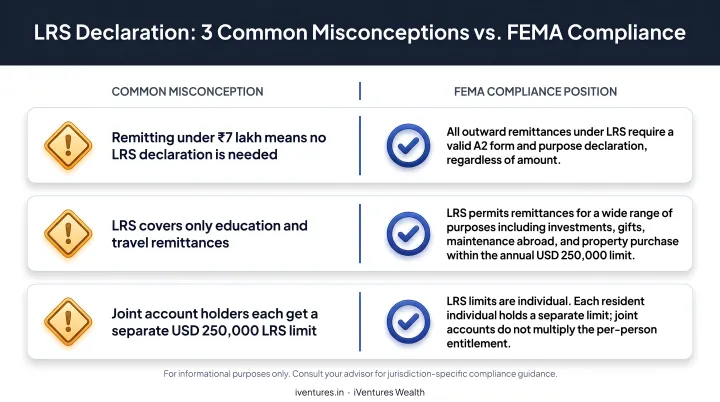

| Misconception | The Correct Position |

|---|---|

| The USD 2,50,000 limit applies per transaction | It is the aggregate annual limit across all outward remittances in a financial year, linked to the remitter's PAN across all AD banks |

| Using multiple banks creates separate sub-limits | PAN-linked reporting means the cumulative figure follows the individual, not the institution |

| AD bank certification removes the remitter's legal liability | The AD certifies in good faith based on submitted documents — FEMA compliance responsibility, including declaration accuracy, stays with the remitter |

On family pooling: The RBI's LRS FAQ permits consolidation of family remittances, provided each member complies with LRS terms individually.

For capital account transactions — overseas property, foreign investments — pooling is only permitted where the remitting family member is a co-owner or co-partner in the asset. One member cannot remit on behalf of another's individual investment or foreign bank account.

When the LRS Declaration May Not Apply or Has Variations

Who Is Outside LRS Scope

LRS applies exclusively to resident individuals under FEMA. The following are not eligible:

- Non-resident Indians (NRIs) — they use NRE, NRO, and FCNR account routes

- Companies, HUFs, trusts, and partnership firms

- Sole proprietors — personal and business remittances share the same USD 2,50,000 annual cap; no separate limit exists for the proprietorship

This matters most for sole proprietors and family businesses: if you remit USD 2,50,000 in a personal capacity, you cannot remit another USD 2,50,000 as the business owner. The LRS framework does not carve out a business sub-limit.

Situations Where the Limit Can Be Exceeded

RBI does permit remittances beyond the USD 2,50,000 annual limit in specific genuine cases:

- Medical treatment abroad — based on estimates from a doctor or hospital in India or abroad

- Studies abroad — based on estimates from the institution abroad

- Emigration — where the emigrating country requires a higher amount

These exceptions are purpose-specific and do not extend to investments, property purchases, or gifts.

Other Process Variations

Two situations require additional attention:

- Education funded by a Section 80E loan — no TCS is collected on the remittance (Finance Bill 2025, effective April 1, 2025); the lending bank's transaction details serve as supporting documentation

- Minor student as beneficiary — the natural guardian signs the LRS declaration and bears full compliance responsibility

Conclusion

The LRS Declaration is a legal instrument under FEMA — it determines how each outward remittance is classified for tax purposes, confirms the transaction is within the annual limit, and establishes that the purpose is permissible. Signing it without understanding what each field means is a genuine compliance risk, not just a paperwork formality.

For most education or travel remittances, careful completion and correct purpose codes are sufficient. For high-value overseas investment remittances, the requirements are more demanding. Before any such remittance is processed, each of the following requires specific attention:

- Source-of-funds documentation

- Correct purpose code selection

- Accurate cumulative remittance figures

- TCS category verification

iVentures Wealth integrates LRS compliance into its global investing advisory process: KYC, LRS declaration submission with PAN for TCS compliance, wire transfer coordination, and post-remittance reporting including capital gains computation and TCS certificates.

For family offices, CXOs, and HNI investors making repeated overseas investment remittances, this advisory structure ensures declarations are accurate and consistent across transactions — rather than reviewed in isolation at ITR filing time.

Frequently Asked Questions

What is the LRS declaration form?

It is Form A2 — also referred to as the A2 cum LRS Declaration — that resident individuals must submit to their Authorised Dealer bank each time they remit money abroad under LRS. The form declares the purpose, amount, and prior foreign exchange transactions made in the current financial year.

What is the purpose of an LRS declaration?

The declaration ensures the remittance is for a permissible purpose under FEMA, allows the AD bank to verify compliance with the USD 2,50,000 annual cap, and determines the Tax Collected at Source applicable to the transaction.

Who must countersign the LRS declaration for a minor?

The natural guardian must countersign Form A2 and takes legal responsibility for FEMA compliance and the annual limit.

What documents are typically required along with the LRS declaration?

Mandatory documents include a PAN card, passport, and a valid ID with address proof (PAN is not accepted as address proof). Purpose-specific documents — such as an admission letter or fee invoice for education — must also be included.

What happens if there is an error in the LRS declaration?

Errors can trigger incorrect TCS deduction, transaction delays, or outright rejection by the AD bank. A corrected declaration must then be submitted, and any excess TCS can only be reclaimed via the annual ITR filing.

Is the LRS declaration required for every outward remittance?

A declaration must be submitted for each remittance transaction through an AD bank under LRS. The cumulative USD 2,50,000 annual limit applies across all such transactions and is tracked via the remitter's PAN.