Introduction

For years, Indian HNIs, NRIs, and family offices seeking global exposure faced the same frustrating tradeoff: foreign brokerage accounts with compliance complexity, or domestic international feeder funds with high costs and limited control. GIFT City mutual funds offer a third path — regulated, USD-denominated access to global markets through an Indian jurisdiction.

According to IFSCA's June 2025 statistics, GIFT City now hosts 177 fund management entities managing 272 funds — a figure that has grown significantly from 162 entities and 229 funds just three months earlier. The retail mutual fund category within this ecosystem is still nascent — only 2 retail schemes counted as of that report — but fund launches and investor interest are accelerating.

This guide covers:

- What GIFT City mutual funds are and how they differ from domestic options

- The types of funds available today

- Who is eligible to invest

- A step-by-step process to get started

- Tax treatment and key risks to weigh before committing capital

Key Takeaways

- GIFT City mutual funds are IFSCA-regulated, USD-denominated schemes that give both resident Indians and NRIs access to global equities and indices

- Two categories exist: actively managed global equity funds and passive index-tracking funds (S&P 500, Nasdaq 100)

- Resident Indians can invest up to USD 250,000 per financial year via RBI's Liberalised Remittance Scheme (LRS)

- Most schemes require a minimum of USD 5,000 to start; IFSC exchange transactions attract no STT, CTT, or stamp duty

- Tax treatment differs between residents and NRIs, making professional advice important before committing capital

What Are GIFT City Mutual Funds?

GIFT City — Gujarat International Finance Tec-City — is India's first and only International Financial Services Centre (IFSC), located in Gandhinagar, Gujarat. Under FEMA's IFSC Regulations 2015, financial institutions operating within GIFT City are treated as persons resident outside India, meaning all transactions occur in foreign currencies.

For practical purposes, investing through GIFT City is structurally equivalent to investing through an offshore financial centre.

GIFT City mutual funds are mutual fund schemes launched by IFSCA-regulated asset management companies operating within this zone. They invest in global equities, indices, debt, and international assets denominated in USD or other foreign currencies — entirely distinct from domestic SEBI-regulated funds.

The Regulator: IFSCA

The International Financial Services Centres Authority (IFSCA), established under the IFSCA Act 2019, acts as a single unified regulator for banking, capital markets, insurance, and fund management within GIFT City. The current framework is governed by the IFSCA Fund Management Regulations, 2025, notified on February 19, 2025, replacing the 2022 regulations.

This unified approach replaces the fragmented multi-regulator model (RBI + SEBI + IRDAI) that applies to domestic financial activity. The consolidation reduces compliance friction for fund managers and lowers structural overhead for investors — a meaningful distinction when evaluating cost efficiency.

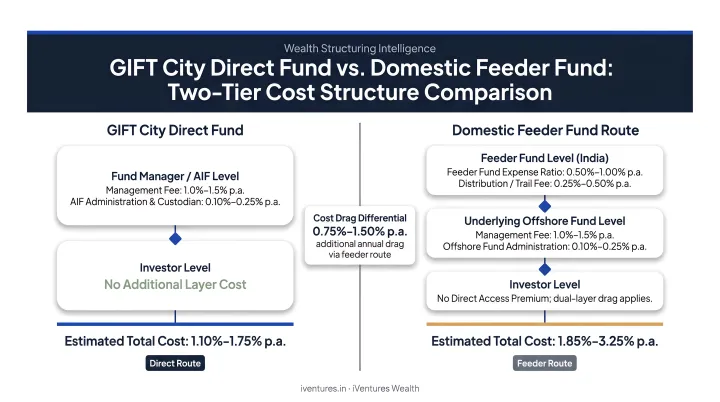

GIFT City Funds vs. Domestic International Feeder Funds

This distinction matters for cost-conscious investors:

- GIFT City funds (like DSP Global Equity Fund) hold global assets directly — single-layer structure, one set of fees

- Domestic international feeder funds route capital through a two-tier structure: a feeder fund investing into a master fund, with fees charged at both layers

- The single-layer structure of direct GIFT City equity funds typically produces a lower total cost of ownership

That said, not every GIFT City fund is single-layer. The PPFAS S&P 500 and Nasdaq 100 offerings are IFSC-domiciled fund-of-funds that invest into ETFs and UCITS funds — still efficient, but structurally distinct from a direct-holding fund.

Types of GIFT City Mutual Funds

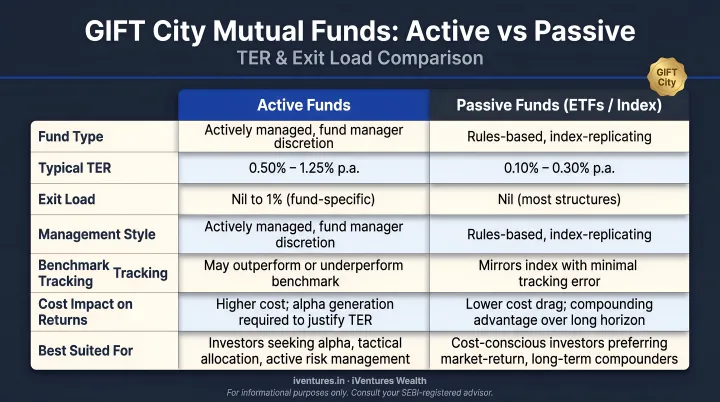

Two broad categories of GIFT City mutual funds are currently available to retail investors: actively managed global equity funds and passive index-tracking fund-of-funds.

Actively Managed Funds

DSP Global Equity Fund (by DSP Fund Managers IFSC Pvt. Ltd.) is the primary example of an active GIFT City retail fund. It builds a concentrated portfolio of 30–50 global stocks across the US, Europe, and Asia, with the fund manager making stock selection and allocation decisions.

Key terms (verify with official scheme documents before investing):

- Class A (Regular): up to 1.75% p.a. TER

- Class B (Direct): up to 1.00% p.a. TER

- Exit load: 1% if redeemed within 24 months; nil thereafter

- Minimum investment: USD 5,000 initial; USD 500 additional

Passive Index Funds

PPFAS Alternate Asset Managers IFSC Pvt. Ltd. (which received its Retail FME licence in April 2025) has launched two passive options:

Parag Parikh IFSC S&P 500 Fund of Fund — invests in ETFs/UCITS tracking the S&P 500 index:

- Direct: 0.30% p.a. (max 0.35% including underlying ETF costs)

- Regular: 0.60% p.a. (max 0.65%)

- No exit load; no lock-in

- Minimum: USD 5,000 initial; USD 500 top-up

Parag Parikh IFSC Nasdaq 100 Fund of Fund — 90–100% in Nasdaq 100 ETFs/UCITS:

- Direct: 0.30% p.a. (max 0.55%)

- Regular: 0.60% p.a. (max 0.85%)

- No exit load; no lock-in

- Minimum: USD 5,000 initial; USD 500 top-up

Active vs. Passive: At a Glance

| DSP Global Equity (Active) | PPFAS IFSC Funds (Passive FoF) | |

|---|---|---|

| Underlying exposure | 30–50 hand-picked global stocks | S&P 500 / Nasdaq 100 index replication |

| TER — Regular | Up to 1.75% p.a. | 0.60–0.85% p.a. |

| TER — Direct | Up to 1.00% p.a. | 0.30–0.55% p.a. |

| Exit load | 1% within 24 months | None |

| Best suited for | Investors willing to pay for active stock selection | Cost-sensitive investors seeking index returns |

The available funds are growing: Baroda BNP Paribas has also registered as a Retail FME (IFSCA/FME/III/2023-24/099). Before investing, check the IFSCA Directory and individual AMC websites for the most current scheme details.

Key Benefits of Investing in GIFT City Mutual Funds

Lower Cost Structure

The single-layer direct-equity structure of funds like DSP Global Equity Fund (Direct TER: up to 1.00%) compares favourably to domestic international feeder funds. For reference, DSP Global Allocation Fund of Fund — a broadly comparable domestic feeder — reported actual TERs of 0.61% (Direct) and 1.25% (Regular) for FY 2022-23.

At first glance, the domestic Direct option appears cheaper. But domestic FoFs layer in costs from their underlying global ETFs and funds that rarely surface in the headline TER. Evaluate total cost of ownership, not just the number on the label.

USD Denomination as Built-In Currency Diversification

Investments, NAVs, and redemptions are all in USD. For NRIs who earn and hold wealth in foreign currencies, this eliminates the friction of constant INR conversion and provides a natural hedge against rupee depreciation over time.

iVentures Wealth advises NRI and OCI clients to use GIFT City funds to track portfolio performance in USD. This lets you benchmark global wealth growth without complex hedging instruments or active currency management.

Transaction Cost Exemptions

Per the IFSCA's tax guidance, IFSC exchange transactions attract:

- No Securities Transaction Tax (STT)

- No Commodity Transaction Tax (CTT)

- No stamp duty

These exemptions meaningfully reduce friction compared to transacting through domestic exchanges.

Regulatory Confidence

IFSCA's December 2024 circular requires regulated entities to maintain board-approved complaint policies and resolve accepted complaints within 30 days — a structured grievance framework comparable to internationally recognised financial centres.

Who Can Invest: Eligibility and Minimum Investment Requirements

Resident Indians

Resident individuals can invest in GIFT City mutual funds under the RBI's Liberalised Remittance Scheme (LRS), which permits remittances of up to USD 250,000 per financial year for permissible capital account transactions — including investments in IFSC securities.

LRS remittances attract Tax Collected at Source (TCS) at 20% beyond a threshold. Note that official Income Tax sources show a conflict on the exact figure — one source cites INR 7 lakh, while a January 2026 guidance document states INR 10 lakh. Confirm the applicable threshold with a tax adviser before remitting.

Two things to keep in mind about TCS:

- It is not an additional tax — it functions as an advance tax credit

- The amount is adjustable against your total income tax liability for the year

NRIs and OCIs

NRIs and Overseas Citizens of India face a simpler path. Per IFSCA's guidance, they can:

- Open accounts directly with IFSC-registered intermediaries using standard KYC

- Invest in USD without converting to INR

- Fund investments directly from foreign bank accounts

This bypasses NRE/NRO account limitations that apply to domestic investments, and proceeds can be fully repatriated.

Minimum Investment Thresholds

| Scheme Type | Minimum Initial | Top-Up |

|---|---|---|

| GIFT City Retail Mutual Funds | USD 5,000 | USD 500 |

| Restricted Schemes (AIFs) | USD 150,000 | Varies |

| Venture Capital Schemes | USD 250,000 | Varies |

Figures for retail funds based on verified DSP and PPFAS scheme documents. Always confirm with the specific scheme's offer documents.

How to Invest in GIFT City Mutual Funds

The process is simpler than most investors assume. Here's a practical walkthrough:

Step 1 — Define your objective Are you seeking global equity exposure, USD-based currency diversification, or a hedge against INR depreciation? Your objective determines whether an active fund or passive index fund is appropriate.

Step 2 — Choose your fund type If cost minimisation and index returns are priorities, the passive PPFAS offerings (S&P 500 or Nasdaq 100 FoF) are the logical starting point. If you want active global stock selection and can tolerate higher fees and a 24-month exit load, DSP Global Equity Fund is the current active option.

Step 3 — Complete KYC with an IFSC-registered intermediary or the AMC's GIFT City unit Documentation typically required:

- PAN card (for resident Indians)

- Passport (for NRIs/OCIs)

- Foreign address proof (for NRIs)

- Bank account details for the designated foreign currency account

Step 4 — Fund the investment

- Resident Indians initiate an LRS remittance through their bank to the scheme's foreign currency account in GIFT City

- NRIs fund directly from foreign bank accounts or existing NRE/NRO accounts

Units are allotted at the applicable NAV once the AMC receives the funds. Redemption proceeds are credited back in USD to the investor's designated account.

Investors can access GIFT City funds directly through the AMC's GIFT City portal or through a SEBI-registered investment adviser. For UHNIs, NRIs, and family offices, working with an adviser like iVentures Wealth means LRS compliance, fund selection, and global portfolio integration are handled together — rather than navigating each step separately.

Tax Treatment and Key Risks to Consider

Tax Rules for Resident Indians

- Capital gains from GIFT City mutual funds are taxable in India under standard income tax provisions

- Short-term capital gains (STCG) on eligible equity-oriented transfers on or after July 23, 2024: 20% under Section 111A; other STCG taxed at slab rates

- Long-term capital gains (LTCG): generally 12.5% without indexation under Section 112, subject to asset category rules

- Section 50AA risk: Gains from a "Specified Mutual Fund" where less than 35% of proceeds are in domestic equity shares may be deemed short-term — verify whether specific GIFT City fund structures trigger this provision

- GIFT City fund holdings must be disclosed as foreign assets in Schedule FA of the ITR; investors cannot use ITR-1 or ITR-4

- The Section 80LA tax holiday (100% deduction for 10 of 15 consecutive years) applies to IFSC units, not automatically to individual investors

Tax Rules for NRIs

NRIs benefit from several concessions:

- Dividend income from IFSC units taxed at a concessional rate of 10%

- No GST on financial services rendered by IFSC intermediaries

- Capital gains on specified instruments listed in IFSC may be exempt under Section 47(viiab), subject to instrument type and investor category — this is not a blanket exemption for all mutual fund unit redemptions

- DTAA benefits may apply depending on country of residence (Tax Residency Certificate required)

GIFT City tax rules are still evolving. Consult a qualified tax adviser before investing — do not rely solely on this article for tax decisions. The risks below are equally important to understand before committing capital.

Key Risks

- Currency risk: USD/INR movements affect INR returns in both directions; rupee appreciation erodes gains for resident investors

- Global market risk: GIFT City funds are directly linked to international market cycles and geopolitical events, which can diverge significantly from Indian market conditions

- Minimum investment barrier: The USD 5,000 entry point makes these funds unsuitable for smaller retail investors

- Regulatory evolution: IFSCA regulations are still maturing. The 2025 Fund Management Regulations replaced the 2022 framework within three years; further changes are likely as the IFSC ecosystem develops

Frequently Asked Questions

What is a GIFT City mutual fund?

A GIFT City mutual fund is an IFSCA-regulated scheme launched by an AMC operating within India's IFSC in Gujarat. These schemes are denominated in foreign currencies (primarily USD) and invest in global equities, indices, and international assets — distinct from domestic SEBI-regulated funds.

Should I invest in GIFT City mutual funds?

They suit UHNIs, NRIs, and family offices seeking regulated, cost-efficient global diversification with a medium-to-long-term horizon and a minimum USD 5,000 to deploy. They are less suitable for smaller retail investors or those needing INR-denominated liquidity on short notice.

How do I invest in a GIFT City mutual fund?

- Complete KYC with an IFSC-registered intermediary or AMC.

- Fund the investment via LRS remittance (resident Indians) or directly from a foreign account (NRIs/OCIs).

- Units are allotted at the applicable NAV once the AMC receives cleared funds.

What is the minimum investment amount?

Most retail GIFT City mutual funds require a minimum initial investment of USD 5,000, with subsequent top-ups from USD 500. AIFs within GIFT City require USD 150,000 and Venture Capital Schemes require USD 250,000. Confirm exact thresholds in each scheme's offer document before investing.

Are GIFT City mutual fund returns taxable in India?

Resident Indians pay capital gains tax under standard provisions and must report GIFT City holdings as foreign assets in Schedule FA of their ITR. NRIs benefit from concessions including a 10% rate on dividends and potential capital gains exemptions on specified instruments. Consult a tax adviser for your specific situation.

Can NRIs invest in GIFT City mutual funds?

Yes. NRIs and OCIs can invest through a simplified KYC process with no requirement to convert funds to INR and full repatriation of proceeds. This makes GIFT City a practical, regulated route for NRIs seeking global market exposure through an India-based structure.