Introduction

Most affluent professionals spend considerable energy planning for retirement or long-term wealth creation — and almost none on the near-term financial decisions that determine whether those plans ever materialise. Emergency funds sit unfunded. High-cost debt compounds quietly. Surplus income disappears into lifestyle spending rather than moving toward defined goals.

According to a Business Standard survey, 75% of Indians lack an emergency fund and could default on EMIs following a sudden layoff. Even among high-income earners, cash flow mismanagement and reactive financial decisions are far more common than the numbers suggest.

Short-term financial planning — covering goals within one to two years — is the foundation on which long-term wealth is actually built. Without it, even sophisticated investment strategies underperform.

This guide covers what you need to build a short-term plan that actually holds:

- What short-term financial planning is and why it matters for HNIs

- The key goals to prioritize within a 1–2 year horizon

- A step-by-step planning process with practical budgeting frameworks

- The right instruments for short-term goals in the Indian context

Key Takeaways

- Short-term financial planning addresses goals within 1–2 years: emergency fund, debt clearance, near-term purchases, and tax planning

- Eliminating high-cost debt — credit cards charge up to 45–55% per annum — delivers one of the highest returns available

- No single budgeting framework fits everyone — income stability, existing debt, and dependents all determine the right approach

- Automating savings transfers on salary day removes the behavioural friction that derails even well-intentioned plans

- Budgeting, automating, and eliminating debt are the same disciplines that build long-term wealth

What Is Short-Term Financial Planning?

Short-term financial planning is the process of identifying, budgeting for, and working toward financial goals achievable within one to two years. This includes both anticipated needs — a vehicle purchase, home renovation, international travel — and protective measures like building an emergency corpus (liquid reserve) or clearing high-interest debt.

It sits within a three-horizon framework:

| Horizon | Timeline | Typical Goals |

|---|---|---|

| Short-term | 1–2 years | Emergency fund, debt clearance, near-term purchases |

| Mid-term | 3–10 years | Home purchase, children's education |

| Long-term | 10+ years | Retirement, generational wealth |

All three horizons must work in coordination. Short-term planning isn't a separate exercise — it's the layer that keeps long-term strategies intact.

Without it, an unfunded emergency corpus forces premature redemption of long-term investments — often during market downturns, when the cost of liquidating is highest.

For busy professionals and business owners, that reactive pattern carries real cost. High incomes don't automatically translate to financial security. Without near-term structure, surplus income gets absorbed by lifestyle spending, tax obligations arrive unexpectedly, and financial decisions default to urgency rather than strategy.

Key Short-Term Financial Goals to Plan For

Building an Emergency Corpus

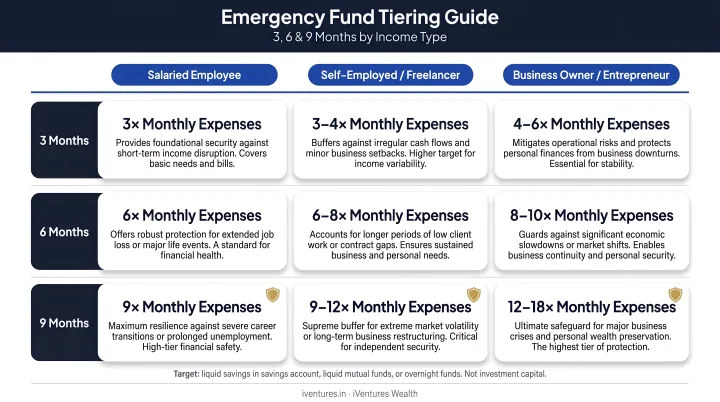

An emergency fund is non-negotiable — it's the buffer that prevents a financial shock from becoming a financial crisis. The general practitioner guideline suggests:

- 3 months' expenses — minimum for salaried individuals with stable income

- 6 months' expenses — for those with variable income or dependents

- 9 months' expenses — for business owners and self-employed professionals with irregular cash flows

Note that this tiering is a widely used practitioner heuristic. SEBI's investor education materials recommend building an emergency fund to cover unexpected expenses but do not specify the exact months' threshold.

Keep the corpus in a liquid, easily accessible instrument — separate from investment accounts — so it's available immediately without disrupting long-term portfolios.

Paying Down High-Cost Debt

Not all debt carries the same cost. Home loans and business loans at moderate interest rates serve legitimate financial purposes. Credit card dues and personal loans are a different matter — the finance charges are steep and often underestimated.

Official bank disclosures show current Indian credit card finance charges ranging from 33% to 55.55% per annum: SBI Card charges up to 45% per annum on unsecured cards, ICICI Bank up to 45% per annum, and Axis Bank SELECT up to 55.55% per annum. CRIF High Mark reported ₹3.5 lakh crore in credit card outstanding as of September 2025, with a 4.1% delinquency rate.

Eliminating high-cost debt within a 12-month horizon is one of the highest-return financial moves available — because every rupee repaid earns a guaranteed return equal to the interest rate you'd otherwise pay.

Saving for a Defined Near-Term Purchase

Funding planned large expenses — a vehicle, family occasion, international trip — through savings rather than credit requires deliberate structure, not just good intentions.

Example: You want ₹3,60,000 for an international trip in 12 months.

- Monthly saving required: ₹3,60,000 ÷ 12 = ₹30,000/month

- Park this in a liquid fund or short-term FD earning approximately 5.7–6.5% per annum

The discipline of calculating a specific monthly number — and automating the transfer — is what separates planned spending from reactive credit use.

Establishing a Tax-Efficient Spending Plan

For business owners, freelancers, and high-income professionals, tax obligations don't arrive in a single annual bill. They arrive as quarterly advance tax instalments, capital gains at the point of asset sale, and TDS deductions throughout the year. A monthly budget that accounts for these obligations prevents the year-end cash crunch that forces reactive decisions.

Aligning your short-term cash flow structure with the April–March Indian financial year also creates natural review points for tax planning, investment rebalancing, and goal progress.

Setting Aside an Annual Investment Contribution

Short-term planning should include a fixed monthly or quarterly investment commitment — even when the goal is long-term. Consistency in the near term is what creates compounding over the long term. Set a specific SIP amount or quarterly transfer on day one — and treat it as a non-negotiable line item, not a residual after spending.

How to Build a Short-Term Financial Plan: Step by Step

Step 1 — Assess Your Current Financial Position

Start with a net worth calculation: total assets minus total liabilities. Then map monthly cash flows — every income source against every expenditure category.

This baseline reveals the actual surplus available for short-term goals after essentials, EMIs, and existing obligations. Many professionals discover their real monthly surplus is 30–40% smaller than their gross income suggests.

At iVentures Wealth, this step precedes any goal allocation: a single cash map is built across all accounts to surface idle capital and confirm what's actually available to deploy.

Step 2 — Define and Prioritise Your Goals

Apply the SMART framework to each short-term goal:

- Specific — "Build a ₹6 lakh emergency fund" not "save more"

- Measurable — attach a rupee amount

- Achievable — realistic given your monthly surplus

- Relevant — aligned with your actual priorities

- Time-bound — a defined completion date

Then rank goals by urgency. Emergency fund and high-cost debt repayment typically come before discretionary goals like vacations. Carrying high-interest debt or staying without a buffer costs more, in real rupees, than delaying a vacation by six months.

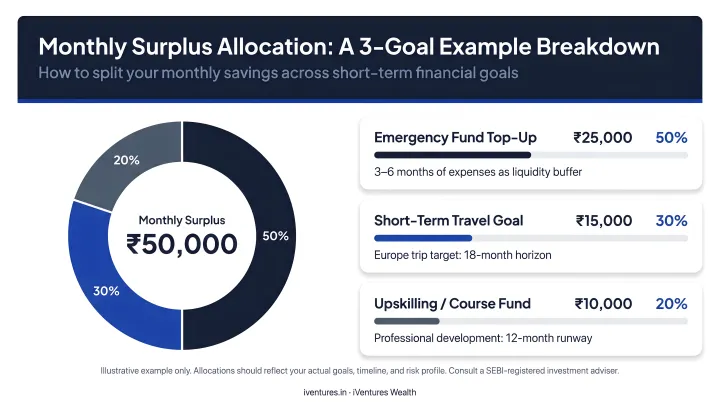

Step 3 — Allocate Surplus Across Goals

Divide your available monthly surplus across ranked goals. Assign a rupee amount and a timeline to each, then calculate the monthly saving required.

Example allocation for a salaried professional with ₹50,000/month surplus:

| Goal | Monthly Allocation | Timeline |

|---|---|---|

| Emergency corpus | ₹20,000 | 9 months |

| Credit card prepayment | ₹15,000 | 6 months |

| Vacation fund | ₹15,000 | 12 months |

When goals compete for the same surplus, trade-offs must be made consciously rather than by default. Delaying a vacation by three months to build the emergency fund first is a deliberate choice — one that preserves your financial position instead of eroding it.

Step 4 — Choose the Right Financial Instrument

Match the instrument to the goal's time horizon and liquidity requirement. A goal three months away needs a different vehicle than one 18 months away. A three-month target, for instance, calls for a liquid fund or high-yield savings account. An 18-month goal can tolerate a short-duration debt fund for modestly better returns without meaningful liquidity risk.

Step 5 — Automate, Track, and Review

Set up automatic transfers to goal-specific accounts or instruments on salary day — before discretionary spending can absorb the surplus. This single habit has an outsized impact on savings consistency.

Behavioural research by Thaler and Benartzi found that participants in the Save More Tomorrow programme increased their saving rates from 3.5% to 13.6% over 40 months through commitment mechanisms alone — no willpower required.

The scale of this effect shows up in India's SIP data. AMFI reported ₹32,087 crore in SIP contributions across nearly 9.72 crore contributing accounts in March 2026, demonstrating how automation has reshaped savings behaviour at a national level.

Review quarterly. Income changes, unexpected expenses, and shifting priorities all require adjustments to the allocation.

Budgeting Frameworks That Support Short-Term Planning

No single framework works for everyone. The value of any framework is in creating intentionality around money allocation — not in following exact percentages.

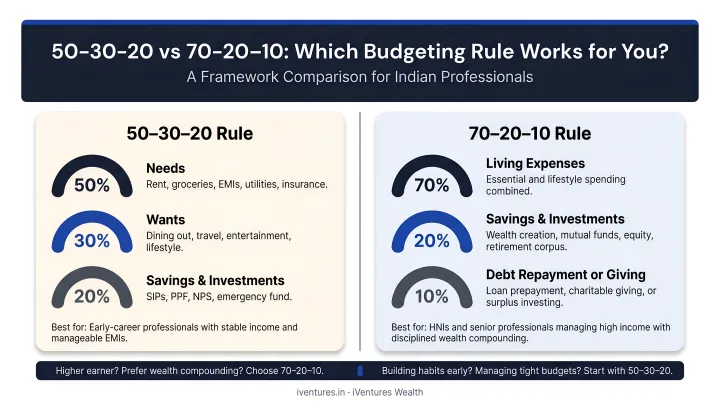

The 50/30/20 Rule

Popularised by Elizabeth Warren and Amelia Warren Tyagi in All Your Worth (2005), this framework allocates:

- 50% of take-home income to needs (housing, food, utilities, EMIs)

- 30% to wants (dining, travel, subscriptions)

- 20% to savings and debt repayment

The 20% savings bucket directly funds short-term goals. For high-income professionals where lifestyle expenses consume a smaller share of income, the savings allocation should be adjusted upward — often significantly.

The 70/20/10 Rule

A practitioner-derived variant that suits those with existing loan obligations:

- 70% for all living expenses

- 20% for savings and investments

- 10% for debt repayment or discretionary goals

The explicit 10% debt repayment bucket is the key distinction. For someone managing personal loan EMIs alongside savings goals, this framework prevents debt repayment from crowding out investment contributions, and vice versa.

Choosing the Right Framework

| Your Situation | Recommended Framework |

|---|---|

| Minimal debt, high savings capacity | 50/30/20 (adjust savings up) |

| Active loan EMIs alongside savings goals | 70/20/10 |

| Variable income, irregular cash flows | Either framework, with larger emergency buffer |

The right framework depends on income stability, existing debt, number of dependents, and near-term goals. Start with one, track for 90 days, and adjust.

Best Investment Instruments for Short-Term Goals in India

Liquid and Ultra-Short Duration Mutual Funds

These funds invest in short-maturity debt instruments and offer better returns than savings accounts while remaining highly liquid. Per Value Research category data, current returns are approximately:

- Debt: Liquid — 5.74% (1-year), 6.68% (3-year)

- Debt: Ultra Short Duration — 5.70% (1-year), 6.57% (3-year)

Redemption proceeds must be transferred within three working days per SEBI's FAQ. SEBI introduced an Instant Access Facility for liquid funds, allowing partial same-day withdrawal up to a specified limit.

These are well-suited for emergency corpus storage or goal timelines up to 6–12 months.

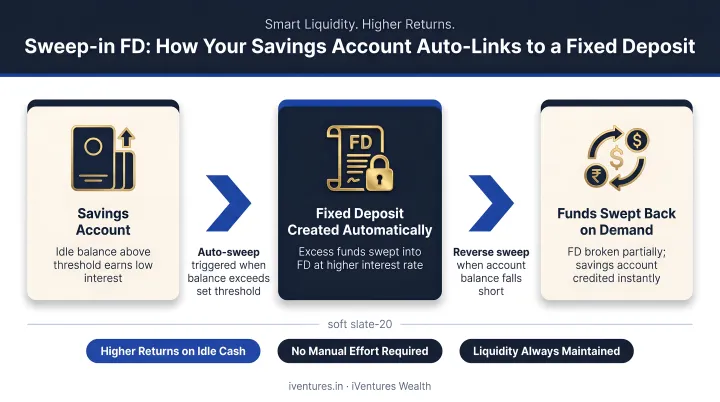

Fixed Deposits and Sweep-In FDs

Bank FDs offer capital safety and defined returns for goals with a fixed timeline (3 months to 2 years). Current general-public rates from major banks:

| Bank | Tenure | Rate |

|---|---|---|

| SBI | 1 year to < 2 years | 6.25% p.a. |

| SBI | 444-day special tenor | 6.45% p.a. |

| HDFC Bank | 18 months to 2 years | 6.45% p.a. |

| HDFC Bank | 1 year to < 15 months | 6.25% p.a. |

(SBI rates effective 15 Dec 2025; HDFC rates effective 6 Mar 2026)

The sweep-in facility links a savings account to an FD — HDFC Bank breaks linked FD units in ₹1 increments to cover account shortfalls, while ICICI Bank's Money Multiplier FD moves surplus into FDs in ₹5,000 multiples and reverses the sweep when the savings balance falls below ₹10,000. This provides FD-level returns with savings account liquidity.

For individuals in higher tax brackets, FD interest is fully taxable as income — making post-tax return comparison against other options important before choosing.

Short-Duration Debt Funds and Arbitrage Funds

For goal timelines of 12–24 months, these offer greater tax efficiency. Arbitrage funds are taxed as equity (15% STCG if held less than 12 months, 12.5% LTCG beyond) rather than at slab rates — which benefits investors in the 30% bracket considerably.

The two instruments serve different risk profiles:

- Short-duration debt funds carry slightly higher interest rate and credit risk than liquid or ultra-short funds

- Arbitrage funds carry minimal market risk but depend on the spread between cash and futures markets — investors should understand how that mechanism works before allocating

The right instrument mix depends on three factors: goal timeline, liquidity needs, and tax bracket. When multiple short-term goals compete for the same surplus — a common situation for HNIs and professionals — the sequencing and instrument choice matters as much as the return. iVentures Wealth's SEBI-registered advisors work through this allocation as part of a consolidated, tax-aware financial plan.

How Short-Term Planning Connects to Long-Term Wealth Building

Short-Term Habits as the Foundation of Wealth

The financial discipline built through short-term planning — budgeting, automating savings, eliminating high-cost debt — is the same discipline that sustains long-term wealth accumulation. Without these near-term habits in place, even well-constructed long-term portfolios underperform due to behavioural inconsistencies:

- Panic selling during market downturns

- Ad hoc withdrawals for unplanned expenses

- Missed SIP contributions during cash flow stress

An emergency corpus specifically reduces the likelihood of premature redemption of long-term investments during financial shocks. This is the mechanism — not just the philosophy.

Integrating Short-Term Plans Into a Broader Wealth Strategy

Short-term goals should be explicitly mapped within a comprehensive financial plan — not treated as a separate personal finance exercise disconnected from investment strategy.

iVentures Wealth's three-bucket structure for larger corpus deployments illustrates this integration:

- Safety bucket: 5–7 years of expenses in high-quality fixed income — functioning as an institutionalised emergency corpus

- Stability bucket: Medium-term balanced allocation for transitional goals

- Growth bucket: Long-horizon assets for wealth compounding over decades

This structure ensures clients never need to liquidate growth assets during a market downturn.

For UHNIs and business owners, short-term cash flow planning also intersects with corporate treasury management, advance tax obligations, and capital structure decisions. Coordinated advisory handles these decisions far more effectively than siloed financial management.

When to Seek Professional Guidance

A SEBI-registered investment advisor adds the most value in short-term planning when:

- Income is variable or comes from multiple sources (business, salary, investments)

- Tax implications of financial decisions are significant — advance tax, capital gains, TDS

- Multiple competing goals require conscious prioritisation

- Short-term cash flow needs must be balanced against long-term portfolio continuity

- Corporate and personal finances need to be structured separately

Frequently Asked Questions

What is short-term financial planning?

Short-term financial planning means setting and working toward financial goals achievable within one to two years. It typically covers emergency fund building, high-cost debt repayment, near-term purchases, and regular investment contributions — structured within a monthly budget.

What is an example of a short-term financial plan?

A salaried professional earning ₹2 lakh per month sets aside ₹30,000/month toward an emergency corpus, ₹20,000/month to prepay a personal loan, and ₹15,000/month toward a vacation fund — all within a 12-month window, automated on salary day and tracked through a simple monthly budget.

What budgeting rules can help with short-term financial planning?

The 50/30/20 rule allocates 50% to needs, 30% to wants, and 20% to savings. The 70/20/10 rule adds a dedicated 10% for debt repayment — better suited when EMI obligations are substantial. Which framework fits depends on your income stability, debt load, and dependents.

What is the difference between short-term and long-term financial planning?

Short-term planning addresses goals within 1–2 years — emergency fund, debt clearance, near-term purchases. Long-term planning covers goals 10+ years away, such as retirement or generational wealth. The two must be coordinated: short-term planning creates the liquidity buffer and behavioural discipline that long-term strategies depend on.

What are the best investment options for short-term financial goals in India?

Liquid mutual funds (currently yielding ~5.7–6.7% p.a.), ultra-short duration funds, bank FDs, and sweep-in FDs are the most commonly used options. The right fit depends on your goal timeline and tax bracket.

How much should I keep in an emergency fund?

Salaried individuals should target 3–6 months of total household expenses. Self-employed professionals and business owners should aim for 6–9 months given income variability. This corpus should be kept in a liquid, accessible instrument — separate from investment accounts — without touching long-term investments.