Many retirees discover this gap too late. According to India's Sample Registration System 2020–24, life expectancy at age 60 is 18.6 years on average — but that's a statistical midpoint. Planning only to that number means half of all retirees outlive their money. A realistic post-retirement planning window is 25–30 years.

The challenge isn't just longevity. Inflation erodes purchasing power, markets introduce volatility, and ad-hoc withdrawals quietly deplete capital. Two retirees with identical corpus sizes can end up in vastly different places a decade later, purely based on how they structured their investments.

This guide covers the key decisions: how to assess your baseline, segment the corpus into functional buckets, select the right instruments, and avoid the mistakes that silently drain retirement wealth.

Key Takeaways

- Establish your monthly income requirement before choosing instruments — not after.

- The 3-bucket approach (liquidity, safety, growth) prevents panic-selling during market downturns.

- Inflation and withdrawal rate are the two biggest threats to corpus longevity — manage both proactively.

- Equity, debt, and income instruments combined outperform any single product type across a 20+ year horizon.

- Rebalance at least annually — and immediately after major life events.

What to Assess Before Investing Your Retirement Corpus

Before selecting a single instrument, three foundational inputs must be established:

- Monthly income required post-retirement (inflation-adjusted)

- Total corpus available across all assets

- Expected retirement duration based on current age and realistic life expectancy

Every subsequent decision — asset allocation, product selection, withdrawal rate — flows from these three numbers.

Risk Profile and Dependents

Risk tolerance changes fundamentally at retirement. The accumulation phase rewards aggression; the distribution phase punishes it. A 30% drawdown at age 35 is recoverable. At age 65, with regular withdrawals in progress, it may not be.

Factor in:

- Whether a spouse depends on the corpus for income

- Whether aging parents create potential large expense obligations

- Whether leaving a financial legacy is a stated goal

A legacy goal, for instance, often justifies keeping a larger equity allocation intact — even late in retirement — than pure income-need analysis would suggest.

Existing Guaranteed Income Sources

Any income already in place — pension, rental income, NPS annuity, PPF payouts — reduces the burden on the invested corpus. A retiree with ₹1.2 lakh/month in guaranteed income needs far less from their portfolio than one starting from zero. That gap directly shapes how much risk the remaining corpus can afford to take on — and how much of it can stay growth-oriented rather than parked in capital-preservation instruments.

How to Invest Your Retirement Corpus: A 5-Step Framework

Step 1: Define Monthly Income Requirement and Time Horizon

Start with today's monthly expenses, then project forward. At India's current CPI of 3.48% year-on-year, costs double roughly every 20 years — though the long-run average runs higher. A retiree spending ₹80,000/month today will need approximately ₹1.6 lakh/month in 12 years if inflation averages 6%.

Map expenses across three distinct retirement phases:

| Phase | Age Range | Characteristics |

|---|---|---|

| Early retirement | 60–70 | Higher activity, travel, social spending |

| Mid-retirement | 70–80 | Moderate lifestyle, first healthcare costs emerge |

| Late retirement | 80+ | Healthcare dominates; lifestyle costs often reduce |

Each phase requires a different drawdown approach. Building the plan around a single flat monthly figure will either underfund the early years or over-withdraw in the later ones.

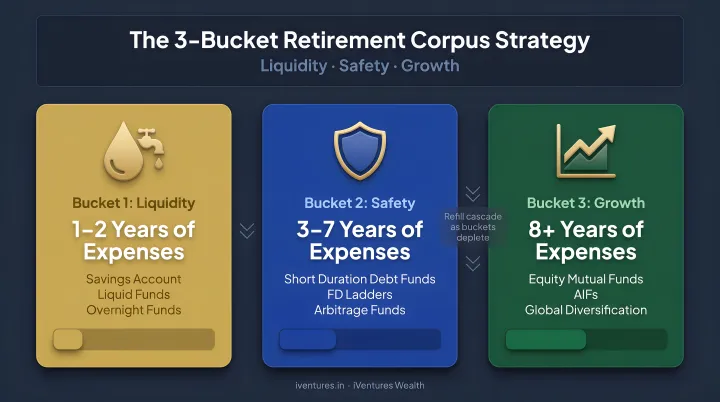

Step 2: Segment the Corpus — The 3-Bucket Approach

The bucket strategy, originally developed by Harold Evensky in 1985, remains the most practical framework for managing retirement income against market volatility.

Bucket 1 — Liquidity (1–2 years of expenses) Held in liquid mutual funds, savings accounts, or ultra-short-term debt. This bucket is accessed first and carries zero market exposure.

Bucket 2 — Safety (3–7 years of expenses) Invested in stable, low-risk instruments: short-duration debt funds, SCSS, RBI Floating Rate Bonds, FDs. As Bucket 1 depletes, this bucket refills it.

Bucket 3 — Growth (remaining corpus, 7+ year horizon) Invested for capital appreciation through equity mutual funds or balanced advantage funds. This bucket is untouched for years — that long runway is the entire point.

The psychological function of this structure matters as much as the financial mechanics. When markets fall 25%, a retiree with Bucket 1 fully funded doesn't need to sell equity at the bottom. That behavioral buffer stops the most damaging mistake in retirement investing: panic-selling at market lows.

iVentures Wealth applies a calibrated version of this framework for HNI/UHNI clients: the Safety bucket covers 5–7 years of expenses in high-quality fixed income, the Stability bucket spans an 8–15 year horizon with balanced asset allocation, and the Growth bucket draws on select AIF, PMS, and private equity strategies for clients whose corpus and risk profile support it.

Step 3: Allocate Across Asset Classes

A reasonable starting allocation for a 60-year-old with moderate risk tolerance:

- 40–50% equity (for inflation-beating growth)

- 40–50% debt (for stability and income)

- 10% liquid (Bucket 1 reserve)

This ratio should drift toward more debt as the retiree ages. A 70-year-old might shift to 25–30% equity. Research by Freefincal suggests that for many Indian retirees, equity allocations at retirement hover around 20–22%, though this is conservative by most long-term planning standards.

For retirees with larger corpora (₹2 Cr+), a higher equity allocation remains viable post-60. The Nifty 50 TRI has delivered 11.8% CAGR over 15 years, and 14.2% CAGR from 1999 to 2021 — meaningful growth that smaller, more conservative corpora can afford to forgo but larger ones cannot.

A simple heuristic: keep equity percentage equal to (100 minus your age). A 65-year-old holds 35% equity. Treat this as a starting point, not a rule.

Step 4: Set Up a Systematic Income Stream

Once the allocation is set, the next question is how to draw income without eroding the corpus. Systematic Withdrawal Plans (SWPs) from mutual funds are the most tax-efficient mechanism for this. Only the gains component is taxed — not the full withdrawal. For equity funds held over 12 months, LTCG above ₹1.25 lakh is taxed at 12.5% (applicable for transfers from July 23, 2024 onwards). FD interest, by contrast, is taxed at your full income slab rate.

iVentures Wealth structures SWPs as part of its passive income advisory, including a documented case where a corpus was structured to generate approximately ₹7.5 lakh per month in predictable income while the principal continued to grow.

Other income mechanisms worth combining:

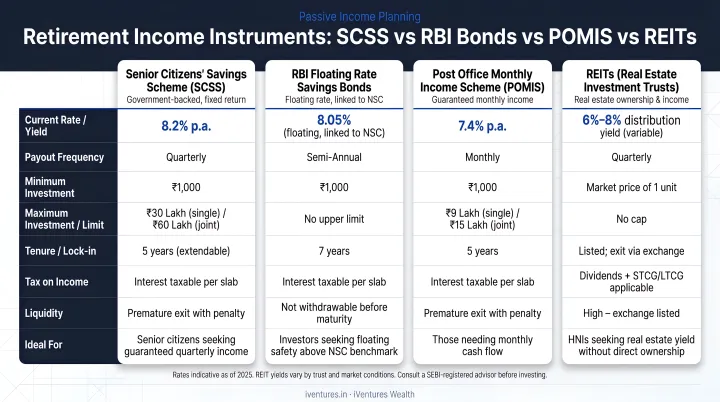

- SCSS — 8.2% p.a., quarterly payout, sovereign-backed, up to ₹30 lakh per individual

- RBI Floating Rate Bonds — currently at 8.05% (January–June 2026), zero default risk

- POMIS — 7.4% p.a., monthly payouts, up to ₹15 lakh (joint)

- REITs/InvITs — distribution yields around 6–8%, quarterly payouts, partial equity-like growth

No single income source should carry the full load. Two or three combined provide reliability that one alone cannot.

Step 5: Schedule Periodic Review and Rebalance

Annual rebalancing is a non-negotiable discipline. As equity grows in a bull market, the portfolio drifts riskier than intended. Rebalancing restores the target allocation, locks in gains, and reduces risk on a planned schedule rather than a reactive one.

Life events — serious illness, death of a spouse, large one-time expenses — should also trigger unscheduled reviews. These often require fundamental restructuring of the income plan, not just minor adjustments.

iVentures Wealth (SEBI RIA registration INA000019026) conducts quarterly portfolio reviews for retired HNI/UHNI clients, with continuous monitoring between reviews. Assessments cover XIRR performance, asset allocation drift, maturity schedules, taxation summaries, and benchmark comparisons — structured so that rebalancing decisions are data-driven, not reactive to market noise.

Best Investment Options for a Retirement Corpus in India

Equity Mutual Funds (Growth Bucket)

Large-cap, flexi-cap, and balanced advantage funds are the preferred equity instruments for retirement portfolios. They offer professional management, diversification, and the flexibility to generate income through SWP.

Direct stock investing suits experienced retirees with time and inclination, but most benefit from the discipline and diversification that funds provide.

Debt Instruments (Safety Bucket)

| Instrument | Rate | Key Feature |

|---|---|---|

| SCSS | 8.2% p.a. | Quarterly payout, sovereign-backed |

| RBI Floating Rate Bonds | 8.05% (Jan–Jun 2026) | Zero default risk, interest taxable |

| POMIS | 7.4% p.a. | Monthly payout |

| Debt Mutual Funds | Market-linked | Better post-tax returns vs. FDs for higher tax brackets |

SCSS and RBI bonds are best suited for retirees in the 0–10% tax bracket; those in higher brackets typically see better after-tax outcomes from debt mutual funds.

REITs, InvITs, and Dividend Stocks (Income Equities)

REITs and InvITs sit between debt and equity, paying regular quarterly distributions while offering some capital appreciation potential. Key reference points:

- Embassy REIT: Paid ₹25.28 per unit in FY2026

- Mindspace REIT: Carried an annualised distribution yield of approximately 6.9%

- InvITs: Primarily infrastructure-backed; yields vary by asset quality and project stage

Beyond REITs and InvITs, dividend-paying stocks — particularly PSU companies with consistent payout histories — can supplement income. However, dividends are not guaranteed and should not serve as a primary income source.

Key Variables That Determine Corpus Longevity

Inflation

At 6% annual inflation, purchasing power halves in roughly 12 years. An FD at 7% with 6% inflation generates a real return of approximately 1%. Equity at 12% with the same inflation generates a 6% real return — the difference that compounds to a materially larger corpus over a 25-year retirement.

The only figure that actually matters is real return, not nominal return.

Safe Withdrawal Rate

India-specific research from Freefincal suggests a sustainable withdrawal rate of around 2.5% for a 30-year retirement. Withdrawing 5–6% annually from day one dramatically increases the probability of corpus depletion within 15–18 years, regardless of returns.

Spending more in the early active years is valid — but only when modeled against corpus longevity projections.

Sequence of Returns Risk

Two retirees with identical 10-year average returns can end up in very different places depending on when those returns arrived. The retiree who experiences strong early years followed by a crash retains far more capital than one who starts retirement in a bear market and withdraws through the downturn.

This is why the bucket strategy isn't optional — it's the structural defense against sequence risk.

Asset Allocation

A 60:40 equity-debt split has historically delivered higher real returns than a 20:80 split, while also carrying deeper short-term drawdowns. The right ratio depends not on age alone but on corpus size, income requirements, risk tolerance, and guaranteed income sources.

A SEBI-registered adviser calibrates this ratio to your actual income gap, guaranteed pension or rental inflows, and corpus size — not generic age-based formulas.

At a glance — what each variable controls:

- Inflation: Erodes real return; the gap between 1% and 6% real return determines whether your corpus lasts 15 years or 30

- Withdrawal rate: Staying near 2.5% dramatically extends longevity; every additional percentage point withdrawn accelerates depletion

- Sequence of returns: Poor early years combined with withdrawals cause irreversible capital loss — structural mitigation is non-negotiable

- Asset allocation: A higher equity allocation improves real returns but requires liquidity buffers to avoid forced selling in downturns

Common Mistakes When Investing a Retirement Corpus

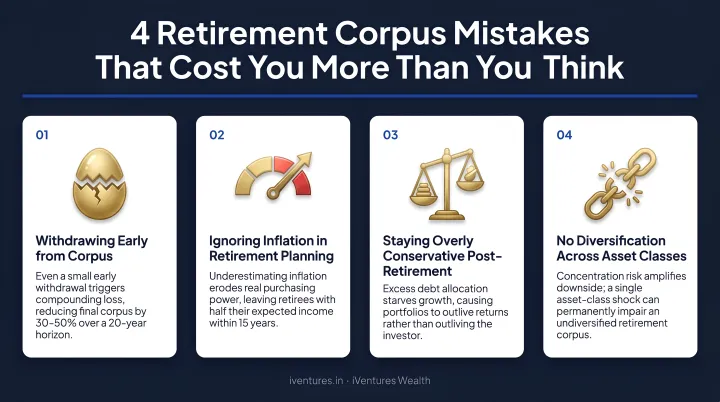

- Over-concentrating in FDs: At 7.05% (SBI senior citizen rate), a 30% tax bracket leaves a real return of roughly 1.4% — barely ahead of recent CPI. That gap compounds into significant corpus erosion over 20 years.

- Exiting equity entirely at retirement: Removing the growth engine at 60 forces the corpus to fight inflation with instruments that barely beat it. Some equity allocation must persist throughout retirement.

- Withdrawing without a plan: Ad-hoc drawdowns lead to poor tax management, unplanned corpus depletion, and missed compounding. A structured SWP approach disciplines all three.

- Ignoring tax drag: FD interest, mutual fund capital gains, REIT distributions, and dividends are taxed differently. The wrong instrument mix in the wrong tax bracket can quietly erode 1–2% of effective annual returns — a consequence that compounds significantly across a 25-year retirement horizon.

Frequently Asked Questions

Where should I invest my retirement corpus?

Use a 3-bucket approach: keep 1–2 years of expenses in liquid instruments, 3–7 years in stable debt or government-backed schemes like SCSS and RBI bonds, and the remainder in equity mutual funds for long-term growth. The exact mix depends on corpus size, existing guaranteed income, and risk tolerance.

What is a safe withdrawal rate for a retirement corpus in India?

India-specific research suggests around 2.5% of the total corpus annually for a 30-year retirement. Withdrawing well above this in early years — without modeling how long the corpus will last — meaningfully increases the risk of outliving your savings.

How do I generate monthly income from my retirement corpus?

The most effective approach combines two or three sources: SWP from equity or balanced mutual funds, fixed interest from SCSS or RBI Floating Rate Bonds, and REIT/InvIT distributions for some growth potential. Relying on a single source creates both income and tax risk.

What is the 3-bucket strategy for retirement?

Bucket 1 holds 1–2 years of expenses in liquid funds for immediate use. Bucket 2 holds 3–7 years of needs in stable debt instruments. Bucket 3 holds the long-term corpus in equity mutual funds for growth. The structure prevents forced selling of equity during market downturns.

Is it safe to keep equity in my portfolio after retirement?

Yes — and for most retirees, it's necessary. A 25–40% equity allocation provides the inflation-beating growth needed to sustain a corpus over 20–30 years. With near-term income needs covered through Buckets 1 and 2, the equity portion has time to recover from market swings.