The confusion is understandable. International funds sit in a grey zone — they feel like equity funds but are taxed differently. The rules also depend heavily on when you invested, not just what you invested in.

This guide covers how international mutual funds are classified for tax purposes, which rates apply, how your investment date affects the outcome, and what steps help you avoid costly filing errors.

Key Takeaways

- International mutual funds are classified as non-equity (debt-like) funds under Indian tax law — they do not qualify for equity fund treatment.

- STCG (held 24 months or less): taxed at your applicable income slab rate.

- LTCG (held more than 24 months, redeemed on or after April 1, 2025): taxed at 12.5% without indexation.

- The ₹1.25 lakh annual LTCG exemption for domestic equity funds does not extend to international funds.

- Dividend income is taxed at your applicable slab rate under "Income from Other Sources."

- Purchase date determines which tax rules apply: investments made before vs. after April 1, 2023 are treated differently.

What Are International Mutual Funds and How Are They Classified for Tax Purposes?

International mutual funds are Indian-registered mutual fund schemes that invest in equities, bonds, or fund units of companies listed outside India. Investors transact entirely in Indian rupees through domestic platforms — no foreign brokerage account or LRS remittance is required.

Most Indian international mutual funds use a Fund of Funds (FoF) structure: the Indian AMC invests in units of an overseas fund or ETF, and the Indian investor holds units of that Indian FoF. The investor never directly owns foreign stocks or overseas fund units.

Why They're Taxed as Non-Equity Funds

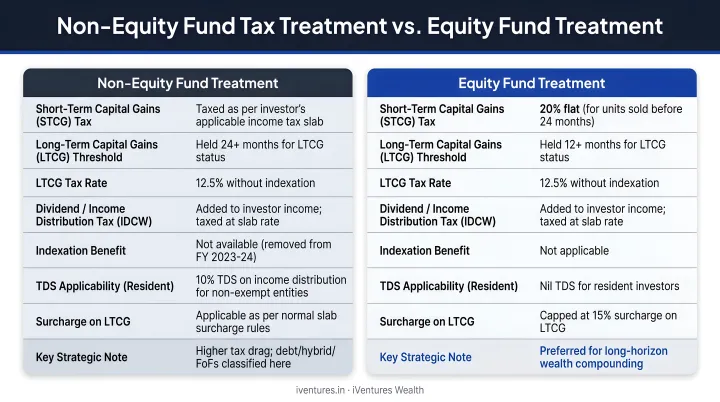

The tax classification of a mutual fund hinges on a single criterion: how much of the fund is invested in Indian equity shares — not foreign ones.

Under Section 112A of the Income Tax Act, an equity-oriented fund must invest at least 65% of its assets in equity shares of domestic companies. International funds invest primarily in foreign equities, which do not qualify as domestic equities. They cannot meet this 65% threshold and are therefore classified as non-equity funds.

This classification carries significant tax consequences for investors:

- No access to the concessional 20% LTCG rate available under Section 112A for domestic equity funds

- No ₹1.25 lakh annual LTCG exemption (available only to equity-oriented funds)

- STCG taxed at the investor's applicable income slab rate

- LTCG also taxed at the investor's slab rate — not at a flat concessional rate — following the Finance Act 2023 amendment

How International Mutual Funds Are Taxed in India

The tax treatment of international mutual funds has changed significantly across two Finance Acts — and the rules that apply to you depend on both when you invested and when you redeem. Here's how the framework breaks down.

The Core Tax Framework

For international equity mutual funds (not covered by Section 50AA's debt-oriented provisions) under current rules:

| Holding Period | Tax Treatment |

|---|---|

| 24 months or less | STCG — taxed at applicable income slab rate |

| More than 24 months | LTCG — taxed at 12.5% without indexation |

The 24-month holding period threshold applies specifically to non-equity funds. This is different from domestic equity funds, which qualify for LTCG treatment after just 12 months.

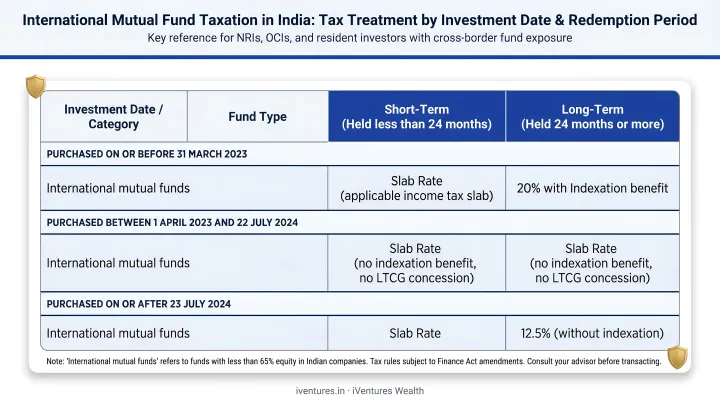

The Purchase Date Factor: Pre vs. Post April 1, 2023

Two separate legislative events, the Finance Act 2023 and Finance (No. 2) Act 2024, created distinct tax scenarios based on when you bought your units.

| Investment Date | Redemption Period | Tax Treatment |

|---|---|---|

| Before April 1, 2023 | Before July 23, 2024 | Old non-equity rules applied: STCG at slab; LTCG with indexation for eligible holdings |

| Before April 1, 2023 | On or after July 23, 2024 | LTCG at 12.5% without indexation if held more than 24 months; STCG at slab rate if 24 months or less |

| On or after April 1, 2023 | FY 2023-24 and FY 2024-25 | All gains taxed at slab rate regardless of holding period (under Section 50AA, old definition) |

| On or after April 1, 2023 | FY 2025-26 onward (April 1, 2025+) | LTCG at 12.5% without indexation if held more than 24 months; STCG at slab rate if 24 months or less |

Important note: The Section 50AA amendment that restored LTCG treatment for international equity FoFs applies from AY 2026-27 (i.e., income earned in FY 2025-26 onward). International debt or bond funds that meet the amended Section 50AA debt-oriented tests may still have all gains treated as STCG regardless of holding period — check each fund's portfolio composition before assuming LTCG applies.

Dividend Taxation

Dividends from international mutual funds are taxed as "Income from Other Sources" and added to your total taxable income at your applicable slab rate. The Dividend Distribution Tax (DDT) was abolished effective April 1, 2020, shifting the tax burden entirely to investors. The holding period and investment date are irrelevant for dividend taxation — the slab rate applies regardless.

International Funds vs. Domestic Equity Funds: Tax at a Glance

| Feature | International Equity Fund | Domestic Equity Fund |

|---|---|---|

| Tax classification | Non-equity | Equity-oriented (Section 112A) |

| STCG rate | Slab rate (up to 30%) | 20% (for transfers on/after July 23, 2024) |

| LTCG rate | 12.5% without indexation | 12.5% above ₹1.25 lakh exemption |

| Holding period for LTCG | More than 24 months | More than 12 months |

| Indexation benefit | Not available | Not available |

| ₹1.25 lakh annual exemption | Not applicable | Applies under Section 112A |

The ₹1.25 lakh annual exemption is a meaningful difference that many investors underestimate when comparing the two. A domestic equity fund investor pays zero tax on LTCG up to ₹1.25 lakh per year: an international fund investor starts paying at rupee one of gains.

How to Calculate Capital Gains Tax on Your International Fund Investment

Step 1: Identify the Fund's Classification and Investment Date

Confirm the fund is a non-equity fund (less than 65% in Indian equities). Then check your purchase date — pre- or post-April 1, 2023 determines which tax scenario from the table above applies to your specific lot.

Step 2: Determine the Holding Period

Count the months from your purchase date to your redemption date. The threshold is:

- 24 months or less → Short-term capital gains (STCG)

- More than 24 months → Long-term capital gains (LTCG)

This 24-month threshold is specific to non-equity mutual funds. Many investors incorrectly apply the 12-month equity rule — a costly mistake covered in the next section.

Step 3: Calculate Capital Gains in Rupees

Capital gains = Redemption value (₹) minus Purchase cost (₹)

Two rules govern this calculation:

- Use INR throughout: All calculations use the INR NAV at purchase and INR NAV at redemption. Do not calculate the gain in foreign currency and then convert.

- No indexation for post-April 2023 investments: For investments made on or after April 1, 2023, indexation benefit is not available. Pre-2023 lots may qualify under older rules — consult a tax professional about any applicable grandfathering provisions.

Step 4: Apply the Correct Tax Rate

- STCG: Add the gain to your total taxable income and apply your income slab rate.

- LTCG (more than 24 months, redeemed on or after April 1, 2025): Apply the 12.5% flat rate without indexation.

There is no annual exemption threshold for international fund LTCG — the 12.5% applies from the first rupee of gain.

Step 5: Report Gains Correctly in Your ITR

Gains from international mutual funds are reported under Schedule CG in your ITR. Because you own units of an Indian-domiciled fund — not foreign stocks or overseas fund units directly — these are not treated as foreign assets requiring disclosure in Schedule FA. Schedule FA applies to directly held foreign assets, such as stocks purchased through LRS.

Misreporting Indian FoF units under Schedule FA can create unnecessary scrutiny. This interpretation is based on the structure of ITR forms and the nature of the asset — if your situation involves direct overseas holdings alongside FoF units, confirm the correct treatment with a tax advisor.

Common Misconceptions and Tax Filing Mistakes

These five mistakes show up repeatedly in tax filings — and each one is avoidable with the right framework.

Mistake 1: Treating International Funds Like Equity Funds

International funds are classified as non-equity, so neither the 20% STCG rate nor the ₹1.25 lakh LTCG exemption applies. For an investor in the 30% tax bracket, short-term gains on an international fund are taxed at 30% — a full 10 percentage points higher than domestic equity funds.

Mistake 2: Applying the Wrong Holding Period

The 12-month threshold is specific to domestic equity funds. For international funds, the relevant cutoff is 24 months. Selling at the 13-month mark doesn't qualify for LTCG treatment — those gains are taxed at your applicable slab rate, which surprises many investors who assume equity-style rules apply.

Mistake 3: Applying Uniform Rules Across Investment Dates

Pre- and post-April 1, 2023 purchase lots in the same fund can carry different tax implications. Applying today's rules to older holdings without checking purchase dates leads to miscalculated liability. Each lot must be tracked separately — purchase date, cost basis, and applicable tax regime all matter.

Mistake 4: Omitting Dividend Income

Dividend income from international funds belongs under "Income from Other Sources" in your ITR. Even modest dividends must be declared — overlooking them creates underreporting exposure and increases the risk of a tax notice.

Mistake 5: Assuming Foreign Underlying Assets Mean No Indian Tax Reporting

The location of a fund's underlying assets doesn't determine reporting obligations. Indian fund units are taxable assets regardless of where the fund invests. Gains must be reported in Schedule CG — no exceptions.

Tax Planning Strategies for International Fund Investors in India

Holding Period Optimisation

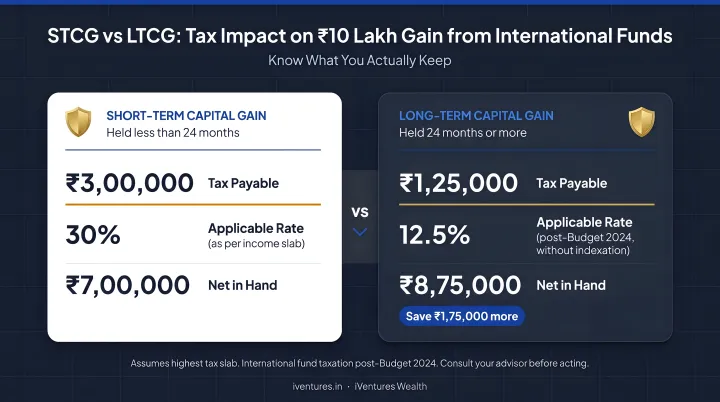

For investors in the 30% tax bracket, the difference between STCG and LTCG treatment is substantial. On a ₹10 lakh gain from an eligible international equity fund:

| Scenario | Tax Liability | Tax with 4% Cess |

|---|---|---|

| STCG at 30% (slab rate) | ₹3,00,000 | ₹3,12,000 |

| LTCG at 12.5% (after 24 months) | ₹1,25,000 | ₹1,30,000 |

| Savings by waiting | ₹1,75,000 | ₹1,82,000 |

The implication is clear: investors approaching the 24-month mark should think carefully before redeeming early. The tax saving from waiting even a few additional weeks — to cross the LTCG threshold — can be material, especially for larger holdings.

Tax-Loss Harvesting

Under Section 74 of the Income Tax Act, capital losses from international mutual funds can be used strategically:

- Short-term capital loss (STCL) can offset both STCG and LTCG from any asset class

- Long-term capital loss (LTCL) can only offset LTCG

- Unabsorbed losses can be carried forward for up to 8 assessment years

For investors with mixed portfolios of domestic and international funds, realising losses in an underperforming international fund position can offset gains elsewhere. One critical requirement: the ITR for the year in which the loss arises must be filed on or before the due date to preserve the carry-forward benefit.

Getting Personalised Guidance

Purchase dates, holding periods, Section 50AA applicability, and redemption timing interact in ways that a general framework alone cannot fully address. A SEBI-registered investment advisor can help structure international fund allocations with full visibility into these variables — mapping each position to its tax profile before any redemption decision is made.

iVentures Wealth works with UHNI and affluent investors on exactly this: capital gains computation, tax statement preparation, and coordination with chartered accountants for ITR filing. The goal is to ensure international holdings are tracked accurately and redemptions are timed with a clear view of the tax outcome.

Frequently Asked Questions

What are international mutual funds in India?

International mutual funds are Indian-registered schemes that invest in stocks, bonds, or fund units of companies based outside India. Investors buy and sell these funds in Indian rupees through domestic platforms, without requiring a foreign brokerage account or LRS remittance.

How are foreign investments taxed in India?

For Indian residents, gains on international mutual fund units are taxed as non-equity capital gains: STCG (held 24 months or less) at your income slab rate, and LTCG (held more than 24 months, redeemed on or after April 1, 2025) at 12.5% without indexation — applicable to units purchased on or after April 1, 2023. Dividend income is taxed at slab rate under "Income from Other Sources."

Is it worth investing in international mutual funds?

International funds offer diversification across global sectors and economic cycles that domestic equity cannot provide. However, the tax treatment is less favourable — no ₹1.25 lakh LTCG exemption, and STCG taxed at slab rate. Whether the benefit justifies the cost depends on your bracket, holding period, and portfolio goals.

What is the LTCG tax rate on international mutual funds after Budget 2024?

Following Budget 2024, the LTCG rate on eligible international mutual funds is 12.5% without indexation, applicable after a holding period of more than 24 months. This matches the domestic equity LTCG rate, but without the ₹1.25 lakh annual exemption that equity investors receive.

Can I claim indexation benefits on international mutual funds purchased after April 2023?

No. Indexation is not available for investments made on or after April 1, 2023. For older pre-2023 holdings, grandfathered rules may apply — consult a tax advisor to confirm treatment for your specific purchase dates.

Where do I report international mutual fund gains in my ITR?

Gains on Indian-domiciled international mutual funds (FoFs) are reported under Schedule CG. Since you hold Indian fund units — not foreign assets directly — Schedule FA is generally not triggered. Note that direct overseas investments through LRS, such as individually purchased foreign stocks, do require Schedule FA disclosure.