Introduction

India is in the middle of the largest intergenerational wealth transfer in its history. An estimated ₹110–170 lakh crore ($1.3–2 trillion) is expected to change hands over the next decade, passing from founders and patriarchs to the next generation — most without a clear plan for how that transfer should happen.

The problem isn't awareness. According to the 360 ONE/CRISIL Wealth Index (2025), 72% of UHNIs acknowledge the importance of succession planning — but only 32% have a formal plan in place. The gap between knowing and doing is where wealth gets lost.

Most affluent families spend decades building assets across equities, real estate, business interests, and insurance — then leave the transfer to chance. The consequences are predictable:

- Estate disputes that drag on for years

- Undiscovered fixed deposits and forgotten properties

- Nominees listed who are not the intended legal heirs

- Families fracturing over wealth that took a generation to build

None of this is inevitable. What's missing, in most cases, is a structured plan — and the discipline to put it in place before a crisis forces the issue.

This guide covers what succession planning actually involves, how to build one step by step, and the legal and behavioral pitfalls that derail even well-intentioned families.

Key Takeaways

- Wealth succession planning is the structured process of transferring assets, business interests, and financial wealth to the next generation — minimising legal disputes, taxes, and family conflict

- Beyond a Will, it covers heir preparation, governance structures, updated nominations, and tax-efficient legal vehicles

- In India, the nominee-vs-legal-heir distinction and personal law regimes make proper documentation non-negotiable

- Starting 5–10 years before a planned transition, with a SEBI-registered fiduciary, significantly improves outcomes

- The three most common failures: treating succession as a one-time event, avoiding difficult conversations, and siloing advisors

What Is Wealth Succession Planning?

Wealth succession planning is the proactive process of organizing how a family's financial assets, business interests, real estate, and other holdings will transfer to the next generation — with minimum tax friction, legal conflict, and family disruption.

It's broader than estate planning, which typically focuses on what happens after death. Succession planning also covers leadership transitions, heir readiness, and ongoing governance — the structures that keep family wealth intact long after the legal transfer is complete.

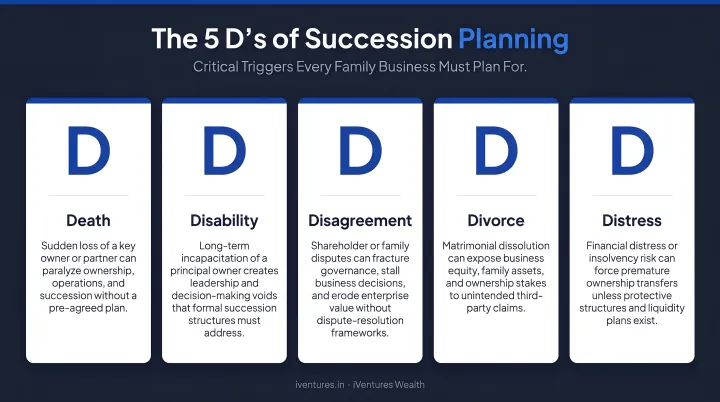

The 5 D's That Demand a Plan

Every succession plan needs to address five trigger events, not just one:

- Death — the most obvious trigger, yet most families still rely on informal arrangements

- Disability — sudden incapacity of the wealth creator with no documented succession pathway

- Disagreement — family conflict over ownership, distribution, or business direction

- Divorce — can involuntarily bring outsiders into ownership structures

- Distress — financial crisis forcing rushed, unplanned asset liquidation

Reacting to any of these events without a plan in place costs more — in money, time, and family relationships — than building the structure in advance.

The Five Forms of Family Wealth

Most succession plans address only financial capital. A complete plan covers all five:

| Form of Capital | What It Includes |

|---|---|

| Financial | Investments, property, business equity, insurance |

| Human | Skills, education, and capabilities of heirs |

| Intellectual | Business knowledge, strategy, institutional memory |

| Social | Relationships, networks, reputation |

| Ethical | Values, family culture, philanthropic commitments |

When families focus only on financial transfer, heirs often receive the assets without the knowledge or shared purpose to manage them well. The result is erosion — not from market forces, but from within the family itself.

Why Wealth Succession Planning Cannot Wait

The Generational Erosion Problem

Research by The Williams Group, based on a study of over 3,200 wealthy families, found that 70% lose their wealth by the second generation and 90% by the third. The primary causes had nothing to do with bad investments or excessive taxation. Communication breakdown within the family accounted for 60% of failures; inadequate heir preparation accounted for another 25%.

In the Indian context, the "shirtsleeves to shirtsleeves in three generations" pattern is compounded by specific structural gaps that go unaddressed until it's too late:

- Joint holdings with no documented ownership clarity

- Forgotten fixed deposits and insurance policies

- Undocumented or title-disputed properties

- Advisors operating in silos with no integrated succession view

What Undocumented Transitions Actually Cost

Three publicly documented Indian family succession disputes illustrate the pattern clearly:

| Family | Trigger | Duration | Key Lesson |

|---|---|---|---|

| Ambani (Reliance) | No Will | ~3 years (2002–2005) | Intestacy forced a family-mediated split; divergent outcomes across decades |

| Murugappa Group | Gender exclusion from board | ~6 years (2017–2023) | Daughters' rights not addressed; Company Law Tribunal filing followed |

| Bajaj Group | Sibling separation | ~7 years (2001–2008) | Company Law Board referral; resolved but consumed years of management attention |

Even the "faster" resolutions took years. Litigation through Indian courts routinely extends timelines to 10–20 years. Those years carry a second cost beyond legal fees: management attention pulled away from the business itself, often at exactly the moment continuity matters most.

The Tax Window You Shouldn't Ignore

Succession disputes aren't the only deferred cost families face. The tax structure around inherited wealth carries its own traps.

India abolished estate duty in 1985, so inheritance itself is currently tax-free. But capital gains tax applies when inherited assets are eventually sold. Under Section 49 of the Income Tax Act, the cost of acquisition traces back to what the previous owner originally paid — not the market value at time of inheritance. For assets held across decades, this creates substantial deferred tax liabilities that heirs rarely anticipate.

Structures like private family trusts, HUFs, and planned gifting can reduce this exposure — but only if built in advance. Once a wealth creator is no longer in the picture, the options narrow considerably.

The Key Components of a Comprehensive Succession Plan

A succession plan isn't a single document. It's a set of coordinated structures, all pointing in the same direction.

Will and Asset Register

The Will communicates intent. The asset register — a living document listing every account, policy, property, nominee, and institution — tells heirs where everything is.

Without both, succession becomes a forensic process. Families of iVentures Wealth clients have encountered this directly: the assumption that joint holdings and nominations were sufficient, only to find that nominees are custodians, not owners. Asset transfer still requires legal succession documentation to proceed without dispute.

A clear, legally valid Will aligned with updated nominations eliminates this ambiguity.

Legal Structures for Wealth Transfer

Two structures are most commonly used in Indian succession planning:

Private family trusts (governed by the Indian Trusts Act, 1882) allow families to:

- Separate legal ownership from beneficial enjoyment

- Ring-fence assets from succession disputes

- Set structured distribution rules across generations

- Avoid probate and maintain privacy

Trusts are particularly valuable for complex, multi-asset families — those with business holdings, NRI beneficiaries, or special-needs dependants. iVentures Wealth has structured private trusts naming specific beneficiaries for clients where clarity of distribution and governance was essential.

Hindu Undivided Families (HUF) function as a separate taxable entity under the Income Tax Act, providing both succession structure and tax efficiency within families governed by the Hindu Succession Act. The right structure depends on asset complexity, family composition, and tax objectives. Most families benefit from a combination of vehicles rather than any single one.

Successor Identification and Heir Preparation

Structures alone don't complete a succession plan — people do. Identifying the right successors means assessing more than availability or interest. The evaluation should cover:

- Financial literacy and decision-making capability

- Alignment with family values and long-term goals

- Whether the role is active (operational) or passive (beneficiary/board)

- Readiness timeline and gaps to address

Heir preparation is an ongoing process, not a handover event. iVentures Wealth's NextGen programs build this readiness through investment reviews, financial literacy sessions, and structured mentorship — all within the family governance framework. The goal is confident stewardship, not just legal ownership.

Family Governance and Communication

Family councils and governance frameworks prevent disputes by establishing rules before disagreements arise. These frameworks cover ownership decisions, investment mandates, profit distribution, and conflict resolution mechanisms.

iVentures Wealth assists families in drafting family charters and constitutions that provide a clear framework against which major decisions can be made. Transparent communication of the succession plan to all stakeholders is as important as the plan itself. Families that keep the plan opaque often generate the exact disputes they were trying to avoid.

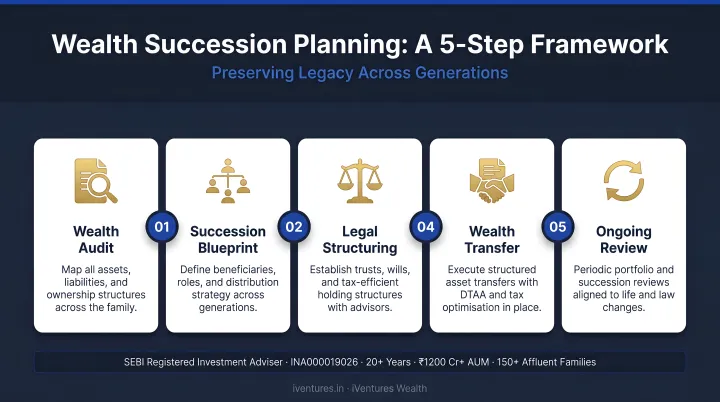

How to Build Your Wealth Succession Plan: Step by Step

Step 1: Conduct a complete wealth audit Map every asset class: equities, mutual funds, real estate, insurance policies, business interests, digital assets, demat holdings, and foreign holdings. Verify that nominations are updated and aligned with succession intent. Identify gaps — assets held in a single name with no nominee are a common and easily overlooked risk.

Step 2: Define your succession goals and timeline Clarify what you want to preserve: financial wealth, business continuity, family unity, or philanthropic legacy. Identify beneficiaries and the expected transition timeline. Succession planning works best when started 5–10 years before the intended transition.

Step 3: Choose and structure your legal vehicles Work with legal and tax advisors to determine the right combination — Will, trust, HUF, or some mix of all three — based on asset complexity, family structure, and tax efficiency. Ensure structures are reviewed against the applicable succession laws for your community.

Step 4: Identify and prepare successors Have explicit conversations with potential successors about their roles, responsibilities, and readiness. These conversations are rarely easy, which is why many families engage a fiduciary advisor to structure them. iVentures Wealth has guided 150+ affluent families through this process, helping develop succession roadmaps that reflect both financial priorities and family values.

Step 5: Document, communicate, and keep it current Formalise the plan in writing and share it with key stakeholders and your advisory team. This document should evolve as your circumstances do — revisit it when major life events occur: marriage, birth, business changes, significant regulatory updates (such as SEBI's January 2025 nomination circular, which now allows up to 10 nominees per account), or material shifts in asset composition.

India-Specific Legal Considerations You Cannot Ignore

Two Modes of Succession

| Mode | Applies When | Governing Law |

|---|---|---|

| Testate succession | A valid Will exists | Hindu Succession Act 1956 (Hindus, Buddhists, Jains, Sikhs); Indian Succession Act 1925 (Christians, Parsis, Special Marriage Act) |

| Intestate succession | No Will exists | Personal laws of the deceased — outcomes can diverge sharply from the wealth creator's intent |

| Muslim succession | Deceased is Muslim | Muslim Personal Law (Shariat Application Act 1937) — fixed shares apply regardless of a Will's instructions |

The applicable law follows the religious affiliation of the deceased. For families with members across communities or jurisdictions, disputes can span multiple courts and legal frameworks simultaneously.

The Nominee Is Not the Owner

This is the most frequently misunderstood gap in Indian succession planning. A nominee is a custodian — not the legal owner of an asset. Legal heirs, as defined by applicable succession law, retain ultimate rights. Nomination does not override a Will or the laws of intestate succession.

Indian courts — including the Supreme Court — have consistently affirmed this across three regulatory domains:

- Banking: Nominees receive funds as custodians, not owners

- Companies Act: Share transmission to nominees does not extinguish heirs' rights

- Depositories Act: Demat holdings follow the same custodian principle

A Will that is aligned with nominations is the only way to prevent conflict between nominees and legal heirs.

Daughters' Equal Rights in Ancestral Property

The Supreme Court's 2020 ruling in Vineeta Sharma v Rakesh Sharma (2020) 9 SCC 1 settled a long-standing ambiguity: daughters have equal coparcenary rights in ancestral property by birth, regardless of whether the father was alive at the time of the 2005 amendment to the Hindu Succession Act.

This has direct implications for family business ownership. Any succession plan that does not explicitly account for daughters as equal coparceners risks legal challenge — as the Murugappa Group family dispute demonstrated over six years in court.

Common Mistakes That Derail Succession Plans

Mistake 1 — Plans go stale when life doesn't. Many families create a Will or trust structure and never revisit it. Life changes: new heirs arrive, businesses are sold, assets are added, laws are amended. An outdated plan can be as harmful as no plan at all. Annual reviews are the standard — with additional reviews triggered by marriage, birth, death, business restructuring, or material regulatory changes.

Mistake 2 — Emotion delays what logic demands. Morgan Stanley's October 2024 analysis identifies founder identity inseparability as a primary barrier — when stepping away feels existential rather than operational. Conflict avoidance within families compounds this, leading to decisions that prioritise short-term peace over long-term financial soundness. A neutral, professional fiduciary advisor surfaces and resolves these blockers in a way that family members often cannot do among themselves.

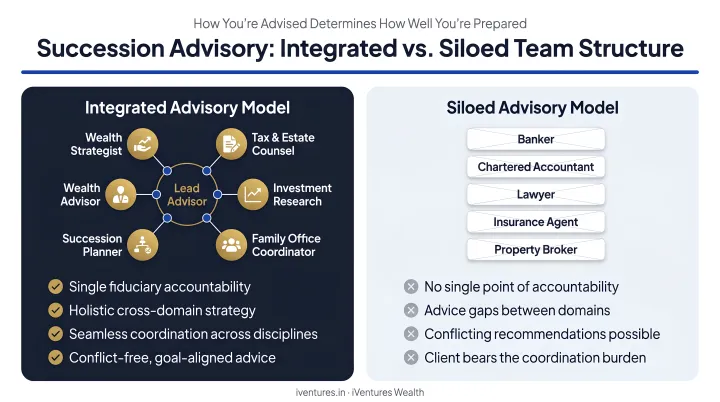

Mistake 3 — Siloed advisors leave dangerous gaps. Succession planning sits at the intersection of investment management, tax planning, legal structuring, and family dynamics. When a lawyer drafts documents without knowing the investment structure, and a CA optimises tax without knowing the trust deed, gaps form.

The most resilient plans use a coordinated advisory team — one where succession planning, family governance, tax coordination, and investment management operate under a single integrated mandate, rather than in separate conversations.

Frequently Asked Questions

What is wealth succession planning?

Wealth succession planning is the structured process of organising how a family's assets, business interests, and wealth transfer to the next generation — minimising taxes, disputes, and disruption through tools like Wills, trusts, and governance frameworks. Unlike estate planning, it also covers heir preparation and family governance.

What are the 5 steps of succession planning?

The five core steps are: conducting a wealth audit, defining succession goals and timelines, selecting appropriate legal structures, identifying and preparing successors, and reviewing the plan regularly as life and regulatory circumstances evolve.

What are the 5 D's of succession planning?

The 5 D's — Death, Disability, Disagreement, Divorce, and Distress — are the five trigger events that can force an unplanned succession. A well-built plan prepares for each scenario in advance, rather than requiring reactive decisions under pressure.

What are the 4 types of succession?

The four types are: family/internal succession (passing to heirs), management succession (transferring to professional managers), external succession (sale or merger), and emergency succession (unplanned transition due to sudden events). Most Indian family businesses default to the first without formal planning.

What is included in wealth management?

Wealth management encompasses investment advisory, tax planning, estate and succession planning, risk management, retirement planning, and philanthropy — all coordinated to protect and grow a family's financial position across generations.

What are the 4 stages of wealth management?

The four stages are: wealth accumulation, wealth preservation (protecting against loss and tax erosion), wealth distribution (planned transfer to heirs or causes), and wealth legacy — ensuring the family's values and impact endure across generations.