Both structures pool investor capital. Both are SEBI-regulated. But they're built for different investors, invest in fundamentally different assets, and serve different roles in a portfolio. The choice isn't about which is "better" — it's about what fits your financial situation.

SEBI governs AIFs under the SEBI (Alternative Investment Funds) Regulations, 2012 and mutual funds under the SEBI (Mutual Funds) Regulations, 2026 (effective April 1, 2026). This article breaks down the structural, strategic, and suitability differences clearly.

Key Takeaways

- AIFs require a minimum investment of ₹1 crore per investor; mutual funds start at ₹500 via SIP

- AIFs access private equity, venture capital, private credit, and hedge strategies not available through mutual funds

- Mutual funds offer daily redemption; most AIFs carry a minimum 3-year lock-in

- Tax treatment differs by AIF category: Cat I & II are pass-through; Cat III is taxed at the fund level

- Neither is universally better — suitability depends on portfolio size, liquidity needs, and investment horizon

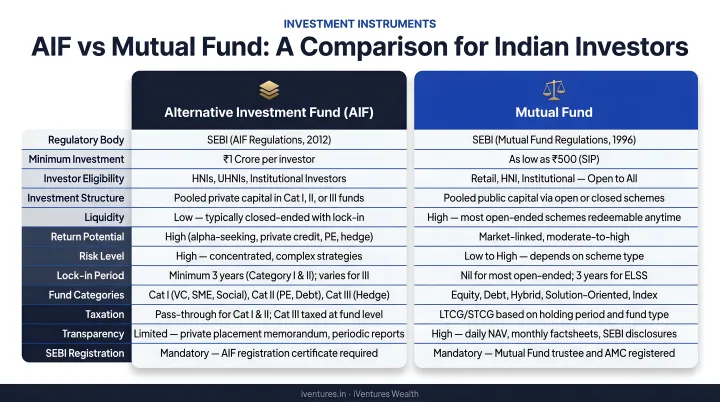

AIF vs Mutual Funds: Quick Comparison

| Parameter | AIF | Mutual Fund |

|---|---|---|

| Minimum Investment | ₹1 crore (₹25 lakh for employees/directors) | SIP from ₹500/month |

| Target Investor | HNIs, UHNIs, institutions | Retail to institutional |

| Investor Cap | 1,000 per scheme | No cap |

| Regulation | SEBI AIF Regulations, 2012 | SEBI (Mutual Funds) Regulations, 1996 |

| Asset Classes | Unlisted equity, private debt, real estate, hedge strategies | Listed equities, bonds, money market |

| Liquidity | Illiquid during lock-in; largely closed-ended | Open-ended: daily redemption; closed-ended: listed on exchange |

| Lock-in Period | Minimum 3 years (Category I & II); Category III may be open-ended | None for open-ended funds |

| Transparency | PPM; annual reports; quarterly for Category III | Daily NAV; monthly portfolio disclosures |

| Fee Structure | Management fee (1–2%) + performance fee | SEBI-capped TER (up to 2.25% for equity) |

| Tax Treatment | Pass-through for Cat I & II; fund-level for Cat III | Standardised — equity LTCG at 12.5% above ₹1.25 lakh; STCG at 20% |

These parameters frame the comparison — but the right choice turns on your specific situation: how much capital you're deploying, how long you can stay illiquid, your tax position, and what role this investment plays in your broader portfolio. The sections below break down suitability in detail.

What Is an AIF?

An Alternative Investment Fund is a privately pooled investment vehicle registered under the SEBI (AIF) Regulations, 2012. It collects capital from a select group of sophisticated investors and deploys it into asset classes typically inaccessible through conventional mutual funds — unlisted companies, private credit, real estate, and complex trading strategies.

AIFs raise capital through private placement only. They cannot solicit funds from the public. As of June 2026, 1,944 AIFs are registered with SEBI, with total commitments of ₹15,74,050 crore as of December 31, 2025.

The Three SEBI Categories

| Category | Description | Leverage |

|---|---|---|

| Category I | Venture capital, angel, infrastructure, SME, social venture funds — economically beneficial sectors | Temporary borrowing only |

| Category II | Private equity, private debt, real estate funds — no specific incentives or concessions | No leverage beyond operational needs |

| Category III | Hedge funds, long-short strategies, complex trading — can use leverage and derivatives | Permitted with investor consent and SEBI limits |

Structural features common to most AIFs:

- Maximum 1,000 investors per scheme

- Closed-ended structure (Category I & II); Category III may be open or closed

- Governed by a Private Placement Memorandum (PPM)

- Minimum investment: ₹1 crore per investor (₹25 lakh for employees or directors of the fund)

Use Cases for AIFs

AIFs serve specific portfolio stages and objectives:

- Category II private credit AIF: structured debt with collateral, targeting 13–16% gross IRR; suited for HNIs seeking inflation-beating yield over traditional fixed deposits

- Category III long-short equity AIF: market-neutral strategies targeting absolute returns uncorrelated with index movements

- Category I VC fund: early-stage startup exposure for investors seeking private company growth ahead of public listings

In practice, private credit within Category II tends to anchor the alternative allocation for many HNI and UHNI portfolios — senior secured lending with 2–3× collateral coverage and quarterly distributions can serve as a predictable yield engine alongside equity-heavy holdings.

What Is a Mutual Fund?

A mutual fund is a publicly offered, SEBI-regulated pooled investment vehicle. It collects money from a large number of investors and deploys it into listed equities, bonds, money market instruments, or a blend of these — managed by a professional AMC (Asset Management Company).

AMFI reports mutual fund AUM at ₹81,58,342 crore as of May 31, 2026 — a scale that reflects decades of retail participation across income levels.

What makes mutual funds accessible:

- No upper limit on investors per scheme

- SIP starting at ₹500/month (₹250/month under Chhoti SIP)

- Daily NAV-based pricing with full transparency

- Monthly portfolio disclosures within 10 working days

- SEBI-capped TERs: up to 2.25% for equity funds on first ₹500 crore of daily net assets

- Wide category range: equity, debt, hybrid, index, ELSS, and more

Use Cases for Mutual Funds

Mutual funds serve distinct roles across investor profiles:

- Salaried professionals building retirement or education corpora through monthly SIPs

- HNIs maintaining a liquid core portfolio with daily redemption flexibility

- Retail investors seeking diversified market exposure with regulatory safeguards

- Institutional investors requiring compliance-ready, transparent allocation

Their liquidity, regulatory transparency, and low entry thresholds make mutual funds a practical baseline — though how much weight they carry in a portfolio depends heavily on the investor's net worth, risk appetite, and access to alternative structures like AIFs.

AIF vs Mutual Funds: Key Differences That Matter

Accessibility and Minimum Investment

The entry barrier is the most immediate difference. Mutual funds are open to any Indian resident or NRI with ₹500 for an SIP. AIFs require ₹1 crore per investor — a threshold that immediately restricts access to HNIs and institutional investors.

There's also a structural cap: each AIF scheme is limited to 1,000 investors, while mutual funds have no equivalent restriction.

Asset Classes and Investment Strategy

Mutual funds are confined to listed securities and must follow SEBI-mandated categories and diversification norms. AIFs have significantly more flexibility:

- Unlisted equity and pre-IPO exposure

- Private debt and structured credit

- Real estate-linked strategies

- Leverage and derivatives (Category III)

- Early-stage venture capital

This flexibility is what makes AIFs attractive for portfolio diversification beyond public markets — not because they're inherently superior, but because they access return streams that mutual funds structurally cannot.

Liquidity and Lock-in

Open-ended mutual funds allow daily redemption at NAV; closed-ended funds list on stock exchanges. Either way, an exit mechanism exists.

AIFs work differently. Category I and Category II AIFs are closed-ended with a SEBI-mandated minimum tenure of 3 years. PE and VC funds often run longer in practice. Category III AIFs may be open or closed-ended.

The liquidity constraint is real, not theoretical: capital is locked up for the fund's tenure with no guaranteed exit. For most investors, this single factor determines AIF suitability more than any other.

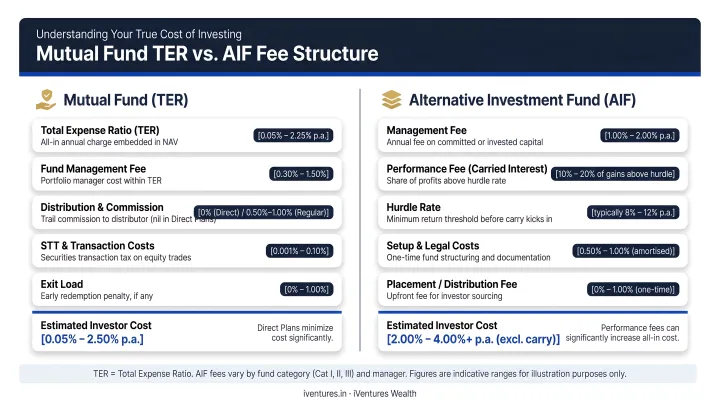

Fee Structure and Cost

| Mutual Funds | AIFs | |

|---|---|---|

| Fee type | Total Expense Ratio (TER) | Management fee + performance fee |

| SEBI cap | Yes — by AUM slab and category | No equivalent TER cap |

| Typical range | 0.80–2.25% (equity funds) | 1–2% management fee; performance fee above hurdle |

| Disclosure | Standardised SEBI norms | PPM-disclosed; material changes notified |

The key distinction: mutual fund costs are capped and standardised. AIF economics are disclosed in the PPM and vary by fund — so comparing total cost (management fee plus carried interest) across funds is essential before committing capital.

Tax Treatment

Under the Finance (No. 2) Act, 2024, equity-oriented mutual fund taxation stands at:

- LTCG: 12.5% above ₹1.25 lakh (for transfers on or after July 23, 2024)

- STCG: 20% (Section 111A)

- Debt funds acquired on or after April 1, 2023: gains taxed at applicable slab rates under Section 50AA

For AIFs, the tax treatment under Section 115UB works differently:

- Category I and II AIFs: Pass-through status — income (other than business income) is taxed in the hands of investors, not at the fund level

- Category III AIFs: Outside Section 115UB's definition; taxed at the fund level

Category III tax rates are not published here as exact surcharge tables were not confirmed from primary sources — consult a qualified tax adviser for current applicable rates.

Transparency and Reporting

Mutual funds publish daily NAVs and monthly portfolio disclosures within 10 working days. Risk-o-meter labelling is mandatory per SEBI circular — standardised, predictable, and investor-accessible.

AIFs are private placement vehicles by design, so disclosure works differently. All AIFs provide annual reports; Category III AIFs must additionally provide quarterly investor reports within 60 days. Investors should review the PPM upfront to understand exactly what reporting cadence to expect from a specific fund.

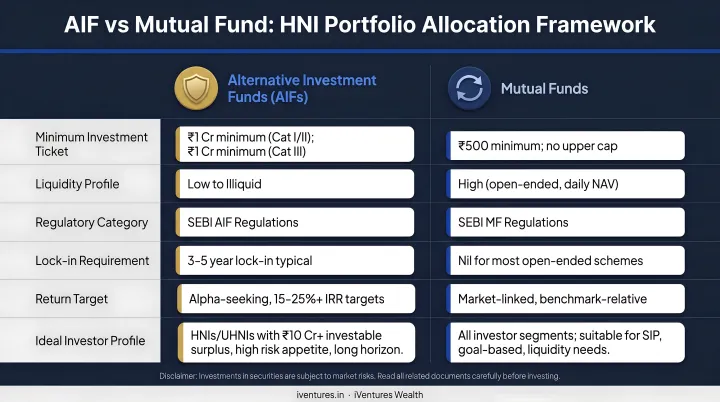

Which Is Right for You: AIF or Mutual Fund?

The decision comes down to four factors: portfolio size, liquidity requirements, risk appetite, and time horizon.

Choose Mutual Funds If:

- You're building your core wealth portfolio

- You need liquidity for near-term or medium-term goals

- Your investable surplus is below ₹1 crore

- You prefer daily transparency and regulatory simplicity

- You're using SIPs for disciplined long-term compounding

Mutual funds are the foundation. They belong in every portfolio at every stage.

Consider AIFs If:

- You have a ₹3 crore+ investable surplus with a liquid core already in place

- You can commit ₹1 crore+ for a minimum of 3 years without impacting your financial flexibility

- You're seeking returns from private markets — credit, equity, or market-neutral strategies — unavailable through mutual funds

- You have access to qualified advisory support to evaluate PPMs, fund managers, and fee structures

For UHNIs and family offices, AIFs and mutual funds aren't substitutes — they coexist. Mutual funds provide liquidity and core market exposure; AIFs provide diversification into private credit, pre-IPO equity, or absolute-return strategies.

AIF selection demands specific expertise: evaluating fund managers, comparing vintage performance, assessing collateral quality in private credit, and mapping each fund's tax implications to your broader portfolio. iVentures Wealth, a SEBI-registered, fee-only investment adviser, works with HNIs and UHNIs to assess AIF opportunities across all three categories — with no commission bias influencing the recommendation.

Conclusion

The AIF vs mutual fund question isn't a binary choice. It's a portfolio construction question.

Mutual funds offer accessibility, daily liquidity, and regulatory transparency suited to a broad investor base — from first-time SIP investors to large institutional allocators. AIFs open the door to private markets and alternative, illiquid strategies, but only for investors who meet the eligibility criteria and can genuinely absorb the liquidity constraints.

As investable wealth grows, the portfolio naturally evolves. What begins with mutual fund SIPs can, over time, incorporate AIFs as one component of a diversified, goal-aligned strategy.

Evaluate your current stage honestly before deciding. The questions that matter most:

- How much liquidity do you need in the near term?

- What surplus can you lock away for 3–7 years?

- What is your realistic time horizon for each goal?

- Can you absorb drawdowns without disrupting your financial plan?

Build your allocation from honest answers to these — not from product novelty or market momentum. An independent advisor can help map where you stand today and structure a portfolio that earns the right to complexity over time.

Frequently Asked Questions

Is an AIF a mutual fund?

No. Both are SEBI-regulated pooled vehicles, but they operate under entirely separate regulatory frameworks. AIFs are privately placed, require a minimum ₹1 crore investment, and are restricted to HNIs and institutions. Mutual funds are publicly offered and open to retail investors starting at ₹500.

Is AIF tax-free?

AIFs are not universally tax-free. Category I and II AIFs have pass-through status under Section 115UB — income is taxed in the hands of investors, not at the fund level. Category III AIFs fall outside this definition and are taxed at the fund level. Confirm applicable rates with a qualified tax adviser.

What is the minimum investment required for an AIF in India?

SEBI mandates a minimum of ₹1 crore per investor. An exception applies to employees, directors, or fund managers of the AIF, who may invest a minimum of ₹25 lakh. Each AIF scheme is also capped at a maximum of 1,000 investors.

Can NRIs invest in AIFs in India?

Yes, NRIs and foreign nationals can invest in Indian AIFs, subject to FEMA regulations and applicable repatriation rules under the Foreign Exchange Management (Non-Debt Instruments) Rules, 2019 — with USD-denominated allocations available for GIFT City-domiciled funds. Tax treatment may differ from that of resident investors.

What are the three categories of AIFs in India?

- Category I: Venture capital, infrastructure, social venture, and SME funds — sectors considered economically beneficial

- Category II: Private equity, private debt, and real estate funds — no leverage beyond operational needs

- Category III: Hedge funds and long-short strategies — leverage and complex derivatives permitted

Are AIFs riskier than mutual funds?

Generally, yes — due to illiquid or unlisted asset exposure, potential leverage in Category III, and lock-in periods that limit exit flexibility. However, risk varies significantly by category: a Category II secured private credit AIF with 2–3× collateral coverage has a fundamentally different risk profile than an equity-heavy mutual fund. The right comparison depends on the specific strategy, not the category label.