Introduction

Picture this: a 45-year-old senior manager in Gurugram, earning well, contributing to EPF, running a few SIPs — but with no clear answer to the question, "Will I actually have enough?" That's not an unusual situation. It's remarkably common.

Unlike government employees with defined pension benefits, India's private sector workforce has no universal retirement guarantee. NPS and APY together covered just 3.7% of India's total population as of 2021-22 — a strikingly thin safety net.

A 2026 survey by 1 Finance found that **75.5% of middle-aged earners lack a detailed retirement plan**, with a median corpus of just ₹28 lakh against a ₹1 crore target.

Life expectancy has climbed to 72+ years (World Bank, 2024), and healthcare costs are rising at 12–14% annually. The numbers demand a plan — not a rough estimate.

This guide gives you concrete savings benchmarks by decade, corpus calculation frameworks, and actionable strategies — whether you're just starting or need to catch up fast.

Key Takeaways

- Target 10–12x your annual income saved before retirement (India's inflation may push this higher)

- Start saving 15–20% of gross income in your 20s — increase this rate every decade

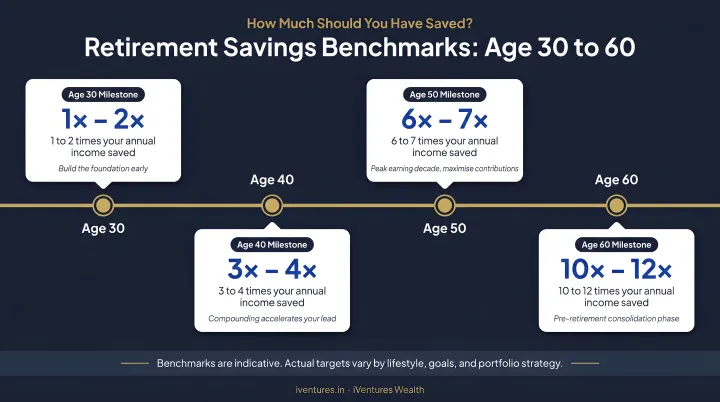

- Use salary-multiple checkpoints: roughly 1x by 30, 3x by 40, 5x by 50, 8x by 60

- Indian retirees should use a 3–3.5% safe withdrawal rate, not the Western 4% benchmark

- Starting late? A higher savings rate, extended working years, and portfolio restructuring can still close the gap

How Much Retirement Corpus Do You Actually Need?

Most people underestimate their retirement corpus — often by a wide margin. The core reason: inflation compounds expenses just as returns compound savings, and the two rarely get planned together.

The Income Replacement Starting Point

Most financial planners recommend replacing 70–80% of your pre-retirement income annually during retirement. For affluent professionals and HNIs with established lifestyle expenses, this figure often sits closer to 80–100%.

Here's a simple illustration. If your household spends ₹1.5 lakh per month today and you plan to retire in 25 years, at India's historical average CPI inflation of approximately 5.1% per year over 2014–2024, that same lifestyle will cost roughly ₹5.1 lakh per month at retirement. Annual retirement expense: ₹61 lakh.

Healthcare is a separate problem. Industry estimates put medical cost inflation at 12–14% annually in India — nearly triple general CPI. This category deserves its own budget line, not just a footnote. These two inflation pressures — general and medical — are precisely why calculating a corpus target requires more than a single multiplier.

The Corpus Formula

The standard approach:

Retirement Corpus = Annual Retirement Expense ÷ Safe Withdrawal Rate

For Indian retirees, a 3–3.5% safe withdrawal rate is more appropriate than the Western 4% benchmark due to higher structural inflation. At iVentures Wealth, advisors apply this same adjustment — starting with the 4% rule and calibrating down to 3–3.5% based on portfolio composition and each client's risk profile.

Worked example:

- Annual retirement expense (inflation-adjusted): ₹61 lakh

- Safe withdrawal rate: 3.5%

- Required corpus: ₹61,00,000 ÷ 0.035 = approximately ₹17.4 crore

This figure aligns with Mint's 2024 analysis, which arrived at ₹15–16 crore for ₹1.5 lakh/month post-retirement income — assuming retirement at 60, life expectancy of 85, and 6% post-retirement inflation.

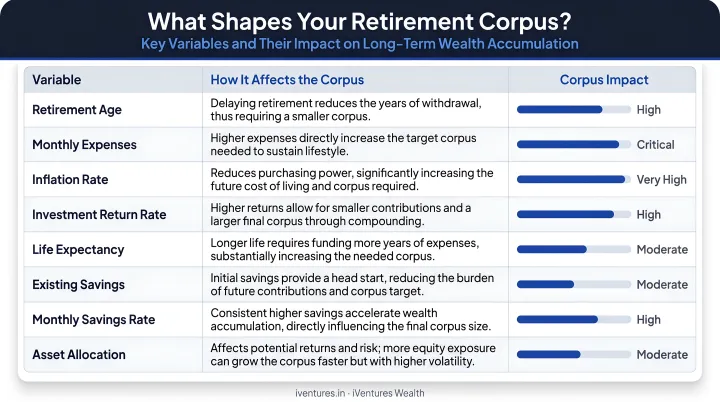

Variables That Change Your Target

| Factor | Impact on Corpus |

|---|---|

| Retiring at 55 vs. 65 | 10 extra years of drawdown; materially larger corpus needed |

| Planning to age 85 vs. 75 | Adds 10 more years of expenses |

| Healthcare costs | Budget separately; 12–14% inflation applies |

| Guaranteed income (EPF, NPS annuity, rent) | Reduces the corpus you must self-fund |

The PGIM India Retirement Readiness Survey 2025 puts the target retirement corpus at 10–12x annual income — a useful starting benchmark. Retirement age, healthcare exposure, and guaranteed income streams are the variables that move individual targets furthest from this range.

Retirement Savings Goals by Age: A Decade-by-Decade Breakdown

Savings in Your 20s: Building the Foundation

Benchmark: 0.5–1x annual salary by age 30 Savings rate target: 10–15% of gross income

Your 20s are when compounding does its heaviest lifting. A ₹5,000/month SIP in an equity mutual fund, started at age 25, grows to approximately ₹1.75 crore over 35 years at a 12% assumed annual return — without a single rupee added. Start the same SIP at 35 and the outcome drops to roughly ₹65–70 lakh. The difference isn't effort or income — it's the decade of compounding you can never recover.

Practical steps:

- Enrol in EPF from day one — your employer contributes 12% of basic wages, and your matched 12% goes directly toward your retirement base

- Open a PPF account (current rate: 7.1% p.a., tax-free maturity after 15 years) or an NPS Tier I account for additional long-term accumulation

- Build a 3–6 month emergency fund before aggressively investing

- Redirect every salary increment toward savings before lifestyle expands to fill it

Savings in Your 30s: Accelerating Growth

Benchmark: 2–3x annual salary by age 40 Savings rate target: 15–20% of gross income

Your 30s typically bring your fastest income growth — but also your biggest expenses: home purchases, children, insurance. The risk isn't that you'll earn less. It's that you'll spend more and save the same.

Practical steps:

- Maximise EPF contributions; consider Voluntary Provident Fund (VPF) top-ups above the mandatory 12%

- Continue NPS contributions — particularly valuable for the Section 80CCD(1B) additional ₹50,000 deduction

- Weight your mutual fund SIP portfolio toward equity funds; a 25–30 year horizon can absorb near-term volatility

- Avoid withdrawing from retirement accounts for short-term needs — the compounding disruption is far costlier than it appears

A 50% equity, 25% debt, 25% gold allocation historically delivered around 13.2% CAGR — close to a pure equity return but with measurably lower volatility. That trade-off matters for portfolios you cannot afford to abandon in a downturn.

Savings in Your 40s: Entering Prime Earning Years

Benchmark: 4–5x annual salary by age 50 Savings rate target: 20–25% of gross income

For most professionals, the 40s are peak earning years. They're also when home loan EMIs, school fees, and aging parent care costs all converge. Without deliberate structure, retirement savings stagnate even as income climbs.

Practical steps:

- Set up a goal-based financial plan that explicitly separates retirement from children's education, property purchases, and other goals

- Build a diversified portfolio across equity, debt, and alternative assets if you haven't already

- Review insurance coverage seriously: adequate term life and health cover prevents one unforeseen event from depleting the retirement corpus

This decade is when working with a SEBI-registered investment adviser pays for itself. Many affluent professionals in their 40s have accumulated assets across EPF, NPS, multiple mutual funds, FDs, and property — but no unified picture of whether they're actually on track.

Savings in Your 50s: The Critical Decade

Benchmark: 6–8x annual salary by age 60 Savings rate target: 25–30% of gross income

With 10–15 years remaining, compounding still works — but there's less room to recover from mistakes. Decisions made here define whether the retirement you planned for is actually available to you.

Practical steps:

- If behind, aggressively cut discretionary spending and redirect the freed-up cash to retirement accounts; even a 5% increase in savings rate at this stage matters significantly

- Begin gradual portfolio rebalancing — not an abrupt shift, but a steady move toward lower-volatility assets as retirement approaches

- Research senior citizen health insurance plans now, before health conditions make coverage expensive or unavailable

- Map all anticipated income sources: EPF corpus, NPS annuity/lump sum, PPF maturity, investment portfolio, rental income

One calculation worth running: extending your working years by just 2–3 years both grows the corpus further and shortens the drawdown period. For someone whose corpus is ₹2 crore short of target, retiring at 62 instead of 59 can close much of that gap.

Savings in Your 60s: The Final Approach

Benchmark: 10–12x annual salary before retiring Priority: Validation and withdrawal planning, not accumulation

Key account timelines to know:

- EPF: Full withdrawal on retirement or two months after ceasing employment; EPS pension begins at age 58

- PPF: Matures after 15 financial years; extendable in 5-year blocks; withdrawals permitted from year 7

- NPS: Normal exit at age 60; non-government subscribers can now take up to 80% as lump sum (corpus above ₹12 lakh), with minimum 20% in annuity — per PFRDA's December 2025 amendment

Practical steps:

- Plan your withdrawal architecture: SWP from mutual funds for monthly income, NPS annuity for guaranteed base, FD laddering for near-term liquidity

- Avoid concentrating remaining wealth in a single asset class

- Update nominees across all accounts and begin estate planning discussions — will, family communication, and a consolidated asset record

Essential Retirement Savings Rules of Thumb

The Safe Withdrawal Rule (4% — or 3.5% for India)

The 4% rule, established by William Bengen in 1994, holds that withdrawing 4% of your retirement corpus annually — adjusted for inflation — should sustain a portfolio for 30+ years. In India, given structurally higher inflation, many planners now recommend 3–3.5% as a more conservative baseline.

In practice: divide your annual retirement expense by 0.035 to get your corpus target. For every ₹10 lakh of annual expenses, you need roughly ₹2.86 crore — a 28–29x multiplier, compared to the Western benchmark of 25x.

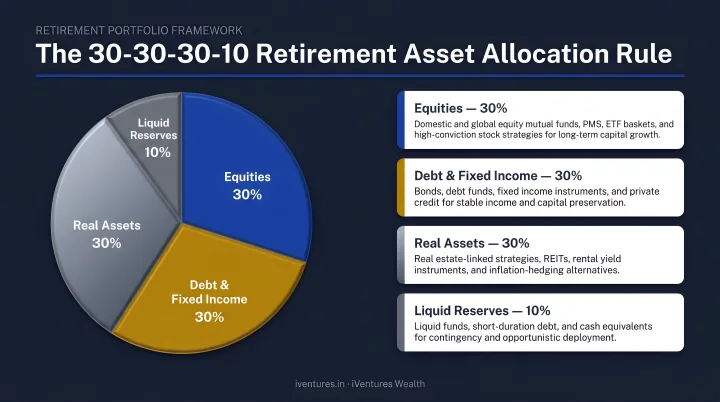

The 30-30-30-10 Allocation Rule

Indian financial planners commonly use this as a retirement asset-allocation framework:

- 30% in growth assets (equity) for long-term appreciation

- 30% in stable assets (debt/bonds) for capital preservation

- 30% in income-generating assets (real estate, REITs) for cash flows

- 10% as liquid reserves for emergencies and near-term expenses

This allocation is most relevant for those near or in retirement. Younger investors should maintain higher equity exposure — the equity component should dominate in your 20s and 30s, with gradual shifts as retirement approaches.

The 70-20-10 Budgeting Rule

This budgeting rule divides income into three buckets: 70% for living expenses, 20% for savings and investments, and 10% for discretionary goals or an emergency buffer.

For those serious about retirement, the savings component should grow with age and income. By your 40s, a 25–30% savings rate is the more appropriate target. Treat the 70-20-10 framework as a starting structure, not a fixed ceiling.

What If You're Behind? Strategies to Catch Up

Only 37% of Indians had a retirement plan in 2025, down from 67% in 2023. If you're in your 40s or 50s and behind on savings, you're not alone — and the situation is recoverable with the right levers.

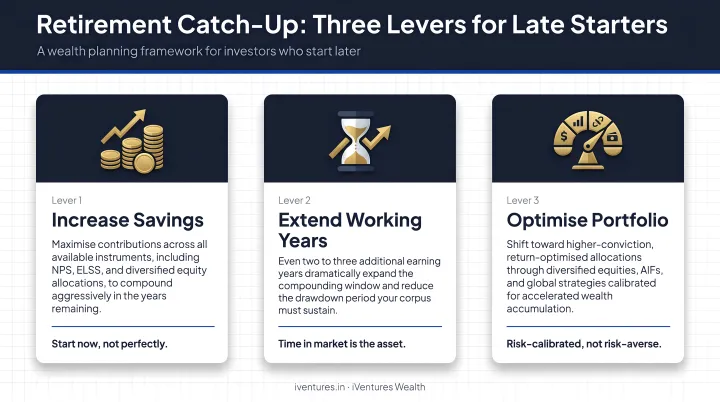

Three Levers That Move the Needle

- Increase your savings rate — Even 5% more of gross income redirected to investments at age 48 can add crores to your corpus by retirement. Bonuses and windfalls redirected rather than spent accelerate this further.

- Extend your working period — Retiring at 62 instead of 58 grows the corpus for four more years while shrinking the drawdown period. For most people, this is the single highest-impact lever available.

- Optimise portfolio returns — Many late-starters hold portfolios that are too conservative (excessive FD/cash) or too scattered (dozens of underperforming funds). Restructuring into a focused, appropriately allocated portfolio can meaningfully improve returns without taking undue risk.

India-Specific Catch-Up Tactics

- Maximise NPS contributions — the additional ₹50,000 deduction under Section 80CCD(1B) is straightforward and tax-efficient

- Assess your property — consider whether downsizing housing could release capital for reinvestment, or whether rental income can serve as a retirement income pillar

- Consolidate scattered assets — many professionals in their late 40s hold 10–15 mutual funds, multiple FDs, NPS, EPF, and property with no unified view of total wealth or retirement readiness

That third point — consolidated assets — is where many affluent professionals get stuck. Holding wealth across a dozen instruments without a unified withdrawal strategy is common; converting it into dependable retirement income is a different challenge entirely.

For HNIs and UHNIs in this position, working with a SEBI-registered investment adviser adds the most value. iVentures Wealth's retirement planning approach maps every asset to a specific goal, builds multi-asset portfolios across equity, debt, alternatives, and global exposures, and structures tax-efficient withdrawal strategies for professionals who have accumulated wealth but need a plan to actually live off it.

Frequently Asked Questions

What is the 30-30-30-10 rule for retirement?

It's an asset allocation framework suggesting 30% each in growth assets (equity), stable assets (debt/bonds), and income-generating assets (real estate/REITs), with 10% as liquid reserves. Most useful for those approaching or in retirement — younger investors should carry far more equity.

What is the ideal retirement amount by age in India?

A practical starting benchmark: approximately 1x annual salary by 30, 3x by 40, 5x by 50, 8x by 60, and 10–12x at retirement. These are directional targets; your actual number depends on lifestyle, planned retirement age, and income replacement goals.

What is the 7% rule for retirement?

The 7% rule refers to a long-term assumed annual investment return, often cited for equity-heavy portfolios — not a withdrawal rate. It's distinct from the 4% withdrawal rule. Actual portfolio returns vary based on asset allocation, market conditions, and time horizon.

What is the 70-20-10 rule in investing?

A budgeting framework: 70% of income covers living expenses, 20% goes to savings and investments, and 10% covers discretionary goals or emergency reserves. For serious retirement targets, the savings component should increase progressively — by your 40s, aim for closer to 25–30%.

How much should I save per month for retirement in India?

Start with 15–20% of gross monthly income and increase it by 1–2% each year. Your actual target depends on your corpus goal, current savings, expected returns, and years remaining — a personalised calculation will sharpen this figure considerably.

Is it too late to start retirement planning at 45 or 50?

No — but the approach must be more aggressive. Aim for a 25–30% savings rate, consider extending your working years, and restructure any underperforming portfolio holdings.