Introduction

India levies no inheritance tax. Assets — property, shares, gold, fixed deposits, jewellery — pass to legal heirs without triggering a tax event at the point of transfer. For families expecting to inherit significant wealth, this is good news.

But "no inheritance tax" doesn't mean "no tax obligations." Many heirs discover this the hard way when rental income hits their bank account or they decide to sell an inherited property. The tax implications that follow can be substantial — and entirely avoidable with the right preparation.

Two factors make this an especially timely read: the active parliamentary debate around reintroducing inheritance tax — spurred by the April 2024 controversy over Sam Pitroda's remarks — and the growing complexity facing NRI families who inherit Indian assets while living abroad.

This guide covers what heirs actually owe, how capital gains on inherited assets are calculated, what NRIs need to know, and how to build an estate plan that holds up — whatever future policy changes may bring.

Key Takeaways

- India abolished inheritance tax (Estate Duty) in 1985 — receiving an inheritance is currently tax-free

- Income generated by inherited assets (rent, dividends, interest) is fully taxable in the heir's hands

- Capital gains tax applies when inherited assets are sold; the deceased's holding period counts toward the total

- NRIs can inherit Indian property under FEMA with no inheritance tax, but rental income and sale proceeds remain taxable in India

- With inheritance tax returning to India's policy debate, structuring your estate now — through wills, trusts, and tax-efficient transfers — is no longer optional for HNIs and family offices

Is There an Inheritance Tax in India?

No. India has no inheritance tax, estate duty, or death tax currently in force. Whether you inherit real estate, bank balances, equity portfolios, gold, or jewellery, no tax is triggered at the point of transfer.

The legal basis is clear. Section 56(2)(x) of the Income Tax Act, 1961 specifically excludes assets received under a will or by way of inheritance from gift-tax provisions — meaning the inheritance doesn't qualify as deemed income in the heir's hands. Property transferred through a valid will or by succession also attracts no stamp duty.

The Estate Duty Act: 1953 to 1985

India did levy an inheritance tax for over three decades under the Estate Duty Act of 1953. At its peak, rates reached 85% for large estates — an extremely steep levy that made it deeply unpopular with business-owning families.

The government abolished it effective 16 March 1985. The 1985-86 Budget Speech cited four core failures:

- Generated only ~₹20 crore in revenue — roughly 0.095% of total gross tax receipts

- Failed to meaningfully reduce wealth inequality

- Did not help states fund development schemes

- Carried disproportionately high administrative costs

The numbers made the case plainly: estate duty was one of the least productive taxes in the system.

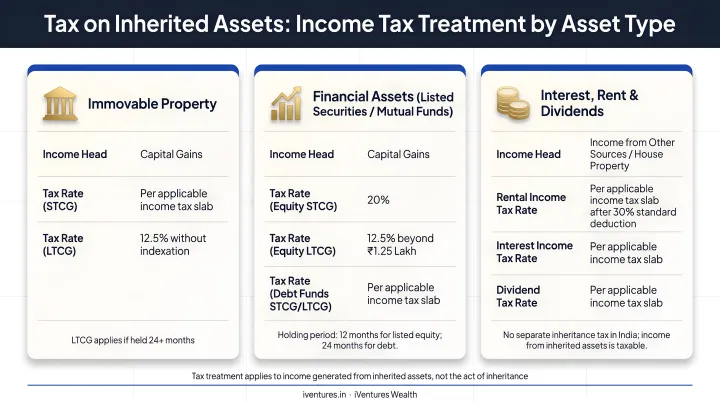

How Inherited Assets Are Taxed in India

Receiving an inheritance is tax-free. Owning the inherited asset is not.

The moment an heir takes possession, they assume full tax responsibility for any income that asset generates. This distinction catches many families off guard — particularly when inheriting income-producing assets like commercial property or an equity portfolio paying dividends.

Income Tax on What the Asset Earns

| Asset Type | Tax Head | Rate |

|---|---|---|

| Rental income from inherited property | Income from House Property | Applicable slab rate |

| Dividends from inherited shares | Income from Other Sources | Applicable slab rate |

| Interest from inherited fixed deposits | Income from Other Sources | Applicable slab rate |

A practical example: if a commercial property generating ₹60,000/month in rent passes to an heir, that ₹7.2 lakh annual rental income must be declared in the heir's ITR under "Income from House Property" (after applicable deductions) and taxed at the heir's income tax slab rate. The inheritance itself is not the taxable event — the ongoing income it generates is.

Section 159 obligation: Under Section 159 of the Income Tax Act, legal representatives can be held liable for unpaid income tax dues of the deceased. Before fully assuming an inherited asset, verify and settle any outstanding tax obligations of the original owner.

How Assets Are Legally Transferred

The method of transfer also determines the heir's legal standing — and their corresponding tax responsibilities from day one. Assets pass to heirs through three primary routes:

- Valid Will — assets go directly to named beneficiaries; the clearest path for named beneficiaries

- Nomination — the nominee becomes the lawful owner of financial instruments

- Joint ownership/survivorship — surviving owner gains full control automatically

Where no will exists, personal law governs distribution: the Hindu Succession Act for Hindus, Muslim Personal Law for Muslims, and the Indian Succession Act for Christians and Parsis.

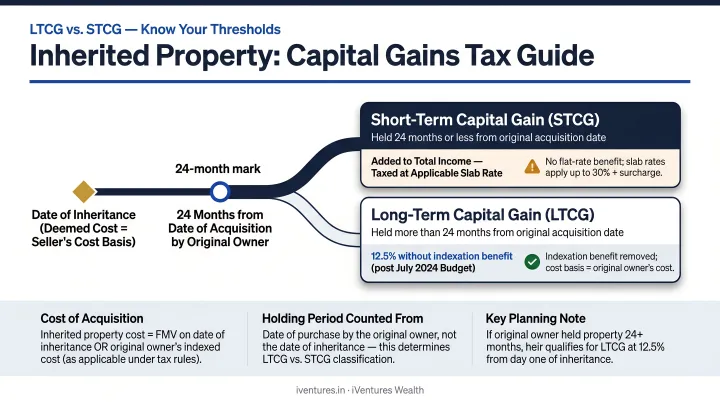

Capital Gains Tax When You Sell Inherited Property

This is where the most significant tax liability typically arises. Capital gains tax applies to the profit from selling inherited assets, and the calculation includes one detail heirs consistently overlook: the deceased's holding period counts toward your own.

The Income Tax Department explicitly includes the period the asset was held by the previous owner when calculating total holding period. The cost of acquisition is the original purchase price paid by the deceased — or fair market value as of 1 April 2001 for assets acquired before that date.

Immovable Property: LTCG vs. STCG

For land and buildings, a combined holding period exceeding 24 months qualifies the asset as long-term.

Post the Budget 2024 amendments (effective 23 July 2024):

- LTCG rate: 12.5% without indexation (replacing the earlier 20% with indexation framework)

- Resident individuals and HUFs who held property before 23 July 2024 have a transitional option: compare tax at 12.5% without indexation versus 20% with indexation, and pay whichever is lower

Numerical example: Father purchases a property in 2008 for ₹40 lakh. He passes away in 2018. The heir sells in 2024 for ₹1.2 crore. The combined holding period is 16 years — clearly long-term. The cost of acquisition is ₹40 lakh (the father's original purchase price). Capital gains = ₹80 lakh, taxed at 12.5% or 20% with indexation, whichever is lower under the transitional provision.

Section 54 relief allows heirs to reduce or eliminate capital gains tax by reinvesting sale proceeds in another residential property. The conditions:

- Purchased within 1 year before or 2 years after the sale date

- Constructed within 3 years after the sale date

- Deduction capped at ₹10 crore (Finance Act 2023 onward)

Shares, Mutual Funds, and Other Securities

For listed equity shares and equity mutual funds, the holding period threshold for long-term classification is 12 months (combined with the deceased's period). Under Section 112A:

- LTCG exemption threshold: ₹1.25 lakh per financial year (increased from ₹1 lakh from 23 July 2024)

- LTCG tax rate: 12.5% (increased from 10% from 23 July 2024)

For unlisted shares and physical gold, the long-term threshold is 24 months, with LTCG taxed at 12.5%.

It's worth noting that not every step in the inheritance process triggers a tax event. Transferring bank accounts, continuing or closing fixed deposits, or dematerialising inherited shares into a demat account carry no tax consequences. Tax applies only when the heir liquidates the asset or earns income from it.

NRI Inheritance Rules: What You Need to Know

NRIs, PIOs, and OCIs can legally inherit any immovable property in India (including agricultural land, plantation property, and farmhouses) from a resident Indian under FEMA regulations. No inheritance tax applies.

However, Indian tax obligations don't disappear simply because the heir lives abroad:

- Rental income from inherited Indian property remains taxable in India

- Capital gains from selling inherited property are taxable in India at standard rates

- TDS will be deducted at source on sale proceeds — NRIs must file ITR to claim refunds or settle tax dues

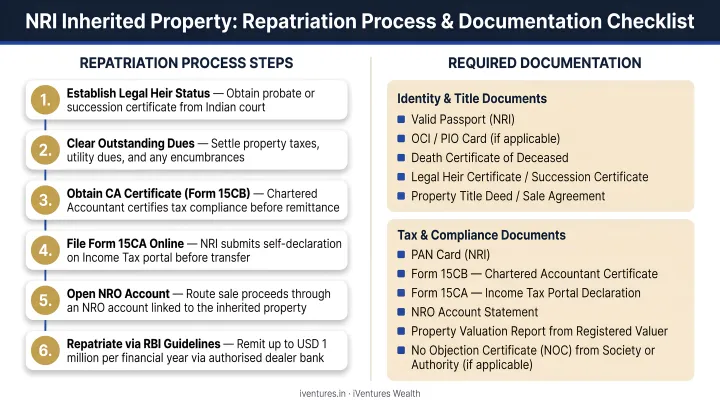

Repatriation Rules

NRIs selling inherited property must first deposit sale proceeds into an NRO account. Repatriation to an overseas account is permitted up to USD 1 million per financial year net of applicable taxes. Prior RBI approval is required for amounts exceeding this threshold.

Documentation required typically includes:

- Form 15CA and Form 15CB (certified by a CA)

- Proof of inheritance (will or succession certificate)

- Sale deed and proof of TDS payment or tax clearance

- NRO account details

DTAA Considerations

India has Double Taxation Avoidance Agreements with the US, UK, UAE, Canada, Australia, Singapore, and 85+ other countries. These treaties can provide relief from being taxed twice on the same income — but they don't eliminate India's taxing rights over Indian-source rental income or gains from Indian immovable property.

NRIs should check applicable DTAA provisions in their country of residence before remitting funds. For UAE residents, for example, Article 6 of the India-UAE DTAA specifically preserves India's right to tax income from Indian immovable property.

Given how quickly DTAA rules, repatriation limits, and foreign probate requirements interact, NRI families often benefit from coordinated advice spanning both Indian and overseas jurisdictions. iVentures Wealth's NRI advisory team works with clients across the US, UK, UAE, Singapore, Canada, and Australia — covering Form 15CA/15CB compliance, FEMA filings, and alignment between Indian succession laws and foreign estate requirements.

The Inheritance Tax Debate: Could It Return?

The April 2024 controversy around inheritance tax remarks — followed by Finance Minister Nirmala Sitharaman's public response that such a tax "directly hits the middle class" — brought the debate into mainstream political discourse. It hasn't gone away.

The Case for Reintroduction

The argument rests largely on wealth concentration data. According to the World Inequality Database (March 2024), India's top 1% owned 40.1% of national wealth in 2022-23. Proponents point to international precedents — Japan levies inheritance tax at up to 55%, France at 45%, and 24 OECD countries maintain some form of wealth transfer tax.

The Case Against

The opposition is equally substantive:

- Assets being transferred have already been taxed as income during the owner's lifetime — a genuine double-taxation concern

- Family-run businesses (the backbone of India's economy) face forced asset liquidation or business fragmentation

- Risk of capital flight as promoters restructure business ownership or change tax residency

- The administrative cost problem that killed the original Estate Duty has not been solved

The debate remains unresolved — and that uncertainty itself is the signal. Whether or not inheritance tax returns, waiting for legislative clarity before structuring your estate is a costly mistake. Private trusts, HUF arrangements, and strategic lifetime gifting can each reduce future tax exposure legally, and the most effective structures take years to set up properly.

Building a Tax-Smart Estate Plan for Your Family

The absence of inheritance tax today doesn't make estate planning optional — it makes the current window valuable. Families who structure wealth transfer proactively benefit whether or not policy changes in the future.

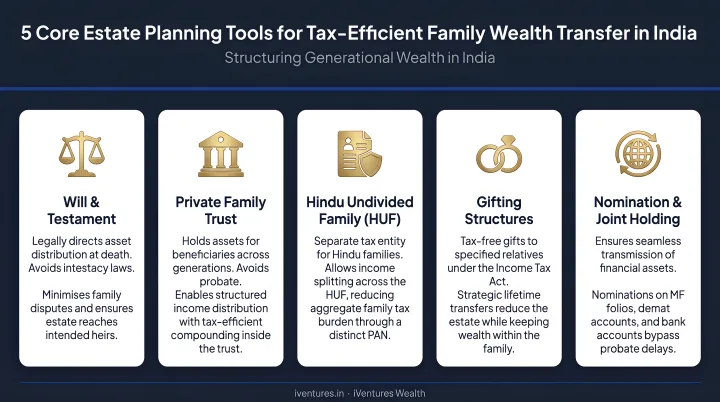

Core estate planning tools:

- Valid Will — the foundation; clearly documents asset distribution intent and avoids disputes

- Nominations — ensure all financial instruments (bank accounts, mutual funds, insurance, demat) have current, accurate nominees

- Private Trusts — particularly effective for business-owning families, special-needs dependents, or NRI children who won't actively manage Indian assets

- HUF structures — can provide tax-efficient pooling of family income and assets where applicable

- Strategic lifetime gifting — transfers within tax-free limits reduce the estate systematically over time

Tax-efficient wealth transfer requires looking across all asset classes simultaneously. Real estate, equity portfolios, business stakes, gold, and international assets each have distinct succession and tax rules — a plan that addresses one without the others leaves gaps.

Closing those gaps is where professional advisory adds the most value. iVentures Wealth's estate planning service — covering ₹1,146+ Cr in assets across 150+ affluent families — works alongside legal professionals including Supreme Court-level practitioners and estate planning specialists.

The firm's Wealth Monitor App gives families a consolidated dashboard across all asset classes, entities (individual, family, HUF), and international holdings, so successors see the complete picture rather than a fragmented one.

In one documented case, a promoter who received ₹100+ crore from a liquidity event used a family trust structured by iVentures to ring-fence the corpus and formalize distribution rules — turning a one-time liquidity event into a structured, generational wealth plan.

Review your estate documents after every significant life event: marriage, birth of a child, acquisition of major assets, a change in NRI status, or a significant market appreciation in your portfolio. Circumstances change — your estate plan should keep pace.

Frequently Asked Questions

How much inheritance is tax-free in India?

Currently, all inherited assets are tax-free in India at the point of transfer — there is no inheritance tax or estate duty. Heirs only become liable for income tax on income generated by inherited assets, or capital gains tax when they choose to sell.

What is the new inheritance law in India?

There is no new inheritance tax law in India as of 2025 — the topic has been debated, but no legislation has been enacted. Asset succession remains governed by personal laws (Hindu Succession Act, Indian Succession Act, Muslim Personal Law) and FEMA for NRIs.

Can NRIs inherit property in India without paying tax?

Yes. NRIs can inherit Indian property with no inheritance tax under FEMA. Rental income or capital gains from selling the property will be taxable in India, and NRIs should verify applicable DTAA provisions in their country of residence to avoid double taxation.

What taxes apply when you sell inherited property in India?

Capital gains tax applies on the sale profit. The combined holding period of the original owner and heir determines LTCG or STCG classification, with the deceased's original purchase price used as acquisition cost. LTCG on immovable property is taxed at 12.5% without indexation (effective 23 July 2024).

Is rental income from inherited property taxable?

Yes. Rental income from an inherited property is fully taxable in the heir's hands under "Income from House Property" and must be declared in their annual ITR. Standard deductions apply, but there is no inheritance-based exemption from this income tax obligation.

What is the difference between inheritance tax and estate duty in India?

Both terms describe the same concept: a tax levied on assets transferred upon death. India's Estate Duty Act (1953) was the formal legal framework for what is commonly called inheritance tax. It was abolished in 1985, and neither form applies in India today.