Introduction

India is in the middle of one of the largest intergenerational wealth transfers in history. According to EY's Indian Family Office Playbook, an estimated US$1.5 trillion will change hands across generations over the next two decades — yet the planning infrastructure to support this transfer remains critically underdeveloped.

Most affluent families spend decades building wealth. Very few spend equivalent energy protecting it.

The gap often comes down to a persistent misconception: that a nominee registration or a basic will is "enough." In practice, nominations don't transfer legal ownership, probate can tie up estates for years, and family disputes over unclear succession can unravel even carefully accumulated wealth in a single generation.

This guide covers what legacy planning actually means in the Indian context — the legal frameworks, the key components, the common mistakes, and how to get started with a durable plan.

Key Takeaways

- Legacy planning covers far more than a will — it's a structured approach to transferring assets, values, and intentions across generations.

- In India, nominee misconceptions, probate delays, and succession law complexity make structured planning especially critical.

- A complete plan spans wills, family trusts, aligned nominations, tax-efficient transfers, and a business succession framework.

- Only about 5% of Indians have a will; among HNIs, 36% have no succession arrangement at all.

- The earlier you start, the more planning options are available to you.

What Is Legacy Planning?

Legacy planning is a coordinated financial, legal, and personal strategy for transferring your assets, values, and intentions to chosen beneficiaries. It covers not just what you own, but how and when it passes on — and what principles guide that transfer.

How It Differs from Estate Planning

These terms get used interchangeably, but the distinction matters.

Estate planning is the legal backbone: wills, trusts, beneficiary designations, and powers of attorney. Legacy planning encompasses all of that and adds a broader dimension:

- Articulating your values and intentions for future generations

- Preparing heirs emotionally and financially

- Incorporating philanthropic goals

- Ensuring business continuity

- Structuring governance for family harmony

In other words, estate planning is one component within a larger legacy plan — not a substitute for it.

The India-Specific Legal Framework

In India, legacy planning intersects with multiple legal frameworks depending on religion and asset type:

| Applicable Law | Who It Covers |

|---|---|

| Hindu Succession Act, 1956 | Hindus, Buddhists, Jains, Sikhs |

| Indian Succession Act, 1925 | Christians, Parsis; testamentary succession for all |

| Indian Trusts Act, 1882 | All communities (private/public trusts) |

| Muslim Personal Law (Shariat) Act, 1937 | Muslims |

One important distinction for Indian families: India currently has no estate or inheritance tax. Estate duty was abolished in 1985. However, capital gains tax on inherited asset sales, gift tax under Section 56(2) of the Income Tax Act, and stamp duty on gift deeds can still create meaningful wealth leakage without proper planning.

Why Legacy Planning Matters for Affluent Families in India

The Nominee Misconception

This is one of the most costly misunderstandings in Indian personal finance. Many families believe that registering a nominee for bank accounts, mutual funds, demat accounts, or insurance policies is equivalent to estate planning.

It is not.

In Shakti Yezdani v. Mahalakshmi (December 14, 2023), the Supreme Court definitively confirmed that a nominee is a trustee or custodian — not the legal owner. Ownership follows succession law (will or personal law), not nomination. Without a coordinated will, disputes between nominees and legal heirs can move into courts and take years to resolve.

iVentures Wealth consistently encounters this gap among new clients: families where every account has a different nominee, none of which form a coherent inheritance plan.

The Business Succession Gap

India's family businesses contribute approximately 79% of the country's GDP — yet 80% fail at succession planning, and only 21% have documented succession plans. The Murugappa Group's valuation disputes, still unresolved after years of planning attempts, illustrate what happens even when families try to plan without adequate governance frameworks.

For founders and promoters, personal wealth and business value are often deeply intertwined. Without a clear succession structure, businesses face forced sales, operational collapse, or prolonged disputes during ownership transitions.

Wealth Erosion Without a Plan

Dying without a valid will (intestate) triggers distribution under applicable succession law — which may not reflect your actual intentions. The financial consequences compound quickly:

- Probate proceedings for contested wills can run several years

- Capital gains tax applies when heirs sell inherited assets (at the original acquisition cost under Section 49 of the Income Tax Act, not the inherited value)

- Gift deeds attract stamp duty ranging from 0.5% to 6% depending on the state

- Forced asset liquidation to resolve disputes destroys long-term value

Proactive structures — family trusts, strategic gifting, HUF arrangements — can significantly reduce this erosion.

Key Components of a Strong Legacy Plan

Will and Testament

A legally valid will is the foundation. In India, requirements include the testator's signature and two witnesses. Registration is not mandatory but is strongly recommended — it reduces contestability and simplifies proof of authenticity.

Beyond a simple will, a testamentary trust within the will can dictate conditions for when and how specific beneficiaries receive assets — useful when heirs include minors, dependants with special needs, or individuals who may not be ready to manage large inheritances.

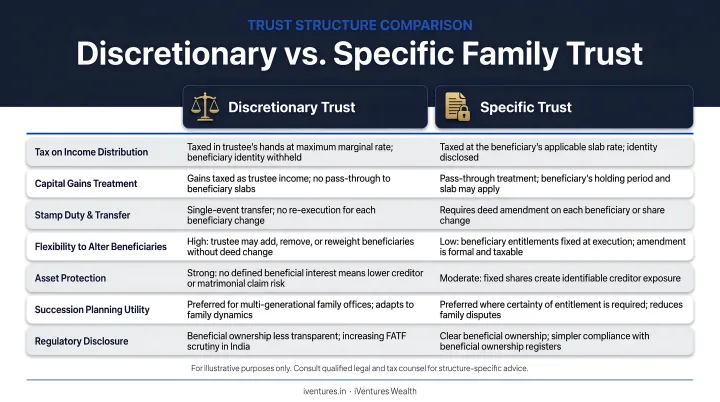

Private Family Trusts

A private family trust under the Indian Trusts Act, 1882 offers several advantages over a plain will:

- Transfers assets without court involvement, bypassing probate entirely

- Keeps distribution details private — unlike wills, trusts are not public documents

- Shields assets from creditors through legally structured arrangements

- Releases assets to beneficiaries over time or tied to specific conditions

Two primary structures exist. A discretionary trust gives the trustee flexibility to determine distribution amounts and timing. A specific trust defines exact beneficiary shares upfront.

The tax implication matters here: discretionary trusts are taxed at the Maximum Marginal Rate (MMR) under Section 164 of the Income Tax Act, while specific trusts are taxed at individual beneficiary rates under Section 161. This trade-off — flexibility versus tax efficiency — is a core planning decision.

iVentures Wealth has implemented private trust structures across several scenarios: securing lifelong support for a special-needs child, protecting Indian business assets for NRI children, and consolidating a ₹100+ crore post-exit corpus into a structured family capital plan.

HUF (Hindu Undivided Family)

The HUF is a uniquely Indian planning structure with its own legal and tax identity. Key features:

- Separate PAN and independent tax filing

- Deductions available under Sections 80C and 80D

- Distributions to members are tax-free under Section 10(2)

- Can hold property, investments, and business interests as a family unit

The 2005 Hindu Succession Amendment granted daughters equal coparcenary rights, significantly expanding the pool of HUF stakeholders. Any HUF structuring today requires updated legal advice that accounts for this broader coparcenary base.

Beneficiary Designations and Nominations

Nominations must be treated as administrative designations — not inheritance decisions. Key practices:

- Align all nominations (mutual funds, EPF, insurance, demat) with the overall legacy plan

- Update nominations after every major life event: marriage, divorce, birth of a child, death of a named nominee

- Ensure your will and nominations are coordinated — inconsistency between them is a leading source of disputes

iVentures Wealth creates consolidated asset listings for clients specifically to ensure no account is overlooked during this alignment process.

Tax-Efficient Wealth Transfer Strategies

Getting nominations right is the defensive half of legacy planning. The other half is proactive — using tax-efficient structures to transfer wealth on your terms. Key tools available to Indian families:

- Gifts to specified relatives (spouse, siblings, parents, certain in-laws) are fully exempt from tax under Section 56(2), with no upper limit — making intra-family gifting a powerful early-transfer tool

- Family trusts provide structured, probate-free transfer with controlled distribution

- Transferring appreciating assets early reduces the future capital gains base for heirs

- Strategic use of HUF for income-splitting and separate tax entity benefits

Coordinating these strategies across SEBI, FEMA, and income tax requirements requires a fiduciary advisor — one with no product-commission incentive to recommend structures that benefit the advisor rather than the family.

Life Insurance in Legacy Planning

Life insurance plays a specific, practical role in legacy plans — separate from its investment function:

- Provides immediate liquidity to heirs without waiting for asset transfers or probate

- Equalises inheritance when one heir receives the business and another receives financial assets

- Funds obligations at transfer — stamp duty, legal costs, or outstanding liabilities — without forcing asset sales

How to Build Your Legacy Plan: A Step-by-Step Approach

Step 1 — Inventory Your Assets and Liabilities

Start with a complete financial picture. Document:

- All assets: real estate, listed investments, business interests, EPF/PPF, insurance policies, jewellery, digital assets, foreign holdings

- All liabilities: loans, guarantees, contingent obligations

- How each asset is titled, who holds each account, and current nomination details

This inventory is the foundation on which every subsequent planning decision is made. iVentures' Wealth Monitor App lets clients and family members consolidate holdings across mutual funds, equities, bonds, fixed deposits, PMS, AIFs, and HUF portfolios in a single view — making this step considerably easier.

Step 2 — Define Your Goals and Intentions

Before drafting documents, get clear on what you want your legacy to accomplish:

- Who benefits, when, and under what conditions?

- Are there charitable intentions?

- Should the business be transferred or sold?

- Are there dependants with special needs?

- Is there concern about a young heir managing a large inheritance too early?

Documenting these intentions — including a "letter of wishes" or ethical will — gives executors and trustees clear direction, and shapes the legal structures that follow.

Step 3 — Assemble Your Team and Create the Documents

Legacy planning in India requires coordination between three professionals:

- Wealth advisor — financial planning, tax strategy, investment structuring

- Estate planning attorney — will drafting, trust creation, legal compliance

- Chartered accountant — tax reporting, compliance, annual filings

When each professional works in isolation, gaps appear — often in the exact areas that matter most during succession. iVentures Wealth coordinates this process end-to-end, with wills prepared and vetted by senior legal practitioners and experienced counsel.

Step 4 — Communicate the Plan and Review Regularly

A plan kept entirely to yourself leaves the same questions unanswered as having no plan.

- Share key elements with heirs: where documents are stored, who the trustees are, the broad intention behind asset allocation

- Review the plan every 3–5 years, or after any major life event: marriage, divorce, new business, significant acquisition, death of a named beneficiary, or material regulatory change

Common Mistakes to Avoid in Legacy Planning

Most estate plans fail not because of bad intentions, but because of predictable, avoidable gaps. Here are four that appear most frequently:

Nominations are not a will. Each account can carry a different nominee — none of whom receive legally binding ownership. A patchwork of nominations without a coordinating will is not a legacy plan; it is a liability.

Planning for death, not incapacity. A legacy plan must cover scenarios where you are alive but unable to act. A Power of Attorney (PoA) allows a trusted person to manage accounts and legal matters on your behalf. A durable PoA remains valid even if the principal is incapacitated — particularly critical for NRIs and OCIs managing assets across jurisdictions. Without these instruments, family members may be legally unable to access accounts or make medical decisions.

Failing to update after major life changes. A will drafted 15 years ago may not reflect your current asset base, family composition, or intentions. Marriages, divorces, births, deaths of named beneficiaries, new business ventures, and changes in tax law all warrant a formal review. The Repealing and Amending Act, 2025 — which abolished mandatory probate in Mumbai, Kolkata, and Chennai effective December 2025 — is one such regulatory shift that affects existing estate plans.

Leaving assets scattered with no unified view. The cumulative effect of these gaps becomes most visible when wealth actually transitions. iVentures Wealth has worked with families managing assets across nine separate broker and bank relationships, with no consolidated picture of what they owned. Bringing that wealth onto a single family balance sheet, formalising a family charter, and aligning nominations across accounts removed the friction that would otherwise have caused serious disputes at the next transition.

Frequently Asked Questions

How does a legacy plan work?

A legacy plan is built through a coordinated set of legal and financial documents — will, trusts, beneficiary designations, and PoA — that dictate how assets are managed and distributed after death or incapacity. In practice, it requires a wealth advisor, estate attorney, and chartered accountant working together on a unified strategy.

What are the key components of a legacy plan?

The core pillars are a legally valid will, private family trusts for probate-free transfer, coordinated beneficiary nominations, tax-efficient gifting strategies, life insurance for liquidity, and a business succession plan where applicable.

What is the difference between legacy planning and succession planning?

Legacy planning covers the full spectrum — assets, values, and family intent across generations. Succession planning specifically addresses the transition of a business or leadership role. In most cases, succession planning sits within — or runs alongside — the broader legacy framework.

Why is legacy planning important?

Without a plan, assets are distributed by law rather than intent, probate can freeze estates for years, and families face disputes that destroy both wealth and relationships. Legacy planning addresses all of these proactively — before a crisis forces the issue.

What are common mistakes to avoid when making a bequest?

The most frequent errors: confusing nominations for legal inheritance, not updating a will after major life changes, failing to coordinate beneficiary designations across all accounts, and not accounting for incapacity scenarios through a PoA or living will.

What is legacy plan insurance?

"Legacy plan insurance" refers to life insurance used within a legacy framework. It typically provides immediate liquidity to heirs, equalises inheritance among children receiving different asset types, or covers tax obligations and debts at the time of estate transfer — without forcing asset sales.