Introduction

Many Indian investors face two opposite but equally damaging tendencies: staying heavily equity-oriented well into their 50s without a plan to preserve what they've built, or abandoning growth entirely at retirement by moving everything into fixed deposits. Both erode long-term wealth.

The data reflects these tendencies clearly. According to NCAER research, Indian households hold 77% of total assets in real estate and only 5% in financial assets — a concentration that creates real liquidity risk and succession complexity, particularly for HNI families.

Risk appetite also changes with age, but rarely with intention. The SEBI Investor Survey 2025 found that 85% of Silver Gen households prioritise capital safety, while 79% of Gen Z are relatively more open to risk — yet most portfolios don't reflect these shifts until it's too late.

Getting allocation right — by life stage, not just instinct — is one of the highest-impact decisions an investor can make. This guide walks through how to do that, from your 20s through your 60s.

Key Takeaways

- Asset allocation means dividing your portfolio across equities, debt, gold, real estate, and cash based on your goals, risk tolerance, and time horizon.

- Younger investors can absorb more equity volatility; as you age, the focus should gradually shift toward capital preservation.

- Frameworks like "100 minus age" or the 60/40 split are useful starting points — not rules carved in stone.

- Rebalance at least once a year — or after major life events — to prevent unintended risk from creeping into your portfolio.

- Indian investors must account for PPF, NPS, ELSS, Sovereign Gold Bonds, and REITs, not just mutual funds.

What Is Asset Allocation and What Shapes It?

Asset allocation is the deliberate decision about how much of your investable wealth to place into different asset categories — equities, fixed income, gold, real estate, and cash equivalents. The goal is to balance growth potential against risk exposure at every stage of life.

Three core factors determine the right allocation for any individual:

- Time horizon — How many years before you need the money

- Risk tolerance — Your emotional and financial capacity to absorb losses

- Liquidity needs — How much wealth must remain accessible at short notice

All three shift meaningfully with age, which is why allocation cannot be set once and forgotten.

Asset Allocation vs. Diversification

Understanding this distinction matters before adjusting anything by age. These two concepts work together but serve different purposes:

- Asset allocation determines what proportion of your portfolio goes into each broad asset class (for example, 60% equities, 30% debt, 10% gold)

- Diversification spreads investments within each class (across sectors, fund managers, geographies, or instruments)

Both reduce portfolio-level risk, but allocation sets the strategic foundation.

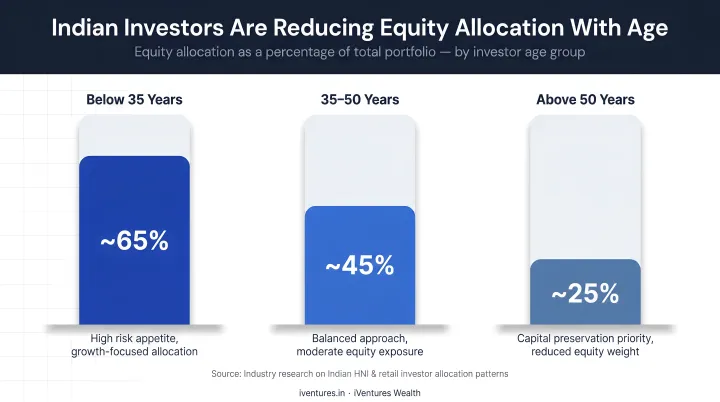

Real-world AMFI-Crisil data confirms that Indian investors naturally age their portfolios: equity allocation runs at 75.5% for investors aged 25–44, falls to 66.3% for ages 45–58, and drops further to 53.6% for investors above 58. The shift happens — but without intentional planning, it tends to lag behind where it should be at each life stage.

Asset Allocation by Age: A Decade-by-Decade Guide

While exact percentages vary by individual circumstance, well-established principles apply to each life stage. For Indian investors, these stages also align with major financial milestones — career launches, marriage, children's education, and retirement — each of which reshapes the financial picture.

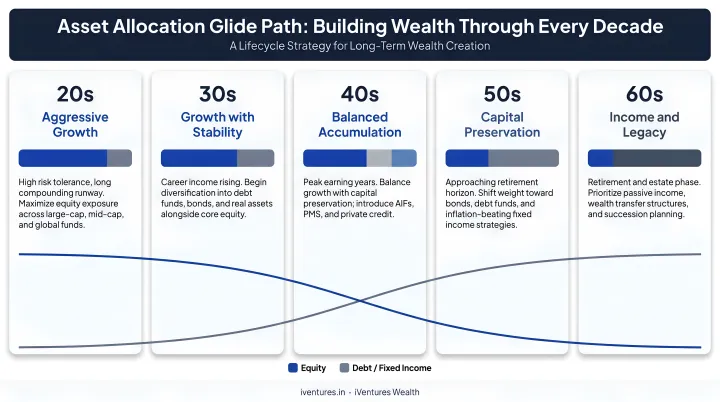

In Your 20s: Build the Foundation

At this stage, time is your most valuable asset. With 30+ years of compounding ahead, maximising equity exposure makes mathematical sense.

Typical allocation: 70–80% equities, with the remainder in an emergency fund, PPF, or NPS contributions

- What to invest in: Diversified equity mutual funds, ELSS (for Section 80C tax savings), index funds, direct stocks for those with appetite

- Start SIPs immediately — SIP AUM for investors aged 18–34 grew 2.6x to ₹1.51 lakh crore between March 2019 and March 2024

- The most common mistake is waiting for the "right time" to invest — even small monthly contributions in this decade create a disproportionate wealth base through compounding

Open an NPS account early. The habit of long-horizon, tax-advantaged saving compounds beyond just the returns.

In Your 30s: Balance Growth With New Responsibilities

Income typically rises in the 30s, but so do obligations — home loans, family expenses, children's education planning. TransUnion CIBIL data shows that consumers aged 26–35 account for 39% of credit inquiry volumes, confirming that leverage rises sharply through this decade.

Typical allocation: 60–70% equities, with a meaningful debt component introduced

- Start a dedicated child education fund via long-horizon equity SIPs

- Review life and term insurance coverage — an under-insured investor carries hidden financial risk that can disrupt any investment plan

- Don't let EMI pressure crowd out SIPs — maintain investment discipline even as loan repayments begin

That discipline around SIPs also makes this the right decade to audit what you already own. Many clients iVentures Wealth encounters at this stage have accumulated mutual funds, ULIPs, and FDs across multiple platforms with no unified view of their portfolio — consolidating early prevents compounding complexity later.

In Your 40s–50s: Shift From Growth to Stability

Retirement moves from abstract to tangible during this period. The priority shifts from maximising returns to protecting the corpus you've built.

Typical allocation: 50–60% equities, progressively increasing debt, balanced advantage funds, and withdrawal-friendly instruments

Key actions for this decade:

- Maximise NPS contributions — the additional ₹50,000 deduction under Section 80CCD(1B) is particularly valuable for those in the 30% tax bracket

- Review real estate concentration — clients with significant illiquid property holdings need a plan to diversify into financial assets before retirement

- Add balanced advantage or hybrid funds to smooth the transition from pure equity to a more defensive posture

PFRDA's own Balanced Life Cycle option holds 50% equity up to age 45, then tapers to 35% equity from age 55 — a useful regulatory benchmark for how India's pension regulator thinks about age-linked glide paths.

In Your 60s and Beyond: Preserve, Distribute, and Stay Ahead of Inflation

The most common mistake here is moving entirely into FDs and cash. The comfort is real; the protection is not.

India's SRS Abridged Life Tables show average remaining life expectancy at age 60 is 18.3 years (17.5 for males, 19.2 for females). A portfolio that abandons growth entirely at 60 must fund nearly two decades of expenses in an environment where CPI inflation averaged 4.6% between 2014 and 2024, per RBI data.

Typical allocation: 30–40% equity retained for purchasing power, remainder in debt, SGBs, and pension income

Priorities at this stage:

- Develop a systematic withdrawal strategy — drawing from different accounts in a tax-efficient sequence

- Introduce estate planning — updated nominations, wills, and trust structures for generational wealth transfer

- Consider SWPs (Systematic Withdrawal Plans) from mutual funds calibrated to LTCG-efficient withdrawal lots

A retirement portfolio still needs growth exposure. Without it, inflation quietly outpaces fixed income, and a 20-year runway becomes far more expensive than it looked at 60.

Popular Asset Allocation Frameworks to Know

The "100 Minus Age" Rule

Subtract your age from 100 to get your approximate equity allocation. A 35-year-old would hold 65% in equities.

Many advisors now adjust this to 110 or 120 minus age to account for longer life expectancy and India's inflation environment, where a retirement corpus must sustain purchasing power for 25–30 years. Think of it as a starting point, not a final answer. Goals, dependents, income stability, and risk tolerance all shift the number.

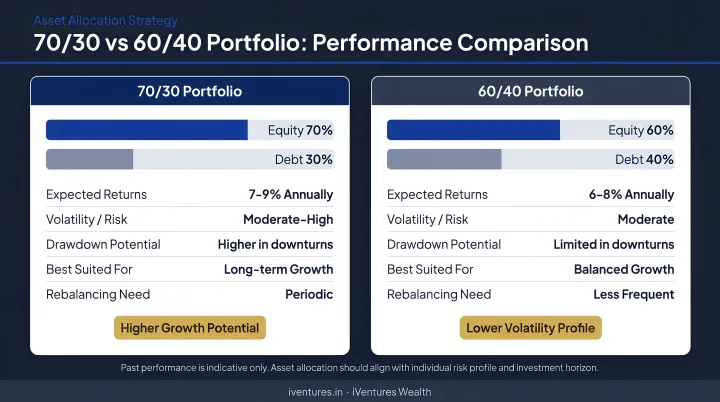

The 60/40 Portfolio

The classic split of 60% equities and 40% debt has long been considered the standard moderate portfolio. The logic: the debt component cushions equity downturns, reducing drawdowns without abandoning growth entirely.

Its weakness emerges in high-inflation or rising-rate environments, where debt returns erode in real terms. To counter this, advisors increasingly layer in gold and international equities — broadening diversification beyond the traditional two-asset split.

The 70/30 Portfolio

For investors with higher risk tolerance or a longer runway, a 70/30 split captures more upside while keeping a meaningful buffer in place.

| Scenario | 70/30 | 60/40 |

|---|---|---|

| Strong bull market | Outperforms | Underperforms slightly |

| Flat or bearish market | More drawdown | Better downside protection |

| Best suited for | Longer horizons, higher risk appetite | Moderate risk, closer to goals |

The right choice depends on your time horizon and liquidity needs, not on where the market is today.

The 15×15×30 Rule

Popular among Indian mutual fund investors: investing ₹15,000 per month via SIP in equity funds targeting a 15% annual return for 30 years illustrates the power of long-term compounding. Mathematically, this produces an approximate corpus of ₹10.4 crore, assuming a 15% annualised return compounded monthly.

This is an illustrative concept, not a guarantee. The NSE's historical data shows Nifty 50 TR delivered a 14.2% CAGR from 1999 to 2021 — useful context for the 15% assumption, but actual future returns will vary. The deeper lesson is that discipline and time in the market matter far more than timing the market.

Asset Classes Indian Investors Should Consider at Every Life Stage

Beyond the standard equity/debt binary, Indian investors have access to a richer toolkit:

| Asset Class | Best Used For | Key Consideration |

|---|---|---|

| Equity mutual funds / direct stocks | Growth, wealth accumulation | Core holding across all age groups |

| ELSS | Tax saving (Section 80C) + equity growth | 3-year lock-in; ideal in 20s–40s |

| PPF | Long-horizon debt, tax-free returns | 15-year lock-in; start early |

| NPS | Retirement savings + tax deduction | Additional ₹50,000 deduction under 80CCD(1B) |

| Sovereign Gold Bonds (SGBs) | Gold exposure + 2.5% annual interest | Capital gains tax-exempt on redemption for individuals |

| REITs | Real estate exposure with liquidity | Five listed REITs distributed over ₹8,900 crore in FY2025-26 |

| Debt mutual funds | Capital preservation, fixed income | Post-2023: taxed at slab rates; affects HNI decision-making |

| Private credit AIFs | Inflation-beating yield (12–16% IRR range) | UHNI/HNI portfolios; longer lock-in |

Tax Efficiency Across Life Stages

- 20s–40s: Use ELSS for 80C, NPS for 80CCD(1B), and equity mutual funds for long-term compounding

- Approaching retirement: Shift toward PPF, SGBs, and tax-free bonds. The 2023 removal of indexation benefits from debt mutual funds makes them less attractive for investors in higher tax brackets — this shift matters more than it used to

- UHNI portfolios: Add alternative investments — private equity, structured products, international equities — to the standard allocation. A SEBI-registered RIA structures these without product bias, aligning each instrument to your specific tax and liquidity position

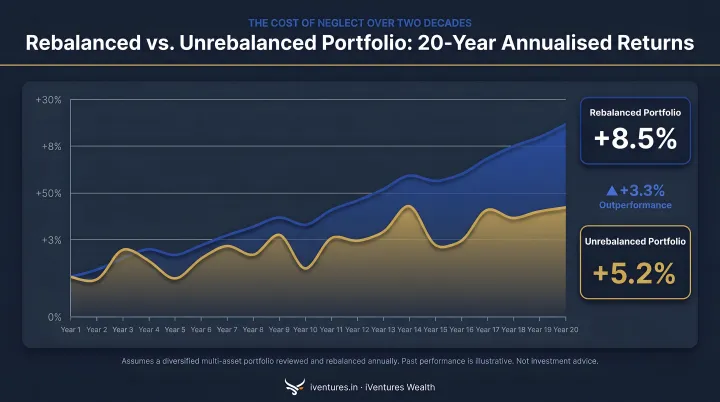

How to Rebalance and Adjust Your Portfolio Over Time

What Rebalancing Means

When market movements push one asset class above or below its target allocation, rebalancing restores the intended mix. Two common approaches:

- Calendar-based — Review and rebalance annually or semi-annually regardless of drift

- Threshold-based — Rebalance whenever an asset class drifts more than 5–10% from its target

A CFA Institute study comparing portfolios over 1992–2012 found that a rebalanced portfolio returned 7.86% annualised versus 7.42% for an unrebalanced portfolio — with lower volatility.

Life Events That Should Trigger a Review

Beyond regular rebalancing, these events warrant an immediate portfolio review:

- Significant income change or job transition

- Marriage or divorce

- Birth of a child

- Inheritance or windfall

- Approaching a major goal (child's education, retirement)

- Major market dislocation

Ad hoc panic selling during downturns is the enemy of good allocation. Market corrections can present opportunities to buy underweight asset classes at lower prices — the opposite of what most investors instinctively do.

Each of these triggers has a cost dimension that's easy to overlook in the moment.

The Tax Dimension of Rebalancing

This is where many Indian investors leave money on the table.

Under current law, equity LTCG above ₹1.25 lakh is taxed at 12.5% for transfers on or after July 23, 2024 (up from the earlier 10% threshold of ₹1 lakh). Debt fund gains are taxed at slab rates for funds acquired post-April 1, 2023.

The smarter approach: Where possible, rebalance through new contributions — adding fresh capital to underweight assets — rather than selling appreciated holdings. This reduces tax drag while still correcting the allocation drift. At iVentures Wealth, rebalancing plans are structured around this principle — phased re-allocation that accounts for tax-loss-harvesting windows and lock-in periods, so clients aren't inadvertently paying avoidable tax to stay on strategy.

Conclusion

Asset allocation by age is not a rigid formula — it is a living strategy. What worked at 28 should look materially different at 45, and different again at 65. The discipline of reviewing, adjusting, and staying invested across market cycles is what separates long-term wealth builders from those who react to headlines.

For investors managing significant wealth across multiple asset classes, life stages, and entities, generic rules of thumb only go so far. The right allocation depends on your tax position, liquidity needs, retirement horizon, and entity structure — not a textbook formula.

iVentures Wealth's SEBI-registered, CFA-led advisory team has helped 150+ affluent families and UHNIs build personalised portfolios aligned to each client's life stage since 2005. If you'd like a structured review of your current allocation, connect with the iVentures team to get a clear picture of where you stand and what needs to change.

Frequently Asked Questions

What asset allocation is best?

There is no single "best" allocation — it depends on your age, risk tolerance, time horizon, and financial goals. Younger investors typically benefit from higher equity exposure, while those nearing retirement should progressively shift toward capital preservation instruments. A personalised risk profiling assessment is the right place to begin.

Is 70/30 better than 60/40?

Neither is universally superior. The 70/30 portfolio offers higher growth potential in bull markets, while 60/40 provides better downside protection. The right choice depends on your runway and risk appetite — 70/30 suits investors with a longer time horizon, while 60/40 better serves those closer to their financial goals.

What is the 15×15×30 rule?

This is a popular Indian mutual fund illustration: investing ₹15,000 per month via SIP at an assumed 15% annual return for 30 years. It is a teaching concept, not a guaranteed outcome — actual returns will vary based on market conditions and fund selection.

What is the 100 minus age rule in investing?

Subtract your age from 100 to get your approximate equity allocation — a 40-year-old would hold roughly 60% in equities. Many advisors now use "110 or 120 minus age" to account for longer life expectancy and the need to outpace inflation across a 25–30 year retirement horizon.

How often should I rebalance my investment portfolio?

At minimum, conduct an annual review or rebalance whenever an asset class drifts more than 5–10% from its target. Major life events — marriage, a new child, a job change, or nearing retirement — should also prompt an immediate review.

Should I change my asset allocation during a market crash?

Avoid panic-driven rebalancing. Market downturns can be an opportunity to buy underweight asset classes at lower prices, not a signal to sell. Selling during a downturn locks in losses and risks missing the recovery. Planned, disciplined rebalancing — not emotional reaction — is the governing principle.