Introduction

Managing significant wealth in India today is complex in ways most advisory models weren't designed for. A founder running an operating business, holding listed and unlisted equity, managing family obligations across generations, navigating NRI tax considerations, and planning for succession — all simultaneously — has a financial life that no standardised portfolio template can address.

Large bank wealth divisions exist to serve thousands of clients. That scale creates structural limitations: relationship managers rotate, product recommendations reflect internal quotas, and advice gets siloed across departments that don't communicate. For affluent families and UHNIs, this isn't a minor inconvenience. It's a structural mismatch.

Boutique private wealth management emerged as a direct response to this gap. Not a premium label or a marketing position — a structurally different advisory model, where the advisor's incentives align with the client's outcomes, continuity is built in, and advice spans the full picture rather than a single product line.

For investors whose financial lives have outgrown the standard template, the question isn't whether a boutique model costs more. It's whether the alternative — fragmented, quota-driven advice — is a cost they can afford.

Key Takeaways

- Boutique private wealth management delivers customised strategy, not standardised portfolio templates

- SEBI-registered investment advisers operate as true fiduciaries — revenue comes from client fees, not product commissions

- Holistic coordination across investments, tax, estate, and liquidity planning prevents the fragmented advice that erodes long-term wealth

- Relationship continuity matters — an adviser who knows your financial history for a decade is far better equipped than one who doesn't

- Deloitte's 2024 Asia Pacific family office report found 37% of wealthy families have no succession plan

What Is Boutique Private Wealth Management?

The CFA Institute defines private wealth management as a discipline combining financial planning and investment management for individual investors — specifically covering tax planning, estate planning, wealth transfer, risk tolerance, assets, liabilities, and Investment Policy Statement design. The word "boutique" adds a structural dimension: a smaller, focused firm serving a deliberately limited number of HNI and UHNI clients with deeply personalised, integrated guidance.

This distinguishes it from two common alternatives:

- Retail advisory — volume-based, standardised, built for breadth across thousands of clients

- Mass-market bank wealth divisions — institutionally structured, product-driven, constrained by proprietary shelves and RM rotation

The boutique model fits clients whose financial lives have grown too interconnected for transactional advice:

- Affluent families managing multi-generational wealth

- Founders navigating liquidity events and concentrated equity

- CEOs and CXOs with complex ESOP structures

- NRIs managing cross-border tax and repatriation

- Family offices requiring coordinated, multi-entity planning

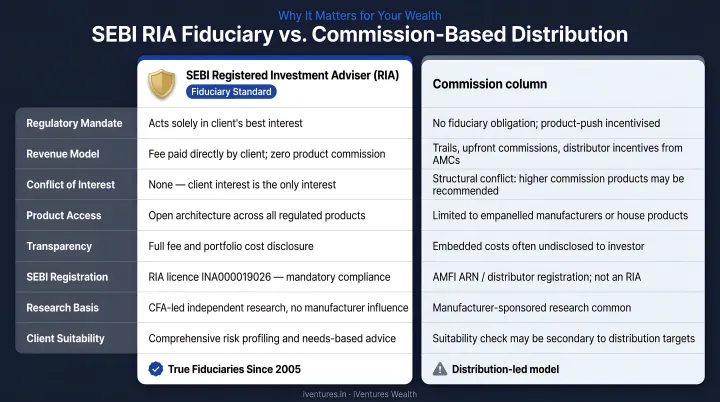

One structural distinction matters before assuming any firm qualifies: "boutique" is not a regulated term in India. Any firm can use it. The real differentiator is whether the firm operates as a SEBI-registered investment adviser (RIA) — a designation that legally requires fiduciary conduct and prohibits commission-based product recommendations. As of August 2024, SEBI reported only 927 registered IAs across India — a rare category relative to the country's growing UHNI population.

Key Advantages of Boutique Private Wealth Management

The advantages below aren't theoretical. They describe what actually changes for clients — in how advice is structured, how decisions get made, and how wealth is managed across time.

Advantage 1: Conflict-Free, Fiduciary Advice

In India's wealth management ecosystem, the dominant model is distribution-led. Mutual fund distributors, bank relationship managers, and insurance-linked advisers earn commissions and trail fees from the products they recommend. Even when well-intentioned, this creates structural bias toward higher-margin products over better-fit alternatives.

SEBI's IA Regulations address this directly: an RIA cannot simultaneously provide distribution services to the same client. Advice and distribution are structurally separated, and fees flow only from the client — no product manufacturer contributes to the adviser's revenue.

Research on conflicted advice from NBER found that broker-advised investors in retirement plans were systematically directed toward higher-fee funds, earning lower after-fee returns than self-directed investors. The mechanism isn't unique to the US — any compensation structure tied to product sales creates the same directional pull.

What this means in practice:

- Portfolios are constructed from the entire universe of regulated products, not a proprietary shelf

- Fund selection is driven by client suitability and risk profile, not distributor margin

- The adviser's incentive is client retention through performance and trust, not transaction volume

For UHNIs with large investable surpluses, even a 0.5–1% annual drag from misaligned product selection compounds significantly over 10–15 years. For NRIs navigating cross-border tax and investment decisions, independent guidance that carries no product incentive is especially critical.

iVentures Wealth, for example, operates exclusively on AUM-based or fixed advisory fees with no commissions, trail income, or product-linked compensation of any kind — a structure enforced by their SEBI RIA registration (INA000019026) and disclosed upfront in every client agreement.

Advantage 2: Holistic Coordination Across Investments, Tax, Estate, and Liquidity

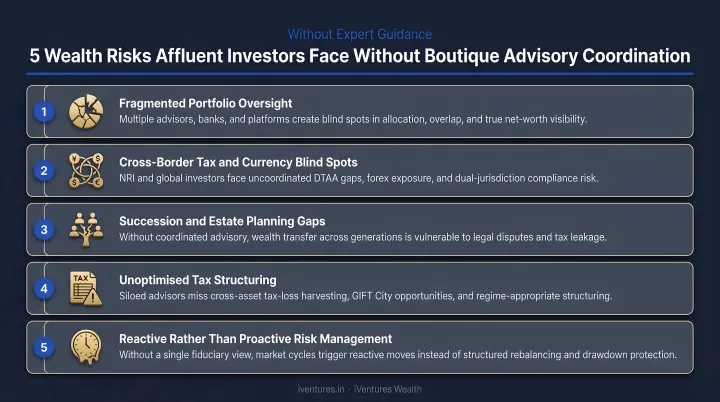

The most common structural failure in UHNI financial management isn't bad investment selection. It's fragmentation. A client's CA handles taxes, a bank RM manages the investment portfolio, and a lawyer drafts the estate plan — and none of the three speak to each other.

The cost of this fragmentation is invisible until a major event reveals it. A business exit, an inheritance, a market drawdown, a death in the family — each of these events triggers consequences across every financial domain simultaneously. When those domains are managed in silos, decisions in one area routinely undermine another.

In the boutique model, the adviser holds a complete picture: business income, personal investments, family liabilities, tax position, liquidity requirements, and succession intentions. This makes coordinated decision-making possible.

A concrete example from iVentures Wealth: When a first-generation promoter received ₹100+ crore from a business exit across multiple banks, the firm structured a simultaneous response across three domains:

- Investment strategy — a three-bucket framework (Safety, Stability, Growth) replacing scattered bank deposits

- Succession planning — a family trust established to ring-fence the corpus and define distribution rules for the spouse and children

- Tax and compliance — structured to ensure tax-efficient deployment across all vehicles

No single domain was addressed in isolation. The outcome was a coordinated family capital plan rather than a reactive deployment of liquidity.

The research supports why this coordination gap matters. Sundaram's 2024 India family office report found that over 20% of Indian family offices outsource tax planning, succession planning, and family trusts separately — and 56% cite attracting and retaining specialised talent as their biggest challenge. This fragmentation is the default, not the exception.

When this matters most: Business exits, inheritance events, retirement structuring, and family office formation — situations where decisions in one domain carry outsized consequences across others.

Advantage 3: Direct Access to Senior Expertise and Relationship Continuity

Relationship manager turnover is one of the least-discussed costs in institutional wealth management. When an RM leaves, their successor starts from scratch — reconstructing the client's risk profile, family dynamics, business complexity, and historical decisions. That handover cost is real, and it repeats every few years.

Boutique firms invert this. Clients work consistently with a small, senior team that accumulates deep institutional knowledge of their financial life over years and decades.

This continuity compounds in value in ways that are difficult to replicate:

- An adviser who has observed your risk behaviour across multiple market cycles can calibrate recommendations with precision no new-to-the-client adviser can match

- Family dynamics — trust structures, next-generation needs, spousal financial goals — are understood without re-explanation

- Complex multigenerational strategies can be designed and executed without the strategy reset that accompanies adviser transitions

Capgemini's 2025 World Wealth Report identifies relationship managers as critical for engaging next-generation HNWIs — and frames RM continuity and evolution as a core wealth retention capability. The implication is direct: relationship instability at the adviser level translates into wealth transfer risk at the client level.

For families managing multigenerational wealth, where philosophical consistency across generations is essential, and for founders whose financial complexity evolves rapidly with each liquidity or equity event, adviser continuity directly determines whether wealth strategies survive the transitions that matter most.

iVentures Wealth has built advisory relationships spanning two decades — with some families served since the firm's founding in 2005. The senior team includes founder Nirmal Bansal (formerly of Merrill Lynch and UCLA Anderson) and CFA charterholder Krishna Makhariya, whose combined tenure at the firm means clients aren't re-explaining their history every few years.

What You Risk Without a Boutique Approach

The costs of standardised, product-driven advisory are often invisible until a major event exposes them. By then, the damage is retrospective and difficult to reverse.

Concrete consequences affluent investors face without a boutique model:

- Generic portfolios built around the adviser's product shelf, not the client's tax situation, liquidity needs, or risk profile

- Advice shaped by product targets and distribution incentives rather than client outcomes

- No single point of accountability when financial domains are managed across separate, uncommunicating specialists

- Estate plans that haven't been updated to reflect current holdings or changed family circumstances

- Wealth transfer decisions made reactively — during a family crisis — rather than proactively with time to structure properly

Each of these gaps compounds the others. Missed tax optimisation, duplicated risk exposure across separately managed accounts, and misaligned succession structures build into structural vulnerabilities that are costly to unwind. Deloitte's 2024 research found 37% of wealthy families have no succession plan while 35% expect next-generation control within a decade — a planning gap that reflects precisely what siloed advice produces.

There's also a less visible cost. When a client deals with multiple advisers who don't communicate and receives conflicting guidance, the result is reactive, emotion-driven decision-making. This happens at precisely the moments when clear, coordinated counsel matters most — and when there's no single trusted relationship to call.

How to Choose the Right Boutique Wealth Management Firm

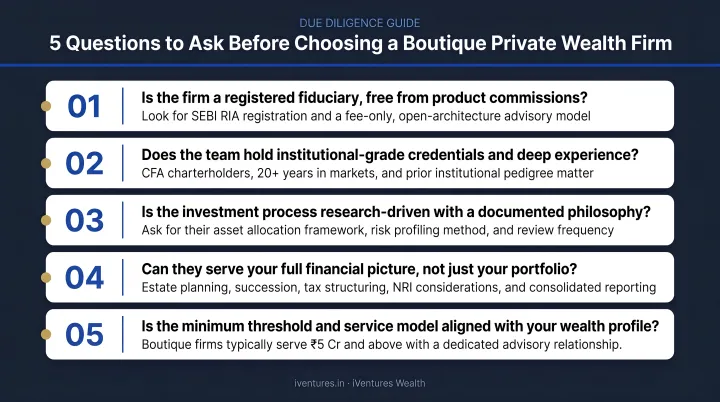

"Boutique" is not a regulated term in India. Any firm can use it. The meaningful differentiators to assess:

SEBI Registration as an Investment Adviser — Verify a current SEBI RIA registration number on SEBI's live register. This is the only designation that legally requires fiduciary conduct and prohibits commission-based product recommendations.

Advisory team credentials and stability — CFA charterholders, multi-decade track records, and low adviser turnover signal genuine expertise and continuity. Ask specifically how long the lead adviser has been with the firm.

Demonstrated breadth across domains — A boutique wealth firm should coordinate across investments, tax planning, estate and succession, and liquidity management. Ask how advice is integrated across these areas in practice, not just delivered in silos.

Key questions to ask a prospective firm:

- Who will be my primary adviser, and how long have they been with this firm?

- How does the firm earn its fees — does it receive any product-linked compensation?

- How many clients does each adviser manage?

- How will advice be coordinated across my tax, estate, and investment needs?

- What does the client relationship look like during market volatility or a major life event?

iVentures Wealth (SEBI RIA since 2010) manages ₹1,200+ Cr for 150+ affluent families, with fees structured as AUM-based or fixed retainer — no product-linked compensation. The firm is led by a CFA-led research team with no proprietary product incentives. Minimum investable asset thresholds: ₹5 Cr for NRIs/OCIs, ₹10 Cr for CXOs and professionals, ₹50 Cr for corporates, and ₹100 Cr for family businesses and family offices.

Conclusion

The value of boutique private wealth management lies in how its elements work together: conflict-free advice, holistic coordination, and relationship continuity — each reinforcing the others as wealth grows more complex over time.

At the UHNI level, wealth management is not primarily an investment problem. It is a coordination, continuity, and trust problem. The boutique model is structurally built to solve it:

- Smaller client base that allows genuine adviser attention

- Fiduciary obligation that removes product-driven conflicts

- Integrated domains covering investment, tax, succession, and estate

- Advisers who stay in the relationship long enough to understand it deeply

If your current advisory relationship is product-led, fragmented across specialists, or lacks a consistent senior adviser who holds your full financial picture — those are structural gaps, not service quality issues. Addressing them means reconsidering the model itself, not just the people within it.

Frequently Asked Questions

What is a boutique wealth management firm?

A boutique wealth management firm is a smaller, focused advisory practice serving a limited number of HNI and UHNI clients with personalised, integrated financial guidance. Unlike larger institutions, it prioritises relationship depth and customised strategy over product volume — with a senior team that maintains direct, long-term continuity with each client.

How is a boutique private wealth management firm different from a large bank's wealth division?

Boutique firms typically operate without proprietary product quotas or commission incentives, offer direct access to senior advisers, and serve a far smaller client base. This allows for genuinely tailored strategies rather than standardised templates, and eliminates the RM rotation that disrupts institutional advisory relationships.

Who should consider a boutique private wealth manager?

Boutique private wealth management is best suited for individuals and families whose financial lives have grown complex — UHNIs, founders, CEOs/CXOs, family offices, and NRIs who need coordinated guidance across investments, tax, estate planning, and liquidity, rather than isolated product advice from disconnected specialists.

Are boutique wealth management firms regulated in India?

"Boutique" is not a regulated term, but the most credible boutique advisers operate as SEBI-registered investment advisers (RIAs) — a designation that legally requires fiduciary conduct, prohibits commission-based recommendations, and mandates transparent fee disclosure. Verify any firm's RIA registration directly on SEBI's public register.

What services do boutique private wealth management firms typically offer?

Reputable boutique firms offer services across the full financial picture, coordinated rather than siloed:

- Investment strategy and portfolio management

- Tax planning and estate/succession planning

- Liquidity management and NRI/cross-border advisory

- Family office services and access to alternative investments

How do boutique wealth management firms charge for their services?

Reputable boutique firms, particularly SEBI-registered investment advisers, charge a transparent advisory fee — fixed, AUM-based, or a hybrid — with no commissions or distribution incentives. SEBI's framework caps AUM-based fees at 2.5% per annum per family, aligning the adviser's compensation directly with the client's interests rather than product sales.