This choice has real consequences. Emotional decision-making, tax drag from excessive churn, and the cognitive demands of tracking 20–30 stocks across sectors can meaningfully erode compounding at higher capital levels. The wrong structure doesn't just cost returns — it costs time and mental bandwidth you'd likely rather spend elsewhere.

This article compares Direct Equity and Portfolio Management Services (PMS) across cost, control, risk management, and investor fit — so you can make a deliberate, informed choice rather than defaulting to familiarity.

Key Takeaways

- Direct Equity gives full control and zero management fees — but all research and risk decisions fall on you

- PMS carries a SEBI-mandated ₹50 lakh minimum and delivers professionally managed, strategy-driven equity portfolios

- Cost structures diverge sharply — Direct Equity involves only transaction costs; PMS adds management and performance fees

- Tax rules are the same for both, but PMS generates more transactions, creating more complex capital gains reporting

- The right choice turns on your investible surplus, time availability, market expertise, and behavioral discipline

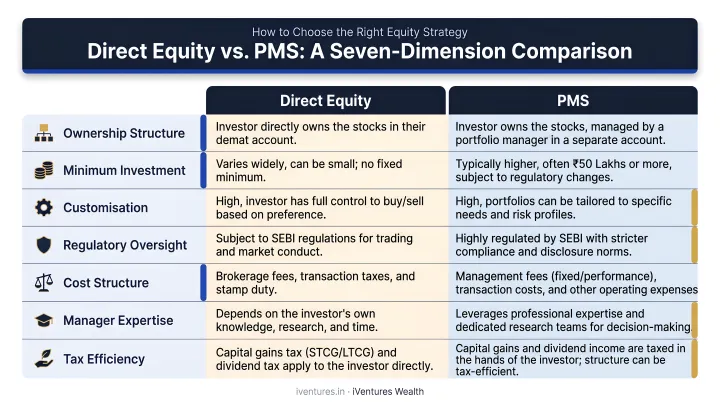

Direct Equity vs PMS: Quick Comparison

Here's how the two routes compare across the dimensions that matter most to HNIs and serious investors.

| Dimension | Direct Equity | PMS |

|---|---|---|

| Minimum Investment | No minimum — start with a single share | ₹50 lakh (SEBI-mandated) |

| Who Manages | The investor — full self-management | SEBI-registered portfolio manager |

| Cost Structure | Brokerage, STT, exchange charges only | Management fee + optional performance fee |

| Risk Management | Depends on individual discipline | Systematic — position sizing, sector limits, rebalancing |

| Tax Reporting | Simpler, fewer transactions | Higher transaction volume; typically requires CA assistance |

| Ownership Structure | Direct — shares in your demat account | Direct — securities held in your own demat account |

| Exit Flexibility | Sell on any trading day | Exit load applies in years 1–3 (SEBI-capped) |

What Is Direct Equity?

Direct equity means purchasing shares of individual companies through a personal demat and trading account. Every decision — stock selection, entry and exit timing, portfolio weightage — belongs entirely to you. No intermediary, no mandate, no fees beyond normal transaction costs.

The appeal is straightforward: zero management fees, complete transparency, direct ownership of dividends and capital gains, and the freedom to act on conviction without waiting for approvals.

Who It Works For

Direct equity suits investors who can genuinely commit the time and focus that consistent portfolio management demands. Tracking earnings results, sector rotations, regulatory changes, and macro developments across even 15–20 stocks is a substantive ongoing workload — one that scales as the portfolio grows.

It works particularly well when an investor has deep sector expertise. A founder in the healthcare space tracking pharmaceutical and diagnostic stocks, for instance, brings genuine informational depth that's difficult to replicate from the outside.

The Real Limitation

The structural risk in direct equity isn't stock selection — it's behavior. Research on Indian stock market investors confirms that overconfidence bias operates across market phases, leading investors to overtrade during rallies and hold concentrated positions beyond reasonable risk levels.

The SEBI Investor Survey 2025 found that 50% of investors have low market knowledge, yet active participation continues. Without a structured risk framework, direct equity portfolios are vulnerable to:

- Overconcentration in familiar names

- Panic selling during market corrections

- Overtrading that erodes long-term returns

Scale amplifies these risks further. At ₹2–5 crore spread across multiple sectors, consistent portfolio management demands the kind of institutional-grade research most individuals cannot sustain on their own.

What Is PMS?

Portfolio Management Services is a professionally managed equity arrangement where a SEBI-registered portfolio manager invests on the client's behalf through a structured, mandate-driven strategy. Unlike mutual funds, each PMS client holds securities directly in their own demat account — the portfolio manager operates at the client level, not through a pooled vehicle.

The Three Types

| Type | How It Works | Best For |

|---|---|---|

| Discretionary | Manager buys/sells within mandate — client is not involved in each trade | Busy professionals who want full delegation |

| Non-Discretionary | Manager recommends; client approves each trade | Investors who want oversight but professional input |

| Advisory | Manager advises; client executes | Closest to direct investing, with professional guidance |

Discretionary PMS is by far the most common and practical choice for HNIs and CXOs who want equity exposure without the day-to-day operational burden. That operational structure also explains why SEBI has set a meaningful entry threshold for this category.

Why ₹50 Lakhs?

SEBI's working group raised the PMS minimum from ₹25 lakh to ₹50 lakh in 2019, partly because the Nifty had more than doubled and inflation had risen significantly since the prior threshold was set. The intent is clear: PMS is designed for investors with sufficient financial capacity and risk awareness to understand concentrated, actively managed equity strategies.

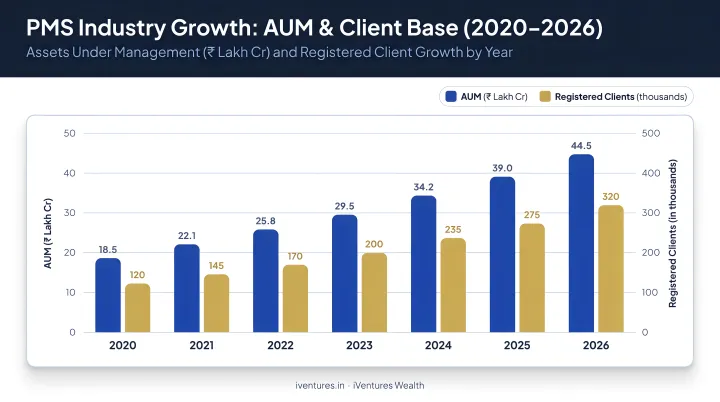

PMS Growth in India

The numbers tell a clear story about rising demand among affluent investors:

- March 2020: ₹18.1 lakh crore total AUM, 1.67 lakh clients

- March 2023: ₹27.8 lakh crore AUM, 1.44 lakh clients

- March 2025: ₹37.8 lakh crore AUM, 1.99 lakh clients

- April 2026: ₹42.4 lakh crore AUM, 2.17 lakh clients

SEBI's April 2026 data also shows 520 registered portfolio managers, up from 336 in 2020. That said, a large portion of total PMS AUM comes from institutional mandates (including EPFO/PFs), so the HNI equity PMS segment is a subset of the headline figure.

What PMS Handles For You

Under a discretionary arrangement, the portfolio manager covers:

- Research and stock selection within the mandate

- Trade execution and position sizing

- Rebalancing based on predefined protocols

- Corporate actions (dividends, buybacks, rights issues)

- Capital gains statements and consolidated reporting

For busy entrepreneurs, CXOs, or family office principals, this operational handoff is often as valuable as the investment strategy itself.

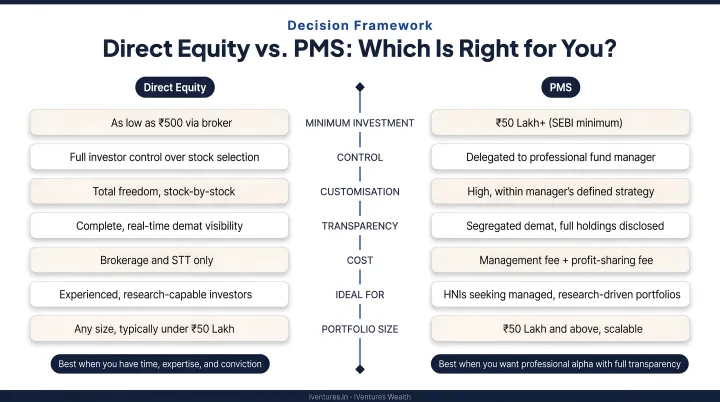

Which Route Is Right for You?

Neither option is inherently superior. The right choice depends on four variables: investible surplus, time availability, market expertise, and behavioral discipline.

Choose Direct Equity If:

- Your investible surplus is under ₹50 lakhs (PMS isn't accessible below this threshold)

- You have deep sector knowledge and can dedicate consistent time to research and monitoring

- You have the emotional discipline to hold through 20–30% drawdowns without reactive selling

- You prefer complete control over every position and allocation decision

Choose PMS If:

- You have ₹50 lakhs or more in investible equity surplus

- You're a business owner, CXO, or professional with limited time for active portfolio management

- You want access to a structured, strategy-driven equity mandate with defined risk protocols

- You prefer consolidated reporting and professional handling of corporate events and rebalancing

The Hybrid Approach

Many experienced investors with larger portfolios don't treat this as a binary choice. A common structure is running a direct equity sleeve for high-conviction sector bets — areas where the investor has genuine informational edge — while allocating a core portion to PMS for disciplined, strategy-driven compounding.

For a surgeon who understands healthcare dynamics deeply, maintaining a 10–15 stock direct equity sleeve in that sector alongside a discretionary PMS mandate for broader market exposure is a coherent, deliberate architecture — purpose-built, not portfolio scatter.

A Note on Costs and Tax

Before committing capital, understanding the cost and tax mechanics of each route matters as much as the strategy itself.

PMS fees vary by provider. SEBI's Master Circular caps operating expenses (excluding brokerage) at 0.50% p.a., and regulates exit loads as follows:

| Period | Maximum Exit Load |

|---|---|

| Year 1 | 3% |

| Year 2 | 2% |

| Year 3 | 1% |

| After Year 3 | Nil |

Management and performance fee structures are disclosed in each provider's disclosure document.

On taxation, both Direct Equity and PMS are subject to the same capital gains rules for listed equity: STCG at 20% and LTCG at 12.5% (with a ₹1.25 lakh annual exemption). The difference is complexity — PMS portfolios often generate 50+ transactions annually, making capital gains statements significantly more involved than a typical self-managed direct equity account.

For investors evaluating this decision with a substantial corpus, an independent, SEBI-registered advisor can provide objective guidance on structuring the equity allocation without conflicts of interest. iVentures Wealth operates on a fee-only model — no product commissions, no distributor trails. Its open-architecture approach covers PMS selection across the full universe of SEBI-registered providers, evaluated on mandate fit, risk-adjusted track record, and fee efficiency.

Frequently Asked Questions

What is direct equity?

Direct equity means buying and holding shares of individual companies through a personal demat account. The investor makes all decisions — stock selection, timing, and portfolio composition — without any professional intermediary or structured mandate.

Is PMS better than a mutual fund?

Neither is universally better — they serve different investor profiles. PMS offers individual demat-level ownership, greater customisation, and mandates tailored to HNIs with ₹50 lakh+ surplus. Mutual funds pool capital and are accessible at any investment level, making them the practical choice for smaller ticket sizes or investors who prefer diversified, pooled exposure.

What is the minimum investment required for PMS in India?

SEBI mandates a minimum of ₹50 lakhs to invest in PMS in India. This applies uniformly across all portfolio managers and strategies registered under SEBI's PMS regulations.

How are taxes handled differently in PMS versus direct equity?

Both are subject to the same equity capital gains tax — STCG at 20% and LTCG at 12.5%. The difference is reporting complexity: PMS portfolios typically involve a much higher volume of transactions annually, making capital gains statements more involved and requiring CA assistance or specialised software for ITR filing.

Can I exit PMS as easily as selling stocks in direct equity?

Direct equity is highly liquid — you can sell on any trading day. PMS carries exit loads for early withdrawals, capped by SEBI at 3% in year one, 2% in year two, and 1% in year three. After three years, no exit load applies. PMS is better suited to investors with a long-term capital commitment of at least three years.

Who should not invest in PMS?

PMS may not suit investors below the ₹50 lakh threshold, those who want full personal control over every decision, or those with a short time horizon. Direct equity or mutual funds are a more appropriate and cost-efficient fit for these situations.

Direct equity suits investors with genuine research capability, dedicated time, and the discipline to stay rational through volatility. PMS suits those who want a professionally managed, directly-held equity portfolio without the overhead of running it themselves.

The right structure depends on your investible surplus, tax position, and how involved you want to be. iVentures Wealth's fiduciary advisory team can assess whether Direct Equity, PMS, or a combination fits your specific situation — without any product bias.