Introduction

Professional athletes face one of the most unusual financial situations imaginable: earning in five to seven years what most people spend an entire career accumulating, then living on that wealth for another 40 to 50 years.

The numbers are sobering. A 2009 Sports Illustrated investigation reported that roughly 60% of former NBA players were broke within five years of retirement, and 78% of former NFL players faced financial stress or bankruptcy within two years of leaving the game. A more rigorous NBER working paper studying 2,016 NFL players found bankruptcy filing rates reaching 15.7% within 12 years post-retirement — still a striking figure for a group that earned far above average.

For Indian athletes, no comparable public dataset exists. Yet the government's PDUNWFS scheme — which provides financial relief to retired sportspersons earning below ₹8 lakh annually — signals that financial hardship after competitive careers is not rare, even in India.

That pattern makes structured financial planning non-negotiable. This guide covers six pillars of athlete wealth management: understanding the unique challenges, building the right advisory team, managing cash flow and taxes, investing strategically, protecting wealth through insurance, and planning your estate.

Key Takeaways

- Athletic careers average 3–7 years, meaning one short window must fund 40–50 years of post-career life

- Successful wealth management requires a coordinated team, not a single advisor

- Save at least 40% of post-tax income during peak earning years

- Follow a three-bucket investment model: build a secure foundation before pursuing higher returns

- Estate planning and insurance are foundational, not afterthoughts

Why Athlete Finances Are Different

The Sudden Wealth Problem

Most professionals develop money management skills gradually — earning ₹5 lakh, then ₹15 lakh, then ₹50 lakh over a decade. Athletes skip that entire learning curve. A first IPL contract, a major kabaddi franchise deal, or a national team retainership can vault a 21-year-old from limited means to multi-crore income almost overnight.

That compressed timeline creates real psychological risk. Family members expect financial support. Teammates model high-consumption lifestyles. Opportunistic contacts arrive with investment deals that rarely survive scrutiny.

The result: athletes often spend at peak-income levels before building any financial security buffer.

The Compressed Earning Window

The average NFL career lasts 3.3 years according to ESPN. The average NBA career runs about 4.5 years. Cricket careers are longer, but even at the international level, most players have a meaningful peak earning window of five to ten years — after which IPL contracts, endorsements, and national retainerships begin declining.

Consider the contrast: a typical professional has 30 to 35 working years to build wealth incrementally. Athletes must generate, save, and invest enough in their peak window to fund the rest of their lives — then manage that corpus for decades with no new employment income.

Pressures Unique to Athletes

- Public income visibility — BCCI publishes annual retainership grades openly, making athlete earnings more visible than nearly any other profession

- Family financial expectations — extended family often assumes proximity to a high-earning athlete translates to shared entitlement

- Agent and manager conflicts — advisors paid on commissions have structural incentives misaligned with the athlete's long-term interests

- High-risk business opportunities — athlete losses in restaurants, music labels, car dealerships, and startups are well-documented globally; individual cases have involved losses equivalent to ₹100 crore or more in ventures that collapsed within a few years

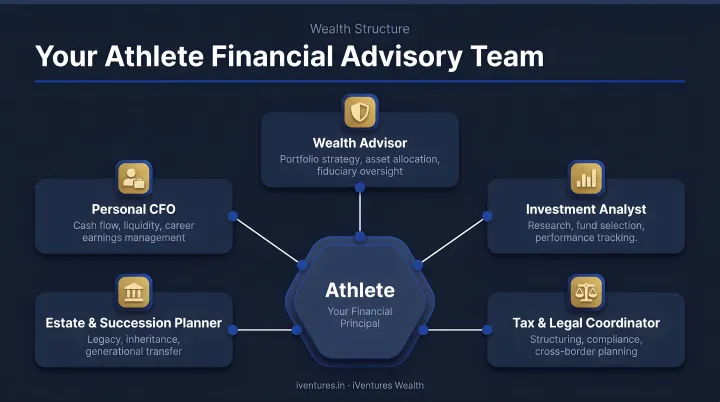

Building Your Financial Team

Who Should Be on Your Team

Athlete wealth management requires at least five specialists operating as a coordinated unit:

| Role | Primary Function |

|---|---|

| Wealth/Financial Advisor | Central coordinator across all financial decisions |

| Chartered Accountant | Tax planning, ITR filing, advance tax management |

| General Insurance Advisor | Home, auto, umbrella liability coverage |

| Life/Disability Insurance Specialist | Career-ending disability, income protection |

| Estate Planning Attorney | Will, trust structuring, power of attorney |

The wealth advisor's job is not just portfolio management — it's ensuring these specialists talk to each other and that no gap exists between them. iVentures Wealth, for instance, operates explicitly as a coordinating partner, working alongside external CAs and legal advisors while maintaining the central view of overall wealth strategy.

What to Look for in an Advisor

Athletes are especially vulnerable to bad actors. Globally, high-earning athletes have lost hundreds of crores to advisors who prioritised commissions over client interests — mismanagement that often goes undetected until the playing career is already over.

Evaluate any financial professional against these five criteria:

- Relevant experience — have they worked with high-income, short-career professionals or HNIs?

- Verified credentials — CFA, CFP, or equivalent designations with a clean regulatory record

- Conflict-free model — a SEBI-registered investment adviser operating as a fiduciary is legally obligated to act in your interest, not earn commissions on products

- Specialised service — a generalist managing hundreds of retail accounts cannot provide the personalised attention high-income athletes need

- Communication fit — responsiveness matters when you're in training camp or competing abroad

A SEBI-registered RIA and a commission-based distributor operate under fundamentally different rules. An RIA like iVentures Wealth (SEBI Registration INA000019026) cannot accept trail income or product kickbacks — so every recommendation reflects suitability, not a sales target. A commission-based advisor, by contrast, earns more when they place you in certain products. That conflict rarely gets disclosed upfront.

Cash Flow, Budgeting, and Tax Planning

Building a Budget Around Your True Lifestyle Cost

The most common budgeting mistake athletes make is conflating two types of spending:

- Lifestyle purchases — recurring commitments that must be sustained indefinitely (a home, staff, vehicles, club memberships)

- Reward purchases — one-time splurges tied to a specific milestone (a celebratory trip, a luxury item)

Athletes who blur this line end up structuring a permanent lifestyle around peak-income spending. Post-career, that lifestyle becomes unsustainable.

Instead, work backward from the "cost of being you." Calculate your total annual lifestyle cost, then determine how large a corpus is needed to generate that income indefinitely through investment returns. This gives you a real savings target — a specific number tied to your life, not a generic percentage.

A reasonable target during peak earning years: save at least 40% of post-tax income. This is not aggressive by the standards of your earning window — it is the minimum that gives you options.

Tax Planning Strategies Athletes Must Know

Athletes typically have two distinct income streams, each with different tax treatment:

- Contract/retainership income — taxed as employment or professional income under the applicable slab rates (under India's new regime for AY 2026-27, the top rate is 30% above ₹24 lakh, with surcharge reaching 25% on incomes above ₹2 crore)

- Off-field income — endorsements, brand deals, appearance fees, and prize money each carry different classification and deduction possibilities

Specific strategies worth implementing:

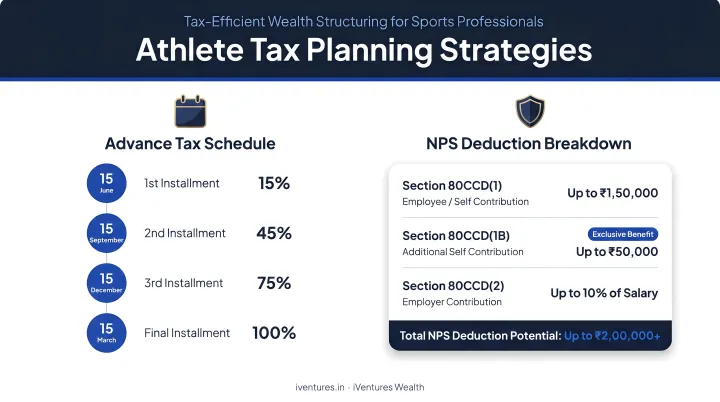

- Advance tax management — Section 208 requires advance tax when annual liability exceeds ₹10,000. The schedule is 15% by June 15, 45% by September 15, 75% by December 15, and 100% by March 15. Missing these triggers 1% monthly interest under Sections 234B and 234C

- NPS contributions — self-employed individuals can deduct up to 20% of gross income under Section 80CCD(1), plus an additional ₹50,000 under Section 80CCD(1B), building retirement savings while reducing current tax

- Section 80G charitable giving — structured donations to approved institutions generate deductions while creating genuine social impact

- Prize money classification — Section 115BB taxes winnings from "games of any sort" at a flat 30% with no deductions permitted; not all athlete payments fall under this provision, but misclassification is costly

Multi-Jurisdiction Tax Obligations

The domestic strategies above cover most athletes' immediate needs. For those competing internationally, a separate layer of planning applies.

Athletes earning income abroad may face tax obligations in multiple countries simultaneously. India's DTAA with the US (Article 18), for example, allows athletic income earned in the US to be taxed there, with corresponding relief available in India — preventing double taxation on the same income. If you compete internationally on a regular basis, DTAA structuring warrants dedicated attention from an adviser familiar with cross-border income treatment.

Sachin Tendulkar's well-documented ITAT case — where commercial and advertising income was accepted as artistic performance income under Section 80RR, saving approximately ₹58 lakh in tax — shows how income classification decisions can produce significant, legally defensible tax outcomes. The catch: these positions require expert structuring and cannot be reverse-engineered after filing.

How Athletes Should Invest

The Three-Bucket Investment Model

The bucket framework organises your portfolio by purpose, not just by asset class:

Bucket 1 — War Chest (Safety)

- 5–7 years of lifestyle expenses

- High-quality fixed income, liquid debt funds, short-duration bonds

- Purpose: financial stability regardless of what happens to income or markets

- Yield benchmark: liquid funds have averaged approximately 6–6.8% annualised in recent years

Bucket 2 — Growth Strategy

- Equities, balanced funds, real estate-linked instruments

- 8–15 year horizon

- Purpose: building lasting wealth through compounding

Bucket 3 — Aspirational

- AIFs, PMS, private equity, private credit, business ventures

- Only accessible once Buckets 1 and 2 are fully funded

- SEBI mandates minimum ₹50 lakh for PMS and ₹1 crore for AIF investments

The most important rule: never move to Bucket 3 before Buckets 1 and 2 are secure. The athletes who lost their wealth overwhelmingly lost it here — a restaurant that failed, a startup that burned cash, a real estate development that stalled.

The pattern repeats across geographies. Antoine Walker earned over USD $100 million and filed for bankruptcy. Deuce McAllister's car dealership collapsed, leaving creditors owed USD $6.6 million. In each case, Bucket 3 bets were made before the foundation was in place.

The Time Horizon Paradox for Athletes

Conventional wisdom says young investors can tolerate more risk because they have decades to recover from losses. For athletes, this logic only partially applies.

If a career-ending injury occurs at 28 — and 67% of former NCAA Division I athletes reported sustaining a major injury during their careers — the portfolio may need to generate income within months, not decades. Early portfolios should prioritise safety, shifting toward growth as financial security is established.

None of this diminishes the opportunity. Compounding remains an athlete's greatest long-term asset — the caution simply determines when and how aggressively to pursue it. ₹1 crore invested at the Nifty 50's historical 10-year return of 12.55% grows to approximately ₹113 crore over 40 years. An athlete who invests wisely at 22 and retires at 30 has four full decades of compounding ahead — the same runway as someone starting a conventional career. The difference is that it must be secured in a far shorter earning window.

iVentures Wealth's CFA-led team structures portfolios using this bucket-based approach, with consolidated reporting across mutual funds, equities, bonds, PMS, and AIFs through the Wealth Monitor App — giving clients a clear view of their full financial position at any point.

Insurance and Estate Planning

The Insurance Stack Every Athlete Needs

Property and casualty coverage:

- Comprehensive motor insurance for all vehicles

- Home insurance for owned property

- Renters/temporary accommodation insurance during tournament travel

- Umbrella liability coverage — athletes with high public profiles face elevated third-party liability risk that standard policies do not cover

Specialty athlete insurance:

- Permanent Total Disability (PTD) — covers career-ending disability from accident or illness; under IRDAI-governed policy definitions, PTD means the insured is permanently and absolutely disabled from engaging in any employment

- Loss of future value coverage — protects against the income loss from a career-altering injury that reduces earning capacity even without ending competition

- Specific injury policies — can be structured to protect against injury to a particular body part critical to performance

These policies are highly customised. Work only with a specialist who has no financial incentive to oversell coverage.

Insurance protects your earning capacity. Estate planning protects what you build with it.

Estate Planning Is Not Just for Retirees

A 24-year-old with a ₹5 crore contract needs an estate plan. Not because death is imminent — because assets must be protected and distributed correctly if anything goes wrong.

A proper estate plan for an athlete includes:

- A will — clearly documenting asset distribution preferences under the Indian Succession Act, 1925

- A revocable private trust — holds assets on your behalf, controls distribution on death, avoids public probate, and provides privacy and liability protection; governed by the Indian Trusts Act, 1882

- Medical and financial power of attorney — designates someone to make decisions if you are incapacitated

- Nominee alignment — ensuring all financial accounts, insurance policies, and investment holdings have correctly designated and updated nominees

The most common mistake: documents are drafted and signed, but assets are never retitled into the trust. This makes those documents legally meaningless. Every asset must be correctly titled in the trust's name, not just referenced in a document.

India currently has no estate duty — the tax was abolished in 1985 — but that does not make estate planning optional. Succession disputes, probate delays, and family conflicts over undocumented assets remain real risks. Careful planning reduces all three by establishing documented intent and ensuring assets are correctly structured from the outset. iVentures Wealth works with athletes on the wealth structuring and asset alignment side — coordinating with external legal advisors to ensure the financial architecture supports whatever estate documents are put in place.

Frequently Asked Questions

How do professional athletes manage their money?

Successful athletes build a coordinated team — wealth advisor, tax professional, insurance specialist, and estate planning attorney — and follow a structured plan across cash flow management, tax planning, diversified investing, and risk protection. The most important step is starting before the first contract is spent.

Which is better for professional athletes: CFP or CPWA?

Both credentials have merit. A CFP covers comprehensive personal financial planning; a CPWA specialises in advanced estate transfer, tax strategy, and family wealth dynamics for HNW clients. What matters more than the designation is whether the advisor has direct experience with high-income, short-career clients and operates as a conflict-free fiduciary.

Is paying advisory fees to a financial advisor worth it for professional athletes?

For athletes managing sudden, large wealth with complex tax, insurance, and investment needs, a qualified fiduciary advisor typically generates far more value than their fee — through tax savings, portfolio optimisation, and costly mistakes avoided. Athletes who go without structured advisory support routinely pay more through avoidable tax leakage and poor investment decisions than any advisory fee would cost.

What should professional athletes do with their first big contract?

Immediately assemble a financial team, establish a budget before any significant spending, set aside advance tax (typically 30–40% depending on income level), and build an emergency fund before structured investing begins. Career spans are short — the financial runway must be built in the early years when income is highest.

When should a professional athlete start financial planning?

Before signing the first professional contract — but the second best time is today. Early planning allows compounding to work longer, bad habits to be avoided from the start, and tax strategies to be implemented during the highest-earning years.

What are the biggest financial mistakes professional athletes make?

Lifestyle inflation that outpaces savings, investing in businesses or ventures without understanding them, trusting advisors with conflicts of interest, failing to plan for advance tax obligations, and neglecting estate planning until assets are already scattered and complex.